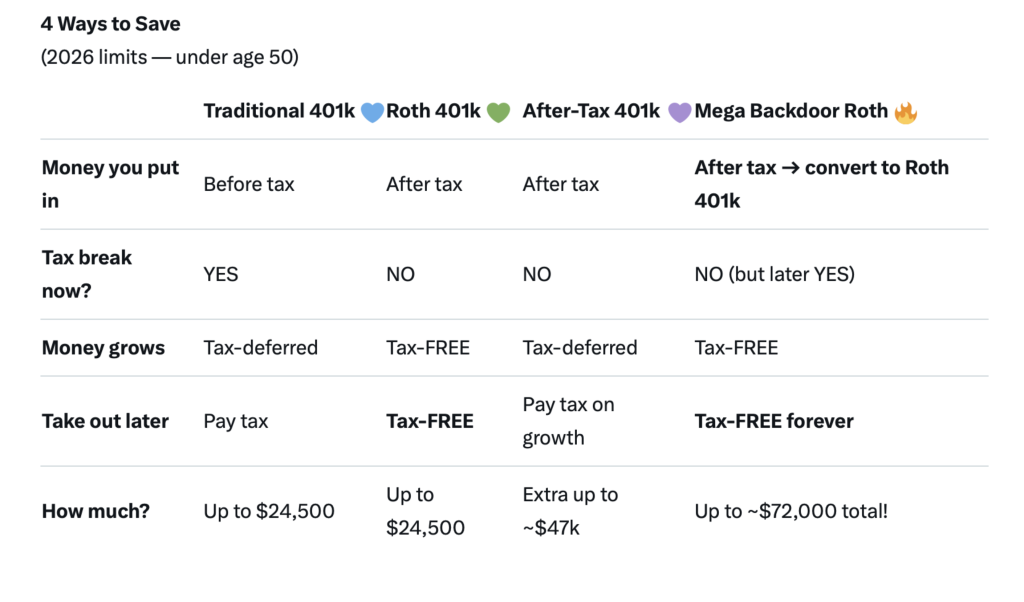

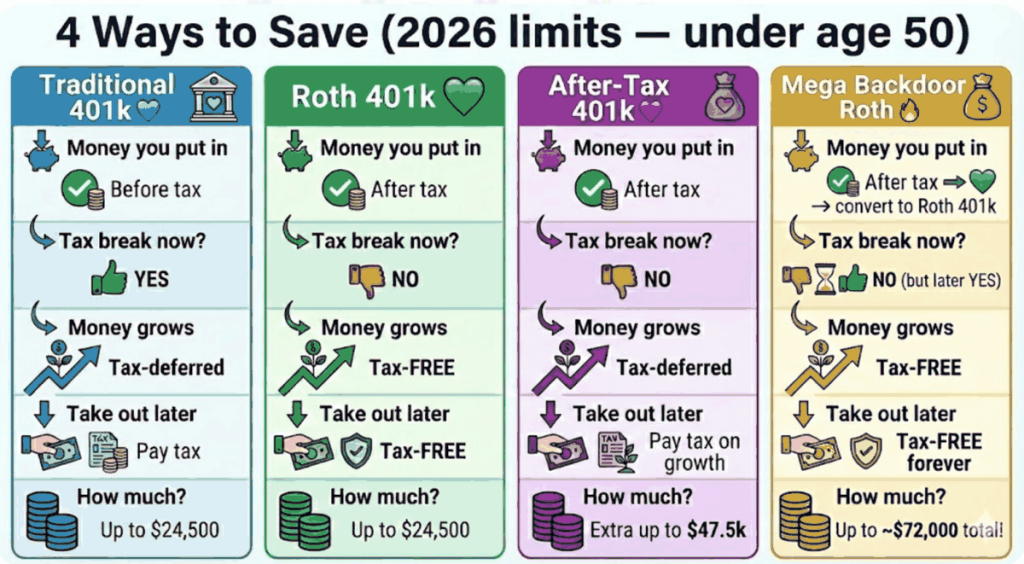

Most employees today, if they look carefully at their benefits portal, usually see more than one 401(k) option. The traditional 401(k) is the default in many plans, pre tax contributions, tax deferred growth, tax paid later. Then there is the Roth 401(k), after tax contributions, tax free growth if rules are met. That Roth feature is no longer rare. Roughly 90% of large employer plans now offer a Roth 401(k) option. So at least on paper, employees can choose between paying taxes now or later.

Less understood are the after tax 401(k) contribution and the so called Mega Backdoor Roth conversion, especially the in plan Roth conversion. After tax 401(k) is different from Roth 401(k), it allows contributions beyond the regular elective deferral limit, up to the overall plan limit, but earnings are taxable unless converted. The Mega Backdoor Roth strategy uses those after tax dollars and converts them to Roth, often inside the plan, to create additional Roth space. Powerful, yes. But not common everywhere. Only about 25% to 30% of large plans allow after tax contributions, and a similar share permit in plan Roth conversions. So while the opportunity exists, many participants either do not have access, or simply do not realize the option is there.

The following are the table and infographic that might be helpful to explain these differences.

The infographic:

You might say, wait, what about I just use backdoor IRA conversion? Well it turns out that first of all, you generally cannot simply move your after tax 401(k) money out to an IRA if you are still with your employer, unless the plan allows in service withdrawals. Furthermore, even if you manage to move your after tax 401(k) to an IRA, or you simply want to convert your traditional IRA to a Roth IRA, you will be subject to the so called pro rata Roth IRA conversion rule. This rule requires that you look at all of your traditional IRAs, pre tax and after tax, in aggregate, and then determine the taxable portion proportionally when converting to a Roth IRA.

What this means in practice is that if you have other traditional IRA balances sitting elsewhere, part of those pre tax dollars will be included in the conversion calculation. You cannot just isolate the after tax portion. So some percentage of the conversion becomes taxable, even if your intention was to convert only after tax money. The most important advantage of an in plan Roth 401(k) conversion is that it is not subject to this pro rata rule. That separation alone can make a meaningful difference.

For related information, see Mega Backdoor Roth Calculator.