So Re-balance Cycle Reminder All MyPlanIQ’s newsletters are archived here.

Regular AAC (Asset Allocation Composite), SAA and TAA portfolios are always rebalanced on the first trading day of a month. the next re-balance will be on Monday May 1, 2023.

As a reminder to expert users: advanced portfolios are still re-balanced based on their original re-balance schedules and they are not the same as those used in Strategic and Tactical Asset Allocation (SAA and TAA) portfolios of a plan.

Cash And Money Market ETFs Review

Many people are now realizing the importance of finding ways to earn higher interest rates on their cash deposits, especially in light of recent bank runs that have shaken their confidence. We have repeatedly highlighted this issues over the past five years, as seen in our article “Bank On My Own For Safer And Much Higher Returns.” One option to consider is using “Cash” or money market style ETFs, which are widely available in most investment brokerage accounts. However, investors should be aware of what these instruments are and whether they qualify as a money market fund.

We have discussed this topic extensively in previous newsletters, but this article aims to provide a more comprehensive review of the subject. We will also make effort to keep this article up to date so that it can serve as a useful reference for our readers.

What are money market funds?

A typical definition: A money market fund is a type of mutual fund that invests in low-risk, short-term debt securities, such as government bonds, certificates of deposit, and commercial paper. The goal of a money market fund is to provide investors with a relatively safe place to park their cash while earning a slightly higher return than traditional savings accounts or other types of cash investments. Money market funds are typically managed to maintain a stable net asset value (NAV, i.e. its holdings’ value) of $1 per share, making them a popular choice for investors who want to preserve their capital and earn some income without taking on too much risk.

A money market fund’s NAV is permitted to fluctuate within a narrow range of 0.5% above or below the stable $1.00 per share value. This means that a money market fund’s NAV may be reported as $1.005 or $0.995 per share without triggering any action to restore the stable NAV. If the NAV falls below this 0.5% threshold, the fund is required to take certain steps to restore its stable NAV, such as waiving fees, suspending redemptions, or liquidating assets.

Notice in the above, a money market fund is a mutual fund. Technically, an ETF can not be classified as a money market fund. We will discuss this more shortly.

There are regulations that govern the duration of a money market fund’s debt holdings. In the United States, for example, the Securities and Exchange Commission (SEC) requires that at least 30% of a money market fund’s assets be invested in securities that mature within 7 days, and at least 60% be invested in securities that mature within 60 days. This is known as the “7-day liquidity rule” and is designed to ensure that money market funds can meet their obligations to investors in the event of sudden redemptions. Additionally, the SEC imposes restrictions on the credit quality and diversification of a money market fund’s holdings to help mitigate the risk of default. These regulations help to make money market funds a relatively safe and stable investment option for short-term cash holdings. For example, Vanguard Federal Money Market Fund maintains an average maturity of 60 days or less.

To summarize, a money market fund needs to

- maintain its NAV to be within a narrow range of 0.5% above or below the stable $1.00 per share value.

- it needs to hold enough short term (30% 7-day maturity and 60% 60-day maturity) debts — interest rate risk.

- it needs to hold high quality debts — credit risk

In general, a money market fund is only available in an investment brokerage account. Some banks might offer money market accounts.

Cash and money market ETFs

Why should we consider ETFs as a substitute for cash or a money market fund? The answer is that many brokerages no longer offer money market funds or, if they do, they often provide lower yields. In addition, only a few brokerages offer good money market funds, and many of these have minimum investment requirements. For instance, the Vanguard Federal Money Market Fund previously required a minimum investment of $3,000, but we are pleased to note that this requirement was recently eliminated (as of 4/1/2023).

In contrast, ETFs can be purchased at any brokerage that offers stock trading, and there is no minimum investment requirement. Some brokers even provide fractional shares, allowing investors to purchase ETFs in any dollar amount.

While no ETF can technically be classified as a money market fund, we can further explore the so-called ultra short-term bond ETFs to see what options are available.

Ultra short term Treasury bill or note ETFs

The first type are the ETFs that invest solely in ultra short term Treasury bills or notes. We have done some comprehensive studies on this and come up with the following liquid enough ETFs in this category:

| Symbol (Name) | Expense | Asset Size | Maximum Drawdown | SEC Yield | YTD Return** |

1Yr AR | 3Yr AR | 5Yr AR |

|---|---|---|---|---|---|---|---|---|

| BIL (SPDR Barclays 1-3 Month T-Bill ETF) | 0.14% | 29B | -0.14% | 4.52% | 1.1% | 2.5% | 0.8% | 1.2% |

| SGOV (iShares 0-3 Month Treasury Bond ETF) | 0.03% | 10B | 0% | 4.64% | 1.2% | 2.8% | ||

| USFR (WisdomTree Floating Rate Treasury Fund) | 0.15% | 15B | -0.05% | 4.78% | 1.3% | 3.0% | 1.1% | 1.4% |

| TFLO (iShares Treasury Floating Rate Bond ETF) | 0.15% | 5.8B | -0.06% | 4.79% | 1.2% | 2.6% | 0.9% | 1.3% |

| CASH (CASH) | N/A | 0% | 1.4% | 2.8% | 1.0% | 1.1% | ||

| VMFXX (Vanguard federal money market) | 0.15% | 238B | N/A | 4.75% | 1.18% | 2.7% | 0.9% | 1.3% |

Maximum Drawdown: maximum loss from a peak to a subsequent trough.

SEC Yield: Based on a 30-day period ending on the last day of the previous month. Note, for a money market mutual fund like VMFXX, its SEC yield is usually a 7-day period’s holdings average yield.

Notice in the above table, SGOV is relatively new (started on 5/28/2020).

Technically, a risk free Cash is defined as the 3-month Treasury bill interest rate (daily reset). CASH is MyPlanIQ’s internal cash tracking symbol whose daily interest is reset daily based on the publicly quoted 3-month Treasury bill interest rate.

There are two large liquid Treasury floating rate ETFs, USFR (WisdomTree Floating Rate Treasury Fund) and TFLO (iShares Treasury Floating Rate Bond ETF). These two ETFs invest in Treasury Floating Rate Notes that essentially reset their interest rates weekly based on 13-week (3-month) Treasury bill auction results. See TreasuryDirect.gov for a more detailed explanation. So even though they hold 2-year mature notes, their interest rate risk is almost zero as they are practically matched to 13-week T-Bill.

BIL (SPDR Barclays 1-3 Month T-Bill ETF) holds 1-3 month Treasury bills and it will replace mature ones to maintain certain ladders. Its average maturity, based on Morningstar, is about 29 days or about one month.

All of the aforementioned ETFs exhibit minimal maximum drawdowns, ranging from -0.05% to -0.14% (BIL), which is significantly smaller than the -0.5% range required for a money market fund. Additionally, they invest in US Treasury bills or notes, which are considered the safest and equivalent to cash. They are also sufficiently liquid, at least for non-large investments. Even if a large sum of money is invested in one of these ETFs (such as multi-millions), as long as daily withdrawals are not substantial, these funds can manage up to a million dollars easily.

It is worth mentioning that these ETFs mostly pay dividends/interest monthly. Using yields to compare these ETFs’ returns is not recommended, as the dividends can sometimes be affected by the price gain/loss (capital gain/loss) of their holdings. In general, the best approach is still to compare their total returns over a period of time, including dividend reinvestment.

In comparison to Vanguard’s money market funds, these ETFs offer comparable returns. Overall, we believe that USFR and TFLO, the two floating rate Treasury ETFs, will likely have the most competitive or even a slight advantage over Vanguard’s money market fund.

Therefore, these ETFs can be viewed as “Cash” ETFs.

‘Prime money market’ ETFs?

Regrettably, extending beyond Treasury bills to include investing in ultra short term corporate bonds or loans is challenging, as we have been unable to locate any ETF whose price remains within the (-)0.5% range. This is due to the fact that, during periods of financial market distress, investors frequently categorize these ETFs as riskier corporate bond/loan options and dispose of them indiscriminately.

Here are the best and most liquid ultra short term ETFs that may be considered as ‘prime money market’ funds. The definition of a prime money market fund is one that may hold not just Treasury and government agency bonds/bills, but also corporate bonds and loans, which are regarded as considerably riskier than Treasury bills.

| Symbol (Name) | Expense | Asset Size | Effective Duration | Max Drawdown | YTD Return** |

1Yr AR | 3Yr AR | 5Yr AR |

|---|---|---|---|---|---|---|---|---|

| JPST (JPMorgan Ultra-Short Income ETF) | 0.18% | 25B | 0.29 | -1.56% | 1.3% | 2.8% | 1.9% | 2.0% |

| ICSH (iShares Ultra Short-Term Bond ETF) | 0.08% | 6.3B | 0.43 | -0.85% | 2.9% | 6.4% | 2.7% | 2.6% |

| NEAR (iShares Short Maturity Bond ETF) | 0.25% | 4.0% | 0.43 | -3.59% | 2.6% | 5.9% | 3.4% | 2.4% |

| MINT (PIMCO Enhanced Short Maturity Active ETF) | 0.36% | 8.3% | 0.44 | -2.49% | 1.5% | 1.9% | 1.3% | 1.3% |

| FLOT (iShares Floating Rate Bond) | 0.15% | 7.6B | 0.05 | -3.43% | 2.7% | 7.6% | 4.1% | 2.7% |

| VUSB (Vanguard Ultra-Short Bond ETF) | 0.1% | 3.4B | 0.96 | -0.7% | 2.7% | 5.0% | ||

| CASH (CASH) | 0.1% | 1.4% | 2.8% | 1.0% | 1.1% |

Note: VUSB (Vanguard Ultra-Short Bond ETF) has a short history (started on 4/27/2021). It also has a longest duration (0.96, almost a year).

From the above, we can see that none of these are qualified as a money market fund as all of them have maximum drawdown bigger than -0.5%. They can’t be simply used as cash or money market fund substitutes.

Enhanced cash or ‘prime money market’ portfolio

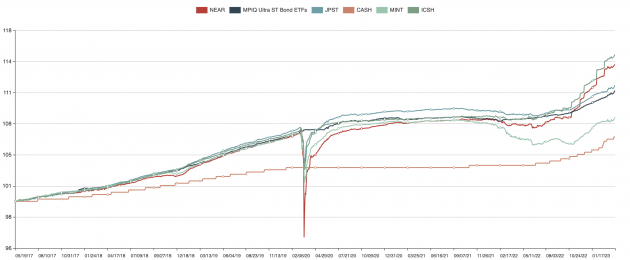

Is it possible to increase the returns of the ultra short term Treasury bill ETFs mentioned earlier? Yes, by taking on additional risk and adopting a more active strategy, one can create a portfolio that dynamically invests in these ultra-safe Treasury ETFs, as well as the riskier ultra short term bond ETFs mentioned above. The concept is to invest in the riskier ETFs when the markets are calm, as these have a low fluctuation rate and incur losses of no more than -0.5%. However, during times of market duress, the portfolio would switch to the “safer” Treasury ETFs to avoid significant drawdown or interim loss.

The following portfolio MPIQ Ultra ST Bond ETFs does just like that:

| Ticker/Portfolio Name | Maximum Drawdown | YTD Return** |

1Yr AR | 3Yr AR | 5Yr AR |

|---|---|---|---|---|---|

| MPIQ Ultra ST Bond ETFs | -0.5% | 1.3% | 2.8% | 1.3% | 1.9% |

| JPST (JPMorgan Ultra-Short Income ETF) | -1.56% | 1.3% | 2.8% | 1.9% | 2.0% |

| MINT (PIMCO Enhanced Short Maturity Active ETF) | -2.49% | 1.5% | 1.9% | 1.3% | 1.3% |

| ICSH (iShares Ultra Short-Term Bond ETF) | -0.85% | 2.9% | 6.4% | 2.7% | 2.6% |

| NEAR (iShares Short Maturity Bond ETF) | -3.59% | 2.6% | 5.9% | 3.4% | 2.4% |

| CASH (CASH) | N/A | 1.4% | 2.8% | 1.0% | 1.1% |

So this portfolio had a small dip in 2021 to 2022 but in general, its maximum drawdown is below -0.5%:

The portfolio basically invests in one ETF at any time. It looks at its holding at the beginning of every month and decides whether to switch to another fund. Its candidate funds include the above riskier ETFs and some of the ‘safe’ Cash Treasury ETFs in the above.

This portfolio requires a basic subscription to MyPlanIQ’s service that also allows to follow MyPlanIQ’s other fixed income portfolios. Subscribers will receive a monthly rebalance email to notify any transaction needed and they can follow the rebalance instruction in their own brokerage accounts to mimic these portfolios. The MPIQ Ultra ST Bond ETFs can be used to enhance cash returns or achieve a prime money market fund’s return.

Conclusions

Instead of a money market fund, one can consider using Ultra short Treasury bills or floating rate ETFs which are highly competitive with even the best government or Treasury money market funds. However, it’s important to note that other ultra short term bond ETFs cannot replace a traditional prime money market fund due to the fact that their prices are determined by markets and are subject to greater fluctuations than a money market fund would allow.

Market overview

The latest employment situation report from last Friday has surprised many by indicating a decline in the unemployment rate from 3.6% in February to 3.5% in March, which is both interesting and frustrating for the Federal Reserve Bank as it implies that the job market is still too hot and inflation might be high. However, the recent banking crisis or scare in March may have tightened financial conditions as banks have become more cautious and increased loan interest rates. This may take some time to fully manifest in economic reports, which makes the Federal Reserve’s situation tricky. Stopping interest rate hikes too early could result in another round of price inflation, while continuing to raise rates in an already slowing economy could push it into a recession.

The uncertainty is reflected in financial markets, with stocks hoping for a ‘soft landing’ and bond markets predicting a more softened economy, as evidenced by the decline in the long-term 10-year Treasury interest rate from 4% to 3.4%. The S&P 500 price has remained virtually unchanged since a year ago, and the markets are choppy.

As always, we call for staying the course which is guided by some well defined and sound strategies:

- For strategic allocation (buy and hold) investors, ignore the current market behavior. Remember, as what we have emphasized numerous times, when you choose and commit to a strategic portfolio, you essentially know and commit that your investment horizon (or the time you need to utilize this capital) is 20 years or preferably much longer given the current high valuation. As we pointed out, if your investments are those diversified (index) funds such as an S&P 500 index fund (VFINX, for example), you know your money is in some solid ‘business’ that eventually (20 years later and preferably many more years later) will deliver some reasonable returns. As long as you are comfortable with this thesis, you should sit tight and forget about the current gyration.

- For tactical investors, again, you have to ignore the current market noise. Furthermore, you should follow your strategy rigorously, especially in a time like this. Human emotion, both optimistic and pessimistic, and human desire, both greedy and fearful, are your worst enemies. This has been shown to be true time and time again.

Stock valuation has dropped and now valuation is becoming less hostile. However, it is still not cheap by historical standard. For the moment, we believe it’s prudent to be extra cautious. However how serious a correction might be, we have confidence in the US economy in the long term and thus in the stocks in aggregate. We just need to manage through interim losses carefully.

We again would like to emphasize that for any new investor and new money, the best way to step into this kind of markets is through dollar cost average (DCA), i.e. invest and/or follow a model portfolio in several phases (such as 2 or 3 months) instead of the whole sum at one shot.

Enjoy Newsletter

How can we improve this newsletter? Please take our survey

–Thanks to those who have already contributed — we appreciate it.

Latest Articles

- March 27, 2023: 401k Company Match: How To Maximize Your Free Money

- March 13, 2023: Bank On My Own For Safer And Much Higher Returns

- February 27, 2023: Dimensional Fund Advisors and Capital Group ETFs

- February 13, 2023: In Praise Of A Conservative Strategic Asset Allocation

- January 30, 2023: The Bond Era

- January 16, 2023: International Stocks In Asset Allocation

- January 3, 2023: Review And Outlook

- December 5, 2022: Latest Market And Trend Review

- November 21, 2022: How To Maximize Your Cash Return

- November 7, 2022: Tactical Bond Fund Portfolios Consistently Outperform

- October 24, 2022: S&P 500: A Solid ‘Business’ In A Volatile Time

- October 10, 2022: 9.62% Treasury I Bonds: Cash Is Indeed King

- September 26, 2022: Markets, Noises, Long Term Strategies …

- September 12, 2022: Factor ETFs Review

- August 29, 2022: Cash Is King

- August 15, 2022: Asset Trends Review

- August 1, 2022: What We Can Learn From 1970s And 1980s

- July 18, 2022: Fixed Income Is Becoming An Alternative

- July 1, 2022: About The Latest Rebalance

- June 6, 2022: Sector Rotation In A Rising Rate Environment

- May 23, 2022: Latest Portfolio And Trend Review

- May 9, 2022: The Secular Market Cycle Change

- April 25, 2022: Survivorship Bias, Sentiment And Market Internals …

- April 11, 2022: Asset Allocation And Risk Management

- March 28, 2022: March Madness And Steady Course

- March 14, 2022: Quality Sectors Prevail

- February 28, 2022: Asset Allocation Fund Review

- February 14, 2022: Inflation, Interest Rates And Fixed Income Investments

- February 1, 2022: Foreign Stocks And Global Asset Allocation

- January 18, 2022: Steady And Consistency Win In The Long Term

- January 3, 2022: The Year In Rear View: Portfolio And Asset Class Review

- December 13, 2021: Present And Future

- November 22, 2021: The ‘Best’ Balanced Fund Revisited

- November 15, 2021: Q&A On MyPlanIQ Strategies And Portfolios

- November 8, 2021: Major Asset Returns In The Past Twenty Years

- November 1, 2021: Latest Momentum Factor ETFs Review

- October 25, 2021: A Long Term Theme Or Trend Doesn’t Necessarily Yield Good Returns

- October 18, 2021: Dimensional Fund Advisors DFA ETFs

- October 11, 2021: MyPlanIQ Ultra Short Term Bond Portfolio vs. Other Funds

- October 4, 2021: Asset Trends, Market Internals And Inflation Implication

- September 27, 2021: Newsletter Collection Update

- September 20, 2021: Benchmarking MyPlanIQ Fixed Income Bond Portfolios

- September 13, 2021: Benchmarking MyPlanIQ Tactical Portfolios

- August 30, 2021: Invest And Speculate: A Sensible Alternative To Buy And Hold

- August 23, 2021: Style ETF Portfolio Review

- August 16, 2021: Smart Factor ETFs Review

- August 9, 2021: Best Global Allocation Funds vs. MyPlanIQ ETF Portfolios

- August 2, 2021: Major Asset Trends And Market Internals

- July 26, 2021: Ultra Short Term Bond ‘Money Market’ Portfolio And Banking

- July 19, 2021: Take The Challenge of The ‘Best’ Balance Fund

- July 12, 2021: The Long Forgotten Bear Market Cycles

- June 28, 2021: Resuming Growth Trends Chaotically?

- June 21, 2021: Stocks Are Not Replacement Of Bonds

- June 14, 2021: Outperform The Best Performing PIMCO Income Bond Fund

- June 7, 2021: “Good” S&P Sectors

- May 17, 2021: Total Return Bond ETFs Review

- May 10, 2021: Financial Independence & Early Retirement

- May 3, 2021: Inflation, Sub Zero Interest Rate …

- April 26, 2021: The Best Active Fixed Income Funds Are Still Hard To Beat

- April 19, 2021: New And Old Useful Features

- April 12, 2021: Risk Parity Funds In Current Environment

- April 5, 2021: DoubleLine Shiller CAPE 10 Based Funds Update

- March 29, 2021: International Stocks vs. US Stocks

- March 22, 2021: Ultra Short Term Bond ETF Portfolio As A Money Market Fund

- March 15, 2021: Make Your Own Private Bank

- March 8, 2021: The Not So Orderly Market Rotation Amid Rising Bond Yields

- March 1, 2021: Average 20% Annual Returns: The Upper Bound Of Stock Investments?!

- February 22, 2021: Rising Bond Yields And Current Stock Trends

- February 8, 2021: Total Return Bond ETFs Review

- February 1, 2021: REITs And Major Asset Trends

- January 25, 2021: Industry ETFs And ARK ETFs Portfolios

- January 11, 2021: Smart Cash Management: Can I Just Withdraw From My Bond Portfolio?

- January 4, 2021: Our Investment Philosophy For 2021 And Beyond

- December 14, 2020: Style and Factor ETFs Portfolio Reviews

- December 7, 2020: A Really Long Term (30 Years) Stock Returns

- November 30, 2020: Higher Return Portfolios: Part 2

- November 16, 2020: Higher Return Portfolios

- November 9, 2020: Fixed Income Funds Update

- November 2, 2020: Polls Are Useless vs. This Investment Strategy Doesn’t Work!

- October 26, 2020: Recent Improvements

- October 19, 2020: REIT Indexes As Businesses

- October 12, 2020: Stock Indexes As Businesses

- October 5, 2020: Asset Trend Review

- September 28, 2020: Retirement Spending: Your Portfolio’s Volatility Matters

- September 21, 2020: Boring Utility Stocks Are Excellent Long Term Winners

- September 14, 2020: Surprised, Active Fixed Income Investors Have Done Better Than Stock Investors For The Last 20 Years!

- August 31, 2020: Investing In An Ultra-Low Return Environment

- August 24, 2020: Target Maturity Bond ETFs For Short Term Cash

- August 17, 2020: Newsletter Collection Update

- August 10, 2020: Fixed Income In A Speculative Era

- August 3, 2020: Sound Investment Strategies

- July 27, 2020: Total Return Bond Funds Update

- July 20, 2020: Divergence Between Value And Growth Stocks Everywhere

- July 13, 2020: Short Term Cash, Treasury Bills, CDs And Future Fixed Income

- July 6, 2020: Bond ETFs vs. Bond Mutual Funds

- June 29, 2020: Industry Sector ETF Rotation With Composite Momentum

- June 22, 2020: Industry Sector Rotation With Composite Momentum

- June 15, 2020: Advanced Minimum Equity Portfolios

- June 8, 2020: Recent Positive Developments

- June 1, 2020: Minimum Equity Portfolios

- May 18, 2020: Core Satellite Portfolios In The Current Pandemic

- May 11, 2020: Asset Trends Review

- May 4, 2020: The Real, Sensible And Wise Warren Buffett

- April 27, 2020: Total Return Bond Funds & Portfolios

- April 20, 2020: Multi-Factor ETFs and Rotation

- April 13, 2020: A Closer Look At 401(k) Investment Portfolios

- April 6, 2020: Long Term Stock Market Timing Since 1871 Revisited

- March 30, 2020: How Did Bond ETFs And Mutual Funds Fare In The Current Crisis?

- March 23, 2020: Chaos And Hope

- March 16, 2020: A Live Lesson

- March 9, 2020: Risk And Reward

- March 2, 2020: The Risk Of Coronavirus Outbreak

- February 24, 2020: Long Term Stock Valuation Based Investment Strategies

- February 10, 2020: Update On Short Term Cash, Treasury Bills and Brokered CDs

- February 3, 2020: Investment Landscape For Retirees And Would-be Retirees: Stocks

- January 27, 2020: Investment Landscape For Retirees And Would-be Retirees: Fixed Income

- January 13, 2020: Portfolio Performance: A Walk In The Past II

- January 6, 2020: Asset Outlook and Portfolio Strategies

- December 16, 2019: Q&As On Our Services

- December 9, 2019: Portfolio Constructions For Advanced Users

- December 2, 2019: Newsletter Collection Update

- November 25, 2019: Core ETFs or Core Mutual Funds Portfolios

- November 18, 2019: Introducing MyPlanIQ Asset Allocation Composite Strategy

- November 11, 2019: Market Indicator And Momentum

- November 4, 2019: Factor ETF Rotation

- October 28, 2019: Multi-factor ETFs vs. Equal Weight Multi-Factor Portfolios

- October 21, 2019: Multi-factor ETFs: Value And Momentum

- October 14, 2019: Low Volatility Factor ETFs

- October 7, 2019: Zero Commission Era Has Arrived, Is It Really That Good?

- September 30, 2019: Boosting Bond ETF Portfolio’s Return With Muni Bond ETFs

- September 23, 2019: Value ETFs

- September 16, 2019: Factor ETFs

- September 9, 2019: Momentum Factor Stock ETFs

- August 26, 2019: Employer 401k Match: Yet Another Free Lunch Not To Be Missed

- August 19, 2019: PIMCO Income Fund and Other Total Return Bond Funds Update

- August 12, 2019: Aggressive Fixed Income Portfolios?

- August 5, 2019: Long Term Investment Strategies And Short Term Market Noises

- July 29, 2019: Fixed Income Portfolios In A Lower Yield Environment

- July 22, 2019: Core Satellite Portfolios Balance Fluctuation

- July 15, 2019: Quality Stock Factor ETFs

- July 8, 2019: Surprise! Brokerages Make Most From Your Cash, Not Commissions

- July 1, 2019: Utilities Sector Review

- June 24, 2019: Asset Allocation Funds Review

- June 17, 2019: Latest Performance Comparison Among Several Advanced Strategies

- June 10, 2019: Money Market And Ultra Short Term Bond Funds

- June 3, 2019: What We Can Learn From The Seasonality Strategy

- May 20, 2019: Morningstar Portfolio Manager Awards

- May 13, 2019: Total Return Bond ETFs Review

- May 6, 2019: Global Allocation Revisited

- April 29, 2019: Asset Trend Review

- April 22, 2019: The Current State Of Fixed Income

- April 15, 2019: The Importance Of Fixed Income Returns For Retirement Spending

- April 8, 2019: Newsletter Collection Update

- April 1, 2019: S&P 500 As A Business

- March 25, 2019: Health Care Sector Review

- March 18, 2019: The Risk Of Stock Investing

- March 11, 2019: Consumer Staples Sector Review

- March 4, 2019: Global Stock Valuation Update

- February 25, 2019: ‘Bad’ Tactical Strategy

- February 11, 2019: “Best” Balanced Fund And Portfolios Revisited

- February 4, 2019: Cash And Money Market Funds: Interests And Safety

- January 28, 2019: Fixed Income Review

- January 14, 2019: Tactical Asset Allocation Portfolio Review

- January 7, 2019: Global Strategic Asset Allocation Portfolio Review

- December 17, 2018: Robinhood’s ‘Revolution’ Or Gimmick

- December 10, 2018: How Defensive Are REITs?

- December 3, 2018: Conservative Core Satellite Portfolio

- November 26, 2018: Allocation Mutual Fund Review

- November 19, 2018: Is The Recent Downtrend Sustainable?

- November 12, 2018: The Staggering Low Interest Rates From Big Banks

- November 5, 2018: The ‘Right’ Or ‘Wrong’ Decision

- October 29, 2018: Taxable Total Return Bond Plus Muni Bond Fund Based Portfolios

- October 22, 2018: DoubleLine Shiller CAPE 10 Based Fund Review

- October 15, 2018: Newsletter Collection Update

- October 8, 2018: Asset Trend Review

- October 1, 2018: Taxable vs. Tax Exempt High Yield Bonds

- September 24, 2018: High Yield Bonds In A Rising Rate Environment

- September 10, 2018: Value, Growth And Blend Stock Style Investing

- August 27, 2018: Money Market ETFs?

- August 20, 2018: How Momentum Investing Stacks Up?

- August 13, 2018: Total Return Bond ETF

- August 6, 2018: Fidelity Zero-Fee Index Funds

- July 30, 2018: Tax Efficient Portfolios

- July 23, 2018: Municipal Bond Funds And Portfolios

- July 16, 2018: A Guide To Conservative Portfolios

- July 9, 2018: Conservative Allocation Mutual Funds Based Portfolios

- July 2, 2018: Small Cap Stocks For The Long Term

- June 25, 2018: What Can We Learn From GE’s Removal From Dow Jones Index?

- June 18, 2018: The ‘Best’ Balanced Portfolio Continues To Excel

- June 11, 2018: Is 10 Year Long Enough For Portfolio Comparison?

- June 4, 2018: Action Plan: Risk Review For Investments

- May 21, 2018: Rising Rates, Consumer Staples And Stock Index

- May 14, 2018: Newsletter Collection Update

- May 7, 2018: Money Market Fund Taxonomy

- April 30, 2018: Momentum Investing Review

- April 23, 2018: Commodities In Current Environment

- April 16, 2018: Municipal Bonds As A Fixed Income Asset Class

- April 9, 2018: Exponential Or Compounding Nature In Investing

- April 2, 2018: Inside Of The Stock Chaos

- March 26, 2018: Total Return Bond Update

- March 19, 2018: Treasury Bills vs. Brokered CDs

- March 12, 2018: Defensive Conservative Portfolio Review

- March 5, 2018: Warren Buffett’s Advices

- February 26, 2018: Pros And Cons of Strategic And Tactical Portfolios In 2018

- February 12, 2018: Trend Review

- February 5, 2018: Market Selloff And Long Term Investing

- January 29, 2018: The New Addition To Our Total Return Bond Fund Candidates

- January 22, 2018: Where Are Bonds Heading?

- January 15, 2018: Tactical Portfolios Review

- January 8, 2018: Strategic Portfolios Review

- December 18, 2017: Record Highs And Risk

- December 11, 2017: Cash Return And Interest Rate Update

- December 4, 2017: Mutual Fund Star Ratings: Are They Useful?

- November 20, 2017: Thankful And Mindful

- November 13, 2017: Is This A Good Time For Retirees Or Would Be Retirees?

- November 6, 2017: Newsletter Collection Update

- October 30, 2017: Rising Interest Rates

- October 23, 2017: A Primer For Portfolios

- October 16, 2017: REITs As An Asset Class

- October 9, 2017: Conservative Portfolios Revisited

- October 2, 2017: The Role of Short Term Bond Funds

- September 25, 2017: Fees In Cash Investments

- September 18, 2017: Conservative Portfolios Review

- September 11, 2017: International Diversification Effect

- September 4, 2017: Invest And Speculate Revisited

- August 28, 2017: Total Return Bond Fund Portfolios: Where Do They Fit?

- August 21, 2017: Portfolio Performance: A Walk In The Past

- August 14, 2017: Fidelity Commission Free ETFs Update

- August 7, 2017: I Didn’t Learn Anything — Mistake vs. Temporary Underperformance

- July 31, 2017: Asset Classes And Fund Choices: A Primer

- July 24, 2017: Total Return Bond Fund Portfolios And Cash

- July 17, 2017: Long Term Stock Holding Periods For Retirement

- July 10, 2017: Half Year Asset Trend Review

- June 26, 2017: How To Beat The Best Balanced Allocation Fund

- June 19, 2017: Newsletter Collection Update

- June 12, 2017: A Mixed Bag Performance of Momentum Investing

- June 5, 2017: How To Start A New Portfolio

- May 29, 2017: Alternative Assets And Their Role In Portfolios

- May 22, 2017: Summer Seasonality And Portfolio Management

- May 15, 2017: Cash: Banking Or Investing?

- May 8, 2017: Holding Period of Long Term Timing Portfolios

- May 1, 2017: Debate on Risk vs. Volatility

- April 24, 2017: The Long Term Stock Market Timing Return Since 1871

- April 17, 2017: Risk vs. Volatility: Long Term Stock Market Returns

- April 10, 2017: Total Return Bond ETFs And Portfolios

- April 3, 2017: Quarter End Asset Trend Review

- March 27, 2017: Practical Consideration For IRAs And 401k Accounts

- March 20, 2017: Fund Fees: That’s (Still) Outrageous

- March 13, 2017: Long Term Stock Valuation Review

- March 6, 2017: Asset Classes for Retirement Investments

- February 27, 2017: Fidelity Total Bond Fund Review

- February 20, 2017: Long Term Stock Timing Based Portfolios And Their Roles

- February 13, 2017: Alternative Investment Portfolios Review

- February 6, 2017: Tax Free Municipal Bond Investments Review

- January 30, 2017: Brokerage Specific Conservative Portfolios

- January 23, 2017: Fixed Income Portfolio Review

- January 16, 2017: Long Term Trend Following Portfolio Review

- January 9, 2017: Tactical Asset Allocation Review

- January 3, 2017: Strategic Asset Allocation Review

- December 12, 2016: Enhanced Index Funds

- December 5, 2016: Review Of Broad Base Core Mutual Funds For Brokerages

- November 28, 2016: Core Index ETFs Review

- November 21, 2016: International Exposure Of U.S. Large Companies

- November 14, 2016: Asset Trends After The Election

- November 7, 2016: Rising Rate And Current Bond Trend

- October 31, 2016: Economy Power And Long Term Stock Returns

- October 24, 2016: Current Commodity Trend And Managed Futures

- October 17, 2016: Investment Mistakes And Good Or Bad Investment Strategies

- October 10, 2016: Momentum Investing Review

- October 3, 2016: Survey & Feedback

- September 26, 2016: Fixed Income Investing: Actively Managed Funds vs. Index Funds

- September 19, 2016: Stock Investing: Actively Managed Funds vs. Index Funds

- September 12, 2016: Newsletter Update

- September 5, 2016: Overvalued Markets And Long Term Timing Strategies

- August 29, 2016: Your 401K Finally Draws Attention

- August 22, 2016: Inflation Protected Securities TIPS For Current Overvalued Markets

- August 15, 2016: Risk On: Emerging Market Stocks And Small Cap Stocks

- August 8, 2016: Portfolio Construction Using Stock ETFs And Bond Mutual Funds

- August 1, 2016: Adding Value To Your Own Investments

- July 25, 2016: Tactical Asset Allocation Funds Review

- July 18, 2016: Strategic Asset Allocation & Lazy Portfolio Review

- July 11, 2016: Asset Trend Review

- June 27, 2016: Secular Cycles For Tactical And Strategic Investment Strategies

- June 20, 2016: A World of Debt

- June 13, 2016: Managed Futures For Portfolio Building

- June 6, 2016: Newsletter Summary

- May 30, 2016: Swensen Portfolio And Permanent Portfolios

- May 23, 2016: AAII Article And Some Web Changes

- May 16, 2016: The PIMCO (Dis)Advantages

- May 9, 2016: Boost Your Dull Summer Investments

- May 2, 2016: Low Cost Index Fund Investing

- April 25, 2016: Tax Free Municipal Bond Funds & Portfolios

- April 18, 2016: Asset Class Trend Review

- April 11, 2016: Construction of Sound And Conservative Portfolios

- March 28, 2016: Total Return Bond ETFs Review

- March 21, 2016: Small And Large Company Stock Performance In Different Economic Expansion Cycles

- March 14, 2016: Are Tactical And Timing Strategies Losing Steam?

- March 7, 2016: Defined Maturity Bond Fund Analysis

- February 29, 2016: Smart Strategic Asset Allocation Rebalance When Market Trend Changes

- February 22, 2016: Be Cash Smart

- February 15, 2016: Bond ETF Portfolios

- February 8, 2016: Newsletter Collection Update

- February 1, 2016: Total Return Bond Fund Portfolios In A Volatile Period

- January 25, 2016: Alternative Portfolios Review

- January 18, 2016: Strategic Asset Allocation: A Cautious Outlook

- January 11, 2016: Review Of Trend Following Tactical Asset Allocation

- January 4, 2016: What Worked And Didn’t In 2015

- December 21, 2015: Distressed Assets

- December 14, 2015: High Yield Bonds And Their Correlation With Stocks

- December 7, 2015: Diversification And Global Allocation

- November 30, 2015: Investors and Speculators Combined

- November 23, 2015: Active Stock Fund Performance Consistency

- November 16, 2015: Permanent, Risk Parity And Alternative Portfolios Review

- November 9, 2015: Broad Base Core Mutual Fund Review

- November 2, 2015: Broad Base Index Core ETFs Review

- October 26, 2015: Total Return Bond Fund Review

- October 19, 2015: Advanced Portfolio Review

- October 12, 2015: What About Commodities?

- October 5, 2015: Core Satellite Portfolios In A 401k Account

- September 28, 2015: Risk Managed Strategic Asset Allocation Portfolios Revisited

- September 21, 2015: Quest For The Best Investment Strategy

- September 14, 2015: Core Satellite Portfolios In Market Turmoil

- September 7, 2015: Market Rout Creates An Opportunity to Reposition Your Portfolios

- August 31, 2015: Review of Asset Allocation Funds and Portfolios

- August 24, 2015: Market Rout And Your Portfolios

- August 17, 2015: ETF or Mutual Fund Based Portfolios

- August 10, 2015: Updated Newsletter Collection

- August 3, 2015: Slippery Asset Trends

- July 27, 2015: Performance Dispersion Among Momentum Based Portfolios

- July 20, 2015: Global Balanced Portfolio Benchmarks

- July 13, 2015: Pain in Tactical Portfolios

- July 6, 2015: Fixed Income Total Return Bond Funds In Strategic Asset Allocation Portfolios

- June 29, 2015: Core ETF Commission Free Portfolios

- June 22, 2015: Secular Asset Trends

- June 15, 2015: Giving Up Bonds?

- June 1, 2015: Summer Blues?

- May 26, 2015: Cash, Bonds and Stocks In A Rising Rate Environment

- May 18, 2015: Portfolio Update

- May 11, 2015: Pain in Fixed Income?

- May 4, 2015: The Balanced Stock and Long Term Treasury Bond Portfolios

- April 27, 2015: Long Term Treasury Bond Behavior

- April 20, 2015: 529 College Savings Plan Rebalance Policy Change

- April 13, 2015: Total Return Bond Funds As Smart Cash

- April 6, 2015: The Low Return Environment

- March 30, 2015: Brokerage Specific Core Mutual Fund Portfolios 2

- March 23, 2015: Investment Arithmetic for Long Term Investments

- March 16, 2015: Brokerage Specific Core Mutual Fund Portfolios

- March 9, 2015: Newsletter Collection Update

- March 2, 2015: Total Return Bond ETFs

- February 23, 2015: Why Is Global Tactical Asset Allocation Not Popular?

- February 16, 2015: Where Are Permanent Portfolios Going?

- February 9, 2015: How Have Asset Allocation Funds Done?

- February 2, 2015: Risk Management Everywhere

- January 26, 2015: Composite Portfolios Review

- January 19, 2015: Fixed Income Investing Review

- January 12, 2015: How Does Trend Following Tactical Asset Allocation Strategy Deliver Returns

- January 5, 2015: When Forecast Fails

- December 22, 2014: Long Term Asset Returns: How Long Is Long?

- December 15, 2014: Beaten Down Assets

- December 8, 2014: Implementing Core Asset Portfolios In a Brokerage

- December 1, 2014: Two Key Issues of Investment Strategies

- November 24, 2014: Holiday Readings

- November 17, 2014: Retirement Spending Portfolios Update

- November 10, 2014: Fixed Income Or Cash

- November 3, 2014: Asset Trend Review

- October 27, 2014: Investment Loss, Mistakes And Market Cycles

- October 20, 2014: Strategic Portfolios With Managed Volatility

- October 13, 2014: Embrace Volatility

- October 6, 2014: Tips For 401k Open Enrollment

- September 29, 2014: What Can We Learn From Bill Gross’ Departure From PIMCO?

- September 22, 2014: Why Total Return Bond Funds?

- September 15, 2014: Equity And Total Return Bond Fund Composite Portfolios

- September 8, 2014: Momentum Based Portfolios Review

- September 1, 2014: Risk & Diversification: Mint.com Interview

- August 25, 2014: Remember Risk

- August 18, 2014: Consistency, The Most Important Edge In Investing: Tactical Case

- August 11, 2014: What To Do In Overvalued Stock Markets

- August 4, 2014: Is This The Peak Or Correction?

- July 28, 2014: Stock Musings

- July 21, 2014: Permanent Portfolios & Four Pillar Foundation Based Framework

- July 14, 2014: Composite Portfolios Review

- July 7, 2014: Portfolio Behavior During Market Corrections

- June 30, 2014: Half Year Brokerage ETF and Mutual Fund Portfolios Review

- June 23, 2014: Newsletter Collection Update

- June 16, 2014: There Are Always Lottery Winners

- June 9, 2014: The Arithmetic of Investment Mistakes

- June 2, 2014: Tips On Portfolio Rebalance

- May 26, 2014: In Praise Of Low Cost Core Asset Class Based Portfolios

- May 19, 2014: Consistency, The Most Important Edge In Investing: Strategic Case

- May 12, 2014: How To Handle An Elevated Overvalued Market

- May 5, 2014: Asset Allocation Funds Review

- April 28, 2014: Now The Economy Backs To The ‘Old Normal’, Should Our Investments Too?

- April 21, 2014: Total Return Bond Investing In The Current Market Environment

Diversified Asset Allocation Portfolios For Your Plans

Diversified Asset Allocation Portfolios For Your Plans