Introducing the Save More, Grow Wise Newsletter

Dear long-time and newly joined subscribers,

For more than a decade, we’ve offered free newsletters on retirement investments and savings. The number of subscribers has grown significantly, and our newsletters have been well received by readers with diverse interests.

Many of you may have noticed that MyPlanIQ has greatly expanded its coverage of retirement-related topics. These now include retirement plans (we can proudly say MyPlanIQ offers the most comprehensive 401(k) and 403(b) plan information), retirement savings and contributions, mutual funds, ETFs, extensive lazy and active investment portfolio strategies, and other personal finance topics. Along with this, we’ve introduced several new tools, including a variety of calculators for you to explore in these areas.

We believe MyPlanIQ has reached a point where our readers would be better served with two separate newsletters:

- A free weekly newsletter titled Save More, Grow Wise, focusing on broad topics like retirement savings, investments, and other relevant personal finance issues and education. We will cover current savings strategies, investment insights, retirement planning, personal finance topics such as debt management and spending, as well as feature calculators and tools to help guide you.

- The In-Depth Retirement Investment Newsletter is designed for our existing paid subscribers who are primarily interested in premium investment portfolios and research. This newsletter will focus on detailed discussions of the portfolios we support, including insights into current premium portfolio transactions, in-depth portfolio strategy analysis, comprehensive studies of ETFs, mutual funds, and even stocks, along with coverage of the current investment landscape and market conditions. Over the years, many of our paid subscribers have requested this traditional investment newsletter format. This newsletter will be delivered monthly, typically on the first Monday of the month.

Let’s dive into this first edition of the Save More, Grow Wise weekly newsletter.

Retirement Crisis or Brighter Future: A Tale of Two Cities

In a 2023 survey conducted by Northwestern Mutual, it was indicated that Americans believe they need approximately $1.27 million to retire comfortably. However, their 2024 survey now shows that this figure has increased to $1.46 million. At that time, it was reported that.

- Half of American households have no retirement savings at all

- Among those who do save, the average amount in retirement accounts is less than $90,000

- Over half of small to mid-sized business employees lack access to a 401(k) plan

- 64% of baby boomers report moderate to high levels of stress about their retirement savings

Fast forward to 2024: the latest report from Fidelity Investments indicates that the number of 401(k) “millionaires” has reached a new record high.

- There were approximately 497,000 401(k) accounts with balances of $1 million or more as of June 30, 2024. The average tenure for 401(k) millionaires is 27 years — long-term saving and investing is the key to success!

- The average 401(k) balance across all accounts rose to $127,100, a 1% increase from the start of the year and a 13% jump from the previous year.

- The median 401(k) account balance was $55,500

- On average, Americans are saving about 14.2% of their income for retirement, just shy of the 15% recommended by experts

On the last point, it’s a paradoxical behavior: when financial markets are performing well, people tend to feel encouraged and save more. However, when markets are struggling, they often retreat and may reduce their savings or even stop contributions altogether. In reality, if you have a solid, diversified portfolio, you should aim to increase your contributions and savings during a market crisis, as assets are simply cheaper at that time. Rest assured, this newsletter will always be by your side, rain or shine, to help you navigate the ups and downs.

As for the median 401(k) account balance at Fidelity, which was only $55,000 and seems low, bear in mind that many Americans switch jobs and may have multiple 401(k) accounts as well as IRAs.

We find ourselves in a challenging situation: nearly half of Americans have no retirement savings, and many who do are saving insufficient amounts. In contrast, those who save diligently and invest wisely have accumulated significant savings. This newsletter aims to guide you on your journey toward building a financially secure retirement, helping you become part of the latter group through consistent saving and smart investing.

ExxonMobil Savings Plan — Halfway to 401(k) Millionaires

Speaking of 401(k) millionaires, a quick study of the EXXONMOBIL SAVINGS PLAN reveals that in 2022, the average employee account value in the plan was $566,353 for approximately 37,549 employees. Notably, the largest energy company also offers a very generous match, contributing an average of $10,382 to each account in 2022! Browse our plan database to discover more interesting data.

On the topic of 401(k) millionaires, we will provide a more in-depth and interesting report later on.

Tools & Tips

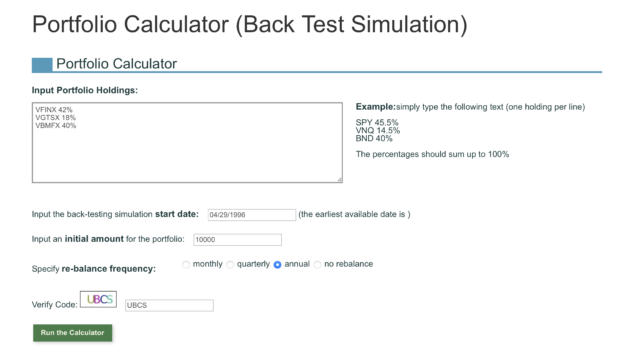

One of our most popular tools is the Portfolio Simulator, or Calculator. It allows you to quickly enter the funds in your 401(k) account and see how that portfolio (the combination of those funds) has performed over the past several years. For example, on the Investments tab of AMAZON 401(K) PLAN, you can find the Portfolio Simulator link. Supposed you have the following combination of funds in your portfolio or you just want to test out such a portfolio:

- 42% US Stocks: VANG INST 500 IDX TR COLLECTIVE TRUST FUND (Index Fund)

- 18% International Stocks: VG IS TL INTL STK MK COLLECTIVE TRUST FUND (Index Fund)

- 40% Bonds: VG IS TOT BD MKT IDX COLLECTIVE TRUST FUND (Index Fund)

You can enter them in the portfolio calculator as follows:

and see returns and other charts once you click on ‘Run the Calculator’:

This calculator generates a wealth of additional data, including historical rolling returns, maximum drawdowns, and more. It’s a quick and efficient way to evaluate how your portfolio would have performed in the past. However, it’s important to remember that these figures reflect historical performance and do not guarantee future results. Always consider that past returns are not indicative of future performance, and it’s essential to stay informed about market conditions and investment strategies.

Investment News

Goldman Sachs recently predicted that the S&P 500 index will deliver an annualized return of just 3% over the next decade. This represents a significant drop compared to the 13% annualized return seen in the previous decade. The forecast is based on concerns about factors such as market concentration, which has reached its highest level in 100 years due to the dominance of a handful of stocks, including Apple, Microsoft, Amazon, Nvidia, and Meta. Excluding this high level of concentration, Goldman Sachs predicts that the equal-weighted S&P 500 (RSP) would return 7% annually over the next decade.

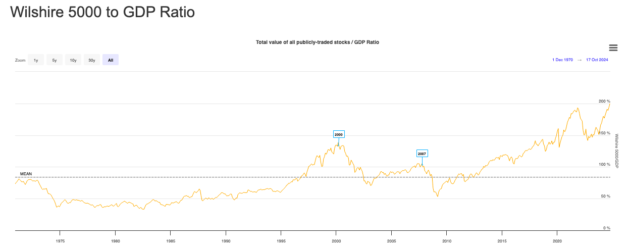

This isn’t entirely new for long-term MyPlanIQ readers; we have pointed out that U.S. stocks have been expensive by many historical metrics. In fact, the famous Buffett Indicator, which measures total stock market capitalization relative to GDP (Gross Domestic Product), has reached 200%—the highest level since 1971, when data first became available. This figure significantly exceeds the high end of 115%, which is considered the threshold for the U.S. stock market to be fairly valued.

Data source: longtermtrends.com

Other market valuation metrics, such as the Shiller CAPE10, also indicate that the stock market is at one of its highest levels in history, currently at 37 compared to its long-term average of 17.

Intuitively, when stocks are expensive, their prices tend to revert back to historical norms over time; they cannot remain at a permanently high plateau indefinitely. Of course, it’s important to recognize that market valuation has a weak correlation with short-term stock market returns. However, it does have a strong correlation with long-term returns, particularly over the subsequent 10 years or longer.

Market Overview

The major U.S. stock indices continued their upward trend, with the S&P 500, Dow Jones Industrial Average, and NASDAQ each rising by more than 1% for the week. The S&P 500 reached new record highs.

However, in fixed income or bonds, intermediate and long-term bond yields rose due to concerns about inflation and the potential for a slower pace of interest rate cuts by the Federal Reserve. This, in turn, drove bond prices lower, as bond yields and prices have an inverse relationship.

The following table shows the major asset price returns:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 0.9% | 2.9% | 6.9% | 18.8% | 40.7% | 14.0% |

| Foreign Stocks | -1.5% | -0.1% | 2.9% | 9.5% | 26.3% | 7.4% |

| US REITs | 0.2% | -2.5% | 7.4% | 22.3% | 38.7% | 13.2% |

| Emerging Market Stocks | -0.9% | 4.4% | 7.5% | 16.0% | 29.1% | 11.2% |

| Bonds | -0.5% | -2.2% | 1.8% | 5.4% | 10.7% | 3.0% |

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?