![]()

Useful Tips for 401(k)s, IRAs, and RMDs in the New Year

In this issue:

-

- Latest in Retirement Savings & Personal Finance

- Useful Tips for 401(k)s, IRAs, and RMDs in the New Year

- Tools & Tips: Roth IRA Compounding

- Market Overview

Latest in Retirement Savings & Personal Finance

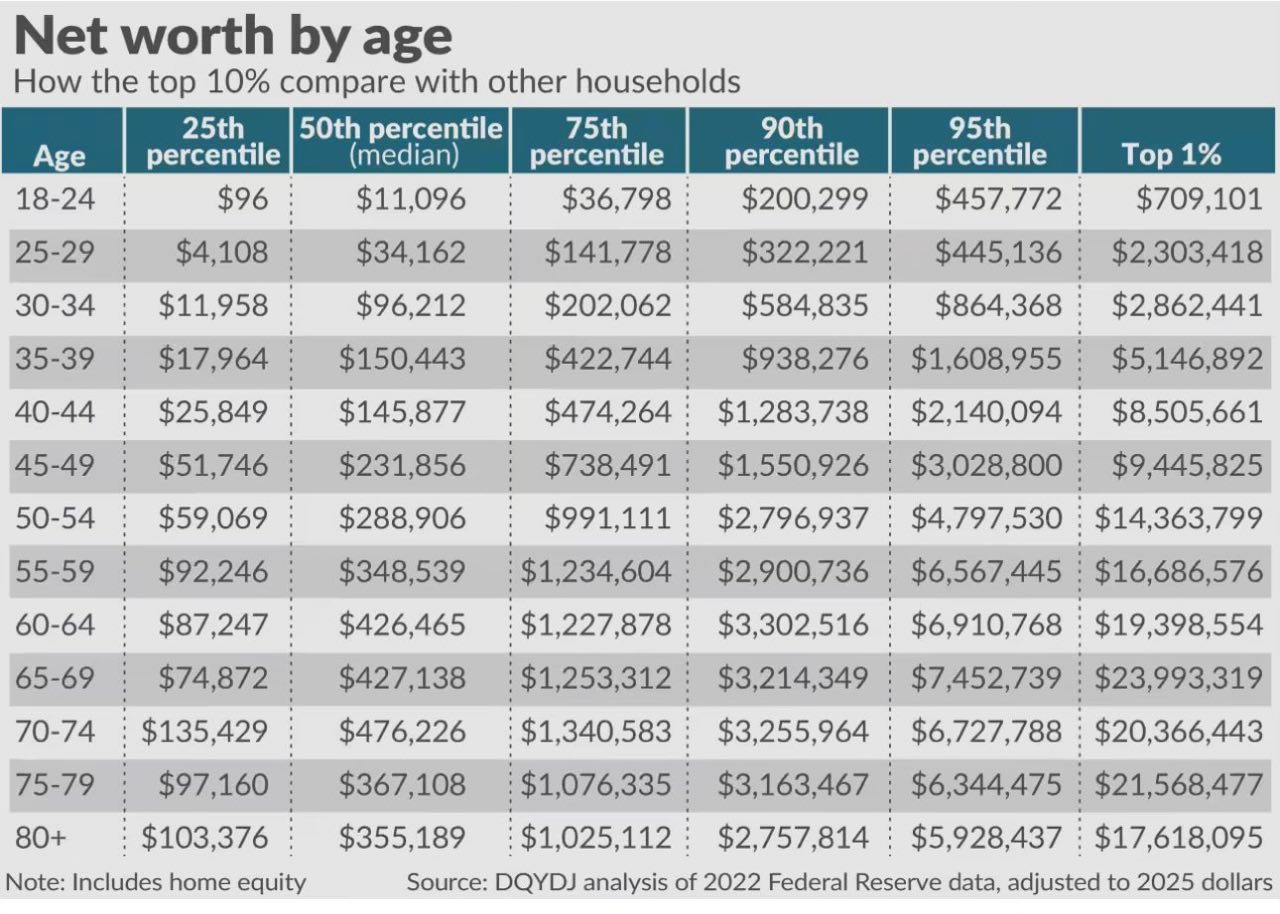

Net Worth by Age: How Small Saving Gaps Quietly Change Your Outcome

The above table is not here to impress you or discourage you. It is simply a mirror. What matters is not that one group compounds faster than another, but how small differences add up over time. Look at ages 30 to 34. The median net worth is about $96,000, while the 75th percentile is roughly $202,000. That gap is not some extreme lifestyle difference. It is usually just saving a bit more, or starting a bit earlier. Fast forward to ages 55 to 59. The median is around $349,000, while the 75th percentile sits near $1.23 million. The ratio is not wildly different, but the dollar gap has grown large simply because time has done its work.

Now put some numbers behind it. Suppose someone saves an extra $7,500 a year starting in their early 30s and invests it steadily. At a conservative 6 to 7 percent return, that alone compounds into roughly $600,000 to $700,000 over 30 years. On this table, that difference by itself is often enough to lift a household from around the median into the 75th percentile range by their late 50s or early 60s, assuming everything else is average. That shift does not require perfect timing or heroic returns. It just requires consistency and patience.

This is the real message of the chart. You do not need to be in the top 1 percent to change your trajectory meaningfully. Saving a little more, earlier, and letting compounding work quietly can move you into a very different percentile over time. The math is not dramatic, but the outcome is. The question for the reader is not where you are today, but whether you are feeding compounding enough to let it do its job.

Trump Administration’s Big Stimulus Push and the Near Term Growth Question

The list below reads like a full throttle attempt to force economic momentum into a midterm election year. President Donald Trump has now put forward or supported the following actions, all aimed at lowering costs, boosting spending power, and supporting asset prices, at least in the short run.

- Called for a 10 percent cap on credit card interest rates

- Banned institutional purchases of single family homes

- Authorized the purchase of $200 billion of mortgage bonds to push mortgage rates lower (as what we discussed in our previous newsletter)

- Publicly called for the Fed to cut interest rates to 1 percent in 2026

- Made $2.00 per gallon gas prices a top economic priority

- Announced $2,000 tariff related stimulus checks

Whether these moves are good for the long term is debatable, and probably will be debated loudly. Price controls, rate pressure on the Fed, and direct stimulus all come with second order effects that do not show up immediately. But in the short term, it is not hard to see why many expect a meaningful push to growth, confidence, and spending. Cheaper credit, lower energy prices, direct checks, and policy headlines alone can move behavior. With midterms approaching, the setup feels aggressive and potentially very stimulative in the near window, even if the longer term bill arrives later.

Meanwhile, we see the prices of Gold, Silver, and other precious metals are going through the roof!

Useful Tips for 401(k)s, IRAs, and RMDs in the New Year

In Ultimate 2026 Retirement Playbook for 401(k)s & IRAs, we give some timely, useful info on maximizing company match, handling RMDs across accounts, and smart IRA tactics like backdoor Roth for the new year. Here are the gist of it:

1. Max Your Company Match

Golden Rule: Contribute enough each paycheck to get 100% of the employer match (often 50-100% on first 3-6% of salary). This is free money with instant 50-100% return.

Most plans match per paycheck. Front-loading and hitting the cap early means missing matches on later paychecks if there is no so-called True-up provision, which is often not provided by most companies. So spread out your deferrals evenly across all pay periods.

Don’t miss the true Free lunch!

2. RMDs (Required Minimum Distributions) with Multiple Accounts

RMD age: 73 (born 1951-1959) or 75 (born 1960+). Withdraw from tax-deferred accounts or face penalties.

- Multiple 401(k)s: Separate RMD from each plan using its own Dec 31 prior-year balance.

- Multiple IRAs (Traditional, SEP, SIMPLE): Calculate each, but aggregate total and withdraw from one or more IRAs.

- Roth IRAs: No RMDs during your lifetime (

Roth 401(k)s have RMDs unless rolled to Roth IRA,this is no longer true after Secure Act 2.0).

3. IRA Moves

Traditional IRAs: No income limit to contribute. Deductibility depends on income and workplace plan.

Roth IRAs: Income phase-outs apply (single full under ~$153K MAGI, joint under ~$242K).

Tax Bracket Rule of Thumb:

- Low bracket (10-12%): Favor Roth. Bite the tax bullet.

- High bracket (32-37%): Favor Traditional. Defer tax.

- Middle (22-24%): Split for diversification. Balanced act.

Spousal IRAs: Non-working spouse contributes based on working spouse’s income.

Backdoor Roth (for high earners, you can’t directly contribute to Roth IRA so pursue this backdoor Roth Conversion route): Contribute non-deductible to Traditional IRA, immediately convert quickly to Roth, file Form 8606. But watch out Pro-Rata pitfall.

Pro-Rata Pitfall: Pre-tax money in any Traditional/SEP/SIMPLE IRA makes conversion partially taxable. Fix by rolling pre-tax IRAs to a 401(k) first. If you don’t have a 401(k), just establish solo 401(k) and roll your traditional IRAs to it, assuming you have earned income as a self-employed.

Mega backdoor Roth (after-tax 401(k) to Roth) possible if plan allows. Check your plan SPD.

Another year passed, a little gain here, a little loss there. Most of us want the same thing, save more, invest better, stop the leaks. So keep it simple and do the basics that actually move the needle.

|

Tools & Tips: Roth IRA Compounding

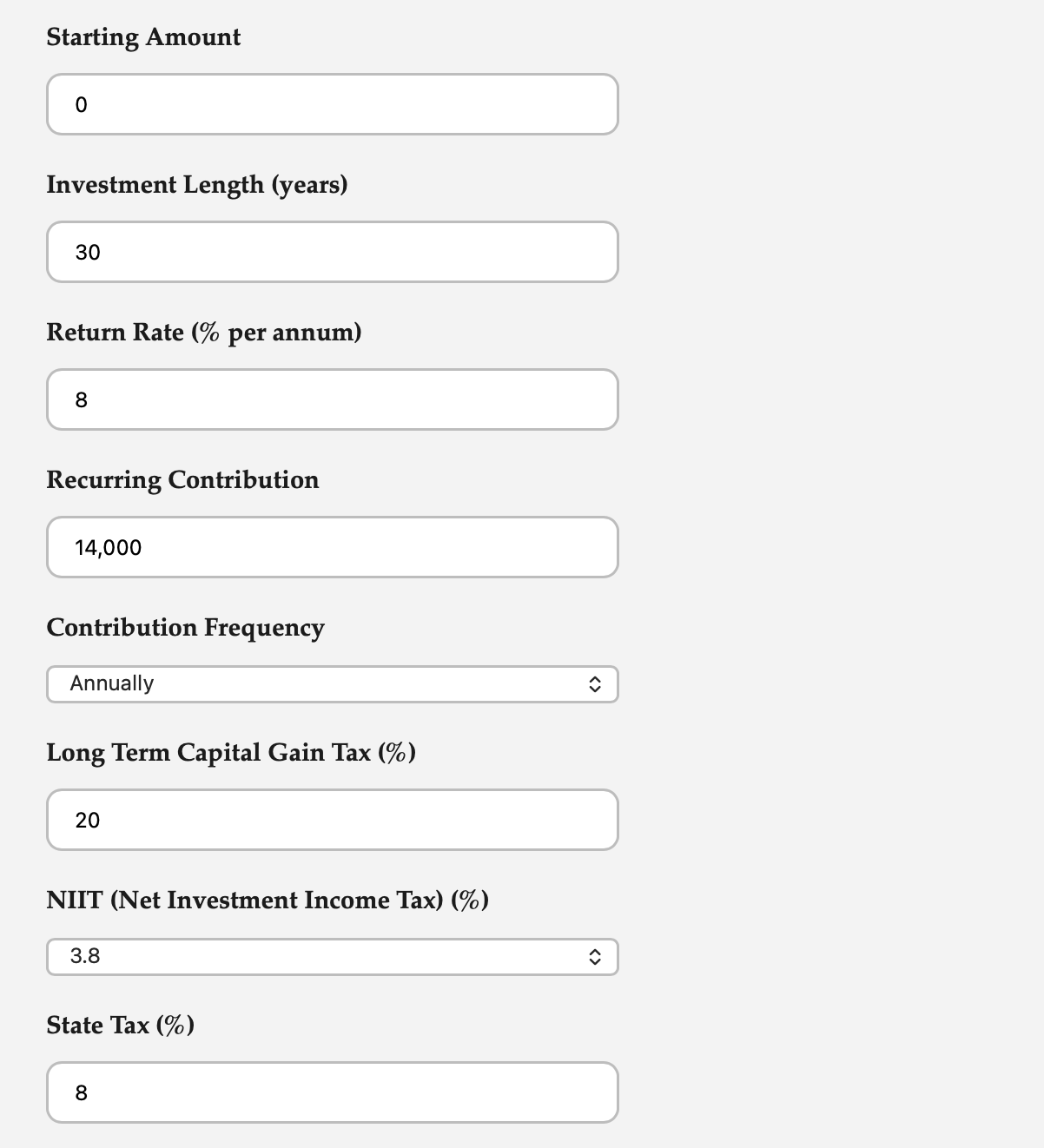

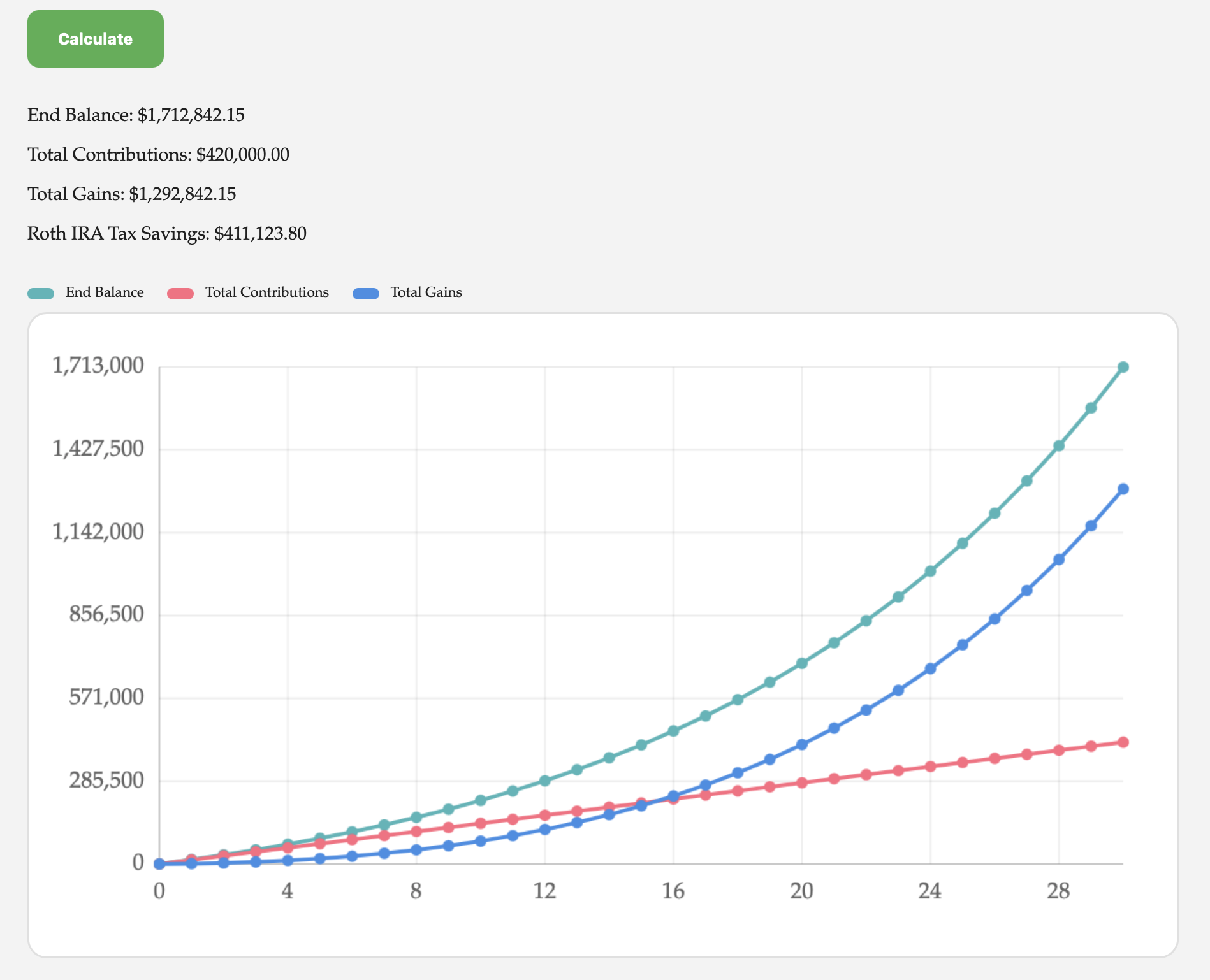

Well, it seems many people don’t treat the annual $7,000 Roth IRA contribution serious. Big mistake. Using Investment Return Calculator, in the following, assuming hushand and wife each contributes $7,000 annually for 30 years (say, 30 year old to 60 year old), you get the following:

Inputs: assuming 8% annual investment return.

Outputs:

The big tax savings for the Roth IRA is something you shouldn’t ignore. You can be a multi-millionaire by simply maxing out the annual Roth IRA contribution. For those who have more questions, refer to this article for more details.

Market Overview

Markets surged last week. With the strong indications and actions by the Administration to prop up the economic growth (see the above), investors simply ignore the geopolitical events such as the U.S. action in Venezuela.

The following table shows the major asset price returns and their trend scores, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 1.1% | 2.4% | 5.1% | 11.9% | 20.9% | 8.3% |

| Foreign Stocks | 1.6% | 5.4% | 9.0% | 16.3% | 39.9% | 14.4% |

| US REITs | 1.0% | 0.7% | 1.9% | 1.0% | 7.4% | 2.4% |

| Emerging Market Stocks | 2.0% | 6.3% | 5.8% | 15.9% | 35.5% | 13.1% |

| Bonds | -0.1% | 0.1% | 0.1% | 3.6% | 7.9% | 2.3% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

|