Re-balance Cycle Reminder All MyPlanIQ’s newsletters are archived here.

Regular AAC (Asset Allocation Composite), SAA and TAA portfolios are always rebalanced on the first trading day of a month. the next re-balance will be on Friday July 1, 2022.

As a reminder to expert users: advanced portfolios are still re-balanced based on their original re-balance schedules and they are not the same as those used in Strategic and Tactical Asset Allocation (SAA and TAA) portfolios of a plan.

About The Latest Rebalance

This is a brief newsletter to explain the current rebalance. We will have more detailed discussions in a newsletter after July 4, 2022 holiday.

The key factors behind our Asset Allocation Composite (AAC) strategy (and other strategies to a less extent) include the following:

Broad base stock markets trends

We all know that all major stock indices including US stocks, foreign developed market stocks and emerging market stocks have negative trend scores for a while. See 360° Market Overview for more details.

Stock valuation

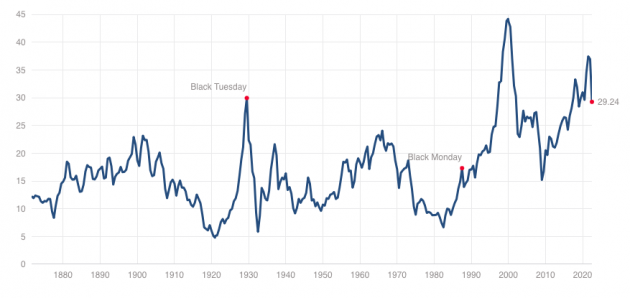

Again, we all know that the valuation of US stocks is still very high by historical standards. The 20% S&P 500 loss from its peak is not enough to lower their valuations or expensiveness: for example, Shiller CAPE is currently at 29.24, still much higher than its 16.95 average. It’s also higher than 2007 and about the same as Black Tuesday in the Great Depression. In fact, It’s only lower than that in 2000.

Bond indicators

Similar to stocks, all major bond segments have negative trend scores. However, we do see some positive short term momentum for Treasury bonds now. See 360° Market Overview for more details.

Market internals

- Sectors: all sectors other than utilities and energy sectors have negative trend scores. These include Consumer Staples and Healthcare that are considered as defensive sectors.

- Majority of stocks in S&P 500, Nasdaq and NYSE are in a long term down trend.

- All equity styles including value stocks are in a downtrend.

Economy indicators

Though some of economy indicators such as unemployment rate and industry production are still positive, many others including retail sales and personal income have indicated a slowdown or recession. Furthermore, housing start, though still lagging, has started to show weakness.

Subjective Rationale

As the Federal Reserve Bank has signaled further interest rate hikes, it’s just the matter of time that unemployment rate will rise in some meaningful way (this is actually one of the goals for the Federal Reserve to raise interest rates). Similarly, much higher interest rates will definitely slowdown housing market.

US economies and most economies in the Eurozone area are either in recession or on the verge of recession. In fact, the Atlanta Fed GDP Now is predicting -1.0% GDP growth in the current quarter. If this materializes, the US is technically in a recession with two consecutive quarters of negative GDP growths.

Though the current 20% S&P 500 stock loss might seem to be high, we are reminded that so far, its loss is really due to interest rate rise or so called PE multiple compression (compared with bond yields, now stocks become less attractive thus their prices over earnings multiples need to come down). So far, we haven’t seen much from company earnings slowdown reports. However, with a Federal Reserve Bank that’s determined to slow down demand (and it’s succeeding), there will be no surprise that we are going to see more weak earning reports from now on.

In a word, it’s highly likely the current market weakness in stocks will continue.

Our strategies don’t rely on our subjective views though we believe that the indicators used are very supportive to the above view.

Of course, we want to caution everyone that as always, our strategies by no means are a surefire. For example, a somewhat popular view right now is that as bond markets are recognizing the current economy weakness and inflation is peaking, they (bond markets) will eventually force the Federal Reserve to pivot and reverse its current tightening stance. This will in turn enables a strong rebound in stocks.

We do agree there is a possibility on this. However, the question is whether by the time the narrative has materialized, the damage to the economies is too much and the turn is too late. Interest rate hikes done by the Federal Reserve can only slow down demand and it doesn’t affect supply side very much, at least initially. The feedback loop might be too long for prices to come down. So it’s very likely that we will see a period of high prices and low growth (so called stagflation) that will still force the Fed to continue to raise interest rates and tighten financial conditions that will further dampen growth to the extent that it might overshoot.

Regardless, as we have repeatedly pointed out, our strategies have strong historical data backing and are intuitively sound. In the long term, they will excel. So be prepared to be frustrated in the short term and stay the course.

About rebalance

As stocks are very over sold right now, we want to point out that it’s also possible to defer rebalance after July 4 holiday as a period after a holiday tends to be favorable to stocks. However, that’s up to individual decisions.

We wish everyone a good long weekend!

Diversified Asset Allocation Portfolios For Your Plans

Diversified Asset Allocation Portfolios For Your Plans