Re-balance Cycle Reminder All MyPlanIQ’s newsletters are archived here.

Regular AAC (Asset Allocation Composite), SAA and TAA portfolios are always rebalanced on the first trading day of a month. the next re-balance will be on Wednesday November 1, 2023.

As a reminder to expert users: advanced portfolios are still re-balanced based on their original re-balance schedules and they are not the same as those used in Strategic and Tactical Asset Allocation (SAA and TAA) portfolios of a plan.

Maximizing Your Retirement Income: The 4% Withdrawal Rule & Retirement Withdrawal Calculator

Retirement planning can be daunting, especially when it comes to determining how much money you can withdraw from your investment portfolio each year without running out of funds. This is where the concept of safe retirement withdrawal rates comes into play. But what exactly is a safe withdrawal rate, and how can you ensure your retirement income will last for at least 30 years?

At MyPlanIQ, we have studied and monitored several popular safe retirement withdrawal rate strategies. In this newsletter, we will first revisit this concept, review the latest data and then introduce our retirement withdrawal calculator that can be very useful for those who like to explore various strategies on various funds and portfolios in various periods.

The Origins of the 4% Rule

A safe annual retirement withdrawal rate refers to the amount of money you can withdraw from your investment portfolio each year without depleting your funds too quickly. In general, a safe withdrawal rate is one that can guarantee income for at least 30 years. This assumption is based on the income being purely from an investment portfolio that includes stocks, bonds, and/or real estate.

The concept of a safe retirement withdrawal rate is not new. In fact, it dates back to the early 1990s when financial planner William P. Bengen introduced what has become known as the “4% rule.” This rule suggests that retirees can safely withdraw 4% of their investment portfolio each year without running out of money for at least 30 years.

The 4% rule is based on historical market data and assumes a portfolio mix of 50% stocks and 50% bonds. Bengen conducted extensive research on stock and bond returns over the past century and found that a 4% withdrawal rate would have provided sufficient income for a 30-year retirement period.

A more challenging objective is to determine an annual withdrawal rate that not only guarantees a stable income for at least 30 years but also maintains the purchasing power of the investments after 30 years, accounting for inflation. While this is a more ambitious target, it is a desirable option for many individuals who aim to leave behind an estate that retains its original value. A even more ambitious goal is to be able to safely spend your retirement fund perpetually for more than 30 years.

Retirement withdrawal strategies or rules

Here is the synopsis of several retirement withdrawal strategies:

- The 4% retirement withdrawal strategy: at the end of every calendar year, withdraw inflation-adjusted 4% for the next year spending. Inflation-adjusted 4% means for the first year, you start at 4%, and then the next year’s withdrawal rate would be adjusted by previous_year_withdrawal_rate*(1+inflation_last_12_month). Inflation is normally defined as using the Federal Reserve CPI for All Urban Consumers data. This approach may provide a consistent income stream, but it does not account for fluctuations in market returns.

- Floor and ceiling withdrawal strategy: the withdrawal amount is calculated as a percentage of the portfolio total value. The withdrawal amount is allowed to rise or fall with the performance of the portfolio. However, the withdrawal will neither fall below a floor nor rise above a ceiling. In Journal of Financial Planning. May 2001 issue, Bengen suggested this strategy to accommodate more volatile portfolio fluctuations.

- Sensible withdrawal strategy: it suggests withdraws at least at a floor percent. But in a good year when investments grow much higher than the inflation, it can allow to withdraw more by setting up a cap such as half (0.5 or 50%) of the amount from the original accumulated floor amount. See Sensible Withdrawal strategy for more details.

Empirical Data Based on MyPlanIQ’s Portfolio Data

While the 4% rule has been widely accepted as a standard for safe retirement withdrawals, there are some who question its validity in today’s market conditions. To address this concern, MyPlanIQ has monitored several portfolios for more than a decade to see how effective these strategies have performed.

MyPlanIQ’s study found that the 4% rule is still a valid guideline for retirement withdrawals, but the actual safe withdrawal rate may vary based on individual portfolio allocation and market conditions. For example, portfolios with a higher allocation to stocks may have a higher safe withdrawal rate than those with a higher allocation to bonds since 2000 as in general, stocks have done well.

- Period: from 12/31/1990 (for VBINX, 12/31/1992) to 12/30/2022

| Ticker/Portfolio Name | Total cumulative withdrawal | Last annual withdrawal | Remaining Value |

|---|---|---|---|

| P Vanguard 500 VBINX Sensible Withdraw 4% No Extra Withdrawal | 182,398 | 8,672 | 220,488 |

| P Vanguard 500 VFINX Sensible Withdraw 4% No Extra Withdrawal | 208,363 | 9,484 | 1,228,190 |

| P Vanguard 500 VFINX Sensible Withdraw 4% | 428,339 | 9,484 | 164,732 |

A few comments:

- The aggressive Sensible Withdraw portfolio has had more than double cumulative withdrawal amount, compared with the pure 4% withdrawal one. However, this comes with a big price: their remaining values (on 12/30/2022) are way too different: the conservative one has 7.4 times more value than the aggressive one! So a good saving goes a long way: double spending or 7 times more wealth at the end!

- The balanced one (VBINX) has a comparable spending (withdrawal) amount, compared with VFINX. However, its remaining value is also much lower than the VFINX one.

Certainly, it’s important to note that the data presented above is significantly influenced by past market conditions. Given that our present bull market has extended beyond 14 years, doubling the typical length of a 7-year bull/bear full market cycle, we would like to advise readers to approach the most recent data with caution. What becomes more intriguing is the examination of data commencing from a bull market peak. To facilitate this, we can utilize MyPlanIQ’s recently introduced retirement withdrawal calculator.

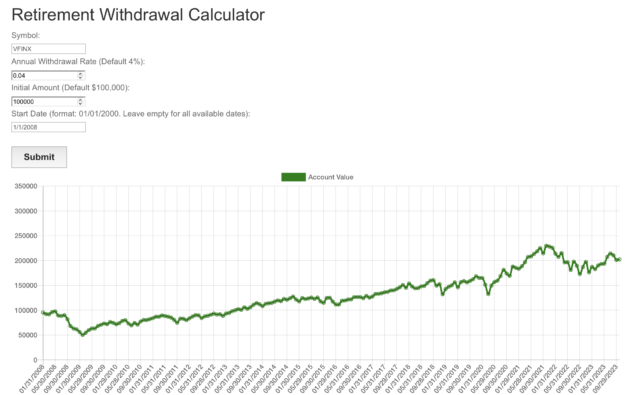

Retirement Withdrawal Calculator

The Retirement Withdrawal Calculator calculates or simulates each year’s withdrawal amount and how much remained in an investment for an annual withdrawal rate that’s inflation adjusted. It can take a fund (ETF or mutual fund) symbol (such as SPY for S&P 500 index ETF) desired. You can also enter a stock symbol (for example, a dividend paying stock such as VZ (Verizon Communication) or XOM (Exxon Mobile). Furthermore, you can even enter a MyPlanIQ portfolio symbol in the format of P_xxxxx where xxxxx is the portfolio ID. For example, P_46880 represents ‘Schwab Total Return Bond‘ portfolio (you can find its ID in its URL https://www.myplaniq.com/invest/port/?ID=46880). In essence, the calculator works for any stock, ETF, mutual fund or even a MyPlanIQ portfolio.

Users have the option to experiment with various settings, such as the annual withdrawal rate (with a default setting of 4%) and the starting date. For instance, if we wish to assess how a fund would perform if we initiated our retirement spending at the height of a bull market, we can specify the starting date for comparison purposes. Below, you’ll find two distinct outputs corresponding to two different starting dates for the S&P 500 fund VFINX. We also encourage users to explore other balanced funds (such as the 60/40 Vanguard balanced fund VBINX) or portfolios.

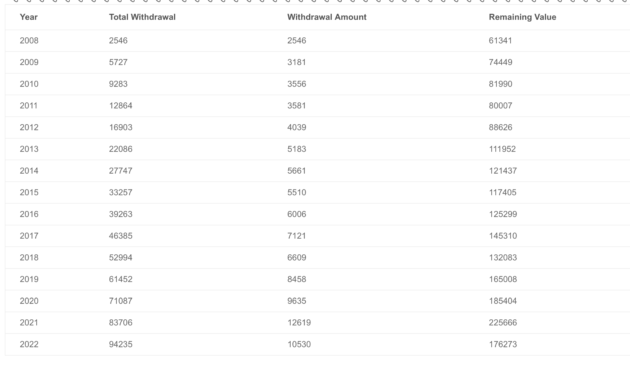

The first one starts retirement withdrawal in 1/1/2008 (a bull market high):

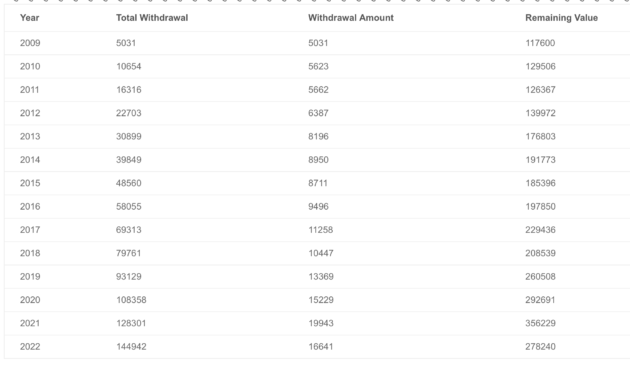

The second one starts retirement withdrawal in 1/1/2009 (a bear market low):

A few observations:

- Starting from a bull market peak (2008), even though it has one more year to spend, its cumulative withdrawal amount at the end of 2022 stood at $94k, compared with $145K for the one starting in 1/1/2009! So retiring in a bull market peak can severely affect your spending!

- Similarly, notice the withdrawal in year 2008: it had only $2.5k. This is because the $100K portfolio at the beginning of 2008 became only $63K at the end of 2008 because of the drawdown or loss of VFINX (S&P 500) in that year! So this retiree must have felt a big squeeze in that year as it really only could spend 2.5% of its money that year (from the beginning $100k point of view)! In fact, its annual withdrawal never caught up with the one starting on 1/1/2009, usually 40% or so lower.

- The final wealth is also very different: the bull market one is about 63% or 2/3 of the bear market one.

The above study shows that retiring at the peak of a bull market turns out to be the worst time to retire. This is somewhat counter intuitive.

Conclusion

Retirement planning requires careful consideration of many factors, including your investment portfolio, market conditions, and retirement goals. A safe retirement withdrawal rate is an essential component of retirement planning and can help ensure your income lasts for at least 30 years. While the 4% rule is a useful guideline, it is important to consider other withdrawal rules and compare and contrast. Furthermore, MyPlanIQ Retirement Withdrawal Calculator can be used to test out various scenarios to better understand how a withdrawal strategy behaves in both good and bad market cycles.

Market Overview

As mentioned in our previous newsletter two weeks ago, the ongoing increase in yields of long-term Treasury bonds is certainly a cause for concern. Currently, the 10-year Treasury yield stands at 4.78%, which is notably higher than the 4.56% observed two weeks ago. The persistence of these elevated long-term interest rates is exerting significant pressure on business spending and overall growth.

Other notable developments:

- the iShares 20+ Year Treasury Bond (TLT) recently suffered one of its most substantial drawdowns from its peak, reaching a maximum drawdown of 42% as of last month (and including this month, its drawdown is now at 44.2%)!

- The utility sector stocks have had their worst year relative to the S&P 500 index since 1999.

- Year to date, all of the ‘safe’ S&P sectors have had negative returns:

| Ticker/Portfolio Name | YTD Return** |

1Yr AR | 3Yr AR | 5Yr AR | 10Yr AR |

|---|---|---|---|---|---|

| XLP (Consumer Staples Select Sector SPDR ETF) | -7.5% | 3.6% | 5.2% | 8.1% | 8.5% |

| XLU (Utilities Select Sector SPDR ETF) | -15.5% | -7.0% | 1.8% | 5.4% | 8.4% |

| XLV (Health Care Select Sector SPDR ETF) | -2.3% | 6.8% | 9.8% | 9.1% | 11.9% |

| XLK (Technology Select Sector SPDR ETF) | 36.6% | 35.8% | 14.7% | 19.5% | 19.8% |

Currently, we observe two potential scenarios: either the economy will persist in its growth despite the prevailing high-cost environment, or interest rates will need to rapidly decrease for the markets to achieve stability. It’s important to emphasize that even in the event of continued economic growth, the current stock valuations are significantly less appealing compared to fixed income and cash, both of which are currently offering much higher yields. If you have the opportunity to secure a risk-free return of 5% or more annually, it might not justify the risk associated with stocks, which could potentially yield low or even negative returns in the upcoming years.

As always, we claim no crystal ball and we call for staying the course which is guided by the well defined and sound strategic and tactical strategies:

- For strategic allocation (buy and hold) investors, ignore the current market behavior. Remember, as we have emphasized numerous times, when you choose and commit to a strategic portfolio, you essentially know and commit that your investment horizon (or the time you need to utilize this capital) is 20 years, preferably much longer, given the current high valuation. As we pointed out, if your investments are those diversified (index) funds such as an S&P 500 index fund (VFINX, for example), you know your money is in some solid ‘business’ that eventually (20 years later and preferably many more years later) will deliver some reasonable returns. As long as you are comfortable with this thesis, you should sit tight and forget about the current gyration.

- For tactical investors, again, you have to ignore the current market noise. Furthermore, you should follow your strategy rigorously, especially during this time. Human emotion, both optimistic and pessimistic, and human desire, both greedy and fearful, are your worst enemies. This is true time and time again.

Stock valuation has dropped, and now valuation is becoming less hostile. However, it is still not cheap by historical standards. For the moment, we believe it’s prudent to be extra cautious. However, how serious a correction might be, we have confidence in the US economy in the long term and thus in the stocks in aggregate. We just need to manage through interim losses carefully.

We again would like to emphasize that for any new investor and new money, the best way to step into this kind of market is through dollar cost average (DCA), i.e., invest and/or follow a model portfolio in several phases (such as 2 or 3 months) instead of the whole sum at one shot.

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?

Latest Articles

- How To Fully Utilize Self-Directed IRAs For Retirement Investments

- Newsletter Collection Update

- Portfolio Calculator (Simulator) And Rolling Returns

- ETFs In Asset Classes For Portfolio Construction

- Retirement Savings: How Much Should You Save For A Comfortable Retirement Life?

- High Yield Bonds Are Good Alternatives For Aggressive Fixed Income Investors

- Trends, Factors & Indicators

- Lazy Portfolios Review

- ‘Best’ Tactical Stock or Dividend Income Balanced Portfolios vs. Best Balanced Allocation Fund

- ‘Best’ Stock or Dividend Income Balanced Portfolios vs. Best Balanced Allocation Fund

- Low-Cost Stock Index Funds: Quality ‘Business Conglomerates’ for Solid, Low-Risk Long-Term Returns

- Cash And Money Market ETFs Review

- March 27, 2023: 401k Company Match: How To Maximize Your Free Money

- March 13, 2023: Bank On My Own For Safer And Much Higher Returns

- February 27, 2023: Dimensional Fund Advisors and Capital Group ETFs

- February 13, 2023: In Praise Of A Conservative Strategic Asset Allocation

- January 30, 2023: The Bond Era

- January 16, 2023: International Stocks In Asset Allocation

- January 3, 2023: Review And Outlook

- December 5, 2022: Latest Market And Trend Review

- November 21, 2022: How To Maximize Your Cash Return

- November 7, 2022: Tactical Bond Fund Portfolios Consistently Outperform

- October 24, 2022: S&P 500: A Solid ‘Business’ In A Volatile Time

- October 10, 2022: 9.62% Treasury I Bonds: Cash Is Indeed King

- September 26, 2022: Markets, Noises, Long Term Strategies …

- September 12, 2022: Factor ETFs Review

- August 29, 2022: Cash Is King

- August 15, 2022: Asset Trends Review

- August 1, 2022: What We Can Learn From 1970s And 1980s

- July 18, 2022: Fixed Income Is Becoming An Alternative

- July 1, 2022: About The Latest Rebalance

- June 6, 2022: Sector Rotation In A Rising Rate Environment

- May 23, 2022: Latest Portfolio And Trend Review

- May 9, 2022: The Secular Market Cycle Change

- April 25, 2022: Survivorship Bias, Sentiment And Market Internals …

- April 11, 2022: Asset Allocation And Risk Management

- March 28, 2022: March Madness And Steady Course

- March 14, 2022: Quality Sectors Prevail

- February 28, 2022: Asset Allocation Fund Review

- February 14, 2022: Inflation, Interest Rates And Fixed Income Investments

- February 1, 2022: Foreign Stocks And Global Asset Allocation

- January 18, 2022: Steady And Consistency Win In The Long Term

- January 3, 2022: The Year In Rear View: Portfolio And Asset Class Review

- December 13, 2021: Present And Future

- November 22, 2021: The ‘Best’ Balanced Fund Revisited

- November 15, 2021: Q&A On MyPlanIQ Strategies And Portfolios

- November 8, 2021: Major Asset Returns In The Past Twenty Years

- November 1, 2021: Latest Momentum Factor ETFs Review

- October 25, 2021: A Long Term Theme Or Trend Doesn’t Necessarily Yield Good Returns

- October 18, 2021: Dimensional Fund Advisors DFA ETFs

- October 11, 2021: MyPlanIQ Ultra Short Term Bond Portfolio vs. Other Funds

- October 4, 2021: Asset Trends, Market Internals And Inflation Implication

- September 27, 2021: Newsletter Collection Update

- September 20, 2021: Benchmarking MyPlanIQ Fixed Income Bond Portfolios

- September 13, 2021: Benchmarking MyPlanIQ Tactical Portfolios

- August 30, 2021: Invest And Speculate: A Sensible Alternative To Buy And Hold

- August 23, 2021: Style ETF Portfolio Review

- August 16, 2021: Smart Factor ETFs Review

- August 9, 2021: Best Global Allocation Funds vs. MyPlanIQ ETF Portfolios

- August 2, 2021: Major Asset Trends And Market Internals

- July 26, 2021: Ultra Short Term Bond ‘Money Market’ Portfolio And Banking

- July 19, 2021: Take The Challenge of The ‘Best’ Balance Fund

- July 12, 2021: The Long Forgotten Bear Market Cycles

- June 28, 2021: Resuming Growth Trends Chaotically?

- June 21, 2021: Stocks Are Not Replacement Of Bonds

- June 14, 2021: Outperform The Best Performing PIMCO Income Bond Fund

- June 7, 2021: “Good” S&P Sectors

- May 17, 2021: Total Return Bond ETFs Review

- May 10, 2021: Financial Independence & Early Retirement

- May 3, 2021: Inflation, Sub Zero Interest Rate …

- April 26, 2021: The Best Active Fixed Income Funds Are Still Hard To Beat

- April 19, 2021: New And Old Useful Features

- April 12, 2021: Risk Parity Funds In Current Environment

- April 5, 2021: DoubleLine Shiller CAPE 10 Based Funds Update

- March 29, 2021: International Stocks vs. US Stocks

- March 22, 2021: Ultra Short Term Bond ETF Portfolio As A Money Market Fund

- March 15, 2021: Make Your Own Private Bank

- March 8, 2021: The Not So Orderly Market Rotation Amid Rising Bond Yields

- March 1, 2021: Average 20% Annual Returns: The Upper Bound Of Stock Investments?!

- February 22, 2021: Rising Bond Yields And Current Stock Trends

- February 8, 2021: Total Return Bond ETFs Review

- February 1, 2021: REITs And Major Asset Trends

- January 25, 2021: Industry ETFs And ARK ETFs Portfolios

- January 11, 2021: Smart Cash Management: Can I Just Withdraw From My Bond Portfolio?

- January 4, 2021: Our Investment Philosophy For 2021 And Beyond

- December 14, 2020: Style and Factor ETFs Portfolio Reviews

- December 7, 2020: A Really Long Term (30 Years) Stock Returns

- November 30, 2020: Higher Return Portfolios: Part 2

- November 16, 2020: Higher Return Portfolios

- November 9, 2020: Fixed Income Funds Update

- November 2, 2020: Polls Are Useless vs. This Investment Strategy Doesn’t Work!

- October 26, 2020: Recent Improvements

- October 19, 2020: REIT Indexes As Businesses

- October 12, 2020: Stock Indexes As Businesses

- October 5, 2020: Asset Trend Review

- September 28, 2020: Retirement Spending: Your Portfolio’s Volatility Matters

- September 21, 2020: Boring Utility Stocks Are Excellent Long Term Winners

- September 14, 2020: Surprised, Active Fixed Income Investors Have Done Better Than Stock Investors For The Last 20 Years!

- August 31, 2020: Investing In An Ultra-Low Return Environment

- August 24, 2020: Target Maturity Bond ETFs For Short Term Cash

- August 17, 2020: Newsletter Collection Update

- August 10, 2020: Fixed Income In A Speculative Era

- August 3, 2020: Sound Investment Strategies

- July 27, 2020: Total Return Bond Funds Update

- July 20, 2020: Divergence Between Value And Growth Stocks Everywhere

- July 13, 2020: Short Term Cash, Treasury Bills, CDs And Future Fixed Income

- July 6, 2020: Bond ETFs vs. Bond Mutual Funds

- June 29, 2020: Industry Sector ETF Rotation With Composite Momentum

- June 22, 2020: Industry Sector Rotation With Composite Momentum

- June 15, 2020: Advanced Minimum Equity Portfolios

- June 8, 2020: Recent Positive Developments

- June 1, 2020: Minimum Equity Portfolios

- May 18, 2020: Core Satellite Portfolios In The Current Pandemic

- May 11, 2020: Asset Trends Review

- May 4, 2020: The Real, Sensible And Wise Warren Buffett

- April 27, 2020: Total Return Bond Funds & Portfolios

- April 20, 2020: Multi-Factor ETFs and Rotation

- April 13, 2020: A Closer Look At 401(k) Investment Portfolios

- April 6, 2020: Long Term Stock Market Timing Since 1871 Revisited

- March 30, 2020: How Did Bond ETFs And Mutual Funds Fare In The Current Crisis?

- March 23, 2020: Chaos And Hope

- March 16, 2020: A Live Lesson

- March 9, 2020: Risk And Reward

- March 2, 2020: The Risk Of Coronavirus Outbreak

- February 24, 2020: Long Term Stock Valuation Based Investment Strategies

- February 10, 2020: Update On Short Term Cash, Treasury Bills and Brokered CDs

- February 3, 2020: Investment Landscape For Retirees And Would-be Retirees: Stocks

- January 27, 2020: Investment Landscape For Retirees And Would-be Retirees: Fixed Income

- January 13, 2020: Portfolio Performance: A Walk In The Past II

- January 6, 2020: Asset Outlook and Portfolio Strategies

- December 16, 2019: Q&As On Our Services

- December 9, 2019: Portfolio Constructions For Advanced Users

- December 2, 2019: Newsletter Collection Update

- November 25, 2019: Core ETFs or Core Mutual Funds Portfolios

- November 18, 2019: Introducing MyPlanIQ Asset Allocation Composite Strategy

- November 11, 2019: Market Indicator And Momentum

- November 4, 2019: Factor ETF Rotation

- October 28, 2019: Multi-factor ETFs vs. Equal Weight Multi-Factor Portfolios

- October 21, 2019: Multi-factor ETFs: Value And Momentum

- October 14, 2019: Low Volatility Factor ETFs

- October 7, 2019: Zero Commission Era Has Arrived, Is It Really That Good?

- September 30, 2019: Boosting Bond ETF Portfolio’s Return With Muni Bond ETFs

- September 23, 2019: Value ETFs

- September 16, 2019: Factor ETFs

- September 9, 2019: Momentum Factor Stock ETFs

- August 26, 2019: Employer 401k Match: Yet Another Free Lunch Not To Be Missed

- August 19, 2019: PIMCO Income Fund and Other Total Return Bond Funds Update

- August 12, 2019: Aggressive Fixed Income Portfolios?

- August 5, 2019: Long Term Investment Strategies And Short Term Market Noises

- July 29, 2019: Fixed Income Portfolios In A Lower Yield Environment

- July 22, 2019: Core Satellite Portfolios Balance Fluctuation

- July 15, 2019: Quality Stock Factor ETFs

- July 8, 2019: Surprise! Brokerages Make Most From Your Cash, Not Commissions

- July 1, 2019: Utilities Sector Review

- June 24, 2019: Asset Allocation Funds Review

- June 17, 2019: Latest Performance Comparison Among Several Advanced Strategies

- June 10, 2019: Money Market And Ultra Short Term Bond Funds

- June 3, 2019: What We Can Learn From The Seasonality Strategy

- May 20, 2019: Morningstar Portfolio Manager Awards

- May 13, 2019: Total Return Bond ETFs Review

- May 6, 2019: Global Allocation Revisited

- April 29, 2019: Asset Trend Review

- April 22, 2019: The Current State Of Fixed Income

- April 15, 2019: The Importance Of Fixed Income Returns For Retirement Spending

- April 8, 2019: Newsletter Collection Update

- April 1, 2019: S&P 500 As A Business

- March 25, 2019: Health Care Sector Review

- March 18, 2019: The Risk Of Stock Investing

- March 11, 2019: Consumer Staples Sector Review

- March 4, 2019: Global Stock Valuation Update

- February 25, 2019: ‘Bad’ Tactical Strategy

- February 11, 2019: “Best” Balanced Fund And Portfolios Revisited

- February 4, 2019: Cash And Money Market Funds: Interests And Safety

- January 28, 2019: Fixed Income Review

- January 14, 2019: Tactical Asset Allocation Portfolio Review

- January 7, 2019: Global Strategic Asset Allocation Portfolio Review

- December 17, 2018: Robinhood’s ‘Revolution’ Or Gimmick

- December 10, 2018: How Defensive Are REITs?

- December 3, 2018: Conservative Core Satellite Portfolio

- November 26, 2018: Allocation Mutual Fund Review

- November 19, 2018: Is The Recent Downtrend Sustainable?

- November 12, 2018: The Staggering Low Interest Rates From Big Banks

- November 5, 2018: The ‘Right’ Or ‘Wrong’ Decision

- October 29, 2018: Taxable Total Return Bond Plus Muni Bond Fund Based Portfolios

- October 22, 2018: DoubleLine Shiller CAPE 10 Based Fund Review

- October 15, 2018: Newsletter Collection Update

- October 8, 2018: Asset Trend Review

- October 1, 2018: Taxable vs. Tax Exempt High Yield Bonds

- September 24, 2018: High Yield Bonds In A Rising Rate Environment

- September 10, 2018: Value, Growth And Blend Stock Style Investing

- August 27, 2018: Money Market ETFs?

- August 20, 2018: How Momentum Investing Stacks Up?

- August 13, 2018: Total Return Bond ETF

- August 6, 2018: Fidelity Zero-Fee Index Funds

- July 30, 2018: Tax Efficient Portfolios

- July 23, 2018: Municipal Bond Funds And Portfolios

- July 16, 2018: A Guide To Conservative Portfolios

- July 9, 2018: Conservative Allocation Mutual Funds Based Portfolios

- July 2, 2018: Small Cap Stocks For The Long Term

- June 25, 2018: What Can We Learn From GE’s Removal From Dow Jones Index?

- June 18, 2018: The ‘Best’ Balanced Portfolio Continues To Excel

- June 11, 2018: Is 10 Year Long Enough For Portfolio Comparison?

- June 4, 2018: Action Plan: Risk Review For Investments

- May 21, 2018: Rising Rates, Consumer Staples And Stock Index

- May 14, 2018: Newsletter Collection Update

- May 7, 2018: Money Market Fund Taxonomy

- April 30, 2018: Momentum Investing Review

- April 23, 2018: Commodities In Current Environment

- April 16, 2018: Municipal Bonds As A Fixed Income Asset Class

- April 9, 2018: Exponential Or Compounding Nature In Investing

- April 2, 2018: Inside Of The Stock Chaos

- March 26, 2018: Total Return Bond Update

- March 19, 2018: Treasury Bills vs. Brokered CDs

- March 12, 2018: Defensive Conservative Portfolio Review

- March 5, 2018: Warren Buffett’s Advices

- February 26, 2018: Pros And Cons of Strategic And Tactical Portfolios In 2018

- February 12, 2018: Trend Review

- February 5, 2018: Market Selloff And Long Term Investing

- January 29, 2018: The New Addition To Our Total Return Bond Fund Candidates

- January 22, 2018: Where Are Bonds Heading?

- January 15, 2018: Tactical Portfolios Review

- January 8, 2018: Strategic Portfolios Review

- December 18, 2017: Record Highs And Risk

- December 11, 2017: Cash Return And Interest Rate Update

- December 4, 2017: Mutual Fund Star Ratings: Are They Useful?

- November 20, 2017: Thankful And Mindful

- November 13, 2017: Is This A Good Time For Retirees Or Would Be Retirees?

- November 6, 2017: Newsletter Collection Update

- October 30, 2017: Rising Interest Rates

- October 23, 2017: A Primer For Portfolios

- October 16, 2017: REITs As An Asset Class

- October 9, 2017: Conservative Portfolios Revisited

- October 2, 2017: The Role of Short Term Bond Funds

- September 25, 2017: Fees In Cash Investments

- September 18, 2017: Conservative Portfolios Review

- September 11, 2017: International Diversification Effect

- September 4, 2017: Invest And Speculate Revisited

- August 28, 2017: Total Return Bond Fund Portfolios: Where Do They Fit?

- August 21, 2017: Portfolio Performance: A Walk In The Past

- August 14, 2017: Fidelity Commission Free ETFs Update

- August 7, 2017: I Didn’t Learn Anything — Mistake vs. Temporary Underperformance

- July 31, 2017: Asset Classes And Fund Choices: A Primer

- July 24, 2017: Total Return Bond Fund Portfolios And Cash

- July 17, 2017: Long Term Stock Holding Periods For Retirement

- July 10, 2017: Half Year Asset Trend Review

- June 26, 2017: How To Beat The Best Balanced Allocation Fund

- June 19, 2017: Newsletter Collection Update

- June 12, 2017: A Mixed Bag Performance of Momentum Investing

- June 5, 2017: How To Start A New Portfolio

- May 29, 2017: Alternative Assets And Their Role In Portfolios

- May 22, 2017: Summer Seasonality And Portfolio Management

- May 15, 2017: Cash: Banking Or Investing?

- May 8, 2017: Holding Period of Long Term Timing Portfolios

- May 1, 2017: Debate on Risk vs. Volatility

- April 24, 2017: The Long Term Stock Market Timing Return Since 1871

- April 17, 2017: Risk vs. Volatility: Long Term Stock Market Returns

- April 10, 2017: Total Return Bond ETFs And Portfolios

- April 3, 2017: Quarter End Asset Trend Review

- March 27, 2017: Practical Consideration For IRAs And 401k Accounts

- March 20, 2017: Fund Fees: That’s (Still) Outrageous

- March 13, 2017: Long Term Stock Valuation Review

- March 6, 2017: Asset Classes for Retirement Investments

- February 27, 2017: Fidelity Total Bond Fund Review

- February 20, 2017: Long Term Stock Timing Based Portfolios And Their Roles

- February 13, 2017: Alternative Investment Portfolios Review

- February 6, 2017: Tax Free Municipal Bond Investments Review

- January 30, 2017: Brokerage Specific Conservative Portfolios

- January 23, 2017: Fixed Income Portfolio Review

- January 16, 2017: Long Term Trend Following Portfolio Review

- January 9, 2017: Tactical Asset Allocation Review

- January 3, 2017: Strategic Asset Allocation Review

- December 12, 2016: Enhanced Index Funds

- December 5, 2016: Review Of Broad Base Core Mutual Funds For Brokerages

- November 28, 2016: Core Index ETFs Review

- November 21, 2016: International Exposure Of U.S. Large Companies

- November 14, 2016: Asset Trends After The Election

- November 7, 2016: Rising Rate And Current Bond Trend

- October 31, 2016: Economy Power And Long Term Stock Returns

- October 24, 2016: Current Commodity Trend And Managed Futures

- October 17, 2016: Investment Mistakes And Good Or Bad Investment Strategies

- October 10, 2016: Momentum Investing Review

- October 3, 2016: Survey & Feedback

- September 26, 2016: Fixed Income Investing: Actively Managed Funds vs. Index Funds

- September 19, 2016: Stock Investing: Actively Managed Funds vs. Index Funds

- September 12, 2016: Newsletter Update

- September 5, 2016: Overvalued Markets And Long Term Timing Strategies

- August 29, 2016: Your 401K Finally Draws Attention

- August 22, 2016: Inflation Protected Securities TIPS For Current Overvalued Markets

- August 15, 2016: Risk On: Emerging Market Stocks And Small Cap Stocks

- August 8, 2016: Portfolio Construction Using Stock ETFs And Bond Mutual Funds

- August 1, 2016: Adding Value To Your Own Investments

- July 25, 2016: Tactical Asset Allocation Funds Review

- July 18, 2016: Strategic Asset Allocation & Lazy Portfolio Review

- July 11, 2016: Asset Trend Review

- June 27, 2016: Secular Cycles For Tactical And Strategic Investment Strategies

- June 20, 2016: A World of Debt

- June 13, 2016: Managed Futures For Portfolio Building

- June 6, 2016: Newsletter Summary

- May 30, 2016: Swensen Portfolio And Permanent Portfolios

- May 23, 2016: AAII Article And Some Web Changes

- May 16, 2016: The PIMCO (Dis)Advantages

- May 9, 2016: Boost Your Dull Summer Investments

- May 2, 2016: Low Cost Index Fund Investing

- April 25, 2016: Tax Free Municipal Bond Funds & Portfolios

- April 18, 2016: Asset Class Trend Review

- April 11, 2016: Construction of Sound And Conservative Portfolios

- March 28, 2016: Total Return Bond ETFs Review

- March 21, 2016: Small And Large Company Stock Performance In Different Economic Expansion Cycles

- March 14, 2016: Are Tactical And Timing Strategies Losing Steam?

- March 7, 2016: Defined Maturity Bond Fund Analysis

- February 29, 2016: Smart Strategic Asset Allocation Rebalance When Market Trend Changes

- February 22, 2016: Be Cash Smart

- February 15, 2016: Bond ETF Portfolios

- February 8, 2016: Newsletter Collection Update

- February 1, 2016: Total Return Bond Fund Portfolios In A Volatile Period

- January 25, 2016: Alternative Portfolios Review

- January 18, 2016: Strategic Asset Allocation: A Cautious Outlook

- January 11, 2016: Review Of Trend Following Tactical Asset Allocation

- January 4, 2016: What Worked And Didn’t In 2015

- December 21, 2015: Distressed Assets

- December 14, 2015: High Yield Bonds And Their Correlation With Stocks

- December 7, 2015: Diversification And Global Allocation

- November 30, 2015: Investors and Speculators Combined

- November 23, 2015: Active Stock Fund Performance Consistency

- November 16, 2015: Permanent, Risk Parity And Alternative Portfolios Review

- November 9, 2015: Broad Base Core Mutual Fund Review

- November 2, 2015: Broad Base Index Core ETFs Review

- October 26, 2015: Total Return Bond Fund Review

- October 19, 2015: Advanced Portfolio Review

- October 12, 2015: What About Commodities?

- October 5, 2015: Core Satellite Portfolios In A 401k Account

- September 28, 2015: Risk Managed Strategic Asset Allocation Portfolios Revisited

- September 21, 2015: Quest For The Best Investment Strategy

- September 14, 2015: Core Satellite Portfolios In Market Turmoil

- September 7, 2015: Market Rout Creates An Opportunity to Reposition Your Portfolios

- August 31, 2015: Review of Asset Allocation Funds and Portfolios

- August 24, 2015: Market Rout And Your Portfolios

- August 17, 2015: ETF or Mutual Fund Based Portfolios

- August 10, 2015: Updated Newsletter Collection

- August 3, 2015: Slippery Asset Trends

- July 27, 2015: Performance Dispersion Among Momentum Based Portfolios

- July 20, 2015: Global Balanced Portfolio Benchmarks

- July 13, 2015: Pain in Tactical Portfolios

- July 6, 2015: Fixed Income Total Return Bond Funds In Strategic Asset Allocation Portfolios

- June 29, 2015: Core ETF Commission Free Portfolios

- June 22, 2015: Secular Asset Trends

- June 15, 2015: Giving Up Bonds?

- June 1, 2015: Summer Blues?

- May 26, 2015: Cash, Bonds and Stocks In A Rising Rate Environment

- May 18, 2015: Portfolio Update

- May 11, 2015: Pain in Fixed Income?

- May 4, 2015: The Balanced Stock and Long Term Treasury Bond Portfolios

- April 27, 2015: Long Term Treasury Bond Behavior

- April 20, 2015: 529 College Savings Plan Rebalance Policy Change

- April 13, 2015: Total Return Bond Funds As Smart Cash

- April 6, 2015: The Low Return Environment

- March 30, 2015: Brokerage Specific Core Mutual Fund Portfolios 2

- March 23, 2015: Investment Arithmetic for Long Term Investments

- March 16, 2015: Brokerage Specific Core Mutual Fund Portfolios

- March 9, 2015: Newsletter Collection Update

- March 2, 2015: Total Return Bond ETFs

- February 23, 2015: Why Is Global Tactical Asset Allocation Not Popular?

- February 16, 2015: Where Are Permanent Portfolios Going?

- February 9, 2015: How Have Asset Allocation Funds Done?

- February 2, 2015: Risk Management Everywhere

- January 26, 2015: Composite Portfolios Review

- January 19, 2015: Fixed Income Investing Review

- January 12, 2015: How Does Trend Following Tactical Asset Allocation Strategy Deliver Returns

- January 5, 2015: When Forecast Fails

- December 22, 2014: Long Term Asset Returns: How Long Is Long?

- December 15, 2014: Beaten Down Assets

- December 8, 2014: Implementing Core Asset Portfolios In a Brokerage

- December 1, 2014: Two Key Issues of Investment Strategies

- November 24, 2014: Holiday Readings

- November 17, 2014: Retirement Spending Portfolios Update

- November 10, 2014: Fixed Income Or Cash

- November 3, 2014: Asset Trend Review

- October 27, 2014: Investment Loss, Mistakes And Market Cycles

- October 20, 2014: Strategic Portfolios With Managed Volatility

- October 13, 2014: Embrace Volatility

- October 6, 2014: Tips For 401k Open Enrollment

- September 29, 2014: What Can We Learn From Bill Gross’ Departure From PIMCO?

- September 22, 2014: Why Total Return Bond Funds?

- September 15, 2014: Equity And Total Return Bond Fund Composite Portfolios

- September 8, 2014: Momentum Based Portfolios Review

- September 1, 2014: Risk & Diversification: Mint.com Interview

- August 25, 2014: Remember Risk

- August 18, 2014: Consistency, The Most Important Edge In Investing: Tactical Case

- August 11, 2014: What To Do In Overvalued Stock Markets

- August 4, 2014: Is This The Peak Or Correction?

- July 28, 2014: Stock Musings

- July 21, 2014: Permanent Portfolios & Four Pillar Foundation Based Framework

- July 14, 2014: Composite Portfolios Review

- July 7, 2014: Portfolio Behavior During Market Corrections

- June 30, 2014: Half Year Brokerage ETF and Mutual Fund Portfolios Review

- June 23, 2014: Newsletter Collection Update

- June 16, 2014: There Are Always Lottery Winners

- June 9, 2014: The Arithmetic of Investment Mistakes

- June 2, 2014: Tips On Portfolio Rebalance

- May 26, 2014: In Praise Of Low Cost Core Asset Class Based Portfolios

- May 19, 2014: Consistency, The Most Important Edge In Investing: Strategic Case

- May 12, 2014: How To Handle An Elevated Overvalued Market

- May 5, 2014: Asset Allocation Funds Review

- April 28, 2014: Now The Economy Backs To The ‘Old Normal’, Should Our Investments Too?

- April 21, 2014: Total Return Bond Investing In The Current Market Environment

Diversified Asset Allocation Portfolios For Your Plans

Diversified Asset Allocation Portfolios For Your Plans