9 Lessons From Retirees’ Biggest Retirement Regrets

In this issue:

- 9 Lessons From Retirees’ Biggest Retirement Regrets

- Returns of MyPlanIQ Core Model Portfolios

- Portfolio Simulator (Calculator)

- Lazy Portfolios: Simple Templates for 401(k) and IRA Investments

- Market Overview

9 Lessons From Retirees’ Biggest Retirement Regrets

Business Insider recently surveyed over 3,300 older Americans that revealed common retirement regrets. Drawing from this survey and additional insights elsewhere, we’ve identified the top 9 lessons younger Americans can use to improve their retirement planning:

The number one regret among these retirees, as many might have guessed, is not starting to save and invest early! This basically aligns with the core message of this newsletter.

Here are the top lessons:

- Start Saving and Investing Early

- Begin saving in your early 20s or even in college, even if contributions are small.

- Contribute enough to employer-sponsored retirement plans to receive the full match and increase savings as your salary grows.

- For those without workplace plans, consider IRAs (Traditional or Roth). Solo 401(k) and SEP IRA are often ignored by self-employed.

- Investing early allows you to capitalize on compound interest and reduce reliance on Social Security.

- Diversify Retirement Accounts and Investments

- Open brokerage accounts to start investing with minimal barriers.

- Explore Roth 401(k)s if you anticipate being in a higher tax bracket later in life.

- Avoid Over-Reliance on Social Security

- Relying solely on Social Security can lead to financial constraints later in life.

- Delay claiming Social Security benefits until full retirement age (67) to maximize payouts.

- Plan for Major Life Events (Divorce or Spouse’s Death)

- Married couples should align their retirement goals and analyze finances as a household.

- Protect assets with prenuptial agreements and consider trusts for wealth preservation.

- Ensure there’s a will and life insurance policy to secure assets and income in the event of a spouse’s death.

- Build a Robust Emergency Fund

- Save three to six months’ worth of expenses as a safety net; increase this to one to two years as retirement nears.

- Be prepared for unexpected expenses, such as medical emergencies, layoffs, or natural disasters like the recent wildfire tragedy in Los Angeles!

- Factor Healthcare Costs into Planning

- Regularly research and evaluate insurance options to minimize out-of-pocket expenses.

- Factor in long-term care cost that will be needed at some point!

- Utilize Government Assistance and Benefits

- Consult benefits counselors to determine eligibility and conserve personal savings.

- Investigate programs like SNAP or Medicaid for potential financial support.

- Balance Saving and Enjoying Life

- Avoid regrets of over-saving by maintaining a balance between preparing for retirement and enjoying the present.

- It’s all about balance: fulfilling experiences while securing your financial future.

- Seek Professional Financial Advice

- Even if you’re financially savvy, advice and guidance from a professional serve as a valuable second opinion and a regular reminder to help you stay on course!

Returns of MyPlanIQ Core Model Portfolios

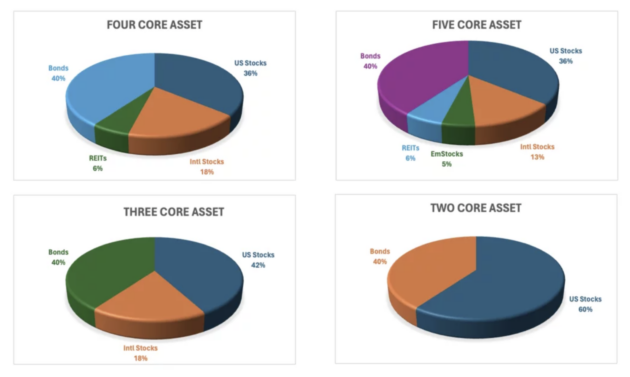

It’s a good time to review the latest returns of the core asset allocation portfolios we maintained on Asset Allocation Portfolio Templates.

Here are the allocations of these model portfolios:

In the above, the four assets US Stocks, Intl (International) Stocks, REITs, and Bonds are represented by index funds:

| Asset Class | Fund |

|---|---|

| US Stocks | VTSMX (VANGUARD TOTAL STOCK MARKET INDEX FUND INVESTOR SHARES) |

| International Stocks | VGTSX (VANGUARD TOTAL INTERNATIONAL STOCK INDEX FUND INVESTOR SHARES) |

| Emerging Market Stocks | VEIEX (VANGUARD EMERGING MARKETS STOCK INDEX FUND INVESTOR SHARES) |

| REITs (Real Estate Investment Trusts) | VGSIX (VANGUARD REIT INDEX FUND INVESTOR SHARES) |

| Bonds | VBMFX (VANGUARD TOTAL BOND MARKET INDEX FUND INVESTOR SHARES) |

The latest total returns (dividends reinvested):

| Name | 2024 | 1Yr AR | 3Yr AR | 5Yr AR | 10Yr AR | 15 Yr AR | 20Yr AR |

|---|---|---|---|---|---|---|---|

| MyPlanIQ Core Two Assets | 13.7% | 13.10% | 3.99% | 7.71% | 7.93% | 8.85% | 7.56% |

| MyPlanIQ Core Three Assets | 10.7% | 10.30% | 2.56% | 6.28% | 6.73% | 7.34% | 6.77% |

| MyPlanIQ Core Four Assets | 9.54% | 9.01% | 1.78% | 5.65% | 6.25% | 7.12% | 6.64% |

| MyPlanIQ Core Five Assets | 9.78% | 9.22% | 1.68% | 5.54% | 6.18% | 7.03% | 6.74% |

| VBINX (VANGUARD BALANCED INDEX FUND INVESTOR SHARES) | 10.54% | 9.81% | 2.10% | 6.42% | 7.30% | 8.41% | 7.18% |

All of these portfolios delivered double-digit returns in 2024. Notably, those with a higher concentration of U.S. stocks, such as MyPlanIQ Core Two Assets or VBINX (VANGUARD BALANCED INDEX FUND INVESTOR SHARES), achieved the highest returns. This outcome isn’t surprising, as U.S. stocks outperformed all other asset classes in 2024.

Stay balanced and diversified

If you’re active on social media platforms like Reddit, you’ve likely come across posts bragging or discussing how people’s 401(k) accounts performed well in 2024.

Some observations:

- Returns varied widely, ranging from about 8% to 25%

- One user reported an 8.9% return as of mid-2024

- Another mentioned achieving a 15.8% one-year return

- Some users saw even higher returns, with one reporting a 25.63% return using Fidelity FCNTX

- A Thrift Savings Plan (federal employee 401(k)) user noted returns around 10% since the 1980s

The core portfolios mentioned above are well-balanced and well-diversified. These portfolios provide smoother and steadier performance during tough times and reasonable returns during good times (as seen over the past two years). Our advice: stay on course and invest in such well-balanced and well-diversified portfolio. Be prepared for the long haul—no need to swing for the fences. Patience and consistency will pay off.

Tools & Tips: Portfolio Simulator (Calculator)

Many people overlook one of the most valuable tools for managing their 401(k) accounts: the MyPlanIQ Portfolio Simulator (Calculator). This tool allows you to see how your current or planned investment mix (portfolio) in a 401(k) account might have performed historically if you had maintained those investments and their allocations over time. For 401(k) beginners, this simulator provides a hands-on understanding of how different investment mixes could have performed in the past.

For example, if you have a 401(k) in NVIDIA CORPORATION 401(K) PLAN, and you have the following fund mixes in the account:

- VFFSX (VANGUARD 500 INDEX FUND INSTITUTIONAL SELECT SHARES): 40%

- RERFX (EUROPACIFIC GROWTH FUND CLASS R-5): 20%

- DODIX (DODGE & COX INCOME FUND DODGE & COX INCOME FUND): 40%

You can enter this in Portfolio Simulator (Calculator) as follows:

Note that among the three funds in the portfolio, VFFSX has the most recent start date of 03/30/2016. The simulator uses this date as the starting point for the portfolio. If you want to see older simulation results, you can replace VFFSX with VFINX, which has a start date going back to 1979.

You’ll find a variety of data for the simulated portfolio history, including its historical returns, a return chart, and other analytical insights.

| Name | YTD | 1Yr AR | 3Yr AR | 5Yr AR | 10Yr AR | 15 Yr AR | 20Yr AR |

|---|---|---|---|---|---|---|---|

| Portfolio | -0.71% | 9.74% | 2.87% | 6.82% | NA | NA | NA |

| VFINX (VANGUARD 500 INDEX FUND INVESTOR SHARES) | -0.89% | 22.97% | 9.07% | 13.93% | 13.02% | 13.44% | 10.27% |

| VBINX (VANGUARD BALANCED INDEX FUND INVESTOR SHARES) | -0.89% | 9.81% | 2.10% | 6.42% | 7.30% | 8.41% | 7.18% |

To save this portfolio for further use, you should register an account and use Create a Static Portfolio instead. You can find the link on your Dashboard.

You can even add stocks to the calculator, making it a great exercise to compare how a stock portfolio has performed against a balanced fund portfolio.

Lazy Portfolios: Simple Templates for 401(k) and IRA Investments

Market Overview

Stocks extended their New Year downtrend, with the main driver appearing to be the surprisingly strong job market data. The December 2024 jobs report revealed stronger-than-expected growth in the U.S. labor market:

- Nonfarm payroll employment increased by 256,000 jobs, way above the Dow Jones consensus forecast of 155,000.

- The unemployment rate dipped slightly to 4.1%, beating the expected 4.2%.

Investors are concerned that a hot job market could keep inflation elevated, reducing the likelihood of the Federal Reserve continuing to cut interest rates. As a result, the 10-year Treasury note yield has climbed above 4.6%, pushing the 30-year mortgage rate up to 6.78%. With high interest rates, consumer spending and business operating costs are likely to stay elevated. This development isn’t favorable for either stocks or bonds.

The following table shows the major asset price returns, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | -2.3% | -4.1% | -0.4% | 3.9% | 23.1% | 4.0% |

| Foreign Stocks | -1.6% | -5.6% | -9.1% | -6.9% | 3.2% | -4.0% |

| US REITs | -4.3% | -8.7% | -9.6% | -1.3% | 1.1% | -4.6% |

| Emerging Market Stocks | -3.9% | -8.2% | -11.6% | -6.0% | 5.7% | -4.8% |

| Bonds | -1.0% | -2.0% | -3.2% | -1.2% | -0.1% | -1.5% |

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?