October 29, 2012: Sharpe, Maximum Draw Down And Sortino Ratios

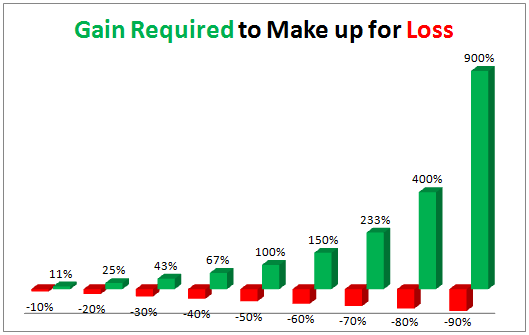

We discussed Sharp ratio, maximum drawdown and Sortino ratio, all of which are important metrics for portfolio behavior measurement.

We discussed Sharp ratio, maximum drawdown and Sortino ratio, all of which are important metrics for portfolio behavior measurement.

We review conservative and bond investing portfolios: fixed income investors can still achieve reasonable returns through diversification and active management of various bond segments.

Asset allocation is the key factor for portfolio returns and risk. Fund selection should be oriented around the target asset allocation and funds’ correlation with their asset classes.

Strategic allocation portfolios have out performed their tactical counterparts for the last 3 years? Is it the time to ditch the tactical portfolios? Not so fast, we argue.

We released Strategic Asset Allocation – Optimal strategy for basic subscribers. This strategy complements with TAA to form solid core satellite portfolios.

Diversified Asset Allocation Portfolios For Your Plans

Diversified Asset Allocation Portfolios For Your Plans

| Vanguard ETF: | 10%* |  |

| Diversified Core: | 11%* | |

| Six Core Asset ETFs: | 10%* | |