-

General Dynamics 401(k) Review: 100% Match Up to 6% With $325 Million in Employer Contributions

General Dynamics matches 100% of the first 6% of compensation, contributing $325.5M annually for 46,065 participants with Roth 401(k) options available.

-

Walmart 401(k) Plan Review: 100% Match on 6% for 1.9 Million Employees

An hourly associate earning $30,000 a year would need to contribute 6%, or $1,800 annually, to get the full $1,800 employer match. For a Walmart associate…

-

FedEx Office 401(k) Review: An 8% Employer Match With Immediate Vesting

Fedex will contribute 8% of your pay, which is $4,000. A 6% contribution equals $4,500 per year.

-

Caterpillar 401(k) Savings Plan Review: A 100% Match on 6% and $487 Million in Employer Contributions

The plan’s 2024 public filing disclosures shows employer contributions of $487 million against participant contributions of $456 million. That is a 106.9 percent…

-

Variable Annuity vs 401(k) vs IRA: A Beginner’s Guide

Variable annuities are rarely a substitute for 401(k)s and IRAs. This guide breaks down fees, tax treatment, and when a plain vanilla variable annuity like Vanguard’s might make sense—plus why a taxable brokerage account often wins anyway.

-

Your IRA Can Buy ETFs That Rival Even the Lowest-Cost Plan Funds

You could almost find the lowest cost reputable ETFs that rival against those lowest funds offered in some large retirement plans.

-

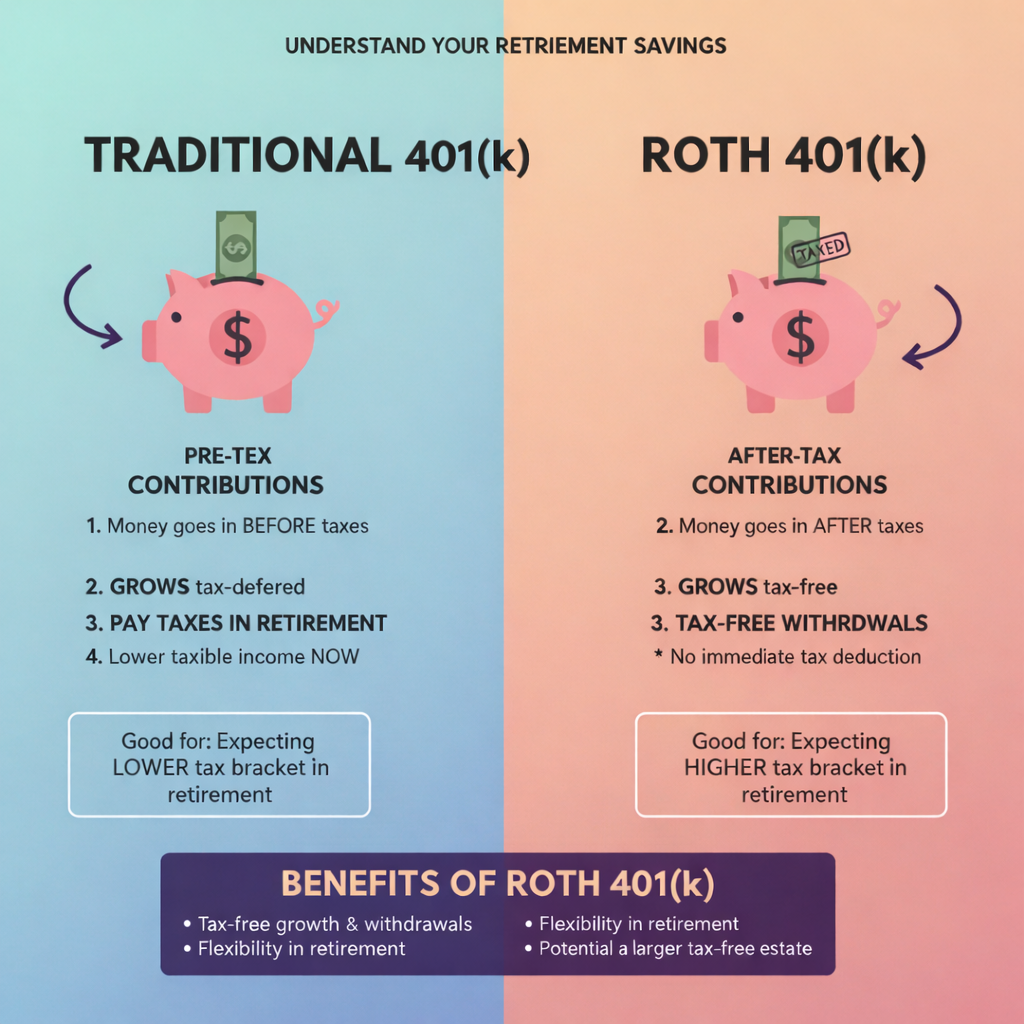

Understand Mega Backdoor Roth Conversion

- Latest in Retirement Savings & Personal Finance

- Understand Mega Backdoor Roth Conversion

- Tools & Tips: Backdoor Roth IRA Pro-Rata Conversion Calculator

- Market Overview

-

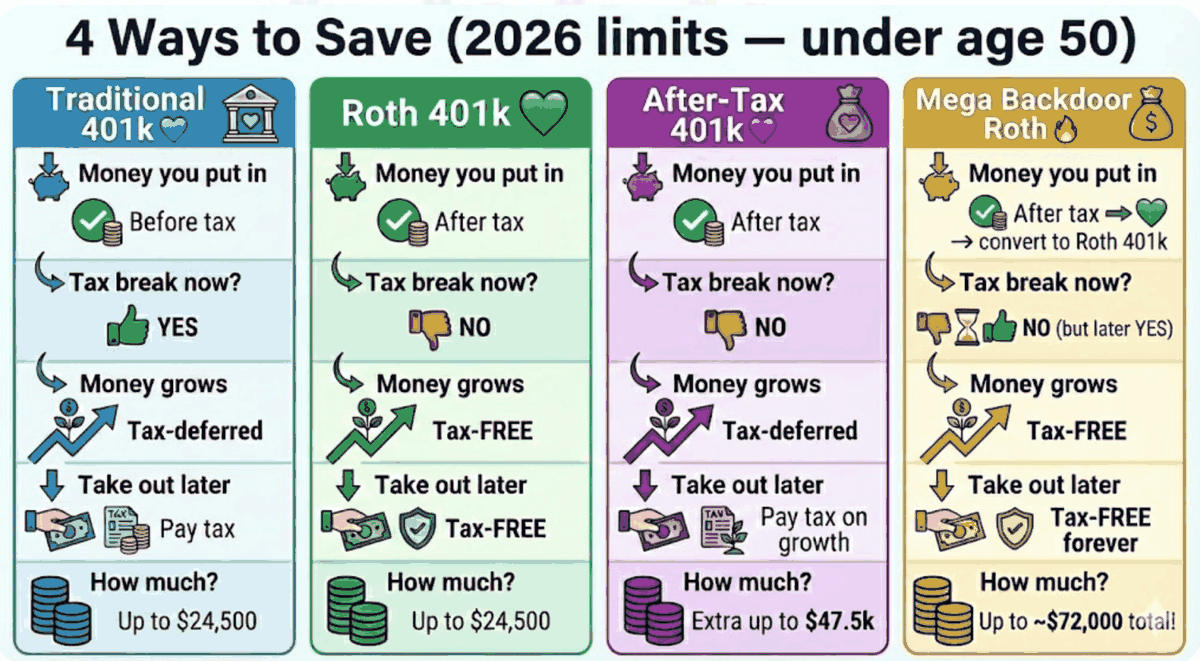

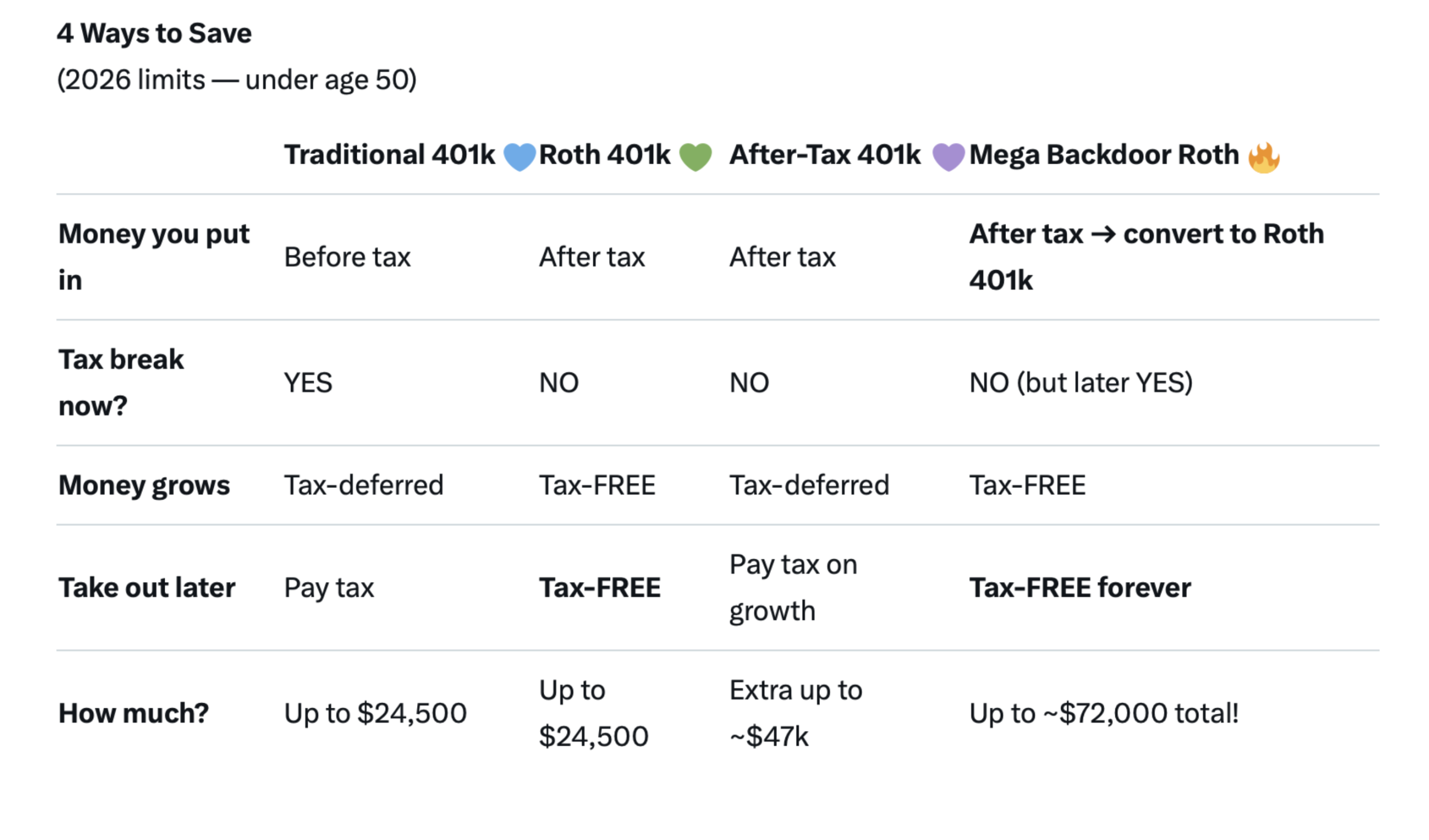

Mega Backdoor Roth Infographic

The infographic to illustrate the differences among traditional 401k, Roth 401k, After Tax 401k and Mega Backdoor Roth Conversion.

-

IRS Is Giving Out Money

- Latest in Retirement Savings & Personal Finance

- IRS Is Giving Out Money

- Tools & Tips: RSU (Restricted Stock Unit) Calculator

- Market Overview

-

The Federal Reserve Bank and Your Money

- Latest in Retirement Savings & Personal Finance

- The Federal Reserve Bank and Your Money

- Tools & Tips: 401(k) Investment Assistant

- Market Overview

-

2026 Tax Season Begins Today

- Latest in Retirement Savings & Personal Finance

- 2026 Tax Season Begins Today

- Tools & Tips: Traditional 401(K) vs. Roth 401(K)

- Market Overview

-

Useful Tips for 401(k)s, IRAs, and RMDs in the New Year

- Latest in Retirement Savings & Personal Finance

- Useful Tips for 401(k)s, IRAs, and RMDs in the New Year

- Tools & Tips: Roth IRA Compounding

- Market Overview

-

The $7,000 Roth IRA Myth, Why It Is a Bigger Deal Than People Think

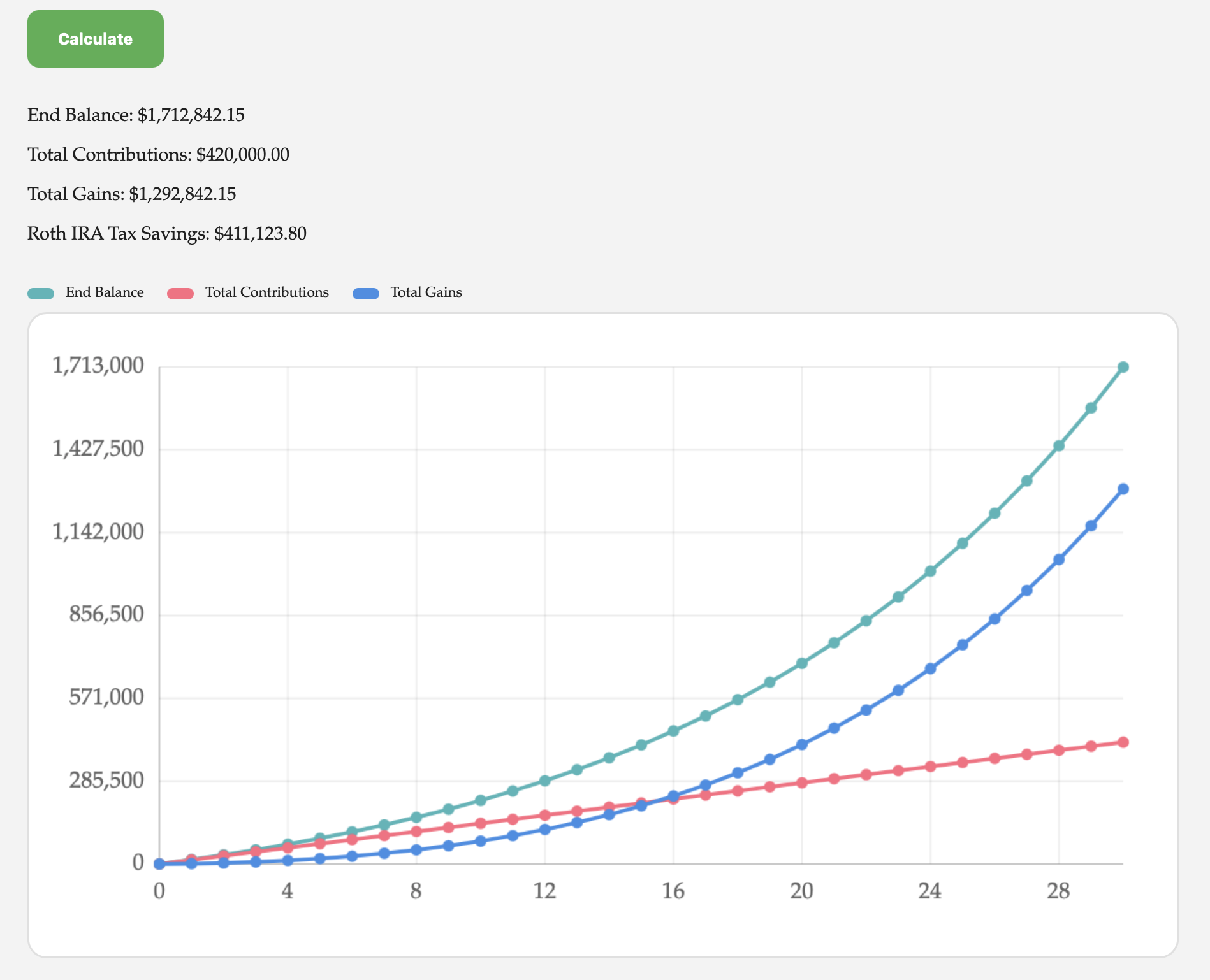

Many people look at the $7,000 annual Roth IRA limit and immediately dismiss it. Too small, not impactful, not worth the hassle. Big mistake! Let’s use a simple example. A husband and wife each contribute $7,000 a year, so $14,000 total, from age 30 to 60. That is 30 years of steady investing at an assumed 8 percent return. Total contributions come to $420,000. By age 60, that Roth balance grows to about $1.6 million. Roughly $1.16 million of that is pure growth, and it comes out tax free. If you live in a no state tax environment, you just avoided federal long term capital gains and the extra 3.8 percent surtax on investment income, already a meaningful number. Now layer in a high tax state. At an 8 percent state tax rate, that same $1.16 million of gains would have faced another large haircut (actually like $411K tax savings). The Roth just simply protects such a big chunk of your gain. The following are results from our Investment Return Calculator: And it does not stop there. Most people do not touch Roth money first. They let it keep compounding while spending from pre tax or taxable accounts. Let that same Roth grow another 10 years, untouched, at the same 8 percent. By age 70, it is worth roughly $3.9 million. Now you are looking at close to $3.3 million of gains that will never be taxed. In a zero state tax scenario, that already avoids a large federal tax bill. In an 8 percent state tax scenario, the difference becomes even more dramatic: a $1 million savings. This is where people underestimate the impact. The contribution feels small. The tax free compounding over decades is not. This is real money, not theoretical. High income earners often respond with another objection. Fine, but my income is too high to contribute to a Roth IRA anyway. Not really. This is where the backdoor Roth comes in. The process is simple in concept. You contribute to a traditional IRA using after tax dollars, since there is no income limit on contributions. Then you convert that contribution to a Roth IRA. If done correctly and promptly, there is little to no tax cost. The key rule is that you cannot have other pre tax IRA balances sitting around, including SEP or SIMPLE IRAs, or the conversion becomes partially taxable. Many people solve this by rolling old IRAs into a 401(k) first. Once set up, this becomes a repeatable annual process. So the real question is not whether the Roth is too small to matter. It is whether you want to keep paying taxes on millions of dollars of future growth, or quietly opt out while you still can.

-

Ultimate 2026 Retirement Playbook for 401(k)s & IRAs

Extremely use tips to maximizing 401(k) match, RMDs and IRA tactics

-

New Year Resolutions for Your Personal Finance

- Latest in Retirement Savings & Personal Finance

- New Year Resolutions for Your Personal Finance

- MyPlanIQ 2026 Market Outlook

-

2025 Crystal Ball Market Prediction Scorecard

- Latest in Retirement Savings & Personal Finance

- Stock Market Bubble & Retirement Savings

- Tools & Tips: Retirement Spending Calculator

- Market Overview

-

Personal Finance Year End Check List

- Latest in Retirement Savings & Personal Finance

- Personal Finance Year End Check List

- Tools & Tips: 12% Tax Bracket Is the Sweet Spot for Roth IRA Conversion

- Market Overview

-

How A Valuation Driven Bear Market Looks Like

- Latest in Retirement Savings & Personal Finance

- Stock Market Bubble & Retirement Savings

- Tools & Tips: Retirement Spending Calculator

- Market Overview

-

Retirement Plan Contribution Limits in 2026

Comprehensive retirement plans (401(k), 403(b, 457(b), Solo 401(k), SEP IRA, SIMPLE IRA, IRA, Roth IRA, TSP, HSA etc.) contribution limits for 2026

-

How Retirement Savings Can Quietly Reduce Your Student Loan Payments

Increasing Retirement Savings such as 401(k) can help reduce your monthly student repayment if you are on the federal IBR program. But