-

Understand Mega Backdoor Roth Conversion

- Latest in Retirement Savings & Personal Finance

- Understand Mega Backdoor Roth Conversion

- Tools & Tips: Backdoor Roth IRA Pro-Rata Conversion Calculator

- Market Overview

-

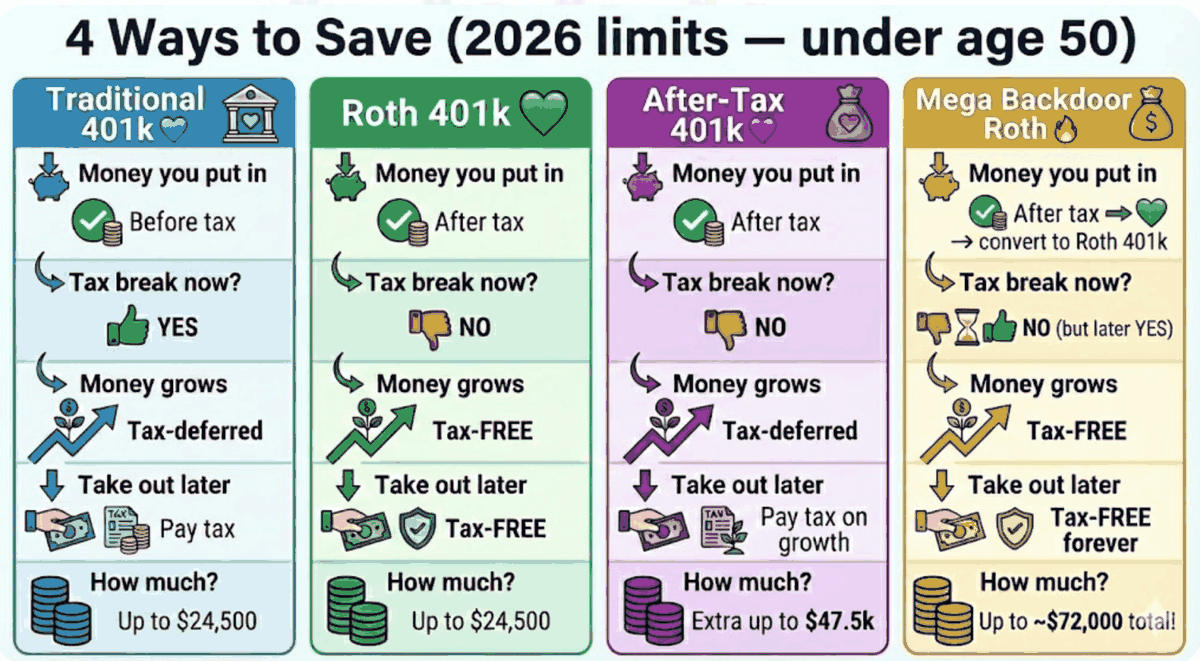

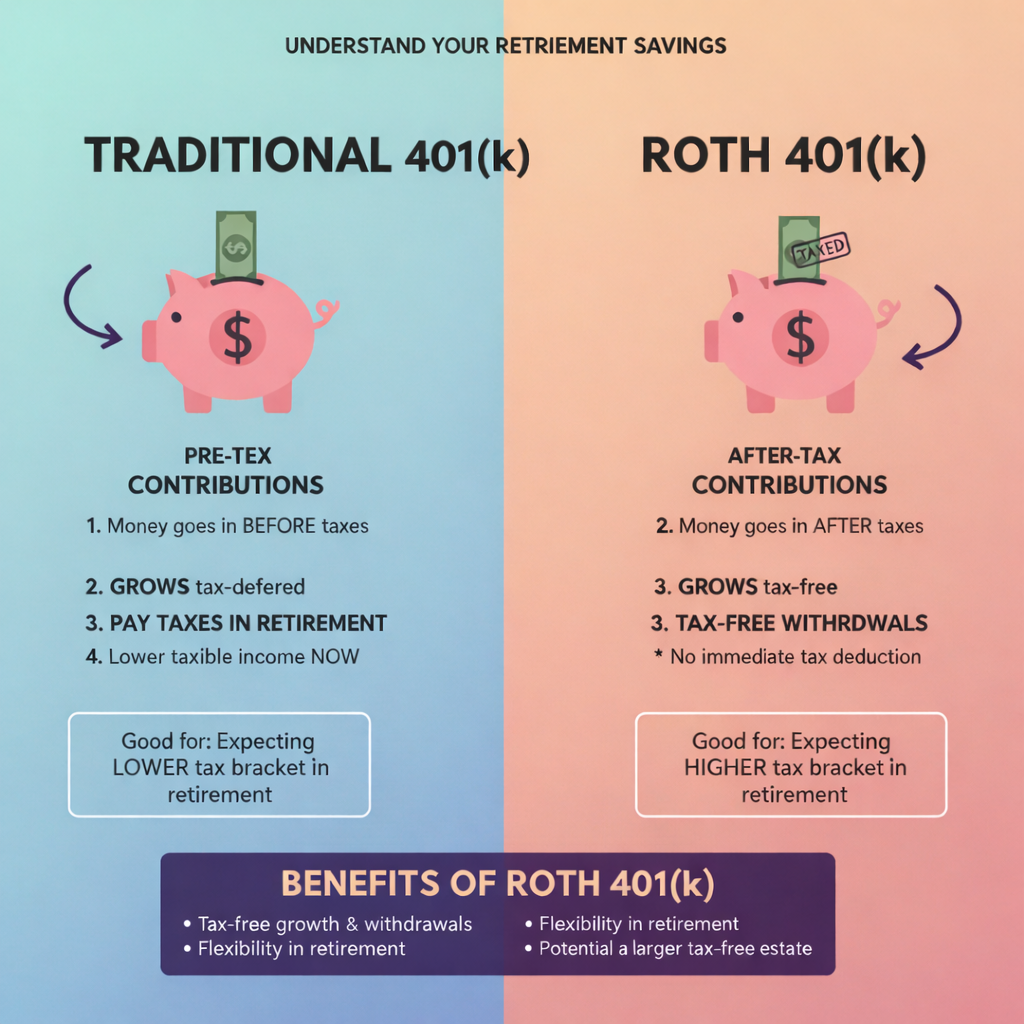

Mega Backdoor Roth Infographic

The infographic to illustrate the differences among traditional 401k, Roth 401k, After Tax 401k and Mega Backdoor Roth Conversion.

-

IRS Is Giving Out Money

- Latest in Retirement Savings & Personal Finance

- IRS Is Giving Out Money

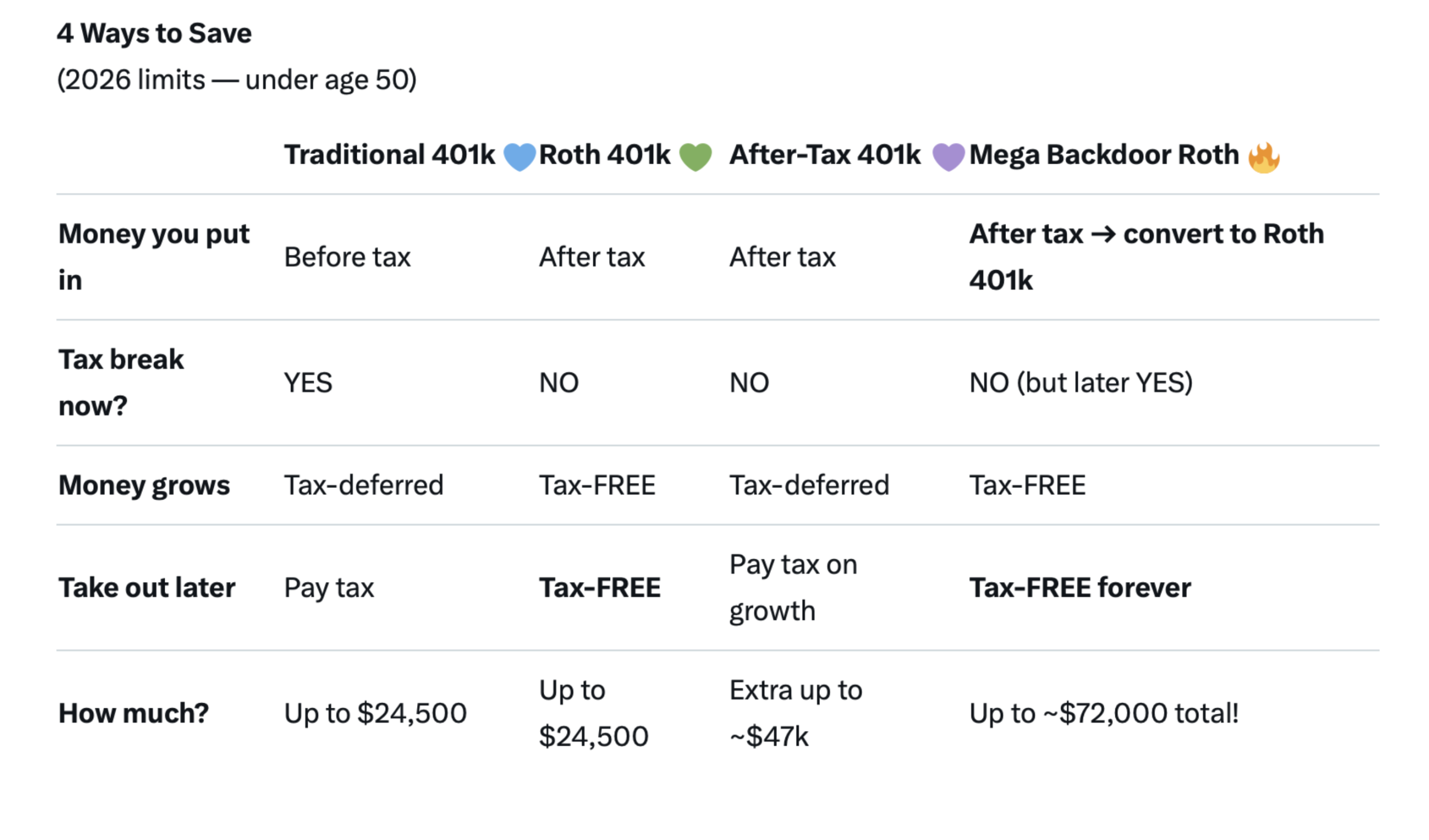

- Tools & Tips: RSU (Restricted Stock Unit) Calculator

- Market Overview

-

The Federal Reserve Bank and Your Money

- Latest in Retirement Savings & Personal Finance

- The Federal Reserve Bank and Your Money

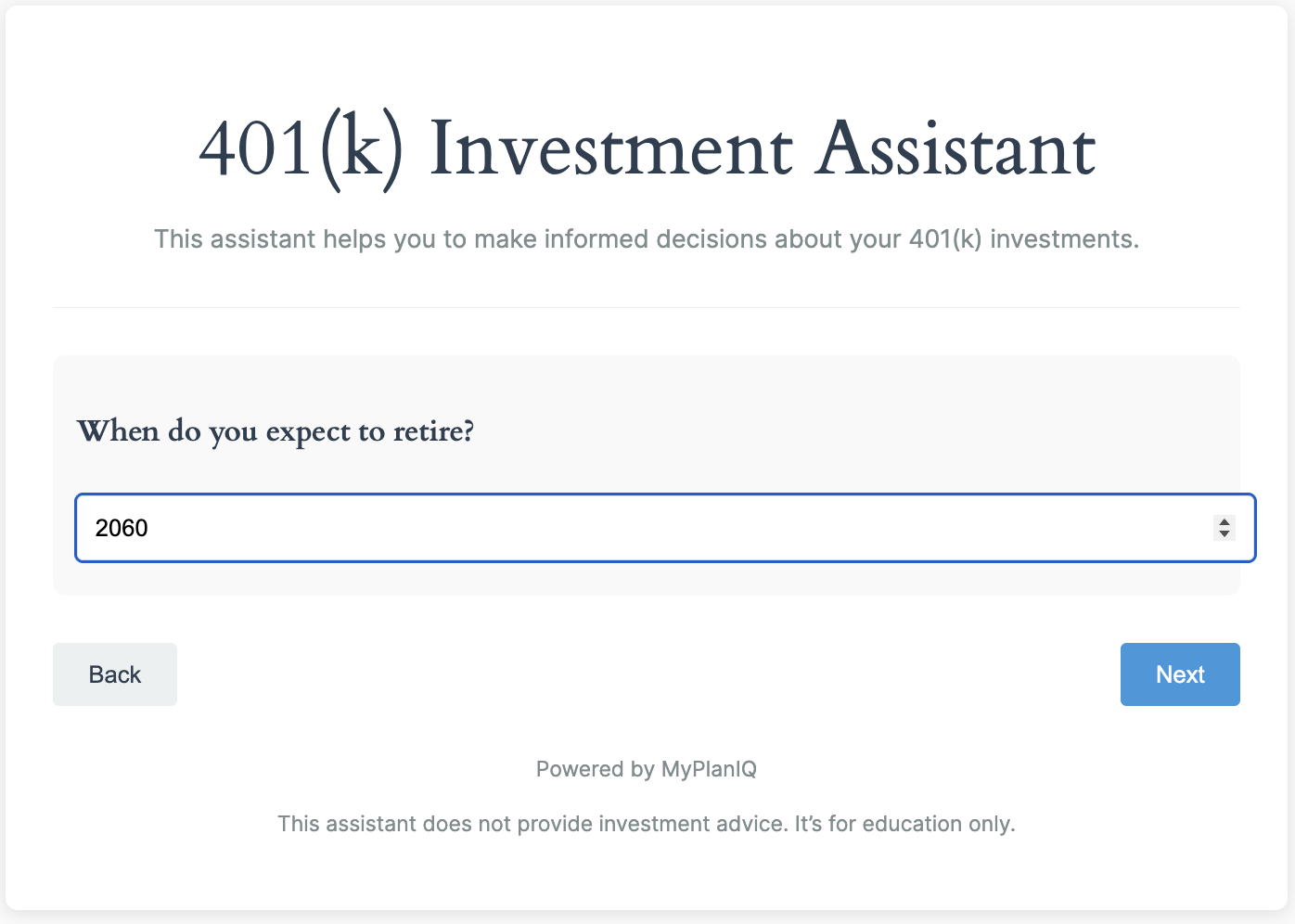

- Tools & Tips: 401(k) Investment Assistant

- Market Overview

-

2026 Tax Season Begins Today

- Latest in Retirement Savings & Personal Finance

- 2026 Tax Season Begins Today

- Tools & Tips: Traditional 401(K) vs. Roth 401(K)

- Market Overview

-

Useful Tips for 401(k)s, IRAs, and RMDs in the New Year

- Latest in Retirement Savings & Personal Finance

- Useful Tips for 401(k)s, IRAs, and RMDs in the New Year

- Tools & Tips: Roth IRA Compounding

- Market Overview

-

The $7,000 Roth IRA Myth, Why It Is a Bigger Deal Than People Think

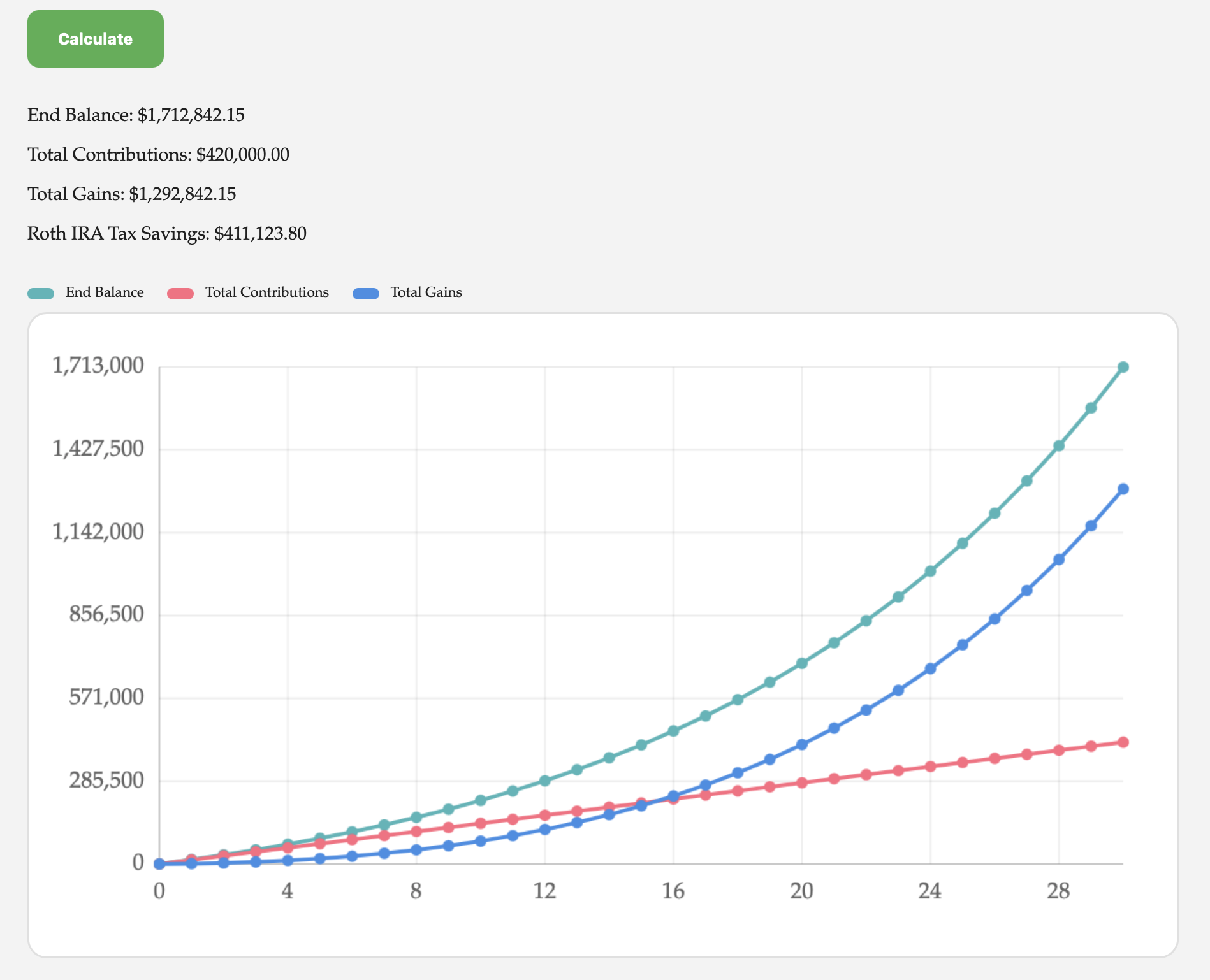

Many people look at the $7,000 annual Roth IRA limit and immediately dismiss it. Too small, not impactful, not worth the hassle. Big mistake! Let’s use a simple example. A husband and wife each contribute $7,000 a year, so $14,000 total, from age 30 to 60. That is 30 years of steady investing at an assumed 8 percent return. Total contributions come to $420,000. By age 60, that Roth balance grows to about $1.6 million. Roughly $1.16 million of that is pure growth, and it comes out tax free. If you live in a no state tax environment, you just avoided federal long term capital gains and the extra 3.8 percent surtax on investment income, already a meaningful number. Now layer in a high tax state. At an 8 percent state tax rate, that same $1.16 million of gains would have faced another large haircut (actually like $411K tax savings). The Roth just simply protects such a big chunk of your gain. The following are results from our Investment Return Calculator: And it does not stop there. Most people do not touch Roth money first. They let it keep compounding while spending from pre tax or taxable accounts. Let that same Roth grow another 10 years, untouched, at the same 8 percent. By age 70, it is worth roughly $3.9 million. Now you are looking at close to $3.3 million of gains that will never be taxed. In a zero state tax scenario, that already avoids a large federal tax bill. In an 8 percent state tax scenario, the difference becomes even more dramatic: a $1 million savings. This is where people underestimate the impact. The contribution feels small. The tax free compounding over decades is not. This is real money, not theoretical. High income earners often respond with another objection. Fine, but my income is too high to contribute to a Roth IRA anyway. Not really. This is where the backdoor Roth comes in. The process is simple in concept. You contribute to a traditional IRA using after tax dollars, since there is no income limit on contributions. Then you convert that contribution to a Roth IRA. If done correctly and promptly, there is little to no tax cost. The key rule is that you cannot have other pre tax IRA balances sitting around, including SEP or SIMPLE IRAs, or the conversion becomes partially taxable. Many people solve this by rolling old IRAs into a 401(k) first. Once set up, this becomes a repeatable annual process. So the real question is not whether the Roth is too small to matter. It is whether you want to keep paying taxes on millions of dollars of future growth, or quietly opt out while you still can.

-

Ultimate 2026 Retirement Playbook for 401(k)s & IRAs

Extremely use tips to maximizing 401(k) match, RMDs and IRA tactics

-

New Year Resolutions for Your Personal Finance

- Latest in Retirement Savings & Personal Finance

- New Year Resolutions for Your Personal Finance

- MyPlanIQ 2026 Market Outlook

-

2025 Crystal Ball Market Prediction Scorecard

- Latest in Retirement Savings & Personal Finance

- Stock Market Bubble & Retirement Savings

- Tools & Tips: Retirement Spending Calculator

- Market Overview

-

Personal Finance Year End Check List

- Latest in Retirement Savings & Personal Finance

- Personal Finance Year End Check List

- Tools & Tips: 12% Tax Bracket Is the Sweet Spot for Roth IRA Conversion

- Market Overview

-

Retirement Plan Contribution Limits in 2026

Comprehensive retirement plans (401(k), 403(b, 457(b), Solo 401(k), SEP IRA, SIMPLE IRA, IRA, Roth IRA, TSP, HSA etc.) contribution limits for 2026

-

How Retirement Savings Can Quietly Reduce Your Student Loan Payments

Increasing Retirement Savings such as 401(k) can help reduce your monthly student repayment if you are on the federal IBR program. But

-

Super Businesses, Super Stocks

- Latest in Retirement Savings & Personal Finance

- Super Businesses, Super Stocks

- Tools & Tips: Return Comparison Calculator

- Market Overview

-

2024 Millionaire Retirement Plans

- Latest in Retirement Savings & Personal Finance

- 2024 Millionaire Retirement Plans

- Tools & Tips: Historical Stock Dividend Yield Chart

- Market Overview

-

Last Quarter Checklist for 2025

- Latest in Retirement Savings & Personal Finance: All the Glittering Gold, Highest Household Credit Card Debt, More PE Funds Than McDonald’s

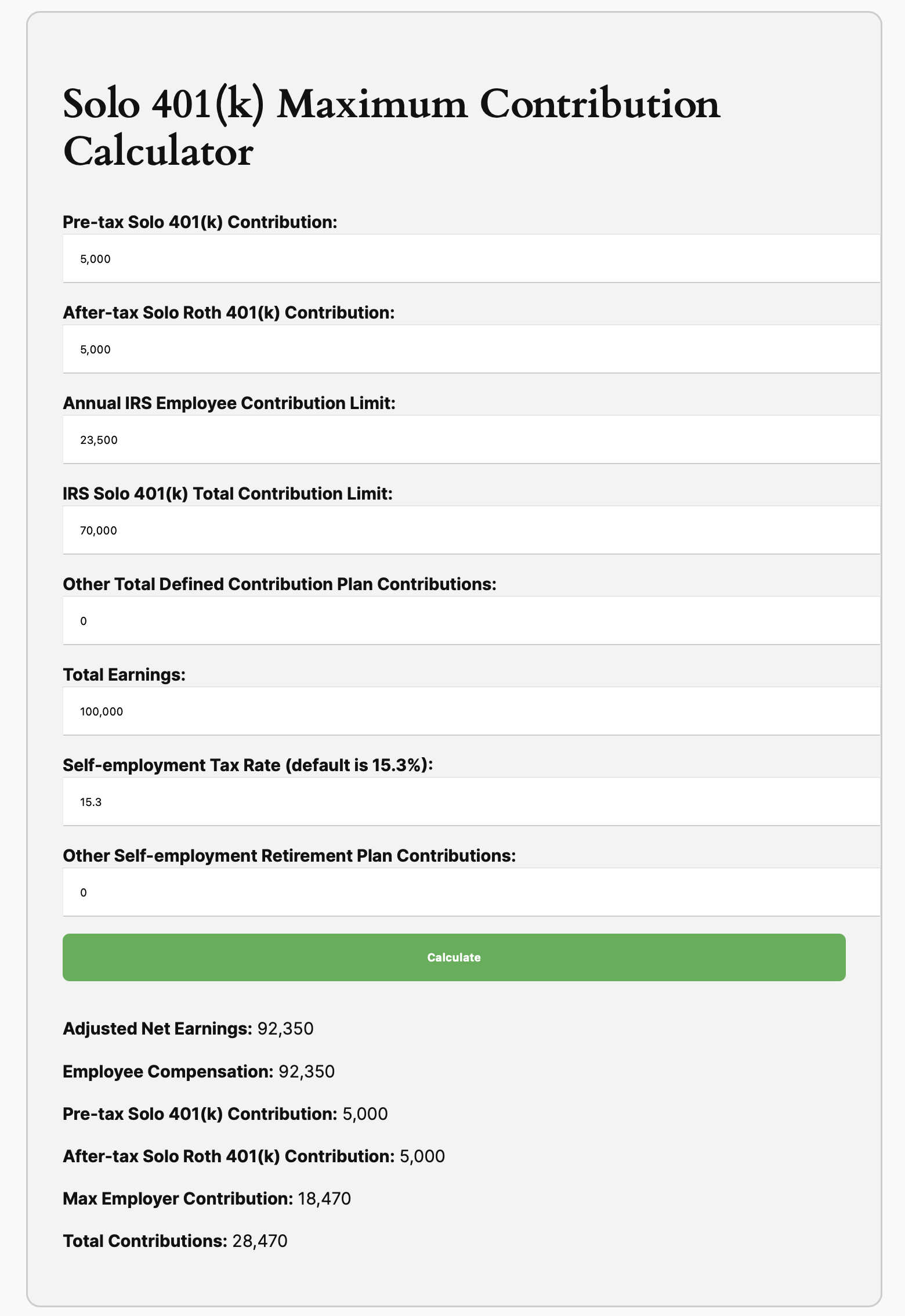

- Last Quarter Checklist for 2025

- Tools & Tips: Solo 401(k) Maximum Contribution Calculator

- Market Overview

-

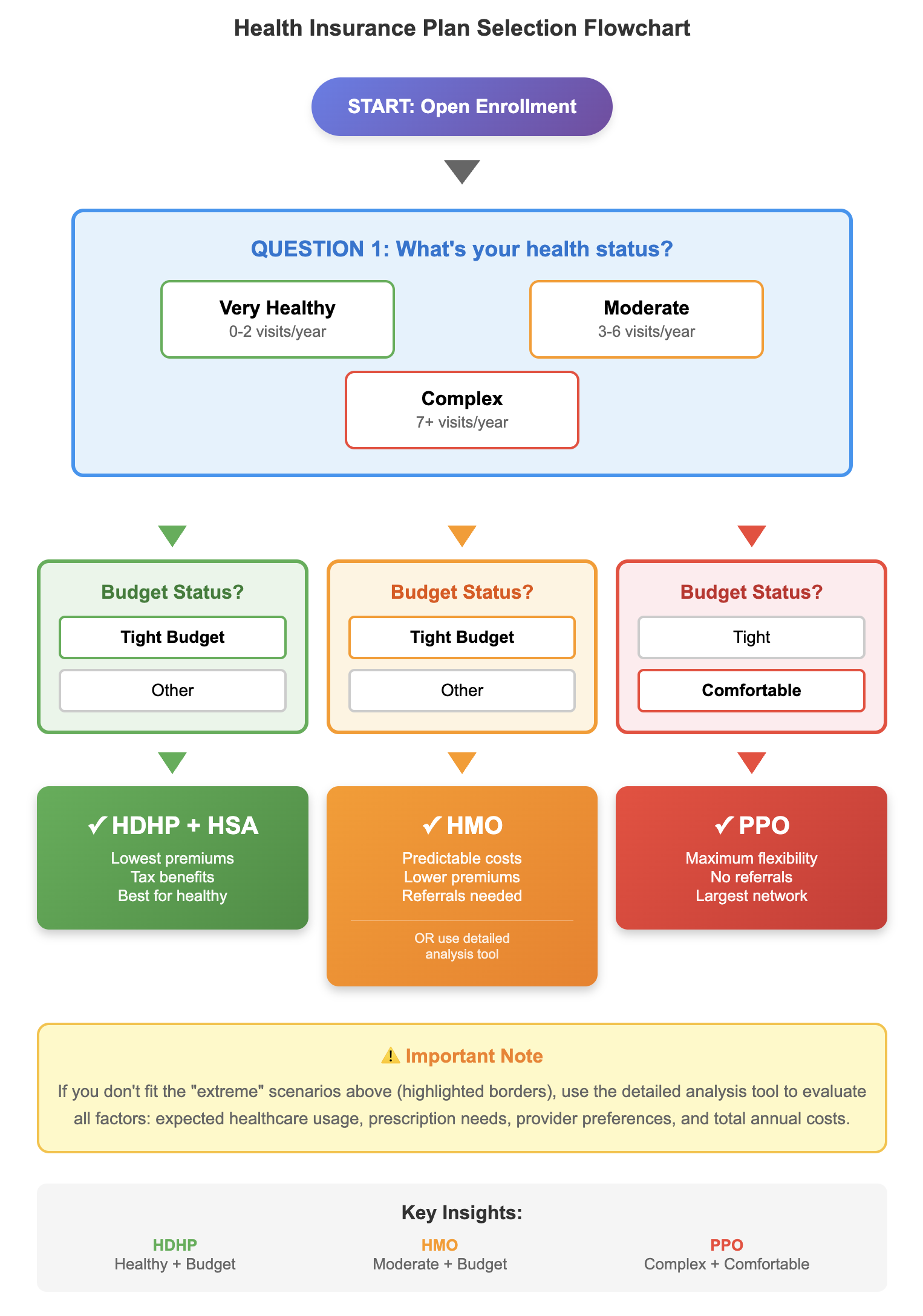

Which Health Insurance Plan Is Better: HMO, PPO or HDHP?

- Latest in Retirement Savings & Personal Finance: Highest Health Benefit Cost in 15 Years, Visualize Americans’ Healthcare Affordability, Americans Admire Luxury Spending

- Which Helath Insurance Plan Is Better: HMO, PPO or HDHP?

- Tools & Tips: Health Insurance Plan Type Helper

- Market Overview

-

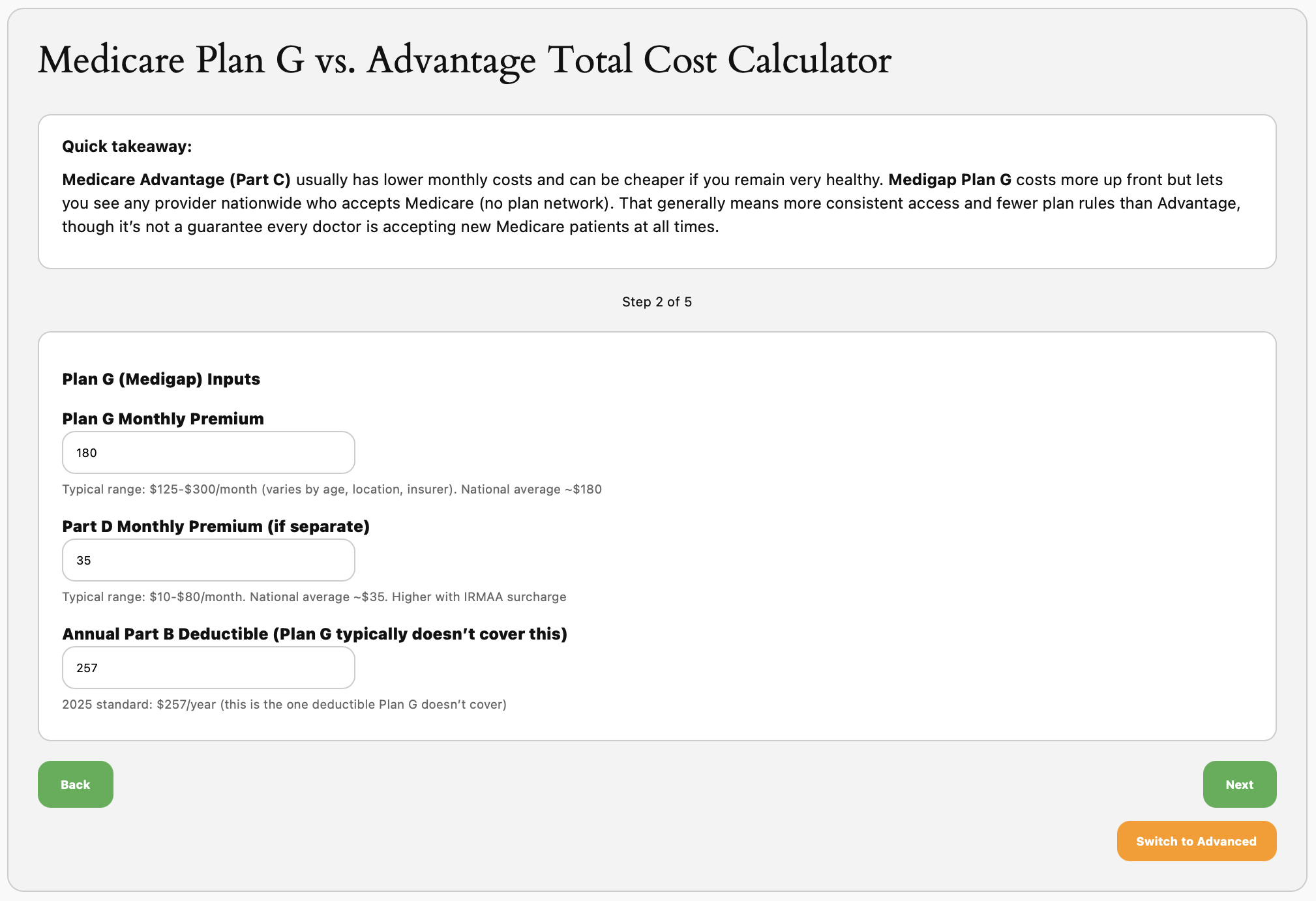

How to Navigate Medicare Maze

- Latest in Retirement Savings & Personal Finance: Shutdown Showdown,Turning Fulough into an Opportunity,Subprime Auto Loan Trouble

- Traditional Medicare (Medigap) vs. Medicare Advantage

- Tools & Tips: Medicare Medigap vs. Medicare Advantage Total Cost Calculator

- Market Overview

-

Microsoft Roth 401(k) & Mega Backdoor Roth Strategy Guide 2025

Microsoft Corporation’s Savings Plus 401(k) Plan gives you every tool needed to build tax-free retirement wealth: Roth salary deferrals, generous after-tax capacity, and instant in-plan conversions. This guide explains how to harness those features in 2025 so you can graduate from “traditional saver” to future tax-free millionaire. ✅ Available: Microsoft Roth 401(k) Pre-tax and Roth deferrals run through the same Fidelity portal. Switching your paycheck elections to Roth lets you pay taxes now while locking in tax-free qualified withdrawals later. Catch-up contributions ($7,500) can be directed to Roth as well. ✅ Available: Mega Backdoor Roth via After-Tax Contributions Microsoft supports sizable after-tax contributions (historically up to $34,500) plus in-plan Roth conversions. That combination satisfies the two critical requirements for executing a mega backdoor Roth inside Fidelity NetBenefits. Roth 401(k) Benefits for Microsoft Employees The Roth 401(k) bucket grows tax-free and distributes tax-free as long as you hold the account for five years and reach age 59½. Because Microsoft allows you to defer up to 65% of eligible pay (subject to the IRS $23,000 limit, or $30,500 with catch-up), high earners can rapidly build Roth balances while still collecting the full employer match. Mega Backdoor Roth Playbook Microsoft’s plan checks every box for the mega backdoor Roth (MBDR) tactic: after-tax contributions, in-plan conversions, and a high overall contribution ceiling (IRS Section 415(c) limit of $69,000, or $76,500 with catch-up). By filling the after-tax bucket and immediately converting it to Roth, you can move tens of thousands of dollars into tax-free growth every year. Interactive Roth vs. Traditional Calculator .available-feature { background: #f3f9ff; border-left: 4px solid #1966d2; padding: 1.25rem 1.5rem; border-radius: 0.75rem; margin: 1.5rem 0; } .strategy-comparison { background: #f7fbff; border: 1px solid #d4e5ff; border-radius: 0.75rem; padding: 1.25rem 1.75rem; margin: 1.5rem 0; } .wp-block-group.roth-calculator, .wp-block-group.mbdr-calculator { background: #f3f3f3; border: 1px solid #cccccc; border-radius: 0.9rem; padding: 1.5rem; margin: 2rem auto; max-width: 60%; } .wp-block-group.roth-calculator h3, .wp-block-group.mbdr-calculator h3 { margin-top: 0; color: #143c7d; } .calculator-inputs { display: flex; flex-direction: column; gap: 1rem; margin-bottom: 1.25rem; } .calculator-inputs label { display: flex; flex-direction: column; font-weight: 700; color: #102a53; } .calculator-inputs input, .calculator-inputs select { margin-top: 0.5rem; padding: 0.65rem 0.8rem; border-radius: 0.6rem; border: 1px solid #b8c7e3; font-size: 1rem; background: #ffffff; max-width: 18rem; } .calculator-inputs button { align-self: flex-start; padding: 0.85rem 1.4rem; border: none; border-radius: 0.6rem; background: #4CAF50; color: #ffffff; font-weight: 700; cursor: pointer; transition: transform 0.15s ease, box-shadow 0.15s ease; } .calculator-inputs button:hover { transform: translateY(-1px); box-shadow: 0 8px 16px rgba(76, 175, 80, 0.25); } .calculator-results { background: #ffffff; border-radius: 0.75rem; border: 1px solid #d5deef; padding: 1.1rem; color: #0f2557; } .calculator-results p { margin: 0.5rem 0; } .calculator-results ul { padding-left: 1.25rem; margin: 0.5rem 0; } .calculator-note { font-size: 0.9rem; color: #374f7a; margin-top: 0.75rem; } @media (max-width: 960px) { .wp-block-group.roth-calculator, .wp-block-group.mbdr-calculator { max-width: 90%; } } @media (max-width: 640px) { .calculator-inputs input, .calculator-inputs select { max-width: 100%; } } Roth vs. Traditional 401(k) Calculator for Microsoft Employees Current Age Household Income ($) Current Tax Bracket 12%22%24%32%35%37% Expected Retirement Tax Bracket 12%22%24%32% Annual Contribution ($) Expected Annual Return (%) Compare Roth vs. Traditional Assumes retirement at age 65 and constant contribution/return rates. Adjust inputs to reflect your tax outlook. const IRS_DEFERRAL_LIMIT = 23000; const CATCH_UP_LIMIT = 7500; const IRS_415C_LIMIT = 69000; function parseCurrencyInput(rawValue) { if (rawValue === undefined || rawValue === null) { return 0; } const cleaned = rawValue.toString().replace(/,/g, ”).trim(); const numeric = Number(cleaned); if (Number.isNaN(numeric)) { return 0; } return numeric; } function formatCurrency(value) { return ‘$’ + value.toLocaleString(‘en-US’, { minimumFractionDigits: 2, maximumFractionDigits: 2 }); } function formatCompactCurrency(value) { return ‘$’ + value.toLocaleString(‘en-US’, { maximumFractionDigits: 2 }); } function syncCurrencyInput(id) { const el = document.getElementById(id); if (!el) { return; } el.value = parseCurrencyInput(el.value).toLocaleString(‘en-US’, { maximumFractionDigits: 0 }); } function calculateFutureValue(contribution, years, rate) { if (rate === 0) { return contribution * years; } const futureFactor = Math.pow(1 + rate, years) – 1; return contribution * futureFactor / rate; } function calculateRothComparison() { syncCurrencyInput(‘rcIncome’); syncCurrencyInput(‘rcContribution’); const age = Number(document.getElementById(‘rcCurrentAge’).value); const income = parseCurrencyInput(document.getElementById(‘rcIncome’).value); const currentTax = Number(document.getElementById(‘rcCurrentTax’).value); const retirementTax = Number(document.getElementById(‘rcRetirementTax’).value); const annualContribution = parseCurrencyInput(document.getElementById(‘rcContribution’).value); const annualReturnPercent = Number(document.getElementById(‘rcReturn’).value); const output = document.getElementById(‘rcResults’); if (age < 18 || annualContribution

-

How Much Cash Do You Need?

- Latest in Retirement Savings & Personal Finance: Stocks Most Expensive,Low Number of Job Postings,Naming Your Baby $30K A Pop

- How Much Cash Do You Need?

- Tools & Tips: Emergency Income Checker

- Market Overview