-

Your IRA Can Buy ETFs That Rival Even the Lowest-Cost Plan Funds

You could almost find the lowest cost reputable ETFs that rival against those lowest funds offered in some large retirement plans.

-

Understand Mega Backdoor Roth Conversion

- Latest in Retirement Savings & Personal Finance

- Understand Mega Backdoor Roth Conversion

- Tools & Tips: Backdoor Roth IRA Pro-Rata Conversion Calculator

- Market Overview

-

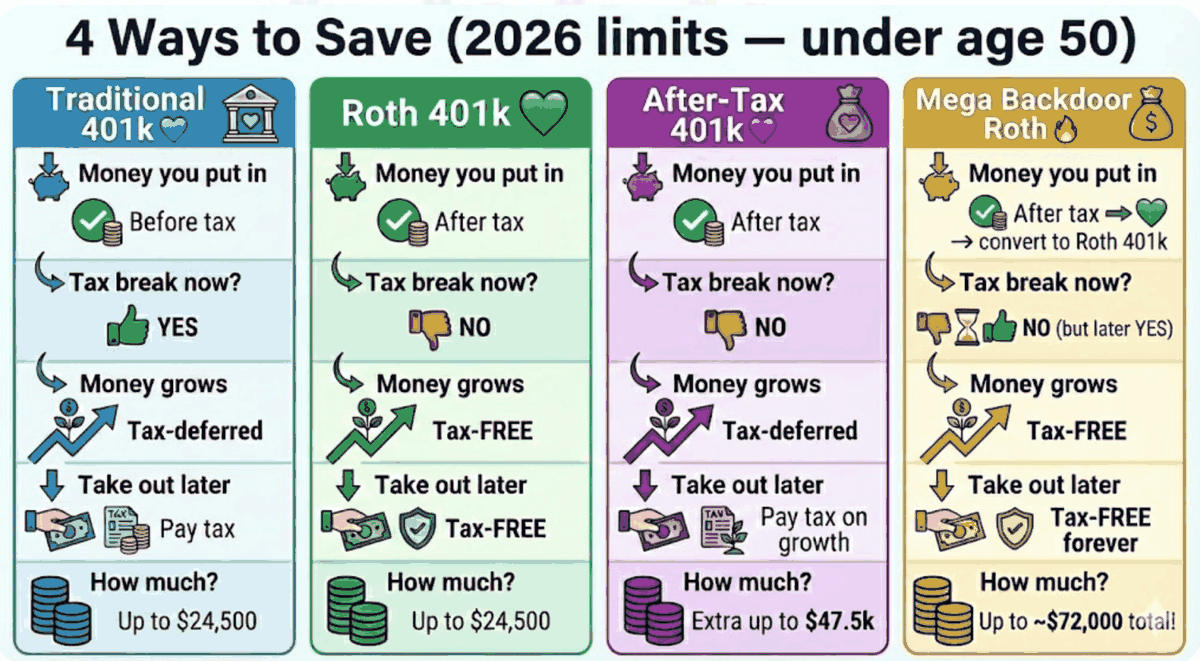

Mega Backdoor Roth Infographic

The infographic to illustrate the differences among traditional 401k, Roth 401k, After Tax 401k and Mega Backdoor Roth Conversion.

-

Ultimate 2026 Retirement Playbook for 401(k)s & IRAs

Extremely use tips to maximizing 401(k) match, RMDs and IRA tactics

-

Retirement Plan Contribution Limits in 2026

Comprehensive retirement plans (401(k), 403(b, 457(b), Solo 401(k), SEP IRA, SIMPLE IRA, IRA, Roth IRA, TSP, HSA etc.) contribution limits for 2026

-

How Retirement Savings Can Quietly Reduce Your Student Loan Payments

Increasing Retirement Savings such as 401(k) can help reduce your monthly student repayment if you are on the federal IBR program. But

-

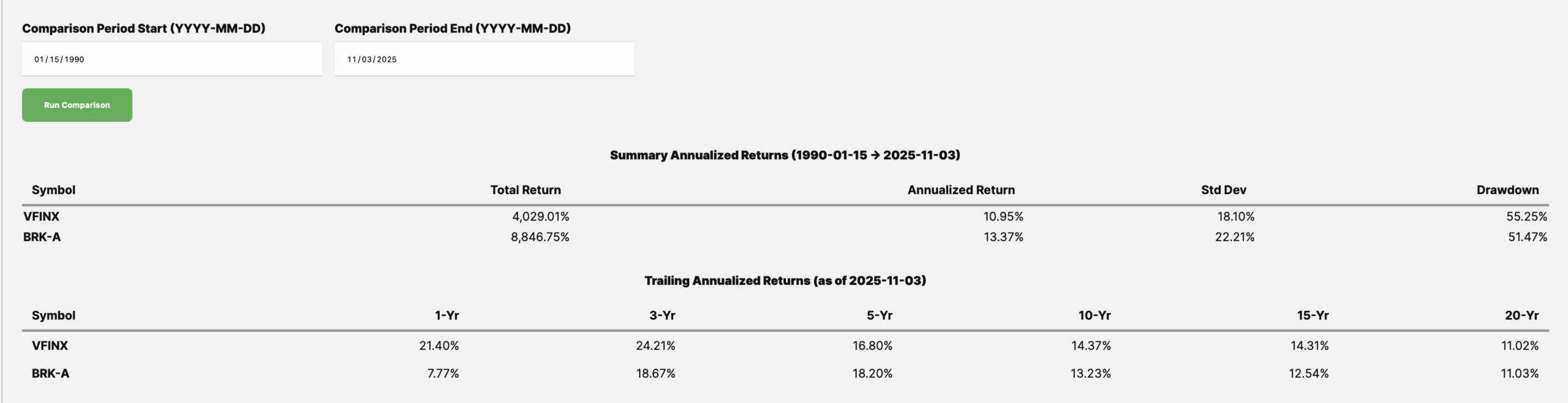

Super Businesses, Super Stocks

- Latest in Retirement Savings & Personal Finance

- Super Businesses, Super Stocks

- Tools & Tips: Return Comparison Calculator

- Market Overview

-

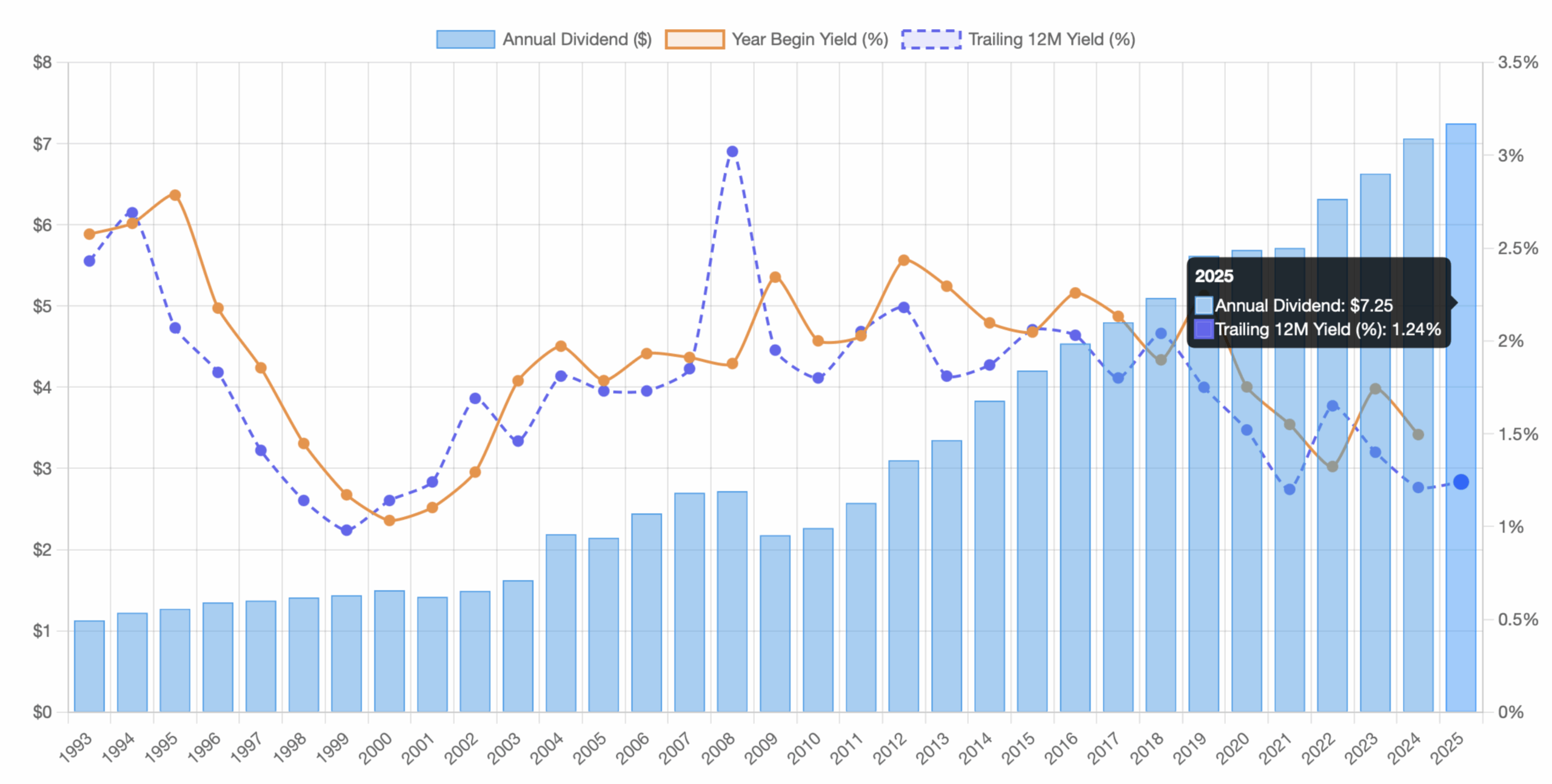

2024 Millionaire Retirement Plans

- Latest in Retirement Savings & Personal Finance

- 2024 Millionaire Retirement Plans

- Tools & Tips: Historical Stock Dividend Yield Chart

- Market Overview

-

The Quiet Millionaires of 2024: What Sets These Retirement Plans Apart

Every year, when new 401(k) data is released, it quietly reveals how uneven wealth building can be. In 2024, that picture is especially clear. The retirement plans with the highest average balances mostly belong to two types of organizations. On one side are high-income professionals such as physicians, lawyers, and boutique asset managers. These groups tend to have both strong personal contributions and large employer matches, often tied to firm profits. On the other side, a few large corporations, such as Texas Instruments and General Re, show that slow and steady saving across decades can also create significant wealth. MyPlanIQ recently did a study on all year 2024 retirement plans. We identified the top retirement plans that have the highest average participant account value. We limited our study in plans that have at least 100 participants. Below is a summary of the top 37 retirement plans by average account value. The numbers speak for themselves. Rank Retirement Plan Sponsor Average Account Value 1 Lone Pine Capital LLC 401(k) Profit Sharing Plan Lone Pine Capital LLC $1,612,021 2 Anesthesia Service Medical Group, Inc. 401(k) Profit Sharing Plan Trust Anesthesia Service Medical Group, Inc. $1,240,779 3 Medical Center Emergency Services Retirement Savings Thrift Plan Medical Center Emergency Services $1,217,978 4 Crescent River Port Pilots’ Association 401(k) Retirement Plan Crescent River Port Pilots’ Association $1,172,843 5 Irell & Manella Profit Sharing Plan Irell & Manella LLP $1,003,150 6 Anesthesia Consultants of Indianapolis, LLC 401(k) Profit Sharing Plan Anesthesia Consultants of Indianapolis, LLC $975,046 7 Fond du Lac Regional Clinic, S.C. 401(k) Profit Sharing Plan Fond du Lac Regional Clinic, S.C. $967,649 8 Wasatch Advisors, LP Deferred Profit Sharing Plan and Trust Wasatch Advisors, LP $924,154 9 Dodge & Cox Profit Sharing Plan Dodge & Cox $912,271 10 National Exchange Carrier Association Retirement Savings Plan National Exchange Carrier Association, Inc. $893,253 11 TI 401(k) Savings Plan Texas Instruments Incorporated $882,313 12 Employee Savings and Stock Ownership Plan of General Re Corp and its Domestic Subsidiaries General Re Corporation $862,746 13 Kleinberg, Kaplan, Wolff & Cohen, P.C. 401(k) Profit Sharing Plan Kleinberg, Kaplan, Wolff & Cohen, P.C. $860,649 14 Zeta Associates Incorporated Savings Plan Zeta Associates $829,709 15 Anesthesia Consultants of Indianapolis, LLC 401(k) Profit Sharing Plan Anesthesia Consultants of Indianapolis, LLC $804,322 16 Jennison Associates Savings Plan Jennison Associates LLC $797,881 17 Nutter, McClennen & Fish, LLP Lawyers Retirement Plan Nutter, McClennen & Fish, LLP $792,777 18 Carter Ledyard & Milburn LLP 401(k) Retirement Plan Carter Ledyard & Milburn LLP $778,761 19 Medical Anesthesia Group, P.A. Profit Sharing Plan Medical Anesthesia Group, P.A. $754,092 20 Bayerische Landesbank NY Employees Retirement Plan Bayerische Landesbank $747,774 21 Barrow, Hanley Profit Sharing & 401(k) Plan Barrow, Hanley, Mewhinney and Strauss, LLC $736,341 22 Callan LLC Retirement Savings Plan Callan LLC $717,465 23 Sills Cummis & Gross P.C. Defined Contribution Plan Sills Cummis & Gross P.C. $716,205 24 Maverick Capital, Ltd. 401(k) Plan Maverick Capital, Ltd. $676,958 25 Progressive Physician Associates, Inc. Retirement Savings Plan Progressive Physician Associates, Inc. $669,937 26 Jeffer Mangels Butler & Mitchell LLP Profit Sharing and 401(k) Plan Jeffer Mangels Butler & Mitchell LLP $663,531 27 QRM 401(k) Retirement Savings Plan Quantitative Risk Management, Inc. $662,045 28 Neuberger Berman Group 401(k) Plan Neuberger Berman Group LLC $661,047 29 MBIA Inc. Employees Pension Plan MBIA Inc. $658,502 30 Maher Terminals LLC Profit Sharing and 401(k) Plan Maher Terminals LLC $657,996 31 Willcox & Savage, P.C. Profit-Sharing Retirement Plan Willcox & Savage, P.C. $647,756 32 Morris, Nichols, Arsht & Tunnell LLP 401(k) Profit Sharing Plan Morris, Nichols, Arsht & Tunnell LLP $647,520 33 Eastman & Smith Ltd. Profit Sharing and Savings Plan and Trust Eastman & Smith Ltd. $643,627 34 APG Asset Management 401(k) Plan APG Asset Management $642,912 35 American Radiology Associates, P.A. Retirement Plan American Radiology Associates, P.A. $638,273 36 First Manhattan 401(k) Plan FMC Group Holdings LP $636,751 37 Downs Rachlin Martin Retirement Plan Downs Rachlin Martin PLLC $632,968 Across these 37 plans, the average account value stands close to $820,000, with a median around $754,000. That is a striking contrast to the national average, which remains under $120,000 for most retirement savers. The first major reason for this difference is compensation. These are high-income groups with the ability to contribute the annual maximum without hardship. Employers in these professional partnerships also tend to make hefty profit-sharing contributions. A doctor earning $400,000 a year or a law partner receiving a share of firm profits can easily reach contribution limits and still receive matching or profit-based additions on top. Over time, that combination of high base income and rich employer match drives account values far above what traditional salaried workers can achieve. The second reason is less about pay and more about time. Companies such as Texas Instruments and General Re demonstrate the quiet power of long-term consistency. Their plans have thousands of participants and more modest individual incomes, yet decades of continuous contributions and steady investment returns have compounded into substantial balances. The difference is discipline rather than income level. These two factors together explain why some retirement plans have reached the million-dollar mark while others lag far behind. High income and employer generosity create the initial lift. Long time horizons finish the job. In a period when many Americans are struggling to save even a fraction of what they will need, these plans are reminders that structure and time still matter more than luck. The quiet millionaires of 2024 did not chase returns or time markets. They simply contributed, matched, and waited long enough for patience to pay.

-

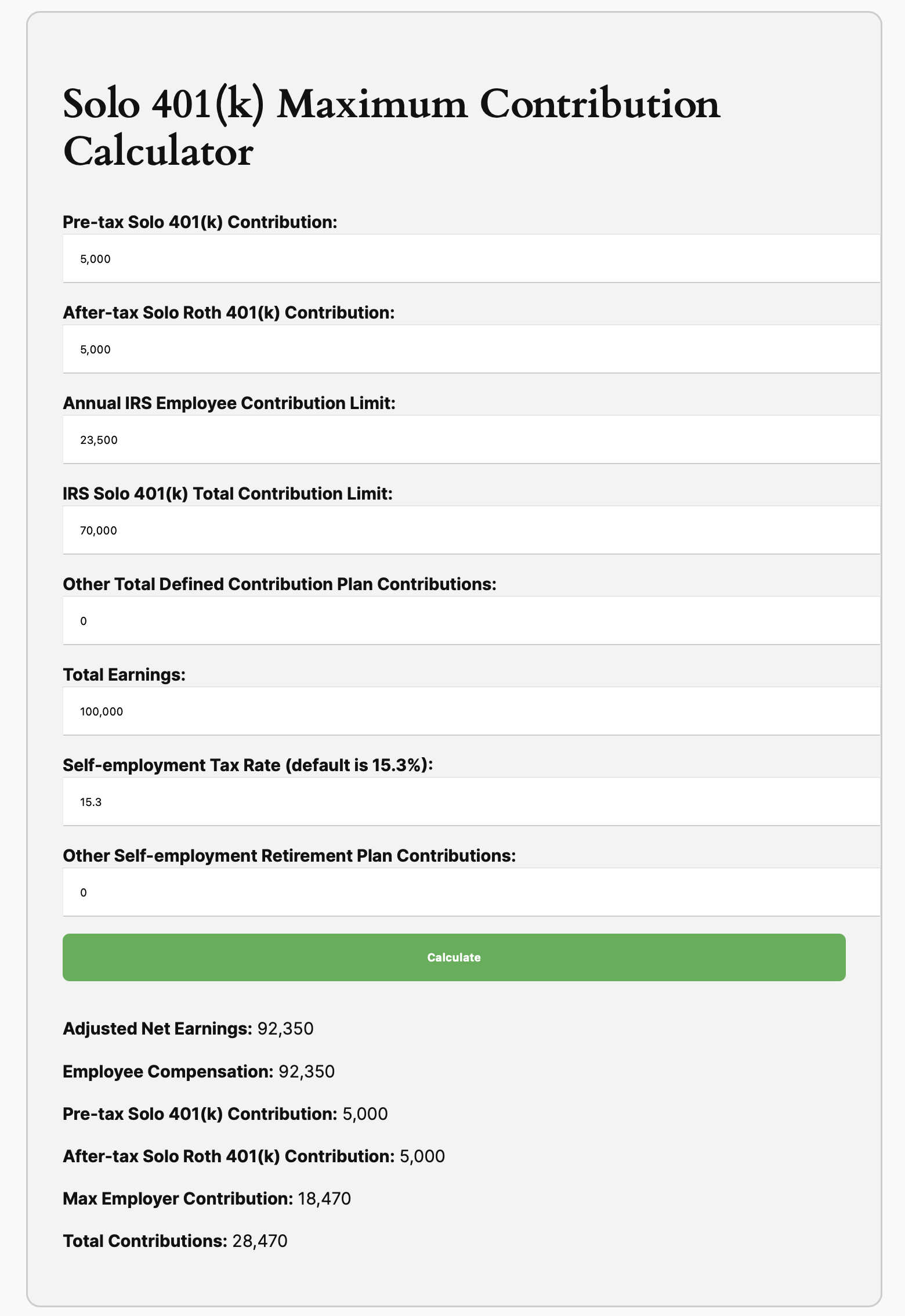

Last Quarter Checklist for 2025

- Latest in Retirement Savings & Personal Finance: All the Glittering Gold, Highest Household Credit Card Debt, More PE Funds Than McDonald’s

- Last Quarter Checklist for 2025

- Tools & Tips: Solo 401(k) Maximum Contribution Calculator

- Market Overview

-

Retirement Withdrawals in Optimal Order

In this issue:

- Latest in Retirement Savings & Personal Finance: Amazon Prime Day Record Sales, Inflation Rise Again? Underestimating Hobby and Pastime Costs

- Retirement Withdrawals in Optimal Order

- Tools & Tips: Retirement Withdrawal Optimal Calculator

- Market Overview

-

Retirement Milestone Cheat Sheet

In this issue:

- Latest in Retirement Savings & Personal Finance: OBBB Tax Changes, More Debt Among Millennials, Adult Children Living at Home

- Retirement Milestone Cheat Sheet

- Tools & Tips: Main ETFs You Can Use

- Market Overview

-

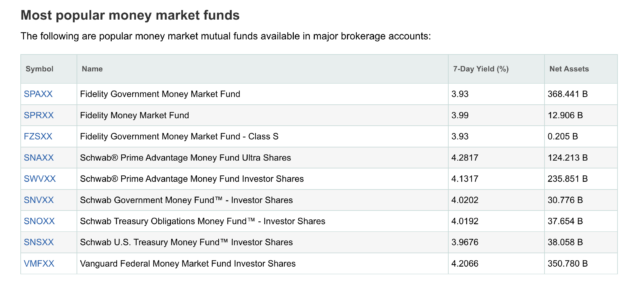

Savings Hacks

In this issue:

- Latest in Retirement Savings & Personal Finance: Crypto in 401(k), Private Investments in Target Date Funds, BNPL Credit Score Impact

- Savings Hacks Using BNPL & Others

- Tools & Tips: Money Market Fund Center

- Market Overview

-

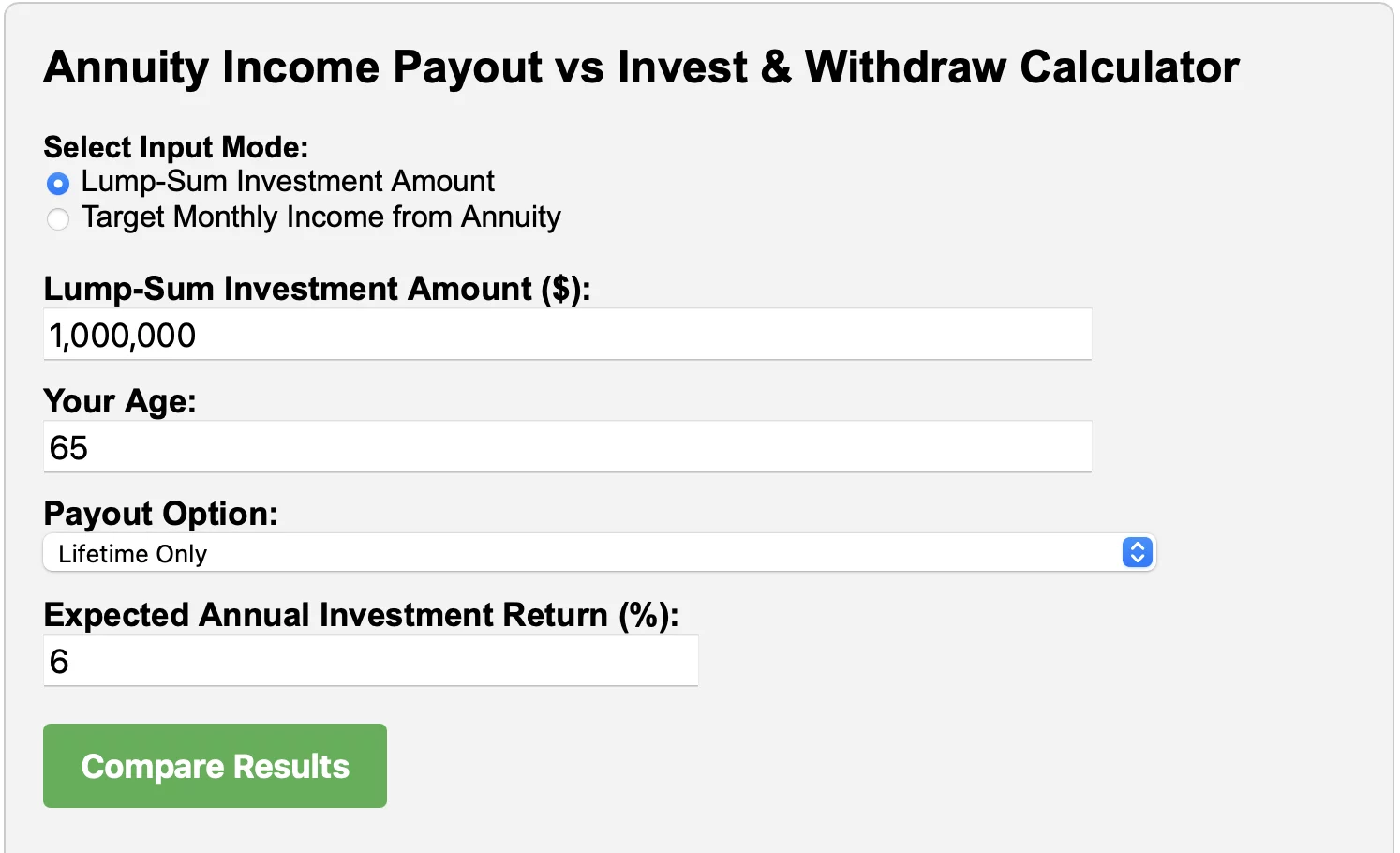

Annuity Income Payout vs. Invest & Withdraw

In this issue:

- Latest in Retirement Savings & Personal Finance: Annuity Is Back, HSA & Retirement Healthcare Improvement, Growing Medical Debt Crisis

- Tools & Tips: Annuity vs Invest Calculator

- Annuity Income Payout vs. Invest & Withdraw

- Market Overview

-

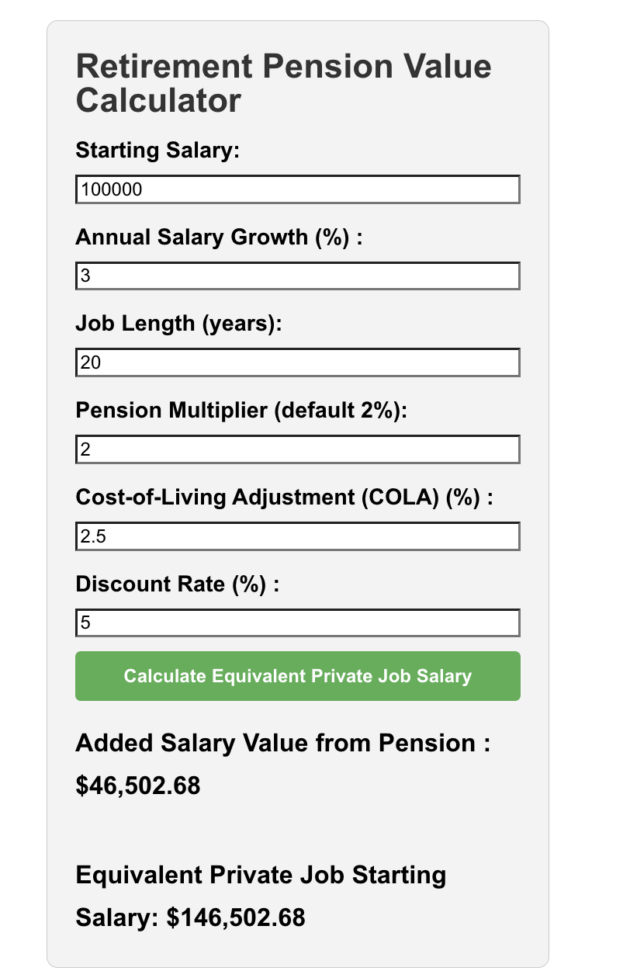

Public Pay Might Be Higher Than You Think (Once You Do the Math)

In this issue:

- Latest in Retirement Savings & Personal Finance: High 401(k) Savings Rate, The Big Beautiful Bill’s Deficit Increase & Who Are Affected by the BBB

- Public Pay Might Be Higher Than You Think (Once You Do the Math)

- Tools & Tips: Retirement Pension Value Calculator

- Market Overview

-

Retirement Plan Contribution Limits in 2024

2024 Retirement Plan Contribution Limits 1. 401(k), 403(b), and 457(b) Plans Employee Contributions: Up to $23,000 (under age 50) Catch-up contribution: $7,500 (ages 50+) Total Combined Limit (Employee + Employer): $69,000 Roth Options: Available for 401(k), sometimes for 403(b) and 457(b) Plan Details: 401(k): Primarily for for-profit companies; includes Roth (after-tax) options. 403(b): For public schools and nonprofits; Roth-style options less common. 457(b): For state/local government and some tax-exempt organizations; Roth availability varies. 2. Solo 401(k) and SEP IRA Solo 401(k): For self-employed individuals/business owners without employees.

- Employee contributions: $23,000, plus $7,500 catch-up (ages 50+)

- Employer contributions: up to 25% of compensation

- Total combined limit: $69,000 or 25% of compensation, whichever is less

SEP IRA: Employer contributes up to 25% of compensation, up to $69,000. No catch-up contribution. 3. SIMPLE IRA

- Employee contribution: up to $16,500

- Catch-up contribution: $3,500 (50+)

- Employer must match dollar-for-dollar up to 3% of employee salary

- Immediate vesting

4. Traditional and Roth IRAs

- Annual contribution: $7,000

- Catch-up: additional $1,000 (50+)

Traditional IRA: Pre-tax contributions, taxable upon withdrawal Roth IRA: After-tax contributions, tax-free withdrawals 5. Thrift Savings Plan (TSP)

- Federal and uniformed services employees only

- Employee contributions: up to $23,000 (under age 50), plus catch-ups ($7,500 at 50+)

- Employer matches up to 5% of salary

- Total Combined Limit (Employee + Employer): $69,000

- Pre-tax (traditional) and Roth contributions allowed

6. Payroll Deduction IRA

- Annual limit: $7,000; catch-up of $1,000 (age 50+)

- Pre-tax or Roth contributions

- No employer matching

7. Health Savings Account (HSA)

- Individual coverage: $4,150

- Family coverage: $8,300

- Catch-up contribution: additional $1,000 for age 55+

- Must have a high-deductible health plan

- Tax-free growth; penalty-free medical withdrawals; penalty-free non-medical withdrawals after age 65 (taxable)

8. Self-Directed IRA (SDIRA)

- Contribution limits same as IRAs ($7,000 + $1,000 catch-up age 50+)

- Allows alternative investments (real estate, precious metals, crypto)

- Requires IRS-approved custodian

9. Nondeductible IRA

- Same limits as traditional IRAs ($7,000 + $1,000 catch-up age 50+)

- Contributions not tax-deductible; earnings taxable at withdrawal

10. Annuities and Pension Plans (Brief Overview)

- Annuities: Insurance-based retirement products, providing guaranteed income. High fees, limited liquidity.

- Pension Plans: Employer-funded defined-benefit plans providing guaranteed lifetime income. Limited investment control.

11. Flexible Spending Account (FSA) Limits for 2024

- The maximum employee contribution to a health care FSA for 2024 is $3,200.

- If the FSA plan allows for carryover, the maximum amount that can be carried over to 2025 is $640.

- For Dependent Care FSAs, the maximum remains $5,000 per household (single or married filing jointly) or $2,500 if married and filing separately.

12. Health Savings Account (HSA) Limits for 2024 Coverage Type 2024 Contribution Limit Catch-Up (Age 55+) Minimum Deductible Out-of-Pocket Max Self-only $4,150 +$1,000 $1,600 $8,050 Family $8,300 +$1,000 (per eligible spouse, each in own HSA) $3,200 $16,100

- Individuals age 55 or older can contribute an additional $1,000 as a catch-up contribution.

- HSA contributions can be made until the tax filing deadline (April 15, 2025, for tax year 2024).

- To be eligible for HSA contributions, you must be enrolled in a high-deductible health plan (HDHP) meeting the minimum deductible and out-of-pocket maximum requirements above.

-

Simple 401(k) Investment Guide

In this issue:

- Latest in Retirement Savings & Personal Finance: College Education Affordability Declined, Rising Debt Puts Your 401(k) Retirement Savings in a Pickle

- Simple 401(k) Investment Guide

- Tools & Tips: 401(k) Investment Assistant

- Market Overview

-

Income Growth, Historical 401(k) Contribution Limit Data

In this issue:

- Latest in Retirement Savings & Personal Finance: Interest Rates Rise Again, Rising Home Insurance Cost, …

- Historical Income Growth, 401(k) Contribution Limit Growth

- Tools & Tips: 401(k) Maximum Match Calculator — Marvell Semiconductor

- Market Overview

-

Historical Year-by-Year Annual 401(k) Contribution Limits

Year-by-Year Annual 401(k) Contribution Limits since 1978. Also we include CPI inflation increase as a reference

-

Realistic Reference Data on Retirement Savings by Age in 2025

A realistic accumulated savings figures by age in 2025 for various income level people.