![]()

Understand Mega Backdoor Roth Conversion

In this issue:

- Latest in Retirement Savings & Personal Finance

- Understand Mega Backdoor Roth Conversion

- Tools & Tips: Backdoor Roth IRA Pro-Rata Conversion Calculator

- Market Overview

Latest in Retirement Savings & Personal Finance

IRAs Now Bigger Than 401(k)s, Is That All Good?

Recently, total assets in IRAs have surpassed those in 401(k)s. By a large margin, roughly $7 trillion more. That did not happen overnight. Over years, workers rolled money out of employer plans when they changed jobs, retired, or simply wanted “more control.” Quietly, the center of gravity in retirement system shifted. Less money sitting inside employer sponsored plans. More money sitting in individual accounts.

There are consequences. Not all good.

Bad side first.

- Protection is weaker. 401(k)s operate under ERISA fiduciary standards. Someone must act in your best interest. In an IRA, that obligation is often lighter. You are more on your own.

- Money is easier to take out. Fewer administrative hurdles. More exceptions. Convenience increases leakage. And leakage is silent enemy of compounding.

- Creditor and spousal protections can be less robust, depending on the situation. Less structural guardrails.

- Behavioral risk increases. Without plan oversight, investors may face higher fees, conflicted advice, or simply poor decisions.

Now the good side.

- More investment choices. A much broader universe than typical employer plans.

- Potentially lower costs, especially if you use low cost index funds or ETFs.

- Greater flexibility in asset allocation and strategy. You are not confined to employer selected options.

But that flexibility shifts responsibility entirely to the individual. More choices means more temptation. Easier to speculate. Easier to chase trends. Freedom is valuable, yes. Discipline becomes even more valuable. And discipline, as experience tells us, is never automatic.

Americans Retire Earlier Than Planned and It’s not what you think

It turns out that many Americans actually retired earlier than they say they want:

- Employee Benefit Research Institute, median expected retirement age is about 65, median actual retirement age is 62.

- Gallup surveys, workers say they plan to retire around 66, retirees report they actually retired around 61 to 62.

- Center for Retirement Research, 2024 estimates show retirement age at 64.6 for men and 62.6 for women.

- Social Security data, age 62 remains the most common claiming age. Roughly one quarter claim at 62, and close to half claim before full retirement age.

Now the reasons. This is where the gap becomes clearer.

From the 2025 EBRI survey:

- 40% of retirees said they retired earlier than planned.

- Among early retirees, 31% cited health problems or disability.

- Another 31% cited company changes, layoffs, downsizing, closures.

From a separate EBRI study of retirees age 62 to 75:

- 58% retired earlier than planned.

- 38% said health problems or disability was the primary reason.

- 23% cited employment related disruptions.

So roughly one third health. Roughly one quarter to one third labor market shocks. Not leisure. Not boredom. Not because markets did well.

Which means early retirement is often not a choice. It is a response to health limits or job loss. That is a different planning problem entirely.

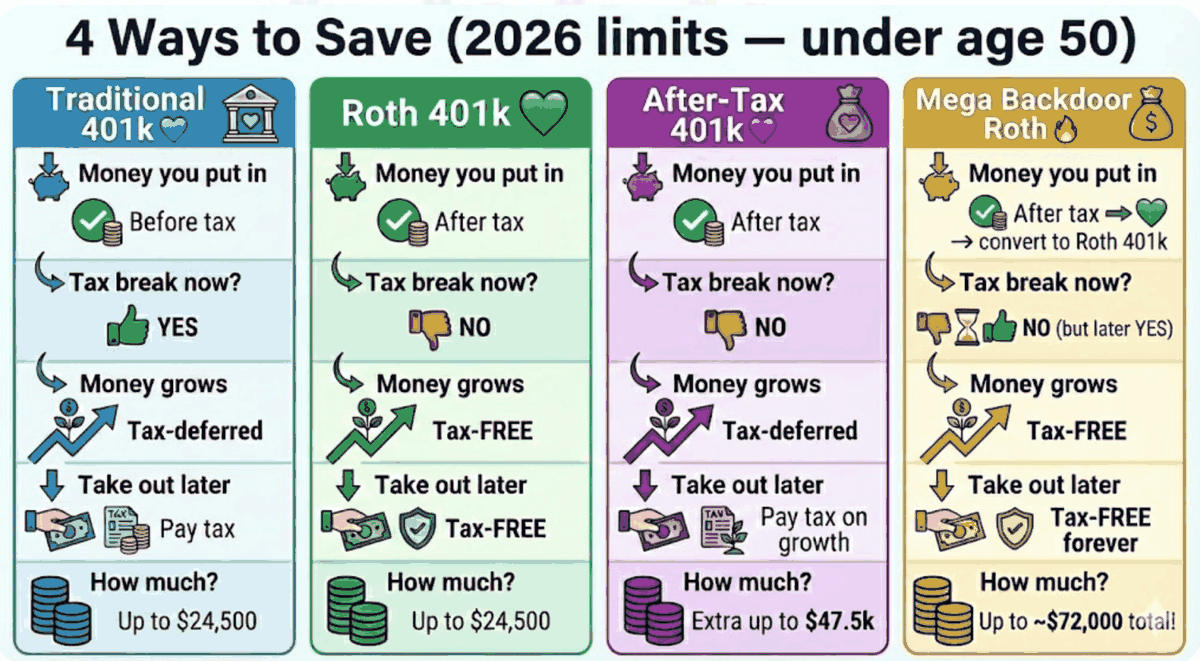

Understand Mega Backdoor Roth Conversion

Most employees today, if they look carefully at their benefits portal, usually see more than one 401(k) option. The traditional 401(k) is the default in many plans, pre tax contributions, tax deferred growth, tax paid later. Then there is the Roth 401(k), after tax contributions, tax free growth if rules are met. That Roth feature is no longer rare. Roughly 90% of large employer plans now offer a Roth 401(k) option. So at least on paper, employees can choose between paying taxes now or later.

Less understood are the after tax 401(k) contribution and the so called Mega Backdoor Roth conversion, especially the in plan Roth conversion. After tax 401(k) is different from Roth 401(k), it allows contributions beyond the regular elective deferral limit, up to the overall plan limit, but earnings are taxable unless converted. The Mega Backdoor Roth strategy uses those after tax dollars and converts them to Roth, often inside the plan, to create additional Roth space. Powerful, yes. But not common everywhere. Only about 25% to 30% of large plans allow after tax contributions, and a similar share permit in plan Roth conversions. So while the opportunity exists, many participants either do not have access, or simply do not realize the option is there.

The following is an infographic that’s helpful to explain these concepts.

See Mega Backdoor Roth Infographic article for more detailed explanations.

Worried About Big Loss That Might Derail Your Retirement Investments?

MyPlanIQ tactical asset allocation strategies utilize economic and financial market indicators to gauge investment risk and tactically reduce stock exposure if it deems necessary.

Our model portfolios have had more than a decade track record. Our well received monthly newsletters give informative insights into investment portfolios, funds and market conditions.

Paid subscription has 30-day free trial

(Expert tier: 14 days). Cancel anytime for a prorated refund.

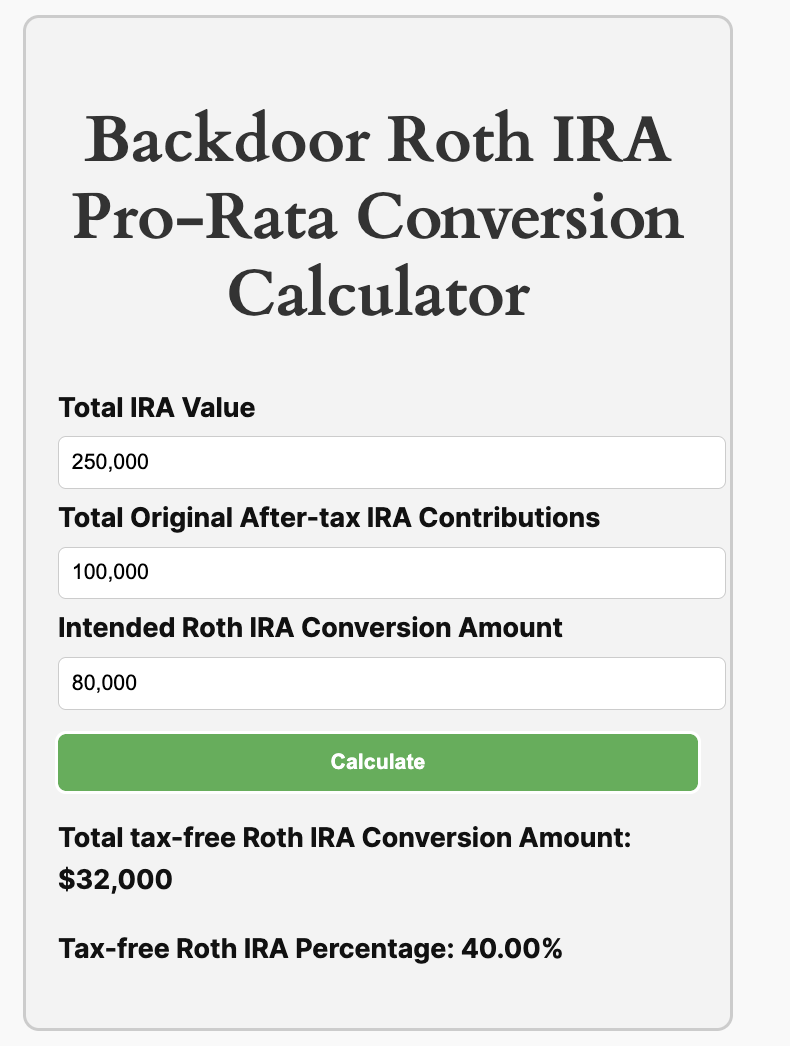

Tools & Tips: Backdoor Roth IRA Pro-Rata Conversion Calculator

This calculator helps you determine the tax-free portion of your Roth IRA conversion based on the pro-rata rule. By entering the total value of your IRA, your original after-tax contributions (excluding earnings), and your intended Roth IRA conversion amount, you can quickly calculate how much of your conversion will be tax-free and what percentage of your conversion is tax-exempt.

The calculator:

Market Overview

Markets have fluctuated so far this month. Though broad base indexes didn’t move much, software stocks and anything related to digital info processing stocks have been hammered.

| Asset Class | 1W | 4W | 13W | 26W | 52W | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 0.1% | -1.5% | 2.2% | 6.8% | 15.6% | 4.6% |

| Foreign Stocks | 0.6% | 3.8% | 15.3% | 18.4% | 37.1% | 15.1% |

| US REITs | 0.3% | 4.9% | 6.5% | 5.3% | 7.0% | 4.8% |

| Emerging Market Stocks | 0.7% | 2.3% | 10.6% | 14.2% | 30.7% | 11.7% |

| Bonds | 0.1% | 1.3% | 1.4% | 3.7% | 6.9% | 2.7% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

Upgrade to strengthen your

retirement savings while managing risk

Use our tactical asset allocation strategies in your retirement portfolio to seek stronger long-term returns while reducing exposure to frothy markets and potential economic slowdowns.

Or choose our fixed income model portfolios, which have outperformed leading bond funds for over a decade,

Or our smart factor and sector rotation portfolios that consistently beat S&P 500 stock index with less risk.

stocks and any other securities could lose money over any period of time. All investments involve risk.

Losses may exceed the principal invested. Past performance is not an indicator of future performance. There

is no guarantee for future results in your investment and any other actions based on the information

provided on the website including, but not limited to, strategies, portfolios, articles, performance data

and results of any tools. All rights are reserved and enforced. By accessing the website, you agree not to

copy and redistribute the information provided herein without the explicit consent from MyPlanIQ.