-

Beware of The Parabolic Stock Market Rise

Stock market melt-up risks, Social Security cap proposal, harder job market.

-

Savings for Your Kids’ Lifetime Education

- Latest in Retirement Savings & Personal Finance

- Lifetime Education Cost Planner

- Market Overview

-

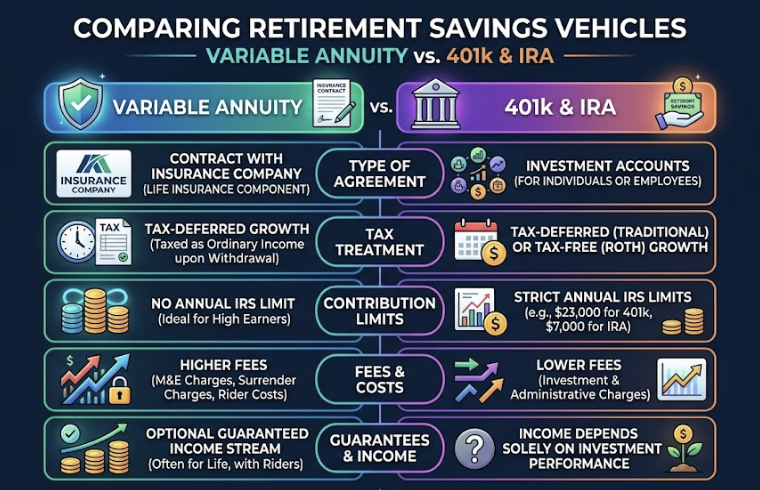

Variable Annuity vs. 401K vs IRA

- Latest in Retirement Savings & Personal Finance

- Variable Annuity vs. 401K vs IRA

- Market Overview

-

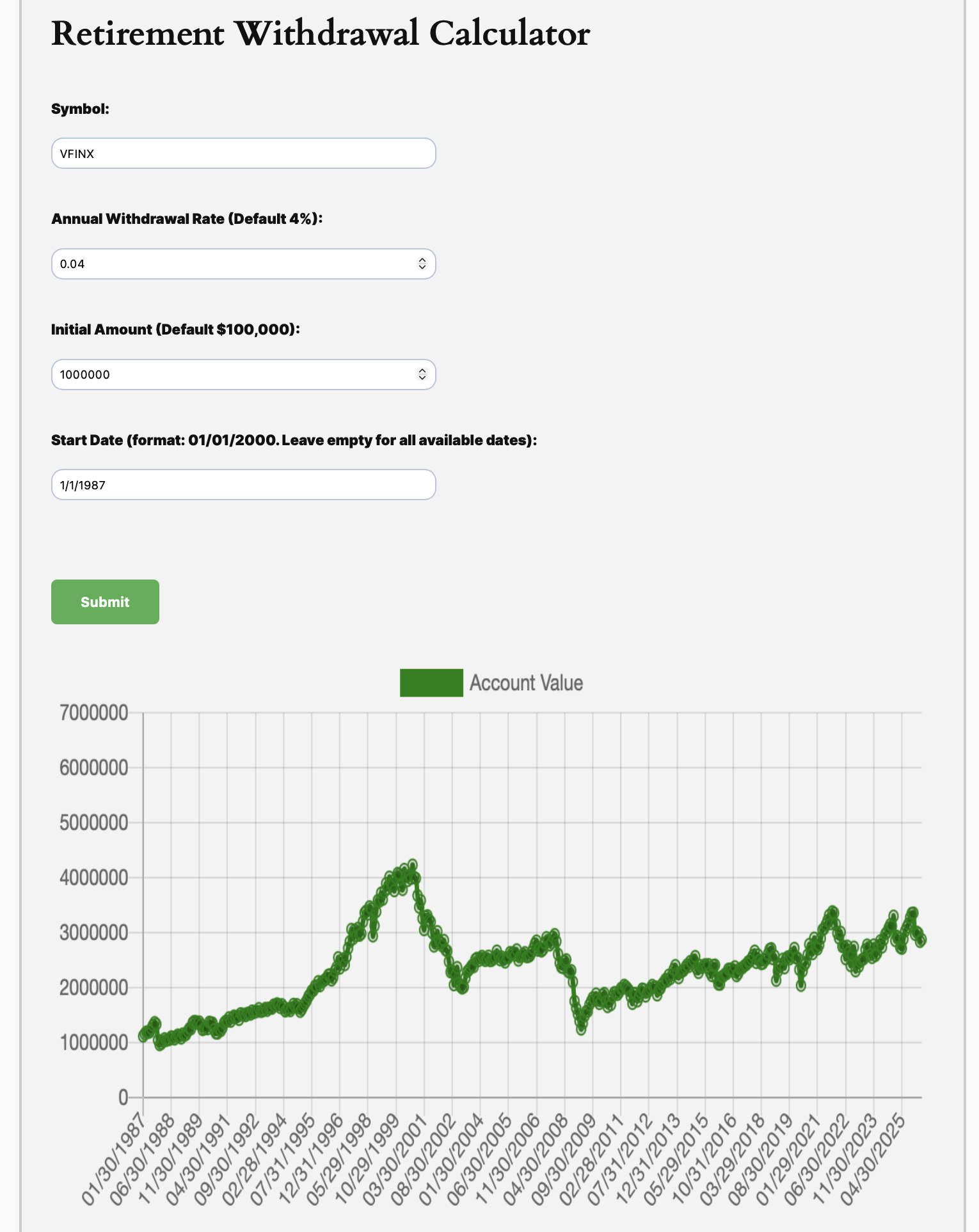

ETFs Can Match Lowest Cost Funds in 401(k) Plans

- Latest in Retirement Savings & Personal Finance

- ETFs Can Match Lowest Cost Funds in 401(k) Plans

- Retirement Withdrawal Calculator

- Market Overview

-

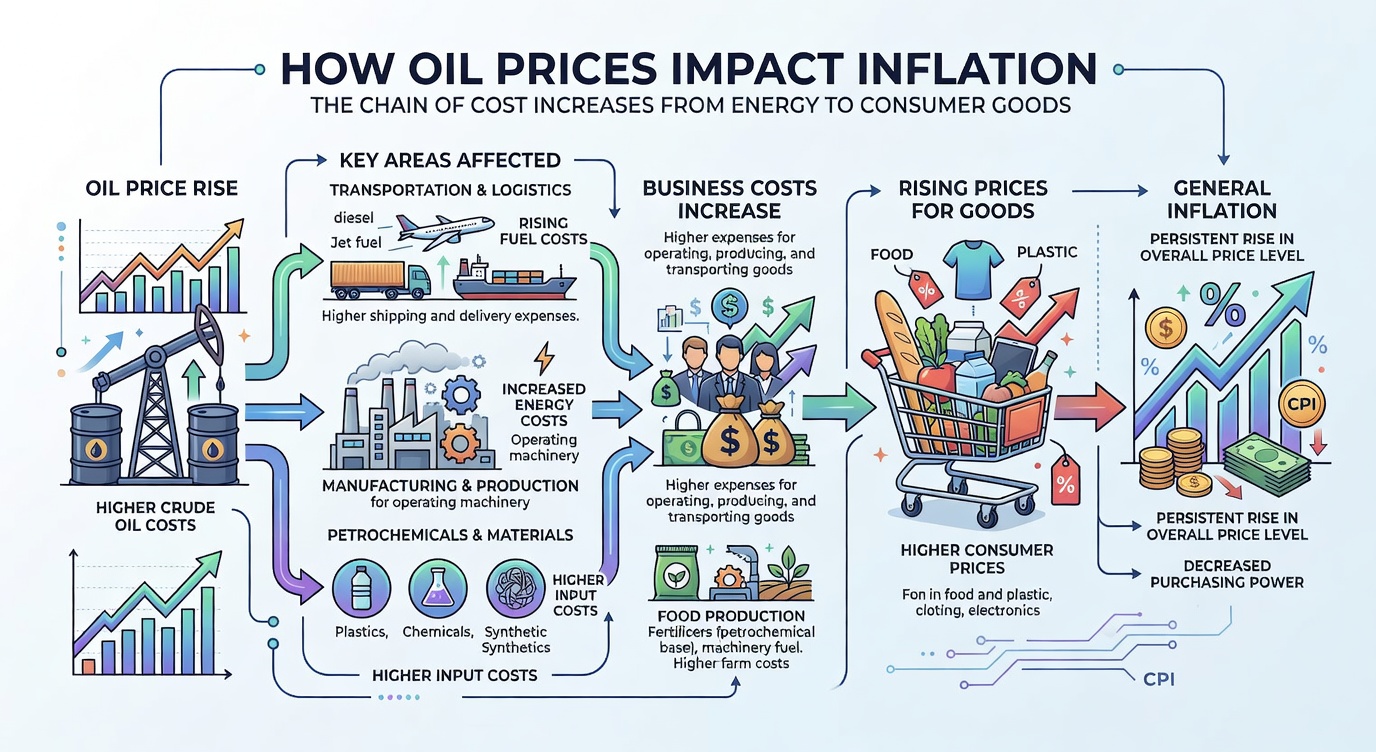

Wars and Investments

- Latest in Retirement Savings & Personal Finance

- Wars and Investments

- Oil Price and Inflation Infographic

- Market Overview

-

Special Report: Iran War, Oil Price & Your Investments

- Special Report: Iran War, Oil Price & Your Investments

- Tools & Tips: Asset Location Calculator

- Market Overview

-

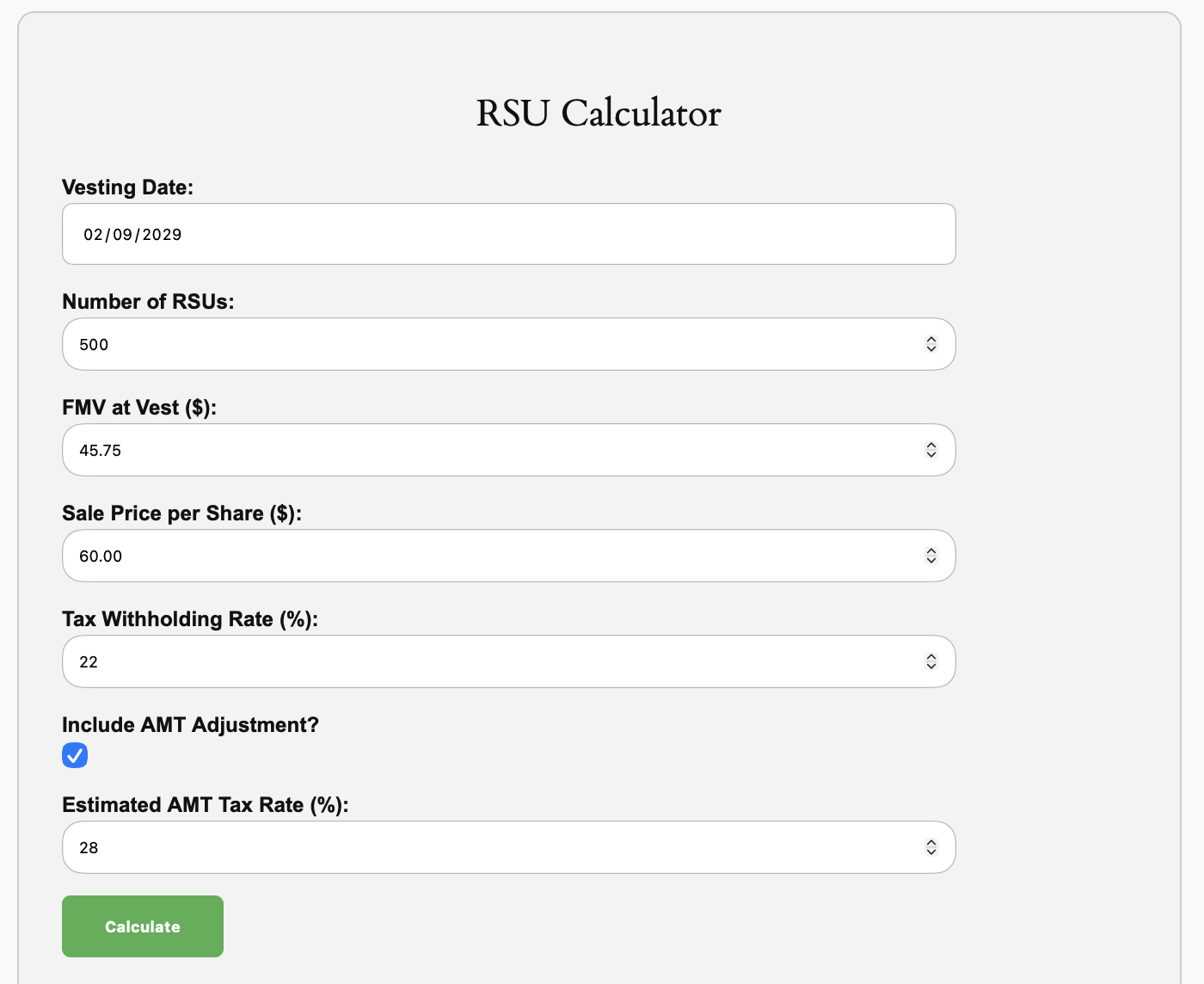

IRS Is Giving Out Money

- Latest in Retirement Savings & Personal Finance

- IRS Is Giving Out Money

- Tools & Tips: RSU (Restricted Stock Unit) Calculator

- Market Overview

-

The Federal Reserve Bank and Your Money

- Latest in Retirement Savings & Personal Finance

- The Federal Reserve Bank and Your Money

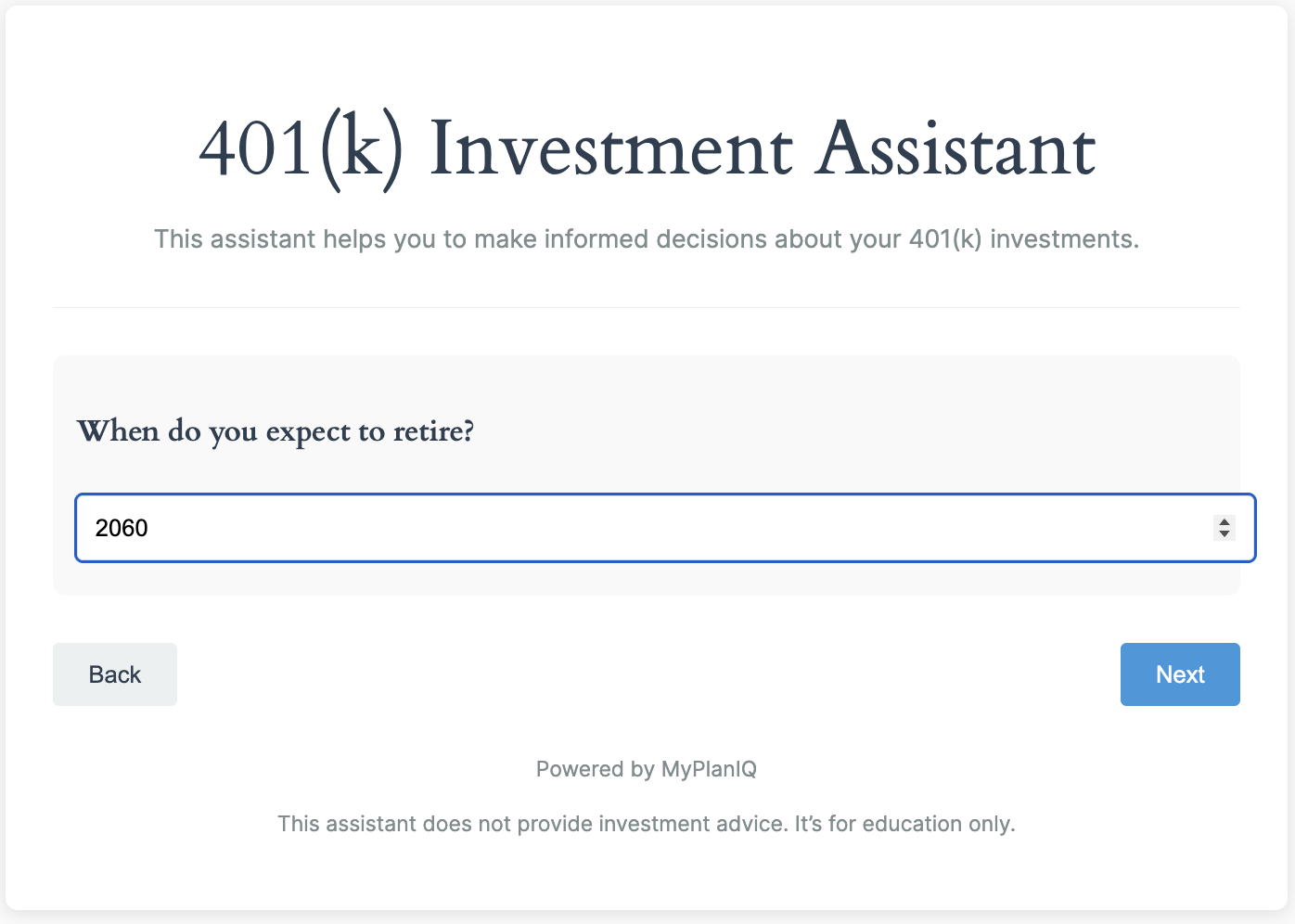

- Tools & Tips: 401(k) Investment Assistant

- Market Overview

-

2026 Tax Season Begins Today

- Latest in Retirement Savings & Personal Finance

- 2026 Tax Season Begins Today

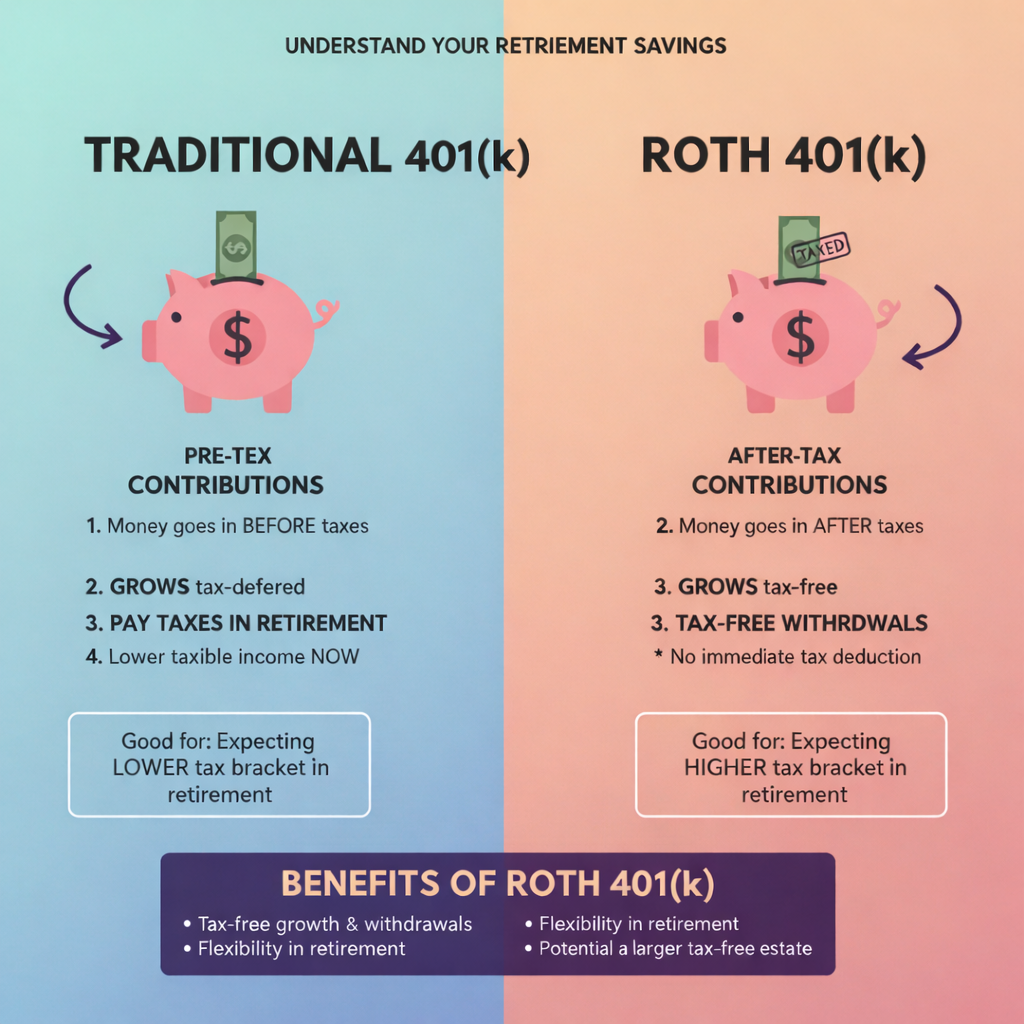

- Tools & Tips: Traditional 401(K) vs. Roth 401(K)

- Market Overview

-

Useful Tips for 401(k)s, IRAs, and RMDs in the New Year

- Latest in Retirement Savings & Personal Finance

- Useful Tips for 401(k)s, IRAs, and RMDs in the New Year

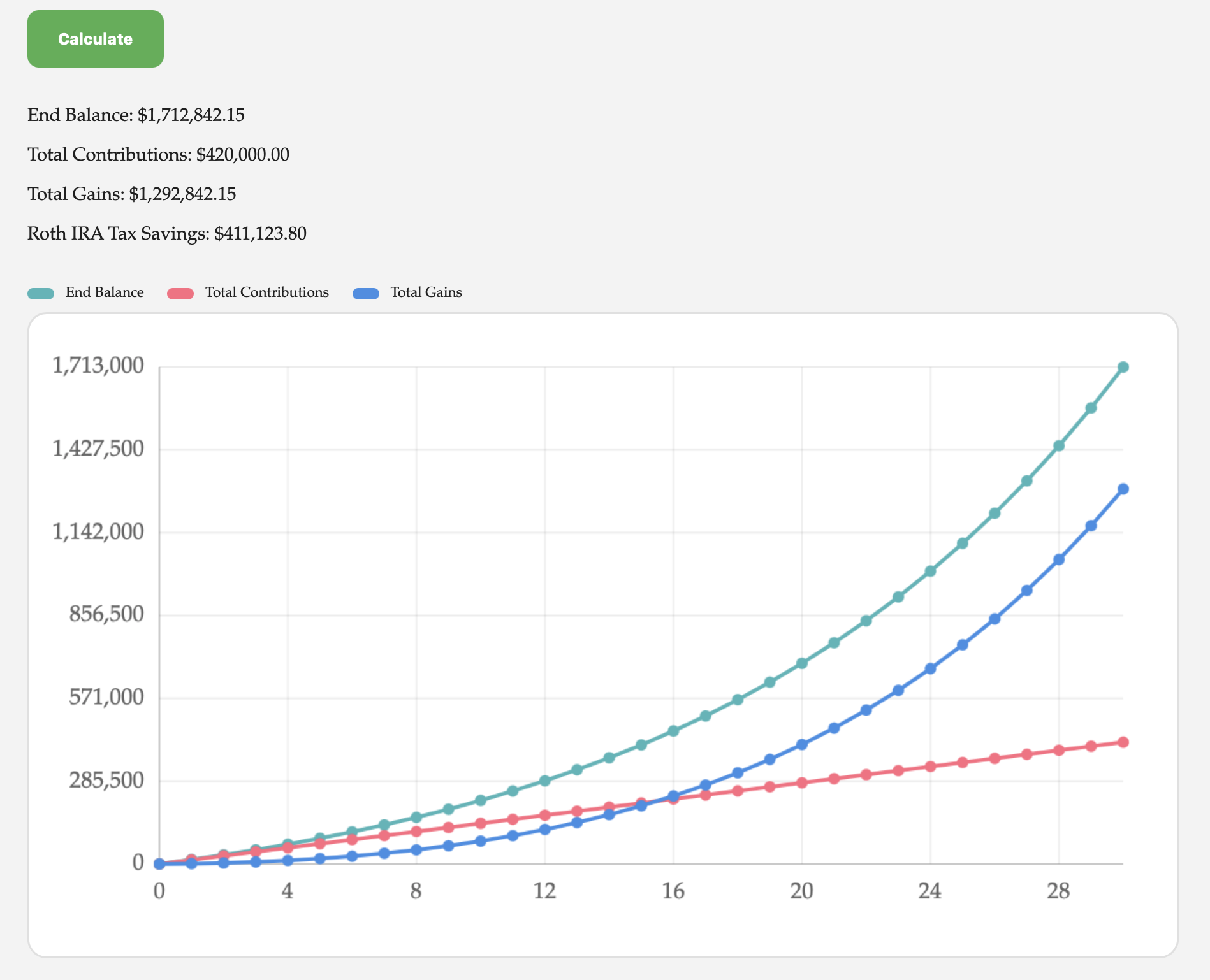

- Tools & Tips: Roth IRA Compounding

- Market Overview

-

New Year Resolutions for Your Personal Finance

- Latest in Retirement Savings & Personal Finance

- New Year Resolutions for Your Personal Finance

- MyPlanIQ 2026 Market Outlook

-

2025 Crystal Ball Market Prediction Scorecard

- Latest in Retirement Savings & Personal Finance

- Stock Market Bubble & Retirement Savings

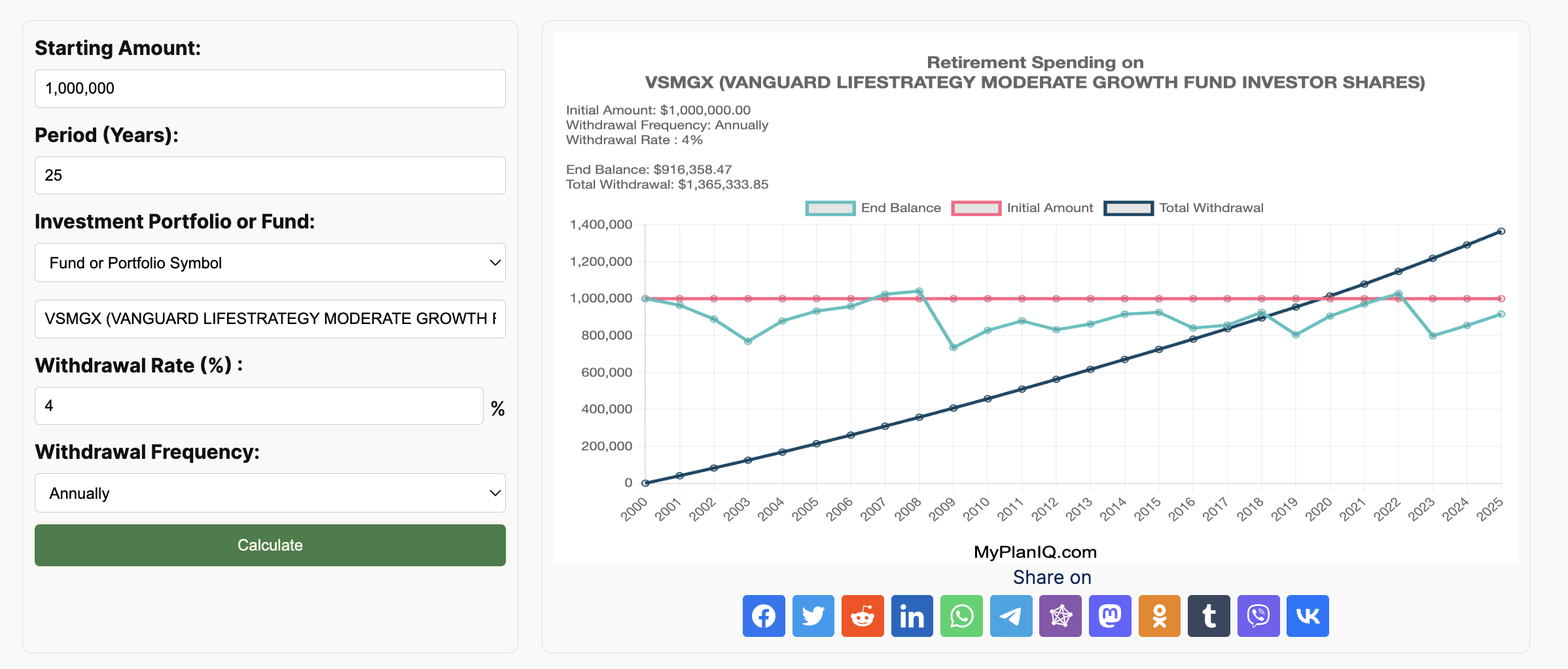

- Tools & Tips: Retirement Spending Calculator

- Market Overview

-

Stock Market Bubble & Retirement Savings

- Latest in Retirement Savings & Personal Finance

- Stock Market Bubble & Retirement Savings

- Tools & Tips: Retirement Spending Calculator

- Market Overview

-

Retirement Savings To Help Student Loan Payments

- Latest in Retirement Savings & Personal Finance

- Retirement Savings To Help Student Loan Payments

- Tools & Tips: I-Bond Comparison Calculator

- Market Overview

-

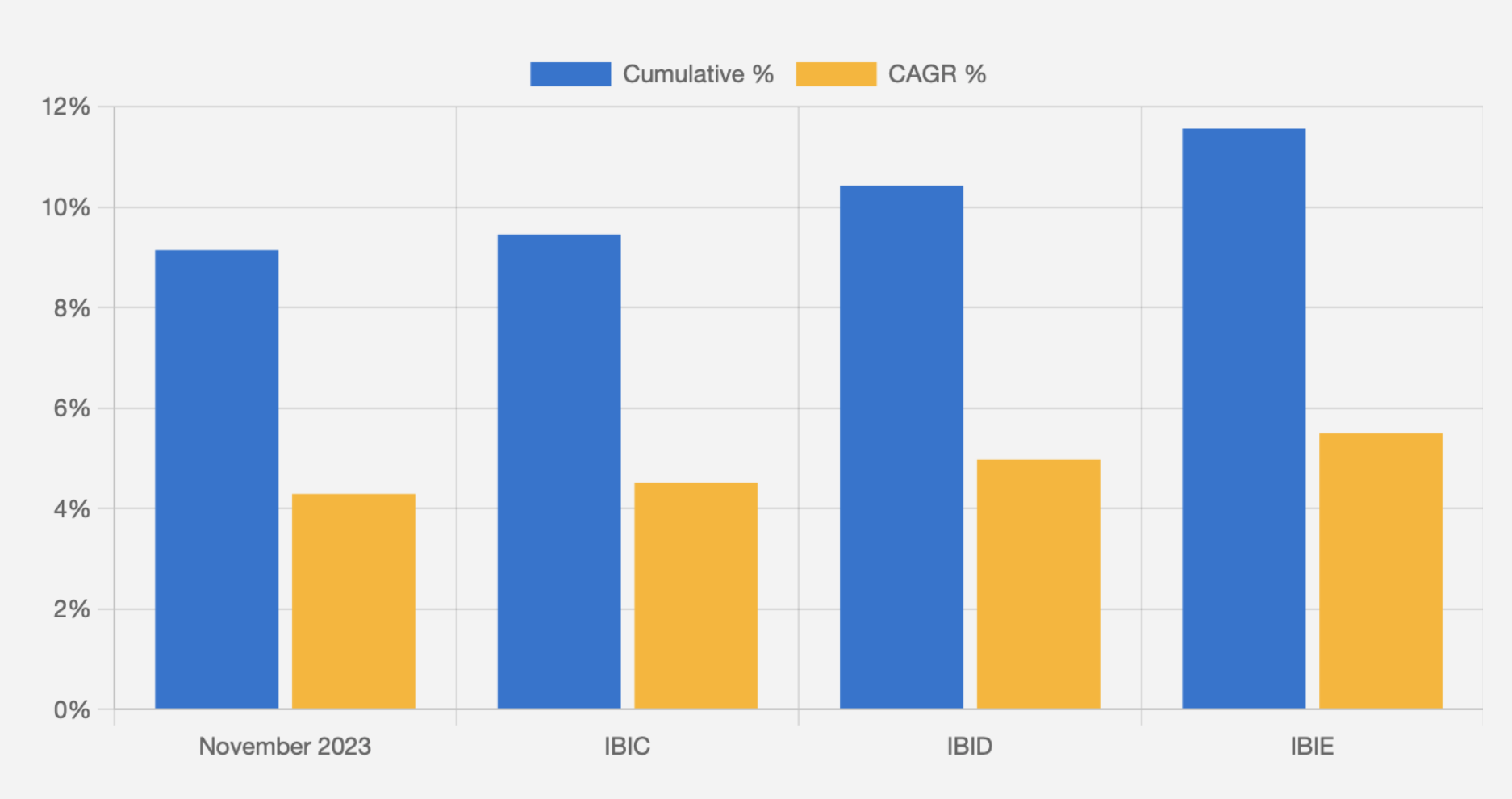

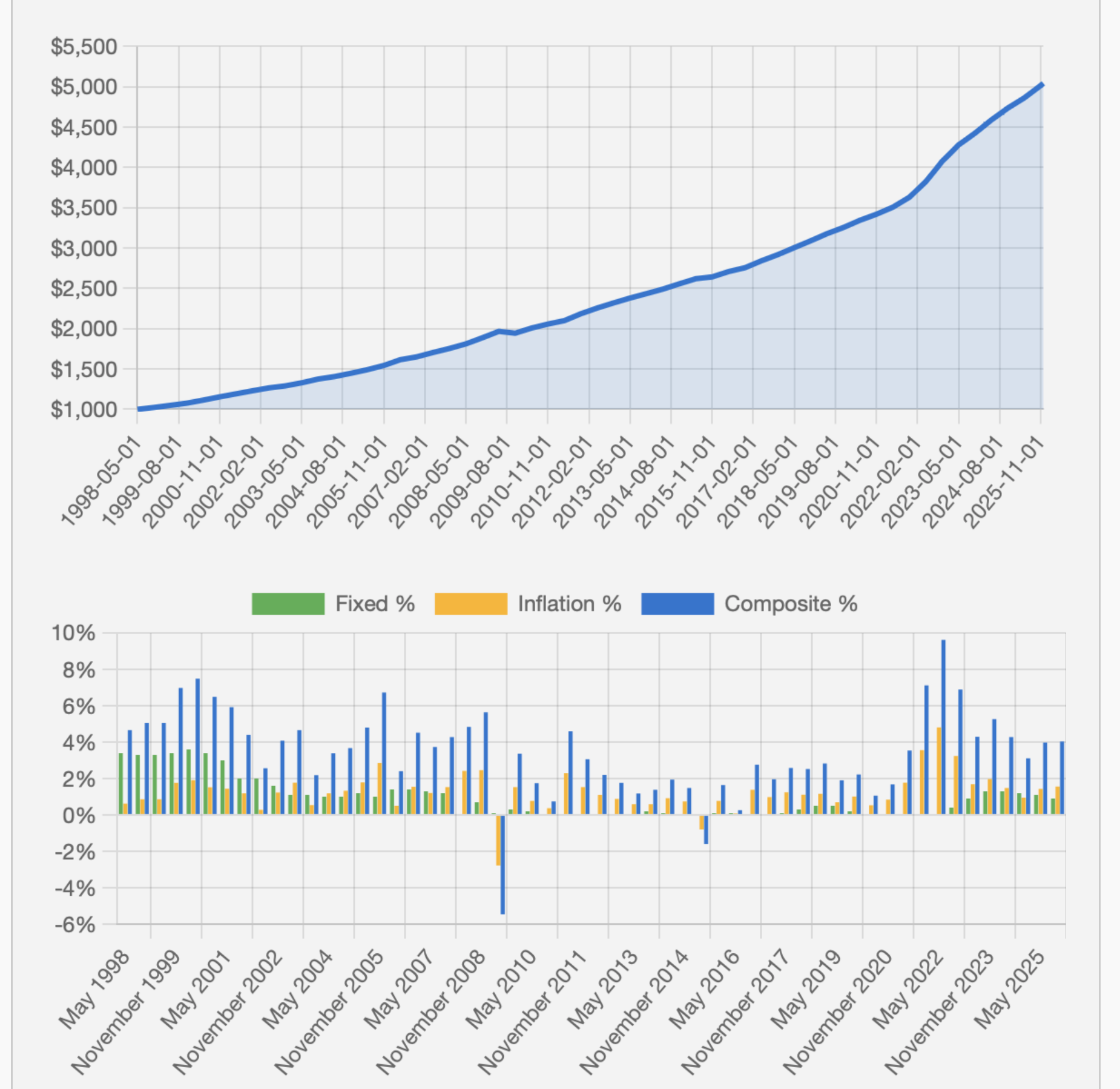

Series I Savings Bonds: Good Time to Buy?

- Latest in Retirement Savings & Personal Finance

- Series I Savings Bonds: Good Time to Buy?

- Tools & Tips: I-Bond Calculator

- Market Overview

-

Series I Savings Bonds: A Decent Shelter Against Inflation (If You Understand the Fine Print)

Is it worth to buy Series I Savings Bonds (I Bonds)? This article discusses what I Bond is and how it’s compared with money market and Inflation-Protected Securities (TIPs).

-

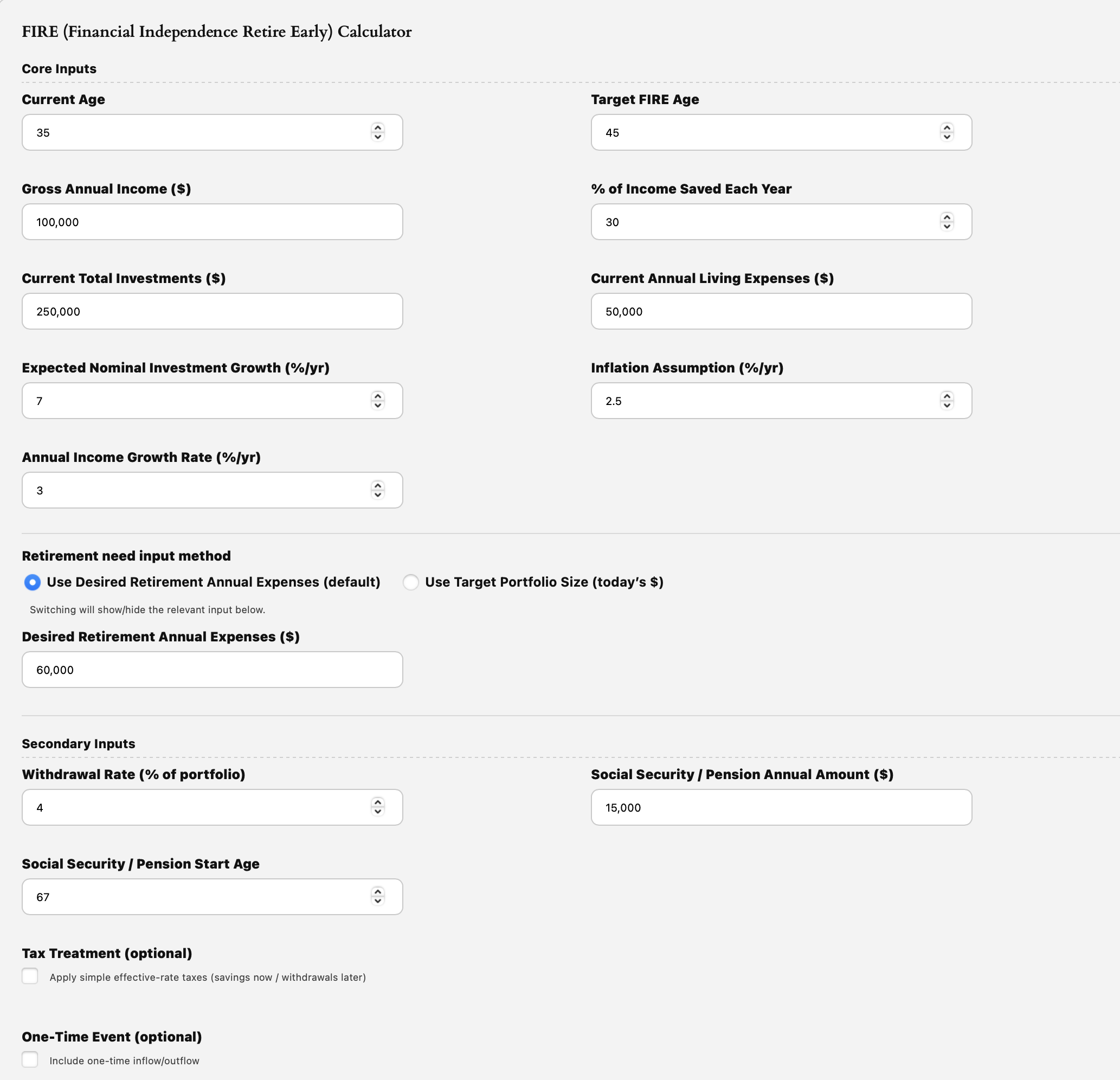

Good Time to FIRE (Financial Independence Retire Early)?

- Latest in Retirement Savings & Personal Finance: Fed to Cut Rate, AI Big Spend, Oracle of Oracle

- Good Time to FIRE (Financial Independence Retire Early)?

- Tools & Tips: FIRE (Financial Independence Retire Early) Calculator

- Market Overview

-

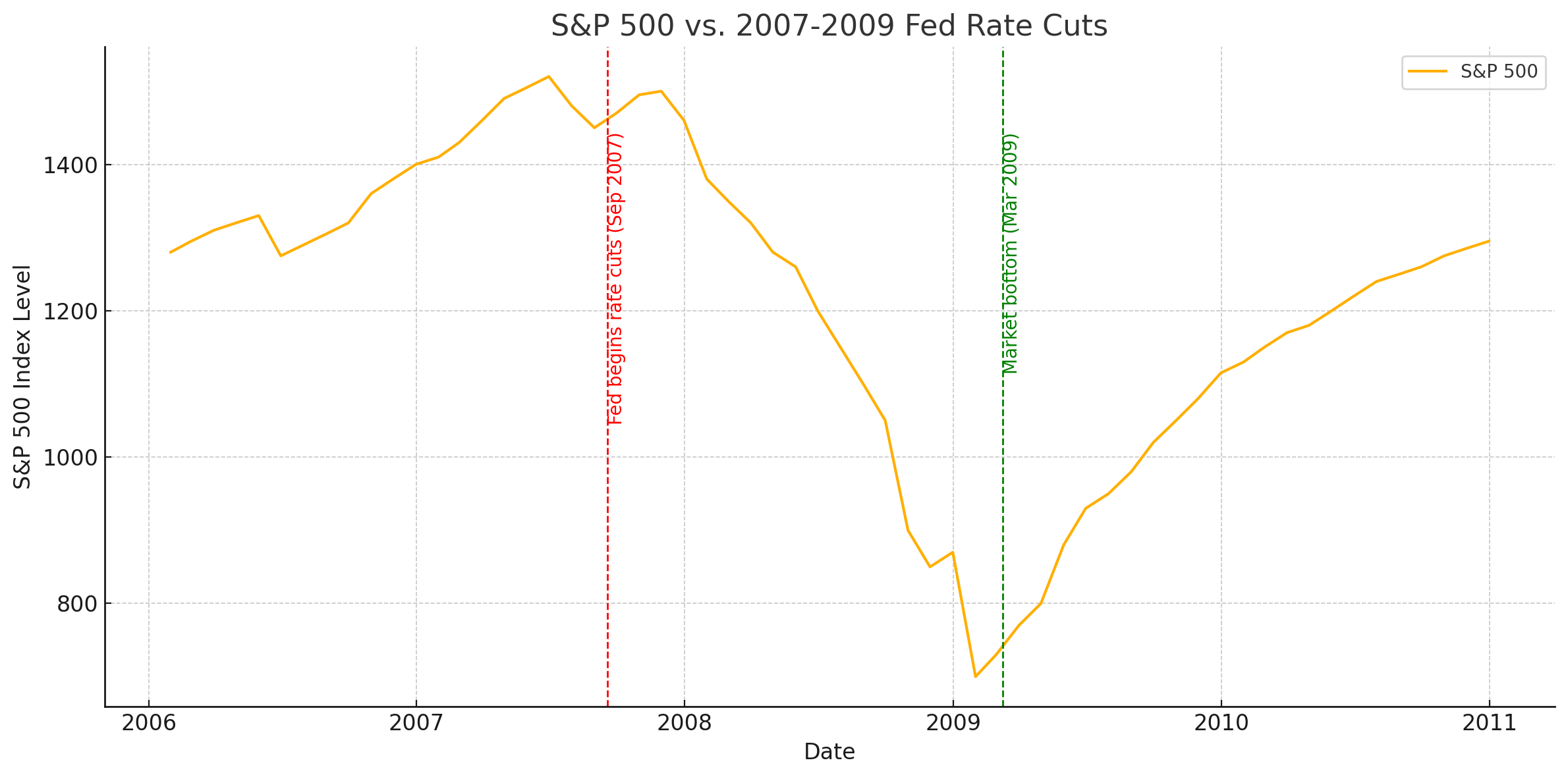

When the Fed Cuts Rates, What Really Happens to Stocks?

- Latest in Retirement Savings & Personal Finance: Job Growth Slowed, Gen Z Dipped into Retirement Savings, Best S&P 500 Earnings in Four Years

- When the Fed Cuts Rates, What Really Happens to Stocks?

- Tools & Tips: Total Compensation Calculator

- Market Overview

-

Why Actively Managed Bond Funds Outperform Index Funds More Often Than Stocks

Multiple research results now point to what seems like a consistent pattern: active bond funds tend to outperform their passive peers more often than stock funds do.

-

Certificates of Deposit (CDs) vs. Treasuries: The Key Pros and Cons Explained

In this article, we summarize the pros and cons between CDs and Treasuries for fixed-income investors. Key Differences Between Certificates of Deposit (CDs) and Treasuries Factor CDs Treasuries Security – FDIC-insured up to $250,000 per depositor per bank. + Backed by the full faith and credit of the U.S. government, Treasuries are considered among the safest investments, with security that surpasses even FDIC insurance. – Limited insurance coverage for amounts above $250,000 at each bank. + No limit to the amount of protection. Yield + Generally higher yields for maturities of 1 year or longer. – Typically lower yields for maturities over 1 year. – Lower yields for shorter maturities compared to Treasuries. + Higher yields for short-term maturities (less than 1 year). Note: this could possibly change so double check yields before purchase. Taxes – Subject to both federal and state income taxes. + Exempt from state income taxes. – State tax impact can reduce effective yield, especially in high-tax states. + More tax-efficient, especially in high-tax states. Maturities – Limited availability for maturities beyond 5 years. + Wide range of maturities (4 weeks to 30 years). – Flexibility can be restricted depending on the bank’s capital needs and availability of brokered CDs in a brokerage like Schwab or Fidelity. + Extensive maturity options between 2023–2053. Liquidity – Less liquid, may involve fees or uncertainty of receiving original principal if sold early. + More liquid, with an active secondary market for easy resale. – Brokered CDs can be sold in secondary markets but may involve a fee. + Easier to sell with tighter bid/ask spreads. Strategy Considerations – Fewer maturity options for building a maturity CD ladder. + Easier to build a flexible bond ladder portfolio. Convenience + Banks often promote CDs with lower yields. – Has to rely on Brokerage to purchase/sell Treasuries most times Detailed Tax Impact Comparison: State Tax Impact CDs Treasuries For High-Tax States – State income taxes can reduce yield significantly (e.g., California, New York). + State income tax exemption offers a clear tax benefit. Example – In California, a 3-year CD yielding 3.90% after state taxes drops to 3.38%. + A 3-year Treasury yielding 3.51% remains unaffected by state taxes. Breakeven Tax Rate – For a CD to equal a Treasury’s yield, a state tax rate of ~10% or more may be required. + More tax-efficient for investors in high-tax states. Conclusion In summary: