How To Fully Utilize Self-Directed IRAs For Retirement Investments

Individual Retirement Accounts (IRAs) represent specialized investment accounts within brokerages. Presently, virtually all major brokerages, such as Fidelity, Schwab, and Vanguard, offer no-fee IRA options. Over the past decade, IRAs have grown significantly more appealing, largely owing to the accessibility of commission-free ultra-low-cost (index) ETFs. In this newsletter, we will delve into the details of harnessing IRAs for retirement investments.

IRA Types

Briefly, there are three major types of IRAs: Traditional IRAs, Roth IRAs, and SEP IRAs that have distinctive features and benefits:

Traditional IRAs: Traditional IRAs are one of the most prevalent retirement savings vehicles. They operate on a tax-deferred basis, allowing individuals to contribute pre-tax income, reducing their current taxable income. This tax advantage can be particularly beneficial during your working years when your income is typically higher. As the funds grow within the account, they remain tax-sheltered until you begin withdrawing them in retirement. At that point, you will pay income taxes on your withdrawals at whatever tax rate you have at that time. Ideally you would hope to have a lower tax rate than during your earning years (which is not always the case if you have large sum of investment income and IRA withdrawals). Traditional IRAs are well-suited for those who anticipate a lower tax bracket in retirement and wish to take advantage of tax deductions during their working years. Normally, a typical 401k account is rolled over to a traditional IRA.

Roth IRAs: Roth IRAs, in contrast, focus on tax-free growth. Contributions to a Roth IRA are made with after-tax dollars, meaning there is no immediate tax deduction. However, the major advantage lies in the fact that qualified withdrawals from a Roth IRA, including both contributions and earnings, are entirely tax-free in retirement. This makes Roth IRAs an excellent choice for individuals who anticipate being in a similar or higher tax bracket when they retire, as they can enjoy tax-free income during their golden years. Additionally, Roth IRAs offer flexibility by allowing penalty-free withdrawals of contributions at any time, providing a measure of financial security and versatility. However, stringent restrictions exist regarding the amount and manner in which contributions can be made to a Roth IRA.

SEP IRAs (Simplified Employee Pension IRAs): SEP IRAs are designed primarily for self-employed individuals and small business owners. These accounts enable employers (or so called solo entrepreneur) to make contributions to their own retirement accounts, as well as those of their employees, in a tax-advantaged manner. Contributions to SEP IRAs are typically tax-deductible for employers, making them an attractive option for businesses looking to provide retirement benefits to their staff. SEP IRAs are relatively easy to set up and maintain, with flexible contribution limits that can scale with the business’s financial performance. Compared with a typical 401k account, SEP IRAs offer higher limit of contributions and flexibility of investments in an IRA brokerage account.

All of these IRAs share one major benefit or feature: they are brokerage accounts that can invest virtually into all of the major ETFs (other than some highly risky leveraged and inverse ETFs), mutual funds and stocks.

Rollover from 401k to IRAs

In Pros and Cons of Rollover from a 401(k) to a Self-Directed IRA, we have detailed some of tor pros and cons of rolling over (moving) your 401k account to an IRA when you leave your job (note: you can’t rollover your 401k account with your current employer when you are still with the employer). We want to emphasize that there are two somewhat obscure benefits for remaining in your old 401k account:

- Legal protection: while your 401(k) or other employer-based retirement plan may enjoy federal protection in a lawsuit, it’s important to note that IRA protections are subject to state regulations, potentially leaving your retirement funds vulnerable to being used for covering damages in a lawsuit.

- Loan: Another advantage of remaining within a 401(k) plan is the potential ability to secure an emergency loan when necessary (Note, this is subject to your former employer’s approval). In general, IRS doesn’t allow you to take a loan from your IRAs. On the other hand, notice that the maximum loan you can borrow from your 401(k) account is $50,000.

- Special investments from a 401(k): aside from some close to new investors mutual funds such as T.Rowe Price Capital Appreciation fund that was closed to new investors in 2017 (but still open to a 401(k) investor if it’s available in that plan), another frequently mentioned advantage of a 401(k) is the potential access to stable value funds, which are insured to ensure higher interest returns while preserving cash value. However, with the availability of some excellent Treasury bill ETFs, this advantage may no longer hold true. We’ll delve into this topic in more detail later on.

How to fully utilize IRAs for retirement investments

Let’s explore how to leverage the resources within a brokerage IRA to build better investment portfolios for retirement:

Ultra-low cost (index) ETFs or mutual funds

Certain sizable 401(k) plans have the capacity to negotiate remarkably low costs for specific funds, particularly pooled separate accounts or collective investments. In essence, fund management companies like the Capital Group craft such investment vehicles, often mirroring their existing mutual funds but with significantly reduced expenses. Nevertheless, in the present landscape, it’s entirely possible to assemble a portfolio with expenses as low as 0.03% that’s almost impossible to match by any separate account or collective investment instruments in a 401(k) plan:

Ultra low-cost ETFs that cover major stock and bond asset classes:

| Ticker | Fund | Expense Ratio | AUM |

| VTI | Vanguard Total Stock Market ETF | 0.03% | $288.78B |

| VOO | Vanguard S&P 500 ETF | 0.03% | $286.59B |

| BND | Vanguard Total Bond Market ETF | 0.03% | $88.98B |

| AGG | iShares Core U.S. Aggregate Bond ETF | 0.03% | $86.60B |

| ITOT | iShares Core S&P U.S. Total Stock Market ETF | 0.03% | $42.13B |

| SCHX | Schwab U.S. Large-Cap ETF | 0.03% | $32.13B |

| SCHB | Schwab U.S. Broad Market ETF | 0.03% | $22.13B |

| STIP | iShares 0-5 Year TIPS Bond ETF | 0.03% | $13.09B |

| SCHO | Schwab U.S. Short-Term U.S. Treasury ETF | 0.03% | $13.06B |

| SCHR | Schwab Intermediate-Term U.S. Treasury ETF | 0.03% | $7.83B |

For example, you can construct a 60% VTI 40% BND balanced portfolio that only pays 0.03% expense. This is actually lower than 0.07% of Vanguard Balanced Index Fund Admiral Shares (VIBAX) or 0.18% of VBINX!

Simply put, there isn’t much cost advantage for 401k plans, compared with IRAs.

Much more availability of good active ETFs

It used to be that mutual funds from famed investment managers such as Capital Group or Dimensional Fund Advisors (DFA) only provide their mutual funds to certain 401(k) plans, as well as to investment advisor managed accounts (taxable or tax deferred). However, now that these funds start to become available as ETFs (see February 27, 2023: Dimensional Fund Advisors and Capital Group ETFs), investors can only get a lot more good funds from a brokerage in their IRA account. For example, one can utilize CGXU (Capital Group International Focus Equity ETF) and DFAE (DFA Emerging Core Equity Market ETF) in a portfolio in an IRA. In a 401(k) plan, it’s more likely that only Capital Group funds or DFA (Dimensional Fund Advisors) funds are accessible, but typically not both.

Speaking of good active ETFs, in fixed income, in a major brokerage, you can find many excellent actively managed bond funds available. For example, in an IRA in Schwab, you can invest in these funds

This used to be one of the advantages offered by certain 401(k) plans, providing access to exceptional fixed income funds. However, this advantage has largely diminished or disappeared.

Excellent short-term investments

In a 401(k) plan, one often sees the availability of retirement income funds or stable value funds. These funds usually provide higher interests than one usually gets from a fund available in a brokerage account. Stable value funds usually guarantee or preserve their value, thus basically are cash-like. However, as what we have repetitively pointed out in the past, there are so many excellent money market ETFs or mutual funds available in an IRA (see Cash And Money Market ETFs Review). In fact, just for Treasury Cash-like ETFs, the latest yields are:

| Symbol (Name) | Expense | Asset Size | Maximum Drawdown | SEC Yield |

|---|---|---|---|---|

| BIL (SPDR Barclays 1-3 Month T-Bill ETF) | 0.14% | 29B | -0.14% | 5.21% |

| SGOV (iShares 0-3 Month Treasury Bond ETF) | 0.03% | 10B | 0% | 5.34% |

| USFR (WisdomTree Floating Rate Treasury Fund) | 0.15% | 15B | -0.05% | 5.38% |

| TFLO (iShares Treasury Floating Rate Bond ETF) | 0.15% | 5.8B | -0.06% | 5.35% |

| CASH (CASH) | N/A | 0% | ||

| VMFXX (Vanguard federal money market) | 0.15% | 238B | NA | 5.29% |

| SPAXX (Fidelity Government Money Market) | 0.42% | 256B | NA | 4.98% |

So one can see that with extremely low expense: 0.03% vs. 0.42% of SPAXX or 0.2%-0.5% a typical money market fund charges, these cash-like ETFs are almost unrivaled.

Lastly, it’s difficult to resist commenting on the high expense ratio of a money market mutual fund. It’s somewhat astonishing to think that money market funds, such as Vanguard’s VMFXX, charge considerably higher fees than those associated with broad-based stock index funds like VTI or bond index funds like BND. Well, generating a favorable spread from cash remains a significant revenue source for brokerages like Schwab!

Excellent general purpose fixed income investments

As alluded above, one can often access to excellent fixed income mutual funds from an IRA in a major brokerage, It’s also possible to get many similar ETFs. Using these funds, one can construct a good fixed income portfolio. For example, the portfolios mentioned on our Fixed Income Investors page utilize excellent total return bond funds (or ETFs) as candidate funds and employ a tactical strategy. They have consistently outperformed even the best total return fixed income funds such as DoubleLine total return fund or PIMCO Income or PIMCO total return bond funds for more than a decade!

The following funds are available in Schwab and used as candidate funds for the Schwab Total Return Bond portfolio:

| Intermediate-Term Bond | PBDAX | PIMCO Investment Grade Corp Bd A |

| Intermediate-Term Bond | PDBZX | Prudential Total Return Bond Z |

| Multisector Bond | PONAX | PIMCO Income A |

| Intermediate-Term Bond | DLTNX | DoubleLine Total Return Bond N |

| Intermediate-Term Bond | WABRX | Western Asset Core Bond R |

| Intermediate-Term Bond | TGMNX | TCW Total Return Bond N |

| Intermediate-Term Bond | PTTAX | PIMCO Total Return A |

| Intermediate-Term Bond | MWTRX | Metropolitan West Total Return Bond M |

| Multisector Bond | LSBRX | Loomis Sayles Bond Retail |

Constructing sound balanced asset allocation portfolios

In an IRA, investors have the opportunity to build a portfolio using the following approach:

For stocks, they can employ excellent ultra-low-cost stock index ETFs and, with some discretion, consider active stock ETFs offered by Capital Group or Dimensional Fund Advisors (It’s important to note that strictly speaking, DFA funds are still considered index funds, or they can be viewed as enhanced index funds rather than actively managed funds. The only difference is that DFA does not open its indexes to other third party).

For bonds, they can make use of outstanding total return bond mutual funds, managed by managers who have been recipients of the Morningstar Manager of the Year award, or opt for their ETF counterparts. One can create either a standalone fixed-income portfolio or design a blended stock and bond portfolio using a strategy like MyPlanIQ’s asset allocations strategies (such as Asset Allocation Composite (AAC) or Strategic Asset Allocation (SAA).

In summary, by fully utilizing the resources available through a brokerage in an IRA, including a wide array of ETFs and possibly some mutual funds, individuals can structure a significantly improved investment portfolio compared to a typical 401(k) account.

Market Overview

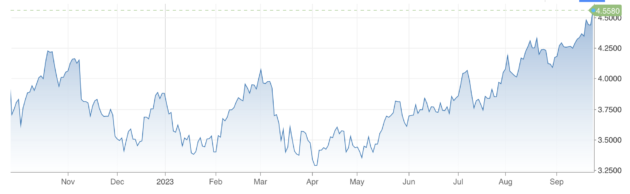

One of the prominent developments in financial markets is the recent swift ascent of the 10-year Treasury yield:

With short-term interest rates reaching as high as 5.5%, the notable increase in long-term bond rates, currently at 4.5% for 10-year Treasury yields, has led to a substantial rise in borrowing costs for businesses. Many businesses depend on long-term borrowing to fund various activities, including capital expenditures and long-term leases for buildings and machinery, among others. Additionally, consumers are feeling the pressure as well, with 30-year fixed mortgage rates reaching their highest levels since 2000, soaring as high as 8%:

We believe that the simultaneous increase in interest rates at both the short and long ends carries immense significance, and it has the potential to severely decelerate the economy. The key question at this juncture is whether the slowdown occurs too swiftly before the Federal Reserve can pivot and reverse its tightening policy. If the economy experiences a sharp derailment, it could have detrimental effects on equity markets, particularly considering their current highly overvalued levels.

As always, we claim no crystal ball and we call for staying the course which is guided by the well defined and sound strategic and tactical strategies:

- For strategic allocation (buy and hold) investors, ignore the current market behavior. Remember, as we have emphasized numerous times, when you choose and commit to a strategic portfolio, you essentially know and commit that your investment horizon (or the time you need to utilize this capital) is 20 years, preferably much longer, given the current high valuation. As we pointed out, if your investments are those diversified (index) funds such as an S&P 500 index fund (VFINX, for example), you know your money is in some solid ‘business’ that eventually (20 years later and preferably many more years later) will deliver some reasonable returns. As long as you are comfortable with this thesis, you should sit tight and forget about the current gyration.

- For tactical investors, again, you have to ignore the current market noise. Furthermore, you should follow your strategy rigorously, especially during this time. Human emotion, both optimistic and pessimistic, and human desire, both greedy and fearful, are your worst enemies. This is true time and time again.

Stock valuation has dropped, and now valuation is becoming less hostile. However, it is still not cheap by historical standards. For the moment, we believe it’s prudent to be extra cautious. However, how serious a correction might be, we have confidence in the US economy in the long term and thus in the stocks in aggregate. We just need to manage through interim losses carefully.

We again would like to emphasize that for any new investor and new money, the best way to step into this kind of market is through dollar cost average (DCA), i.e., invest and/or follow a model portfolio in several phases (such as 2 or 3 months) instead of the whole sum at one shot.

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?

Latest Articles

- Newsletter Collection Update

- Portfolio Calculator (Simulator) And Rolling Returns

- ETFs In Asset Classes For Portfolio Construction

- Retirement Savings: How Much Should You Save For A Comfortable Retirement Life?

- High Yield Bonds Are Good Alternatives For Aggressive Fixed Income Investors

- Trends, Factors & Indicators

- Lazy Portfolios Review

- ‘Best’ Tactical Stock or Dividend Income Balanced Portfolios vs. Best Balanced Allocation Fund

- ‘Best’ Stock or Dividend Income Balanced Portfolios vs. Best Balanced Allocation Fund

- Low-Cost Stock Index Funds: Quality ‘Business Conglomerates’ for Solid, Low-Risk Long-Term Returns

- Cash And Money Market ETFs Review

- March 27, 2023: 401k Company Match: How To Maximize Your Free Money

- March 13, 2023: Bank On My Own For Safer And Much Higher Returns

- February 27, 2023: Dimensional Fund Advisors and Capital Group ETFs

- February 13, 2023: In Praise Of A Conservative Strategic Asset Allocation

- January 30, 2023: The Bond Era

- January 16, 2023: International Stocks In Asset Allocation

- January 3, 2023: Review And Outlook

- December 5, 2022: Latest Market And Trend Review

- November 21, 2022: How To Maximize Your Cash Return

- November 7, 2022: Tactical Bond Fund Portfolios Consistently Outperform

- October 24, 2022: S&P 500: A Solid ‘Business’ In A Volatile Time

- October 10, 2022: 9.62% Treasury I Bonds: Cash Is Indeed King

- September 26, 2022: Markets, Noises, Long Term Strategies …

- September 12, 2022: Factor ETFs Review

- August 29, 2022: Cash Is King

- August 15, 2022: Asset Trends Review

- August 1, 2022: What We Can Learn From 1970s And 1980s

- July 18, 2022: Fixed Income Is Becoming An Alternative

- July 1, 2022: About The Latest Rebalance

- June 6, 2022: Sector Rotation In A Rising Rate Environment

- May 23, 2022: Latest Portfolio And Trend Review

- May 9, 2022: The Secular Market Cycle Change

- April 25, 2022: Survivorship Bias, Sentiment And Market Internals …

- April 11, 2022: Asset Allocation And Risk Management

- March 28, 2022: March Madness And Steady Course

- March 14, 2022: Quality Sectors Prevail

- February 28, 2022: Asset Allocation Fund Review

- February 14, 2022: Inflation, Interest Rates And Fixed Income Investments

- February 1, 2022: Foreign Stocks And Global Asset Allocation

- January 18, 2022: Steady And Consistency Win In The Long Term

- January 3, 2022: The Year In Rear View: Portfolio And Asset Class Review

- December 13, 2021: Present And Future

- November 22, 2021: The ‘Best’ Balanced Fund Revisited

- November 15, 2021: Q&A On MyPlanIQ Strategies And Portfolios

- November 8, 2021: Major Asset Returns In The Past Twenty Years

- November 1, 2021: Latest Momentum Factor ETFs Review

- October 25, 2021: A Long Term Theme Or Trend Doesn’t Necessarily Yield Good Returns

- October 18, 2021: Dimensional Fund Advisors DFA ETFs

- October 11, 2021: MyPlanIQ Ultra Short Term Bond Portfolio vs. Other Funds

- October 4, 2021: Asset Trends, Market Internals And Inflation Implication

- September 27, 2021: Newsletter Collection Update

- September 20, 2021: Benchmarking MyPlanIQ Fixed Income Bond Portfolios

- September 13, 2021: Benchmarking MyPlanIQ Tactical Portfolios

- August 30, 2021: Invest And Speculate: A Sensible Alternative To Buy And Hold

- August 23, 2021: Style ETF Portfolio Review

- August 16, 2021: Smart Factor ETFs Review

- August 9, 2021: Best Global Allocation Funds vs. MyPlanIQ ETF Portfolios

- August 2, 2021: Major Asset Trends And Market Internals

- July 26, 2021: Ultra Short Term Bond ‘Money Market’ Portfolio And Banking

- July 19, 2021: Take The Challenge of The ‘Best’ Balance Fund

- July 12, 2021: The Long Forgotten Bear Market Cycles

- June 28, 2021: Resuming Growth Trends Chaotically?

- June 21, 2021: Stocks Are Not Replacement Of Bonds

- June 14, 2021: Outperform The Best Performing PIMCO Income Bond Fund

- June 7, 2021: “Good” S&P Sectors

- May 17, 2021: Total Return Bond ETFs Review

- May 10, 2021: Financial Independence & Early Retirement

- May 3, 2021: Inflation, Sub Zero Interest Rate …

- April 26, 2021: The Best Active Fixed Income Funds Are Still Hard To Beat

- April 19, 2021: New And Old Useful Features

- April 12, 2021: Risk Parity Funds In Current Environment

- April 5, 2021: DoubleLine Shiller CAPE 10 Based Funds Update

- March 29, 2021: International Stocks vs. US Stocks

- March 22, 2021: Ultra Short Term Bond ETF Portfolio As A Money Market Fund

- March 15, 2021: Make Your Own Private Bank

- March 8, 2021: The Not So Orderly Market Rotation Amid Rising Bond Yields

- March 1, 2021: Average 20% Annual Returns: The Upper Bound Of Stock Investments?!

- February 22, 2021: Rising Bond Yields And Current Stock Trends

- February 8, 2021: Total Return Bond ETFs Review

- February 1, 2021: REITs And Major Asset Trends

- January 25, 2021: Industry ETFs And ARK ETFs Portfolios

- January 11, 2021: Smart Cash Management: Can I Just Withdraw From My Bond Portfolio?

- January 4, 2021: Our Investment Philosophy For 2021 And Beyond

- December 14, 2020: Style and Factor ETFs Portfolio Reviews

- December 7, 2020: A Really Long Term (30 Years) Stock Returns

- November 30, 2020: Higher Return Portfolios: Part 2

- November 16, 2020: Higher Return Portfolios

- November 9, 2020: Fixed Income Funds Update

- November 2, 2020: Polls Are Useless vs. This Investment Strategy Doesn’t Work!

- October 26, 2020: Recent Improvements

- October 19, 2020: REIT Indexes As Businesses

- October 12, 2020: Stock Indexes As Businesses

- October 5, 2020: Asset Trend Review

- September 28, 2020: Retirement Spending: Your Portfolio’s Volatility Matters

- September 21, 2020: Boring Utility Stocks Are Excellent Long Term Winners

- September 14, 2020: Surprised, Active Fixed Income Investors Have Done Better Than Stock Investors For The Last 20 Years!

- August 31, 2020: Investing In An Ultra-Low Return Environment

- August 24, 2020: Target Maturity Bond ETFs For Short Term Cash

- August 17, 2020: Newsletter Collection Update

- August 10, 2020: Fixed Income In A Speculative Era

- August 3, 2020: Sound Investment Strategies

- July 27, 2020: Total Return Bond Funds Update

- July 20, 2020: Divergence Between Value And Growth Stocks Everywhere

- July 13, 2020: Short Term Cash, Treasury Bills, CDs And Future Fixed Income

- July 6, 2020: Bond ETFs vs. Bond Mutual Funds

- June 29, 2020: Industry Sector ETF Rotation With Composite Momentum

- June 22, 2020: Industry Sector Rotation With Composite Momentum

- June 15, 2020: Advanced Minimum Equity Portfolios

- June 8, 2020: Recent Positive Developments

- June 1, 2020: Minimum Equity Portfolios

- May 18, 2020: Core Satellite Portfolios In The Current Pandemic

- May 11, 2020: Asset Trends Review

- May 4, 2020: The Real, Sensible And Wise Warren Buffett

- April 27, 2020: Total Return Bond Funds & Portfolios

- April 20, 2020: Multi-Factor ETFs and Rotation

- April 13, 2020: A Closer Look At 401(k) Investment Portfolios

- April 6, 2020: Long Term Stock Market Timing Since 1871 Revisited

- March 30, 2020: How Did Bond ETFs And Mutual Funds Fare In The Current Crisis?

- March 23, 2020: Chaos And Hope

- March 16, 2020: A Live Lesson

- March 9, 2020: Risk And Reward

- March 2, 2020: The Risk Of Coronavirus Outbreak

- February 24, 2020: Long Term Stock Valuation Based Investment Strategies

- February 10, 2020: Update On Short Term Cash, Treasury Bills and Brokered CDs

- February 3, 2020: Investment Landscape For Retirees And Would-be Retirees: Stocks

- January 27, 2020: Investment Landscape For Retirees And Would-be Retirees: Fixed Income

- January 13, 2020: Portfolio Performance: A Walk In The Past II

- January 6, 2020: Asset Outlook and Portfolio Strategies

- December 16, 2019: Q&As On Our Services

- December 9, 2019: Portfolio Constructions For Advanced Users

- December 2, 2019: Newsletter Collection Update

- November 25, 2019: Core ETFs or Core Mutual Funds Portfolios

- November 18, 2019: Introducing MyPlanIQ Asset Allocation Composite Strategy

- November 11, 2019: Market Indicator And Momentum

- November 4, 2019: Factor ETF Rotation

- October 28, 2019: Multi-factor ETFs vs. Equal Weight Multi-Factor Portfolios

- October 21, 2019: Multi-factor ETFs: Value And Momentum

- October 14, 2019: Low Volatility Factor ETFs

- October 7, 2019: Zero Commission Era Has Arrived, Is It Really That Good?

- September 30, 2019: Boosting Bond ETF Portfolio’s Return With Muni Bond ETFs

- September 23, 2019: Value ETFs

- September 16, 2019: Factor ETFs

- September 9, 2019: Momentum Factor Stock ETFs

- August 26, 2019: Employer 401k Match: Yet Another Free Lunch Not To Be Missed

- August 19, 2019: PIMCO Income Fund and Other Total Return Bond Funds Update

- August 12, 2019: Aggressive Fixed Income Portfolios?

- August 5, 2019: Long Term Investment Strategies And Short Term Market Noises

- July 29, 2019: Fixed Income Portfolios In A Lower Yield Environment

- July 22, 2019: Core Satellite Portfolios Balance Fluctuation

- July 15, 2019: Quality Stock Factor ETFs

- July 8, 2019: Surprise! Brokerages Make Most From Your Cash, Not Commissions

- July 1, 2019: Utilities Sector Review

- June 24, 2019: Asset Allocation Funds Review

- June 17, 2019: Latest Performance Comparison Among Several Advanced Strategies

- June 10, 2019: Money Market And Ultra Short Term Bond Funds

- June 3, 2019: What We Can Learn From The Seasonality Strategy

- May 20, 2019: Morningstar Portfolio Manager Awards

- May 13, 2019: Total Return Bond ETFs Review

- May 6, 2019: Global Allocation Revisited

- April 29, 2019: Asset Trend Review

- April 22, 2019: The Current State Of Fixed Income

- April 15, 2019: The Importance Of Fixed Income Returns For Retirement Spending

- April 8, 2019: Newsletter Collection Update

- April 1, 2019: S&P 500 As A Business

- March 25, 2019: Health Care Sector Review

- March 18, 2019: The Risk Of Stock Investing

- March 11, 2019: Consumer Staples Sector Review

- March 4, 2019: Global Stock Valuation Update

- February 25, 2019: ‘Bad’ Tactical Strategy

- February 11, 2019: “Best” Balanced Fund And Portfolios Revisited

- February 4, 2019: Cash And Money Market Funds: Interests And Safety

- January 28, 2019: Fixed Income Review

- January 14, 2019: Tactical Asset Allocation Portfolio Review

- January 7, 2019: Global Strategic Asset Allocation Portfolio Review

- December 17, 2018: Robinhood’s ‘Revolution’ Or Gimmick

- December 10, 2018: How Defensive Are REITs?

- December 3, 2018: Conservative Core Satellite Portfolio

- November 26, 2018: Allocation Mutual Fund Review

- November 19, 2018: Is The Recent Downtrend Sustainable?

- November 12, 2018: The Staggering Low Interest Rates From Big Banks

- November 5, 2018: The ‘Right’ Or ‘Wrong’ Decision

- October 29, 2018: Taxable Total Return Bond Plus Muni Bond Fund Based Portfolios

- October 22, 2018: DoubleLine Shiller CAPE 10 Based Fund Review

- October 15, 2018: Newsletter Collection Update

- October 8, 2018: Asset Trend Review

- October 1, 2018: Taxable vs. Tax Exempt High Yield Bonds

- September 24, 2018: High Yield Bonds In A Rising Rate Environment

- September 10, 2018: Value, Growth And Blend Stock Style Investing

- August 27, 2018: Money Market ETFs?

- August 20, 2018: How Momentum Investing Stacks Up?

- August 13, 2018: Total Return Bond ETF

- August 6, 2018: Fidelity Zero-Fee Index Funds

- July 30, 2018: Tax Efficient Portfolios

- July 23, 2018: Municipal Bond Funds And Portfolios

- July 16, 2018: A Guide To Conservative Portfolios

- July 9, 2018: Conservative Allocation Mutual Funds Based Portfolios

- July 2, 2018: Small Cap Stocks For The Long Term

- June 25, 2018: What Can We Learn From GE’s Removal From Dow Jones Index?

- June 18, 2018: The ‘Best’ Balanced Portfolio Continues To Excel

- June 11, 2018: Is 10 Year Long Enough For Portfolio Comparison?

- June 4, 2018: Action Plan: Risk Review For Investments

- May 21, 2018: Rising Rates, Consumer Staples And Stock Index

- May 14, 2018: Newsletter Collection Update

- May 7, 2018: Money Market Fund Taxonomy

- April 30, 2018: Momentum Investing Review

- April 23, 2018: Commodities In Current Environment

- April 16, 2018: Municipal Bonds As A Fixed Income Asset Class

- April 9, 2018: Exponential Or Compounding Nature In Investing

- April 2, 2018: Inside Of The Stock Chaos

- March 26, 2018: Total Return Bond Update

- March 19, 2018: Treasury Bills vs. Brokered CDs

- March 12, 2018: Defensive Conservative Portfolio Review

- March 5, 2018: Warren Buffett’s Advices

- February 26, 2018: Pros And Cons of Strategic And Tactical Portfolios In 2018

- February 12, 2018: Trend Review

- February 5, 2018: Market Selloff And Long Term Investing

- January 29, 2018: The New Addition To Our Total Return Bond Fund Candidates

- January 22, 2018: Where Are Bonds Heading?

- January 15, 2018: Tactical Portfolios Review

- January 8, 2018: Strategic Portfolios Review

- December 18, 2017: Record Highs And Risk

- December 11, 2017: Cash Return And Interest Rate Update

- December 4, 2017: Mutual Fund Star Ratings: Are They Useful?

- November 20, 2017: Thankful And Mindful

- November 13, 2017: Is This A Good Time For Retirees Or Would Be Retirees?

- November 6, 2017: Newsletter Collection Update

- October 30, 2017: Rising Interest Rates

- October 23, 2017: A Primer For Portfolios

- October 16, 2017: REITs As An Asset Class

- October 9, 2017: Conservative Portfolios Revisited

- October 2, 2017: The Role of Short Term Bond Funds

- September 25, 2017: Fees In Cash Investments

- September 18, 2017: Conservative Portfolios Review

- September 11, 2017: International Diversification Effect

- September 4, 2017: Invest And Speculate Revisited

- August 28, 2017: Total Return Bond Fund Portfolios: Where Do They Fit?

- August 21, 2017: Portfolio Performance: A Walk In The Past

- August 14, 2017: Fidelity Commission Free ETFs Update

- August 7, 2017: I Didn’t Learn Anything — Mistake vs. Temporary Underperformance

- July 31, 2017: Asset Classes And Fund Choices: A Primer

- July 24, 2017: Total Return Bond Fund Portfolios And Cash

- July 17, 2017: Long Term Stock Holding Periods For Retirement

- July 10, 2017: Half Year Asset Trend Review

- June 26, 2017: How To Beat The Best Balanced Allocation Fund

- June 19, 2017: Newsletter Collection Update

- June 12, 2017: A Mixed Bag Performance of Momentum Investing

- June 5, 2017: How To Start A New Portfolio

- May 29, 2017: Alternative Assets And Their Role In Portfolios

- May 22, 2017: Summer Seasonality And Portfolio Management

- May 15, 2017: Cash: Banking Or Investing?

- May 8, 2017: Holding Period of Long Term Timing Portfolios

- May 1, 2017: Debate on Risk vs. Volatility

- April 24, 2017: The Long Term Stock Market Timing Return Since 1871

- April 17, 2017: Risk vs. Volatility: Long Term Stock Market Returns

- April 10, 2017: Total Return Bond ETFs And Portfolios

- April 3, 2017: Quarter End Asset Trend Review

- March 27, 2017: Practical Consideration For IRAs And 401k Accounts

- March 20, 2017: Fund Fees: That’s (Still) Outrageous

- March 13, 2017: Long Term Stock Valuation Review

- March 6, 2017: Asset Classes for Retirement Investments

- February 27, 2017: Fidelity Total Bond Fund Review

- February 20, 2017: Long Term Stock Timing Based Portfolios And Their Roles

- February 13, 2017: Alternative Investment Portfolios Review

- February 6, 2017: Tax Free Municipal Bond Investments Review

- January 30, 2017: Brokerage Specific Conservative Portfolios

- January 23, 2017: Fixed Income Portfolio Review

- January 16, 2017: Long Term Trend Following Portfolio Review

- January 9, 2017: Tactical Asset Allocation Review

- January 3, 2017: Strategic Asset Allocation Review

- December 12, 2016: Enhanced Index Funds

- December 5, 2016: Review Of Broad Base Core Mutual Funds For Brokerages

- November 28, 2016: Core Index ETFs Review

- November 21, 2016: International Exposure Of U.S. Large Companies

- November 14, 2016: Asset Trends After The Election

- November 7, 2016: Rising Rate And Current Bond Trend

- October 31, 2016: Economy Power And Long Term Stock Returns

- October 24, 2016: Current Commodity Trend And Managed Futures

- October 17, 2016: Investment Mistakes And Good Or Bad Investment Strategies

- October 10, 2016: Momentum Investing Review

- October 3, 2016: Survey & Feedback

- September 26, 2016: Fixed Income Investing: Actively Managed Funds vs. Index Funds

- September 19, 2016: Stock Investing: Actively Managed Funds vs. Index Funds

- September 12, 2016: Newsletter Update

- September 5, 2016: Overvalued Markets And Long Term Timing Strategies

- August 29, 2016: Your 401K Finally Draws Attention

- August 22, 2016: Inflation Protected Securities TIPS For Current Overvalued Markets

- August 15, 2016: Risk On: Emerging Market Stocks And Small Cap Stocks

- August 8, 2016: Portfolio Construction Using Stock ETFs And Bond Mutual Funds

- August 1, 2016: Adding Value To Your Own Investments

- July 25, 2016: Tactical Asset Allocation Funds Review

- July 18, 2016: Strategic Asset Allocation & Lazy Portfolio Review

- July 11, 2016: Asset Trend Review

- June 27, 2016: Secular Cycles For Tactical And Strategic Investment Strategies

- June 20, 2016: A World of Debt

- June 13, 2016: Managed Futures For Portfolio Building

- June 6, 2016: Newsletter Summary

- May 30, 2016: Swensen Portfolio And Permanent Portfolios

- May 23, 2016: AAII Article And Some Web Changes

- May 16, 2016: The PIMCO (Dis)Advantages

- May 9, 2016: Boost Your Dull Summer Investments

- May 2, 2016: Low Cost Index Fund Investing

- April 25, 2016: Tax Free Municipal Bond Funds & Portfolios

- April 18, 2016: Asset Class Trend Review

- April 11, 2016: Construction of Sound And Conservative Portfolios

- March 28, 2016: Total Return Bond ETFs Review

- March 21, 2016: Small And Large Company Stock Performance In Different Economic Expansion Cycles

- March 14, 2016: Are Tactical And Timing Strategies Losing Steam?

- March 7, 2016: Defined Maturity Bond Fund Analysis

- February 29, 2016: Smart Strategic Asset Allocation Rebalance When Market Trend Changes

- February 22, 2016: Be Cash Smart

- February 15, 2016: Bond ETF Portfolios

- February 8, 2016: Newsletter Collection Update

- February 1, 2016: Total Return Bond Fund Portfolios In A Volatile Period

- January 25, 2016: Alternative Portfolios Review

- January 18, 2016: Strategic Asset Allocation: A Cautious Outlook

- January 11, 2016: Review Of Trend Following Tactical Asset Allocation

- January 4, 2016: What Worked And Didn’t In 2015

- December 21, 2015: Distressed Assets

- December 14, 2015: High Yield Bonds And Their Correlation With Stocks

- December 7, 2015: Diversification And Global Allocation

- November 30, 2015: Investors and Speculators Combined

- November 23, 2015: Active Stock Fund Performance Consistency

- November 16, 2015: Permanent, Risk Parity And Alternative Portfolios Review

- November 9, 2015: Broad Base Core Mutual Fund Review

- November 2, 2015: Broad Base Index Core ETFs Review

- October 26, 2015: Total Return Bond Fund Review

- October 19, 2015: Advanced Portfolio Review

- October 12, 2015: What About Commodities?

- October 5, 2015: Core Satellite Portfolios In A 401k Account

- September 28, 2015: Risk Managed Strategic Asset Allocation Portfolios Revisited

- September 21, 2015: Quest For The Best Investment Strategy

- September 14, 2015: Core Satellite Portfolios In Market Turmoil

- September 7, 2015: Market Rout Creates An Opportunity to Reposition Your Portfolios

- August 31, 2015: Review of Asset Allocation Funds and Portfolios

- August 24, 2015: Market Rout And Your Portfolios

- August 17, 2015: ETF or Mutual Fund Based Portfolios

- August 10, 2015: Updated Newsletter Collection

- August 3, 2015: Slippery Asset Trends

- July 27, 2015: Performance Dispersion Among Momentum Based Portfolios

- July 20, 2015: Global Balanced Portfolio Benchmarks

- July 13, 2015: Pain in Tactical Portfolios

- July 6, 2015: Fixed Income Total Return Bond Funds In Strategic Asset Allocation Portfolios

- June 29, 2015: Core ETF Commission Free Portfolios

- June 22, 2015: Secular Asset Trends

- June 15, 2015: Giving Up Bonds?

- June 1, 2015: Summer Blues?

- May 26, 2015: Cash, Bonds and Stocks In A Rising Rate Environment

- May 18, 2015: Portfolio Update

- May 11, 2015: Pain in Fixed Income?

- May 4, 2015: The Balanced Stock and Long Term Treasury Bond Portfolios

- April 27, 2015: Long Term Treasury Bond Behavior

- April 20, 2015: 529 College Savings Plan Rebalance Policy Change

- April 13, 2015: Total Return Bond Funds As Smart Cash

- April 6, 2015: The Low Return Environment

- March 30, 2015: Brokerage Specific Core Mutual Fund Portfolios 2

- March 23, 2015: Investment Arithmetic for Long Term Investments

- March 16, 2015: Brokerage Specific Core Mutual Fund Portfolios

- March 9, 2015: Newsletter Collection Update

- March 2, 2015: Total Return Bond ETFs

- February 23, 2015: Why Is Global Tactical Asset Allocation Not Popular?

- February 16, 2015: Where Are Permanent Portfolios Going?

- February 9, 2015: How Have Asset Allocation Funds Done?

- February 2, 2015: Risk Management Everywhere

- January 26, 2015: Composite Portfolios Review

- January 19, 2015: Fixed Income Investing Review

- January 12, 2015: How Does Trend Following Tactical Asset Allocation Strategy Deliver Returns

- January 5, 2015: When Forecast Fails

- December 22, 2014: Long Term Asset Returns: How Long Is Long?

- December 15, 2014: Beaten Down Assets

- December 8, 2014: Implementing Core Asset Portfolios In a Brokerage

- December 1, 2014: Two Key Issues of Investment Strategies

- November 24, 2014: Holiday Readings

- November 17, 2014: Retirement Spending Portfolios Update

- November 10, 2014: Fixed Income Or Cash

- November 3, 2014: Asset Trend Review

- October 27, 2014: Investment Loss, Mistakes And Market Cycles

- October 20, 2014: Strategic Portfolios With Managed Volatility

- October 13, 2014: Embrace Volatility

- October 6, 2014: Tips For 401k Open Enrollment

- September 29, 2014: What Can We Learn From Bill Gross’ Departure From PIMCO?

- September 22, 2014: Why Total Return Bond Funds?

- September 15, 2014: Equity And Total Return Bond Fund Composite Portfolios

- September 8, 2014: Momentum Based Portfolios Review

- September 1, 2014: Risk & Diversification: Mint.com Interview

- August 25, 2014: Remember Risk

- August 18, 2014: Consistency, The Most Important Edge In Investing: Tactical Case

- August 11, 2014: What To Do In Overvalued Stock Markets

- August 4, 2014: Is This The Peak Or Correction?

- July 28, 2014: Stock Musings

- July 21, 2014: Permanent Portfolios & Four Pillar Foundation Based Framework

- July 14, 2014: Composite Portfolios Review

- July 7, 2014: Portfolio Behavior During Market Corrections

- June 30, 2014: Half Year Brokerage ETF and Mutual Fund Portfolios Review

- June 23, 2014: Newsletter Collection Update

- June 16, 2014: There Are Always Lottery Winners

- June 9, 2014: The Arithmetic of Investment Mistakes

- June 2, 2014: Tips On Portfolio Rebalance

- May 26, 2014: In Praise Of Low Cost Core Asset Class Based Portfolios

- May 19, 2014: Consistency, The Most Important Edge In Investing: Strategic Case

- May 12, 2014: How To Handle An Elevated Overvalued Market

- May 5, 2014: Asset Allocation Funds Review

- April 28, 2014: Now The Economy Backs To The ‘Old Normal’, Should Our Investments Too?

- April 21, 2014: Total Return Bond Investing In The Current Market Environment