Re-balance Cycle Reminder All MyPlanIQ’s newsletters are archived here.

Regular AAC (Asset Allocation Composite), SAA and TAA portfolios are always rebalanced on the first trading day of a month. the next re-balance will be on Friday May 1, 2020.

Please note: As of March 1, 2020, we officially phased out our old rebalance calendar for both SAA and TAA. They are now always rebalanced on the first trading day of a month.

As a reminder to expert users: advanced portfolios are still re-balanced based on their original re-balance schedules and they are not the same as those used in Strategic and Tactical Asset Allocation (SAA and TAA) portfolios of a plan.

Total Return Bond Funds & Portfolios

We have featured and monitored our total return bond fund portfolios for about 10 years now. These portfolios are listed on our Fixed Income page. In light of the recent volatile events in financial markets, it’s a good time to review the latest performance of the candidate funds and the portfolios.

Total return bond mutual funds

Our fixed income portfolios are based on the momentum fund selection strategy utilized in MyPlanIQ portfolios. Every month, the strategy chooses a fund with the highest momentum score among a list of candidate funds. In the event that all of the candidate funds have negative momentum scores, cash or money market fund is chosen. The candidate funds are total return bond funds (and some intermediate term corporate bond funds) whose managers have been named at least once as Fixed Income Manager of The Year by Morningstar. These funds should be no-load (or load waived), no transaction fee in a brokerage. For example, the following are the candidate funds for Schwab Total Return Bond:

| PBDAX | PIMCO Investment Grade Corp Bd A |

| PDBZX | Prudential Total Return Bond Z |

| PONAX | PIMCO Income A |

| DLTNX | DoubleLine Total Return Bond N |

| WABRX | Western Asset Core Bond R |

| TGMNX | TCW Total Return Bond N |

| PTTAX | PIMCO Total Return A |

| MWTRX | Metropolitan West Total Return Bond M |

| LSBRX | Loomis Sayles Bond Retail |

All of them are available in Schwab as no load and no transaction fee. In general, these funds are retail class shares so that they have a ver low minimum (such as $1000 to $3000). Furthermore, our strategy automatically enforces the minimum holding period and round trip limit restriction imposed by a brokerage. Most funds do have three month minimum holding period requirement.

The rationale to only use total return bond funds managed by great managers is that excellent fixed income manager tend to have a sustainable outperformance track record and thus their funds are more suitable for a momentum based strategy.

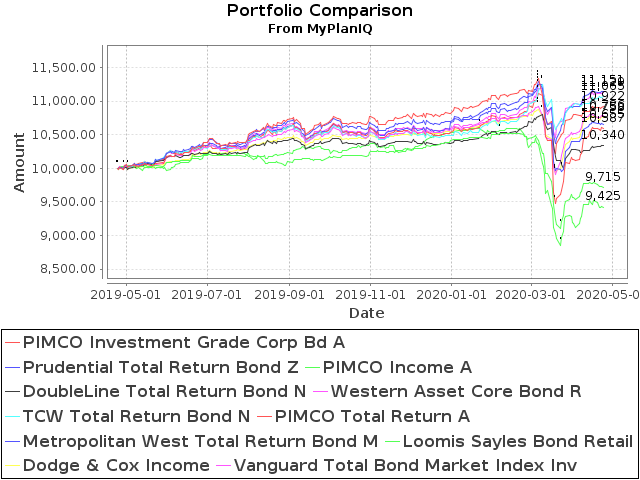

Let’s first look at these funds’ recent performance:

| Fund | YTD Return** |

1Yr AR | 3Yr AR | 5Yr AR | 5Yr Sharpe | 10Yr AR | 15Yr AR |

|---|---|---|---|---|---|---|---|

| PBDAX (PIMCO Investment Grade Corp Bd A) | -2.1% | 5.9% | 4.0% | 3.7% | 0.57 | 5.4% | 6.0% |

| PDBZX (Prudential Total Return Bond Z) | -0.4% | 6.5% | 4.4% | 3.6% | 0.66 | 4.9% | 5.4% |

| PONAX (PIMCO Income A) | -6.6% | -2.7% | 1.6% | 3.2% | 0.69 | 6.7% | |

| DLTNX (DoubleLine Total Return Bond N) | -0.2% | 3.5% | 3.0% | 2.5% | 0.64 | 5.1% | |

| WABRX (Western Asset Core Bond R) | 2.0% | 7.9% | 4.4% | 3.3% | 0.65 | ||

| TGMNX (TCW Total Return Bond N) | 5.5% | 10.6% | 4.9% | 3.4% | 0.72 | 4.8% | 5.6% |

| PTTAX (PIMCO Total Return A) | 3.8% | 9.2% | 4.6% | 3.2% | 0.62 | 3.8% | 4.9% |

| MWTRX (Metropolitan West Total Return Bond M) | 4.4% | 11.5% | 5.3% | 3.6% | 0.79 | 4.8% | 5.5% |

| LSBRX (Loomis Sayles Bond Retail) | -10.5% | -5.8% | -1.0% | 0.2% | -0.1 | 3.4% | 4.8% |

| DODIX (Dodge & Cox Income) | 2.1% | 7.6% | 4.6% | 3.7% | 1 | 4.4% | 4.9% |

| VBMFX (Vanguard Total Bond Market Index Inv) | 5.1% | 11.3% | 5% | 3.5% | 0.72 | 3.8% | 4.3% |

1 Year Total Return Chart:

Unfortunately, YTD (Year To Date), other than TGMNX, all other funds underperformed VBMFX, the total bond market index fund. In particular, Loomis Sayles fund LSBRX was hit hardest, losing -10.5% this year, while PIMCO’s two corporate bond centric funds: PIMCO investment grade corporate bond fund PBDAX and PIMCO Income fund PONAX also suffered from some substantial loss in March this year. The main culprit here is their outsized exposure to high yield bonds (LSBRX) and even investment grade corporate bonds (PBDAX and PONAX) while VBMFX has a very large exposure in Treasury bonds. In fact, if the Federal Reserve didn’t intervene bond markets in the unprecedented way (buying Treasury, investment grade corporate bonds and now even buying high yield bond ETFs), these funds would have experienced even more serious losses and might not recover so quickly.

The current crisis also caused most of these excellent funds to lag behind the index fund VBMFX for the past 1 and 3 years. Most of them now have similar 5 year returns compared with VBMFX. However, majority of them still outperform VBMFX in a longer period such as 10 years or 15 years time frame.

What we can learn from this crisis is that other than Treasury bonds, all other debts can be severely impacted in a crisis. Bonds as ‘safe’ asset class are not as safe as one would expect. Furthermore, regardless how safe a fund is or how excellent a fund manager is, there should be a fail safe mechanism in a portfolio to switch to safer investments or cash in the event of severe downturn. Currently, though the Federal Reserve’s unconventional intervention has been able to avoid the severe bond market crisis for now, whether that can sustain remains to be a question as the fundamentals for underlying businesses have been damaged and are now weak.

The performance of total return bond portfolios

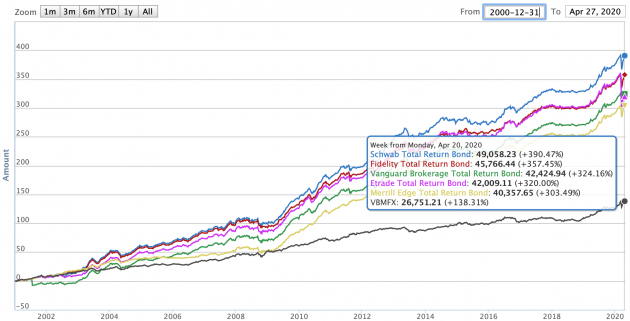

The following major brokerage specific portfolios are very similar:

| Ticker/Portfolio Name | YTD Return** |

1Yr AR | 3Yr AR | 5Yr AR | 10Yr AR | 15Yr AR |

|---|---|---|---|---|---|---|

| Schwab Total Return Bond | 3.5% | 12.0% | 6.1% | 5.2% | 6.6% | 7.8% |

| Fidelity Total Return Bond | 3.5% | 12.0% | 5.7% | 4.7% | 6.3% | 7.4% |

| Vanguard Brokerage Total Return Bond | 3.5% | 12.0% | 6.1% | 5.2% | 6.6% | 7.9% |

| Etrade Total Return Bond | -5.4% | 2.3% | 3.0% | 3.3% | 5.5% | 7.2% |

| Merrill Edge Total Return Bond | 3.5% | 12.0% | 6.1% | 4.6% | 7.5% | 7.3% |

| PTTRX (PIMCO Total Return Instl) | 3.8% | 9.6% | 5.0% | 3.6% | 4.2% | 5.3% |

| DLTNX (DoubleLine Total Return Bond N) | -0.2% | 3.5% | 3.0% | 2.5% | 5.1% | |

| VBMFX (Vanguard Total Bond Market Index Inv) | 5.1% | 11.3% | 5.0% | 3.5% | 3.8% | 4.3% |

The following chart shows the total returns since 2001:

A few comments:

- All of the portfolios have outperformed VBMFX for the past 10 years, 15 years and since 2001. For the past 15 years, the annualized excessive returns of these portfolios over VBMFX are up to 3.9%. The Etrade portfolio, even after this year’s underperformance, still had 2.9% excessive annualized return over VBMFX (7.2% vs. 4.3%) for the past 15 years.

- In fact, other than the Etrade portfolio, all other portfolios have outperformed for 1, 3, 5, 10, 15 years and since 2001.

- The portfolios did worse year to date. The worst is Etrade portfolio that lost -5.4% up to now.

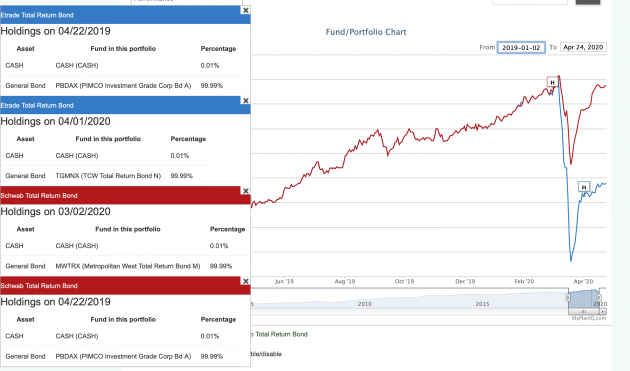

A closer examination reveals that Etrade portfolio’s candidate funds have MWTRX missing. This is because MWTRX is not available as a no transaction fee (NTF) fund in Etrade. The following chart compares the historical holdings of both Schwab Total Return Bond and the Etrade portfolio:

We can see that until 3/22/2020, both portfolios had the exact same holding (PBDAX) since 4/22/2019. In the rebalance on 3/2/2020, Schwab portfolio switched its holding to MWTRX. Since MWTRX is not available in Etrade as an NTF fund, the portfolio had to wait till the next rebalance on 4/1/2020 to switch its holding to TGMNX. Unfortunately, this one month delay proved to be costly: PBDAX suffered from a large loss in March because of the wide spread pessimism on investment grade corporate bonds.

Notice that MWTRX had year to date return 4.4%, just behind TGMNX and is the second highest among the total return bond funds listed in the previous table.

The above example shows the sensitivity of candidate funds. However, the long term outperformance over bond index funds has been so great such that the recent underperformance in the Etrade portfolio seems to be still limited.

Short term trading restriction for mutual fund (401k) portfolios

The following question posted by a user might be of interests to many mutual fund portfolio users, in particular 401k portfolios.

Question: Many 401k plans have minimum 30 day holding period for mutual funds. Some of them also have round trip trading limit. Since February only has 28 days (or at most 29 days in a leap year), it’s likely to have issues if there is a rebalance at the end of February. How to handle this?

Answer: In the case when a 30 day thing is violated, it’s really a case by case decision to decide whether you want to postpone the rebalance a few days later (that’s really only for Feb.) and hope there won’t be another dramatic rebalance in March.

Other practical thing is that: if it’s not a dramatic equity/bond allocation change, you can always wait it out without much performance impact: for example, if a rebalance calls for changing from an equity fund A to another equity fund B, you can always wait for a few days if 30 day restriction is still in effect. Similarly, bond to bond change can be a bit lax.

The only combination case that one really needs to care is for equity to bond rebalance (just like in the end of Feb. this year): for that, you have to make a case by case decision to decide to go for the rebalance on the exact date or to postpone for two days.

By the way, even if you are denied to invest in a particular fund for a year, you can always find a substitute in most cases to invest. The return effect should be minimal as long as the major stock/bond allocations are maintained.

Market overview

It seems like people are getting more anxious and somewhat optimistic on reopening economy, judging from stock market behavior: stocks are hanging around the recent high levels. Some states like Georgia and Texas have opened or planned to open part of their economy. We are, however, more cautious on the following two counts: first, as we stated before, even in the most optimistic scenario, it will still take several more months for the economy to be fully open. We believe, by that time, global and the US economy will be materially impaired to the extent it takes time to recover. This is because the shut down damages many businesses and supply chains in an already debt heavy corporate environment. The damages will further cloud businesses’ outlook that in turn will affect business growth planning.

Secondly, though investors seem to totally write off the previous quarter earnings: based on Factset, with 24% of the companies in the S&P 500 reporting actual results, the blended (actual and expected) earnings for Q1 now stands on -15.8%. Since many companies withdrew their next quarter or this year’s earnings projections, investors are somewhat relying on a more subjective guess on this year’s earnings growth (which analysts now expect -15.2% decline for 2020 full year). For now, it looks like investors are mostly pinning hope on 2021’s strong recovery to justify current hefty stock valuation. It’s very likely any further disruption on the pandemic side such as vaccination delay, cure development hiccups and second wave of the pandemic will destabilize this market.

Regardless of our subjective opinions, we shall stick to our strategies and act accordingly. This means:

- For strategic allocation (buy and hold) investors, ignore the current market behavior. Remember, as what we have emphasized numerous times, when you choose and commit to a strategic portfolio, you essentially know and commit that your investment horizon (or the time you need to utilize this capital) is 20 years or longer. As we pointed out, if your investments are those diversified (index) funds such as an S&P 500 index fund (VFINX, for example), you know your money is in some solid ‘business’ that eventually (20 years later) will deliver some reasonable returns. As long as you are comfortable with this thesis, you should sit tight and forget about the current gyration.

- For tactical investors, again, you have to ignore the current market noise. Furthermore, you should follow your strategy rigorously, especially in a time like this. Human emotion, both optimistic and pessimistic, and human desire, both greedy and fearful, are your worst enemies. This has been shown to be true time and time again.

For more detailed current market trends, please refer to 360° Market Overview.

In terms of investments, stocks are somewhat cheaper. Investors should not be swayed by the current market volatility and economic distress, instead, they should stand ready to take advantage of the opportunities. For most Americans, we offer the following Winston Churchill’s remark made in the darkest days of World War II: “The Americans will always do the right thing, but only after they have tried everything else.” As a country, the US (and the rest of the world) will get over this, as always, even after stumbles. The past development has been very supportive to our optimistic long term view so far.

We again would like to stress for any new investor and new money, the best way to step into this kind of markets is through dollar cost average (DCA), i.e. invest and/or follow a model portfolio in several phases (such as 2 or 3 months) instead of the whole sum at one shot.

Enjoy Newsletter

How can we improve this newsletter? Please take our survey

–Thanks to those who have already contributed — we appreciate it.

Latest Articles

- April 20, 2020: Multi-Factor ETFs and Rotation

- April 13, 2020: A Closer Look At 401(k) Investment Portfolios

- April 6, 2020: Long Term Stock Market Timing Since 1871 Revisited

- March 30, 2020: How Did Bond ETFs And Mutual Funds Fare In The Current Crisis?

- March 23, 2020: Chaos And Hope

- March 16, 2020: A Live Lesson

- March 9, 2020: Risk And Reward

- March 2, 2020: The Risk Of Coronavirus Outbreak

- February 24, 2020: Long Term Stock Valuation Based Investment Strategies

- February 10, 2020: Update On Short Term Cash, Treasury Bills and Brokered CDs

- February 3, 2020: Investment Landscape For Retirees And Would-be Retirees: Stocks

- January 27, 2020: Investment Landscape For Retirees And Would-be Retirees: Fixed Income

- January 13, 2020: Portfolio Performance: A Walk In The Past II

- January 6, 2020: Asset Outlook and Portfolio Strategies

- December 16, 2019: Q&As On Our Services

- December 9, 2019: Portfolio Constructions For Advanced Users

- December 2, 2019: Newsletter Collection Update

- November 25, 2019: Core ETFs or Core Mutual Funds Portfolios

- November 18, 2019: Introducing MyPlanIQ Asset Allocation Composite Strategy

- November 11, 2019: Market Indicator And Momentum

- November 4, 2019: Factor ETF Rotation

- October 28, 2019: Multi-factor ETFs vs. Equal Weight Multi-Factor Portfolios

- October 21, 2019: Multi-factor ETFs: Value And Momentum

- October 14, 2019: Low Volatility Factor ETFs

- October 7, 2019: Zero Commission Era Has Arrived, Is It Really That Good?

- September 30, 2019: Boosting Bond ETF Portfolio’s Return With Muni Bond ETFs

- September 23, 2019: Value ETFs

- September 16, 2019: Factor ETFs

- September 9, 2019: Momentum Factor Stock ETFs

- August 26, 2019: Employer 401k Match: Yet Another Free Lunch Not To Be Missed

- August 19, 2019: PIMCO Income Fund and Other Total Return Bond Funds Update

- August 12, 2019: Aggressive Fixed Income Portfolios?

- August 5, 2019: Long Term Investment Strategies And Short Term Market Noises

- July 29, 2019: Fixed Income Portfolios In A Lower Yield Environment

- July 22, 2019: Core Satellite Portfolios Balance Fluctuation

- July 15, 2019: Quality Stock Factor ETFs

- July 8, 2019: Surprise! Brokerages Make Most From Your Cash, Not Commissions

- July 1, 2019: Utilities Sector Review

- June 24, 2019: Asset Allocation Funds Review

- June 17, 2019: Latest Performance Comparison Among Several Advanced Strategies

- June 10, 2019: Money Market And Ultra Short Term Bond Funds

- June 3, 2019: What We Can Learn From The Seasonality Strategy

- May 20, 2019: Morningstar Portfolio Manager Awards

- May 13, 2019: Total Return Bond ETFs Review

- May 6, 2019: Global Allocation Revisited

- April 29, 2019: Asset Trend Review

- April 22, 2019: The Current State Of Fixed Income

- April 15, 2019: The Importance Of Fixed Income Returns For Retirement Spending

- April 8, 2019: Newsletter Collection Update

- April 1, 2019: S&P 500 As A Business

- March 25, 2019: Health Care Sector Review

- March 18, 2019: The Risk Of Stock Investing

- March 11, 2019: Consumer Staples Sector Review

- March 4, 2019: Global Stock Valuation Update

- February 25, 2019: ‘Bad’ Tactical Strategy

- February 11, 2019: “Best” Balanced Fund And Portfolios Revisited

- February 4, 2019: Cash And Money Market Funds: Interests And Safety

- January 28, 2019: Fixed Income Review

- January 14, 2019: Tactical Asset Allocation Portfolio Review

- January 7, 2019: Global Strategic Asset Allocation Portfolio Review

- December 17, 2018: Robinhood’s ‘Revolution’ Or Gimmick

- December 10, 2018: How Defensive Are REITs?

- December 3, 2018: Conservative Core Satellite Portfolio

- November 26, 2018: Allocation Mutual Fund Review

- November 19, 2018: Is The Recent Downtrend Sustainable?

- November 12, 2018: The Staggering Low Interest Rates From Big Banks

- November 5, 2018: The ‘Right’ Or ‘Wrong’ Decision

- October 29, 2018: Taxable Total Return Bond Plus Muni Bond Fund Based Portfolios

- October 22, 2018: DoubleLine Shiller CAPE 10 Based Fund Review

- October 15, 2018: Newsletter Collection Update

- October 8, 2018: Asset Trend Review

- October 1, 2018: Taxable vs. Tax Exempt High Yield Bonds

- September 24, 2018: High Yield Bonds In A Rising Rate Environment

- September 10, 2018: Value, Growth And Blend Stock Style Investing

- August 27, 2018: Money Market ETFs?

- August 20, 2018: How Momentum Investing Stacks Up?

- August 13, 2018: Total Return Bond ETF

- August 6, 2018: Fidelity Zero-Fee Index Funds

- July 30, 2018: Tax Efficient Portfolios

- July 23, 2018: Municipal Bond Funds And Portfolios

- July 16, 2018: A Guide To Conservative Portfolios

- July 9, 2018: Conservative Allocation Mutual Funds Based Portfolios

- July 2, 2018: Small Cap Stocks For The Long Term

- June 25, 2018: What Can We Learn From GE’s Removal From Dow Jones Index?

- June 18, 2018: The ‘Best’ Balanced Portfolio Continues To Excel

- June 11, 2018: Is 10 Year Long Enough For Portfolio Comparison?

- June 4, 2018: Action Plan: Risk Review For Investments

- May 21, 2018: Rising Rates, Consumer Staples And Stock Index

- May 14, 2018: Newsletter Collection Update

- May 7, 2018: Money Market Fund Taxonomy

- April 30, 2018: Momentum Investing Review

- April 23, 2018: Commodities In Current Environment

- April 16, 2018: Municipal Bonds As A Fixed Income Asset Class

- April 9, 2018: Exponential Or Compounding Nature In Investing

- April 2, 2018: Inside Of The Stock Chaos

- March 26, 2018: Total Return Bond Update

- March 19, 2018: Treasury Bills vs. Brokered CDs

- March 12, 2018: Defensive Conservative Portfolio Review

- March 5, 2018: Warren Buffett’s Advices

- February 26, 2018: Pros And Cons of Strategic And Tactical Portfolios In 2018

- February 12, 2018: Trend Review

- February 5, 2018: Market Selloff And Long Term Investing

- January 29, 2018: The New Addition To Our Total Return Bond Fund Candidates

- January 22, 2018: Where Are Bonds Heading?

- January 15, 2018: Tactical Portfolios Review

- January 8, 2018: Strategic Portfolios Review

- December 18, 2017: Record Highs And Risk

- December 11, 2017: Cash Return And Interest Rate Update

- December 4, 2017: Mutual Fund Star Ratings: Are They Useful?

- November 20, 2017: Thankful And Mindful

- November 13, 2017: Is This A Good Time For Retirees Or Would Be Retirees?

- November 6, 2017: Newsletter Collection Update

- October 30, 2017: Rising Interest Rates

- October 23, 2017: A Primer For Portfolios

- October 16, 2017: REITs As An Asset Class

- October 9, 2017: Conservative Portfolios Revisited

- October 2, 2017: The Role of Short Term Bond Funds

- September 25, 2017: Fees In Cash Investments

- September 18, 2017: Conservative Portfolios Review

- September 11, 2017: International Diversification Effect

- September 4, 2017: Invest And Speculate Revisited

- August 28, 2017: Total Return Bond Fund Portfolios: Where Do They Fit?

- August 21, 2017: Portfolio Performance: A Walk In The Past

- August 14, 2017: Fidelity Commission Free ETFs Update

- August 7, 2017: I Didn’t Learn Anything — Mistake vs. Temporary Underperformance

- July 31, 2017: Asset Classes And Fund Choices: A Primer

- July 24, 2017: Total Return Bond Fund Portfolios And Cash

- July 17, 2017: Long Term Stock Holding Periods For Retirement

- July 10, 2017: Half Year Asset Trend Review

- June 26, 2017: How To Beat The Best Balanced Allocation Fund

- June 19, 2017: Newsletter Collection Update

- June 12, 2017: A Mixed Bag Performance of Momentum Investing

- June 5, 2017: How To Start A New Portfolio

- May 29, 2017: Alternative Assets And Their Role In Portfolios

- May 22, 2017: Summer Seasonality And Portfolio Management

- May 15, 2017: Cash: Banking Or Investing?

- May 8, 2017: Holding Period of Long Term Timing Portfolios

- May 1, 2017: Debate on Risk vs. Volatility

- April 24, 2017: The Long Term Stock Market Timing Return Since 1871

- April 17, 2017: Risk vs. Volatility: Long Term Stock Market Returns

- April 10, 2017: Total Return Bond ETFs And Portfolios

- April 3, 2017: Quarter End Asset Trend Review

- March 27, 2017: Practical Consideration For IRAs And 401k Accounts

- March 20, 2017: Fund Fees: That’s (Still) Outrageous

- March 13, 2017: Long Term Stock Valuation Review

- March 6, 2017: Asset Classes for Retirement Investments

- February 27, 2017: Fidelity Total Bond Fund Review

- February 20, 2017: Long Term Stock Timing Based Portfolios And Their Roles

- February 13, 2017: Alternative Investment Portfolios Review

- February 6, 2017: Tax Free Municipal Bond Investments Review

- January 30, 2017: Brokerage Specific Conservative Portfolios

- January 23, 2017: Fixed Income Portfolio Review

- January 16, 2017: Long Term Trend Following Portfolio Review

- January 9, 2017: Tactical Asset Allocation Review

- January 3, 2017: Strategic Asset Allocation Review

- December 12, 2016: Enhanced Index Funds

- December 5, 2016: Review Of Broad Base Core Mutual Funds For Brokerages

- November 28, 2016: Core Index ETFs Review

- November 21, 2016: International Exposure Of U.S. Large Companies

- November 14, 2016: Asset Trends After The Election

- November 7, 2016: Rising Rate And Current Bond Trend

- October 31, 2016: Economy Power And Long Term Stock Returns

- October 24, 2016: Current Commodity Trend And Managed Futures

- October 17, 2016: Investment Mistakes And Good Or Bad Investment Strategies

- October 10, 2016: Momentum Investing Review

- October 3, 2016: Survey & Feedback

- September 26, 2016: Fixed Income Investing: Actively Managed Funds vs. Index Funds

- September 19, 2016: Stock Investing: Actively Managed Funds vs. Index Funds

- September 12, 2016: Newsletter Update

- September 5, 2016: Overvalued Markets And Long Term Timing Strategies

- August 29, 2016: Your 401K Finally Draws Attention

- August 22, 2016: Inflation Protected Securities TIPS For Current Overvalued Markets

- August 15, 2016: Risk On: Emerging Market Stocks And Small Cap Stocks

- August 8, 2016: Portfolio Construction Using Stock ETFs And Bond Mutual Funds

- August 1, 2016: Adding Value To Your Own Investments

- July 25, 2016: Tactical Asset Allocation Funds Review

- July 18, 2016: Strategic Asset Allocation & Lazy Portfolio Review

- July 11, 2016: Asset Trend Review

- June 27, 2016: Secular Cycles For Tactical And Strategic Investment Strategies

- June 20, 2016: A World of Debt

- June 13, 2016: Managed Futures For Portfolio Building

- June 6, 2016: Newsletter Summary

- May 30, 2016: Swensen Portfolio And Permanent Portfolios

- May 23, 2016: AAII Article And Some Web Changes

- May 16, 2016: The PIMCO (Dis)Advantages

- May 9, 2016: Boost Your Dull Summer Investments

- May 2, 2016: Low Cost Index Fund Investing

- April 25, 2016: Tax Free Municipal Bond Funds & Portfolios

- April 18, 2016: Asset Class Trend Review

- April 11, 2016: Construction of Sound And Conservative Portfolios

- March 28, 2016: Total Return Bond ETFs Review

- March 21, 2016: Small And Large Company Stock Performance In Different Economic Expansion Cycles

- March 14, 2016: Are Tactical And Timing Strategies Losing Steam?

- March 7, 2016: Defined Maturity Bond Fund Analysis

- February 29, 2016: Smart Strategic Asset Allocation Rebalance When Market Trend Changes

- February 22, 2016: Be Cash Smart

- February 15, 2016: Bond ETF Portfolios

- February 8, 2016: Newsletter Collection Update

- February 1, 2016: Total Return Bond Fund Portfolios In A Volatile Period

- January 25, 2016: Alternative Portfolios Review

- January 18, 2016: Strategic Asset Allocation: A Cautious Outlook

- January 11, 2016: Review Of Trend Following Tactical Asset Allocation

- January 4, 2016: What Worked And Didn’t In 2015

- December 21, 2015: Distressed Assets

- December 14, 2015: High Yield Bonds And Their Correlation With Stocks

- December 7, 2015: Diversification And Global Allocation

- November 30, 2015: Investors and Speculators Combined

- November 23, 2015: Active Stock Fund Performance Consistency

- November 16, 2015: Permanent, Risk Parity And Alternative Portfolios Review

- November 9, 2015: Broad Base Core Mutual Fund Review

- November 2, 2015: Broad Base Index Core ETFs Review

- October 26, 2015: Total Return Bond Fund Review

- October 19, 2015: Advanced Portfolio Review

- October 12, 2015: What About Commodities?

- October 5, 2015: Core Satellite Portfolios In A 401k Account

- September 28, 2015: Risk Managed Strategic Asset Allocation Portfolios Revisited

- September 21, 2015: Quest For The Best Investment Strategy

- September 14, 2015: Core Satellite Portfolios In Market Turmoil

- September 7, 2015: Market Rout Creates An Opportunity to Reposition Your Portfolios

- August 31, 2015: Review of Asset Allocation Funds and Portfolios

- August 24, 2015: Market Rout And Your Portfolios

- August 17, 2015: ETF or Mutual Fund Based Portfolios

- August 10, 2015: Updated Newsletter Collection

- August 3, 2015: Slippery Asset Trends

- July 27, 2015: Performance Dispersion Among Momentum Based Portfolios

- July 20, 2015: Global Balanced Portfolio Benchmarks

- July 13, 2015: Pain in Tactical Portfolios

- July 6, 2015: Fixed Income Total Return Bond Funds In Strategic Asset Allocation Portfolios

- June 29, 2015: Core ETF Commission Free Portfolios

- June 22, 2015: Secular Asset Trends

- June 15, 2015: Giving Up Bonds?

- June 1, 2015: Summer Blues?

- May 26, 2015: Cash, Bonds and Stocks In A Rising Rate Environment

- May 18, 2015: Portfolio Update

- May 11, 2015: Pain in Fixed Income?

- May 4, 2015: The Balanced Stock and Long Term Treasury Bond Portfolios

- April 27, 2015: Long Term Treasury Bond Behavior

- April 20, 2015: 529 College Savings Plan Rebalance Policy Change

- April 13, 2015: Total Return Bond Funds As Smart Cash

- April 6, 2015: The Low Return Environment

- March 30, 2015: Brokerage Specific Core Mutual Fund Portfolios 2

- March 23, 2015: Investment Arithmetic for Long Term Investments

- March 16, 2015: Brokerage Specific Core Mutual Fund Portfolios

- March 9, 2015: Newsletter Collection Update

- March 2, 2015: Total Return Bond ETFs

- February 23, 2015: Why Is Global Tactical Asset Allocation Not Popular?

- February 16, 2015: Where Are Permanent Portfolios Going?

- February 9, 2015: How Have Asset Allocation Funds Done?

- February 2, 2015: Risk Management Everywhere

- January 26, 2015: Composite Portfolios Review

- January 19, 2015: Fixed Income Investing Review

- January 12, 2015: How Does Trend Following Tactical Asset Allocation Strategy Deliver Returns

- January 5, 2015: When Forecast Fails

- December 22, 2014: Long Term Asset Returns: How Long Is Long?

- December 15, 2014: Beaten Down Assets

- December 8, 2014: Implementing Core Asset Portfolios In a Brokerage

- December 1, 2014: Two Key Issues of Investment Strategies

- November 24, 2014: Holiday Readings

- November 17, 2014: Retirement Spending Portfolios Update

- November 10, 2014: Fixed Income Or Cash

- November 3, 2014: Asset Trend Review

- October 27, 2014: Investment Loss, Mistakes And Market Cycles

- October 20, 2014: Strategic Portfolios With Managed Volatility

- October 13, 2014: Embrace Volatility

- October 6, 2014: Tips For 401k Open Enrollment

- September 29, 2014: What Can We Learn From Bill Gross’ Departure From PIMCO?

- September 22, 2014: Why Total Return Bond Funds?

- September 15, 2014: Equity And Total Return Bond Fund Composite Portfolios

- September 8, 2014: Momentum Based Portfolios Review

- September 1, 2014: Risk & Diversification: Mint.com Interview

- August 25, 2014: Remember Risk

- August 18, 2014: Consistency, The Most Important Edge In Investing: Tactical Case

- August 11, 2014: What To Do In Overvalued Stock Markets

- August 4, 2014: Is This The Peak Or Correction?

- July 28, 2014: Stock Musings

- July 21, 2014: Permanent Portfolios & Four Pillar Foundation Based Framework

- July 14, 2014: Composite Portfolios Review

- July 7, 2014: Portfolio Behavior During Market Corrections

- June 30, 2014: Half Year Brokerage ETF and Mutual Fund Portfolios Review

- June 23, 2014: Newsletter Collection Update

- June 16, 2014: There Are Always Lottery Winners

- June 9, 2014: The Arithmetic of Investment Mistakes

- June 2, 2014: Tips On Portfolio Rebalance

- May 26, 2014: In Praise Of Low Cost Core Asset Class Based Portfolios

- May 19, 2014: Consistency, The Most Important Edge In Investing: Strategic Case

- May 12, 2014: How To Handle An Elevated Overvalued Market

- May 5, 2014: Asset Allocation Funds Review

- April 28, 2014: Now The Economy Backs To The ‘Old Normal’, Should Our Investments Too?

- April 21, 2014: Total Return Bond Investing In The Current Market Environment