-

Super Businesses, Super Stocks

- Latest in Retirement Savings & Personal Finance

- Super Businesses, Super Stocks

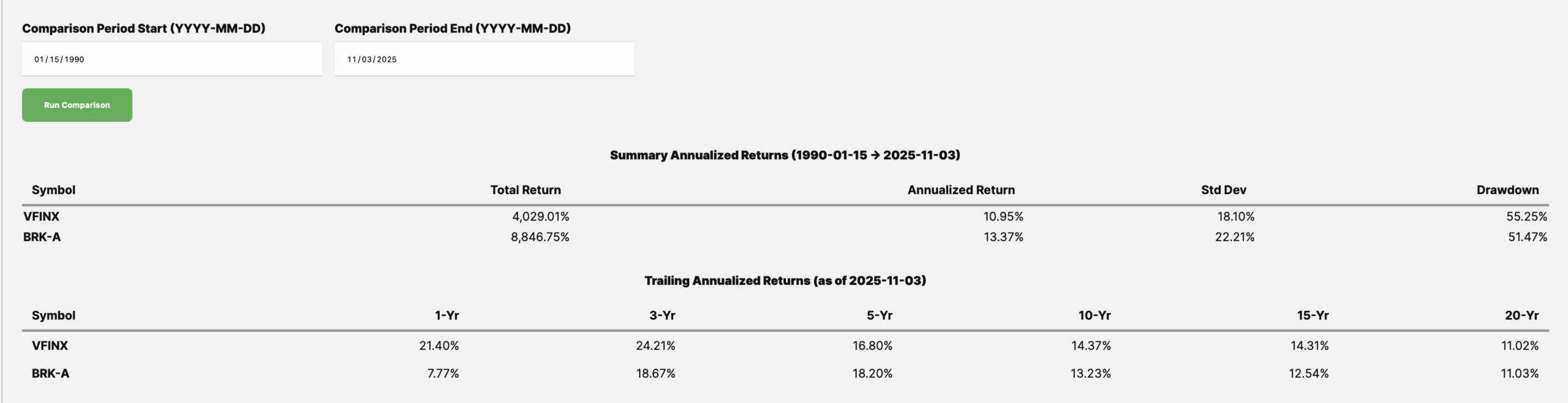

- Tools & Tips: Return Comparison Calculator

- Market Overview

-

2024 Millionaire Retirement Plans

- Latest in Retirement Savings & Personal Finance

- 2024 Millionaire Retirement Plans

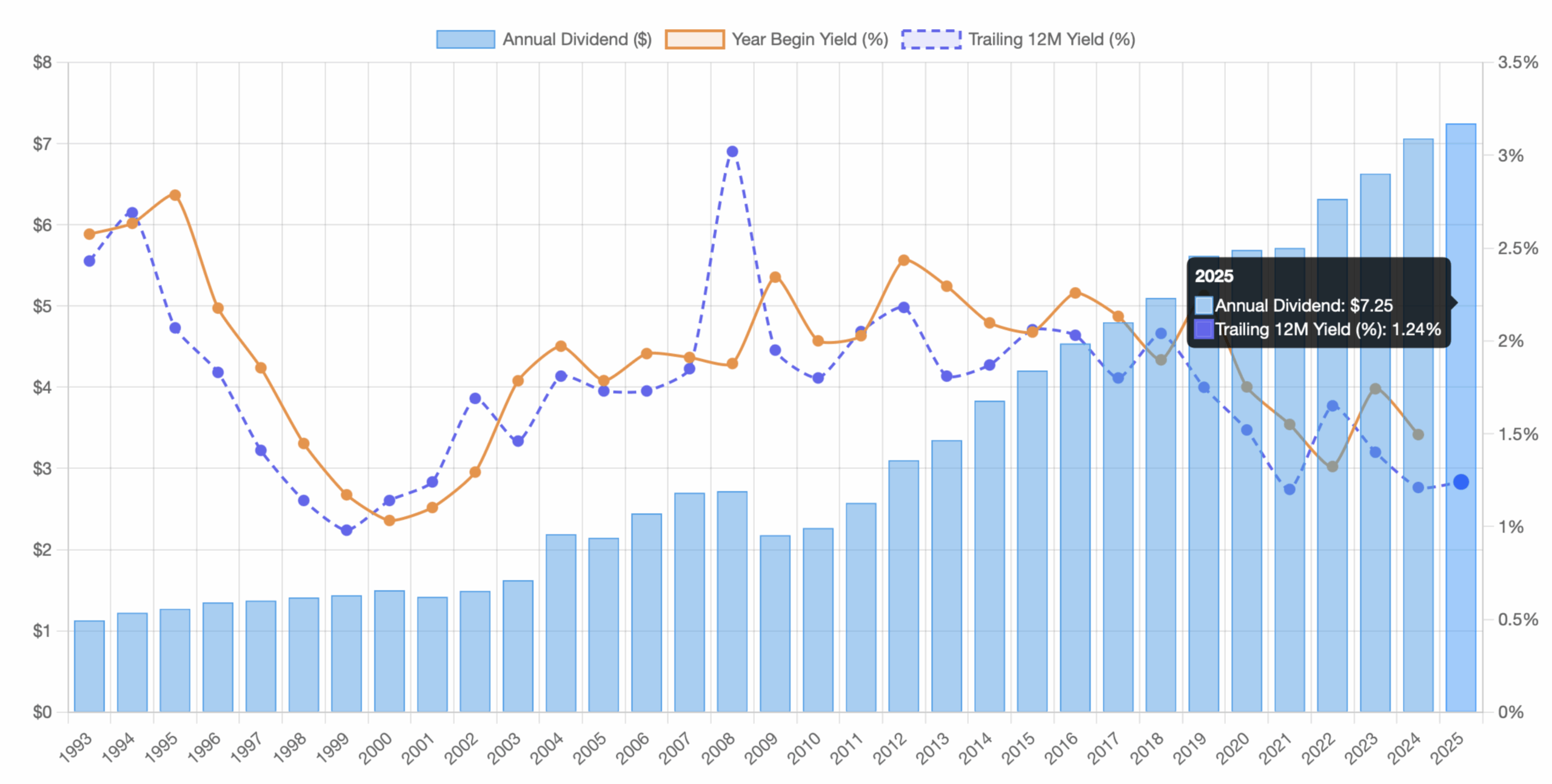

- Tools & Tips: Historical Stock Dividend Yield Chart

- Market Overview

-

Last Quarter Checklist for 2025

- Latest in Retirement Savings & Personal Finance: All the Glittering Gold, Highest Household Credit Card Debt, More PE Funds Than McDonald’s

- Last Quarter Checklist for 2025

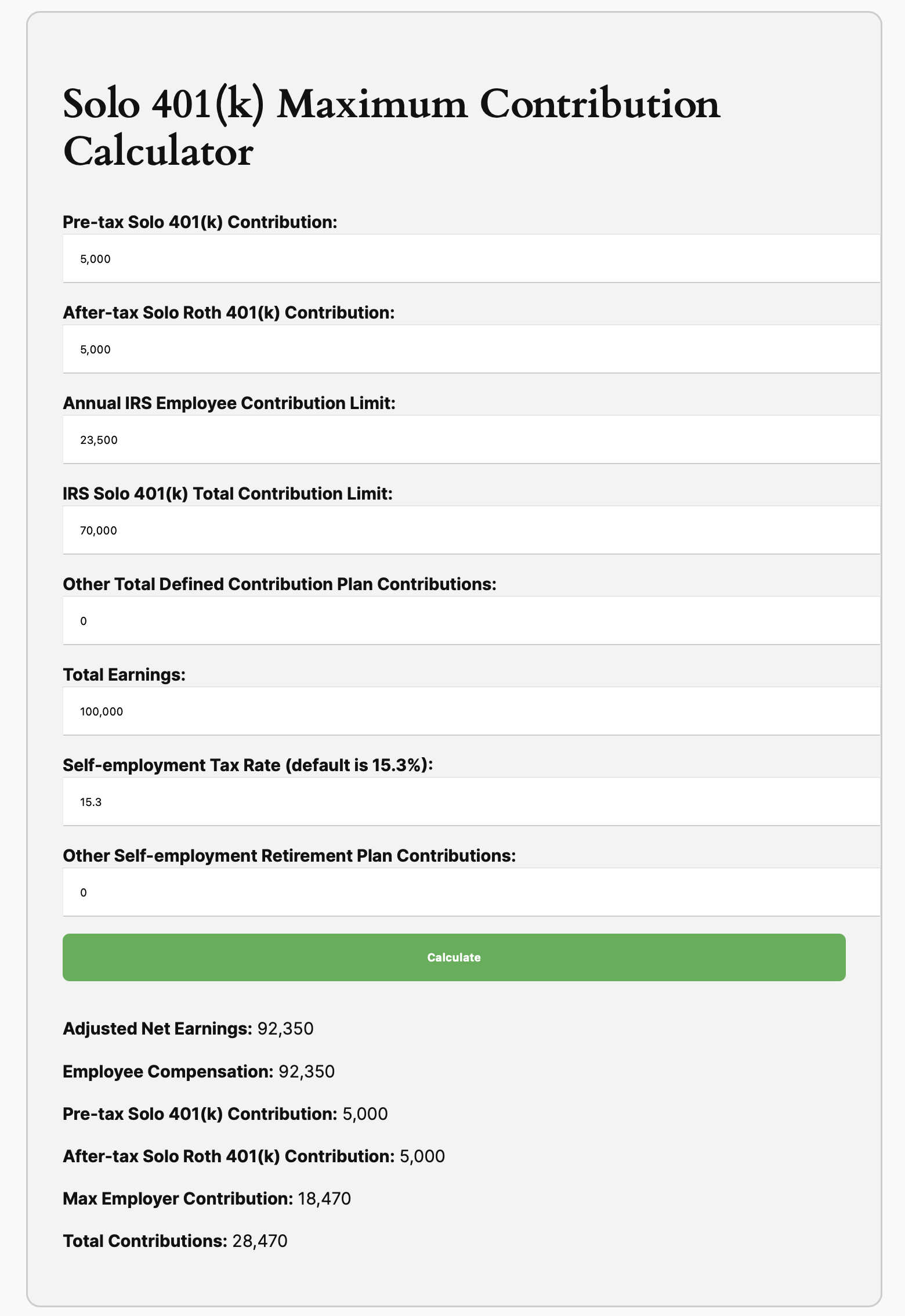

- Tools & Tips: Solo 401(k) Maximum Contribution Calculator

- Market Overview

-

HSA: One of The Biggest Tax Break You Shouldn’t Ignore

- Latest in Retirement Savings & Personal Finance: What Fed Rate Cut Means for You? Surge in Electricity Prices

- Health Savings Account (HSA): One of The Biggest Tax Break You Shouldn’t Ignore

- Tools & Tips: HSA Savings Calculator

- Market Overview

-

Best Strategy to Withdraw Funds in Retirement

When you retire, the order you pull funds from your accounts (whether taxable, traditional, or Roth) can make big difference.

-

Retirement Plan Contribution Limits in 2024

2024 Retirement Plan Contribution Limits 1. 401(k), 403(b), and 457(b) Plans Employee Contributions: Up to $23,000 (under age 50) Catch-up contribution: $7,500 (ages 50+) Total Combined Limit (Employee + Employer): $69,000 Roth Options: Available for 401(k), sometimes for 403(b) and 457(b) Plan Details: 401(k): Primarily for for-profit companies; includes Roth (after-tax) options. 403(b): For public schools and nonprofits; Roth-style options less common. 457(b): For state/local government and some tax-exempt organizations; Roth availability varies. 2. Solo 401(k) and SEP IRA Solo 401(k): For self-employed individuals/business owners without employees.

- Employee contributions: $23,000, plus $7,500 catch-up (ages 50+)

- Employer contributions: up to 25% of compensation

- Total combined limit: $69,000 or 25% of compensation, whichever is less

SEP IRA: Employer contributes up to 25% of compensation, up to $69,000. No catch-up contribution. 3. SIMPLE IRA

- Employee contribution: up to $16,500

- Catch-up contribution: $3,500 (50+)

- Employer must match dollar-for-dollar up to 3% of employee salary

- Immediate vesting

4. Traditional and Roth IRAs

- Annual contribution: $7,000

- Catch-up: additional $1,000 (50+)

Traditional IRA: Pre-tax contributions, taxable upon withdrawal Roth IRA: After-tax contributions, tax-free withdrawals 5. Thrift Savings Plan (TSP)

- Federal and uniformed services employees only

- Employee contributions: up to $23,000 (under age 50), plus catch-ups ($7,500 at 50+)

- Employer matches up to 5% of salary

- Total Combined Limit (Employee + Employer): $69,000

- Pre-tax (traditional) and Roth contributions allowed

6. Payroll Deduction IRA

- Annual limit: $7,000; catch-up of $1,000 (age 50+)

- Pre-tax or Roth contributions

- No employer matching

7. Health Savings Account (HSA)

- Individual coverage: $4,150

- Family coverage: $8,300

- Catch-up contribution: additional $1,000 for age 55+

- Must have a high-deductible health plan

- Tax-free growth; penalty-free medical withdrawals; penalty-free non-medical withdrawals after age 65 (taxable)

8. Self-Directed IRA (SDIRA)

- Contribution limits same as IRAs ($7,000 + $1,000 catch-up age 50+)

- Allows alternative investments (real estate, precious metals, crypto)

- Requires IRS-approved custodian

9. Nondeductible IRA

- Same limits as traditional IRAs ($7,000 + $1,000 catch-up age 50+)

- Contributions not tax-deductible; earnings taxable at withdrawal

10. Annuities and Pension Plans (Brief Overview)

- Annuities: Insurance-based retirement products, providing guaranteed income. High fees, limited liquidity.

- Pension Plans: Employer-funded defined-benefit plans providing guaranteed lifetime income. Limited investment control.

11. Flexible Spending Account (FSA) Limits for 2024

- The maximum employee contribution to a health care FSA for 2024 is $3,200.

- If the FSA plan allows for carryover, the maximum amount that can be carried over to 2025 is $640.

- For Dependent Care FSAs, the maximum remains $5,000 per household (single or married filing jointly) or $2,500 if married and filing separately.

12. Health Savings Account (HSA) Limits for 2024 Coverage Type 2024 Contribution Limit Catch-Up (Age 55+) Minimum Deductible Out-of-Pocket Max Self-only $4,150 +$1,000 $1,600 $8,050 Family $8,300 +$1,000 (per eligible spouse, each in own HSA) $3,200 $16,100

- Individuals age 55 or older can contribute an additional $1,000 as a catch-up contribution.

- HSA contributions can be made until the tax filing deadline (April 15, 2025, for tax year 2024).

- To be eligible for HSA contributions, you must be enrolled in a high-deductible health plan (HDHP) meeting the minimum deductible and out-of-pocket maximum requirements above.

-

Simple 401(k) Investment Guide

In this issue:

- Latest in Retirement Savings & Personal Finance: College Education Affordability Declined, Rising Debt Puts Your 401(k) Retirement Savings in a Pickle

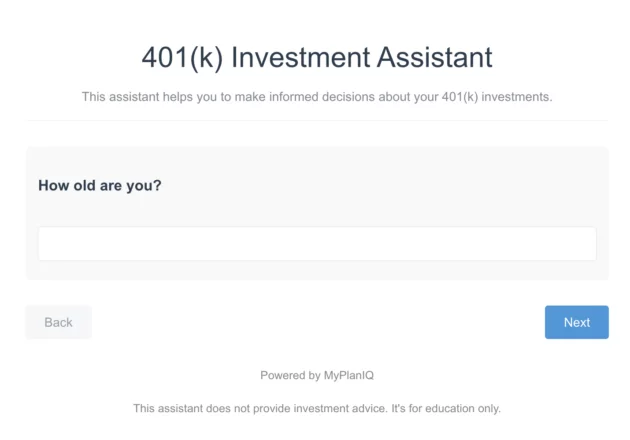

- Simple 401(k) Investment Guide

- Tools & Tips: 401(k) Investment Assistant

- Market Overview

-

Income Growth, Historical 401(k) Contribution Limit Data

In this issue:

- Latest in Retirement Savings & Personal Finance: Interest Rates Rise Again, Rising Home Insurance Cost, …

- Historical Income Growth, 401(k) Contribution Limit Growth

- Tools & Tips: 401(k) Maximum Match Calculator — Marvell Semiconductor

- Market Overview

-

How Much Should I Save for Retirement By Age? A Realistic Reference

In this issue:

- Latest in Retirement Savings & Personal Finance: Medicare Rude Surprise, Scoop to Be a Millionaire

- How Much Should I Save for Retirement By Age? A Realistic Reference

- Tools & Tips: Retirement Savings by Age Calculator

- Market Overview

-

Realistic Reference Data on Retirement Savings by Age in 2025

A realistic accumulated savings figures by age in 2025 for various income level people.

-

Warren Buffett’s Phenomenal Run: The Oracle May Retire, But His Legacy Endures

In this issue:

- Latest in Retirement Savings & Personal Finance: Social Security Early Claims Surge, Student Loan Collection Resumed, …

- Warren Buffett’s Phenomenal Run: The Oracle May Retire, But His Legacy Endures

- Tools & Tips: Rolling Return Calculator

- Market Overview

-

One Fund Does It All

In this issue:

- Latest in Retirement Savings & Personal Finance: US Food & Engergy Inflation Charts, Empty Shelfs Coming? Part-time Contractors Rejoin on 401(k) Eligibility

- One Fund Does It All: Savings & Investing in 401(k) Might Not Be That Intimidating

- Tools & Tips: Retirement Spending Calculator

- Market Overview

-

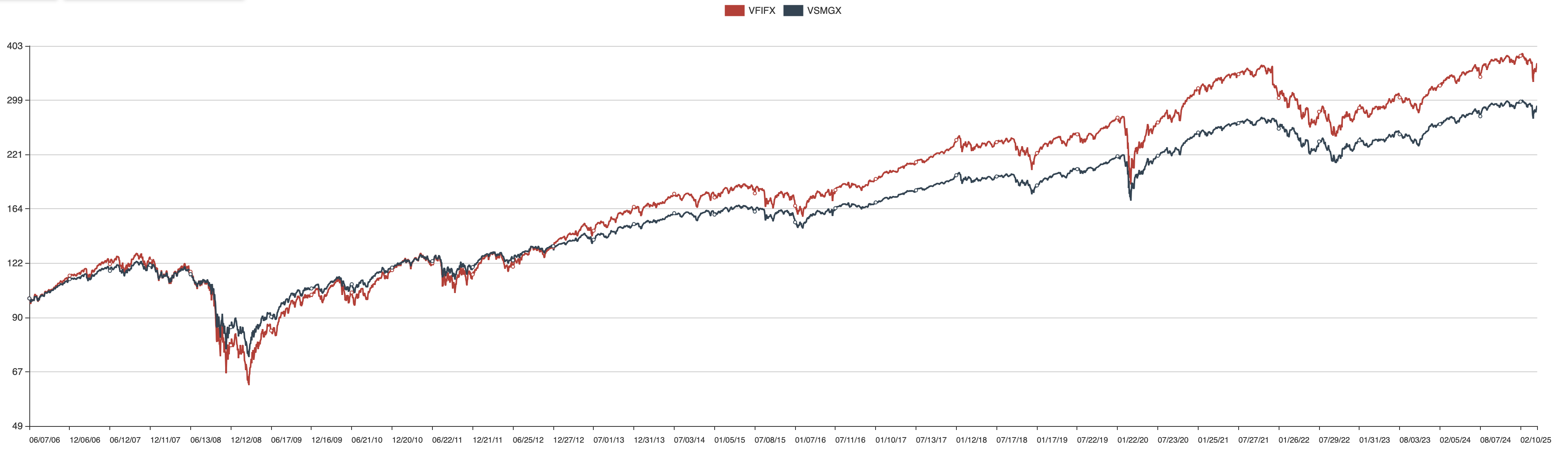

The One-Fund 401(k) Portfolio: Simple Yet Does Its Job

One-fund portfolio, either a target-date fund or just a balance index fund, does a good job for retirement plan investors who have little experience or who don’t want to mess around.

-

Roth IRAs for Retirees

Roth IRAs can be very useful for retirees in terms of medicare premiums, estate planning and other benefits.

-

Lazy Portfolios Aren’t Lazy in Growing Wealth

In this issue:

- Latest in Retirement Savings & Personal Finance: Golden Rule and The Roth IRA Evangelist

- Lazy Portfolios Aren’t Lazy in Growing Wealth

- Tools & Tips: Investment Arithmetic

- Market Overview

-

IRAs as One of the Emergency Fund Sources

In this issue:

- Latest in Retirement Savings & Personal Finance: Back-and-forth Tariff Policies, Stock Market Swings, and Low Retirement Savings Rates

- IRAs as One of the Emergency Fund Sources

- The Gotcha in Maximum Solo 401(k) or SEP IRA Contribution Limits

- Market Overview

-

How to Borrow From an IRA?

There are several ways to take money out for short-term emergency purposes. This article explores some of those options.

-

Special Issue: Staying the Course Amid Market Turmoil

In this special issue:

- Latest in Retirement Savings & Personal Finance: Market Turmoil, Majority of Americans Invest in Stocks, …

- Staying the Course Amid Market Turmoil

- Tools & Tips: Longest S&P 500 Losses (Drawdowns)

- Market Overview

-

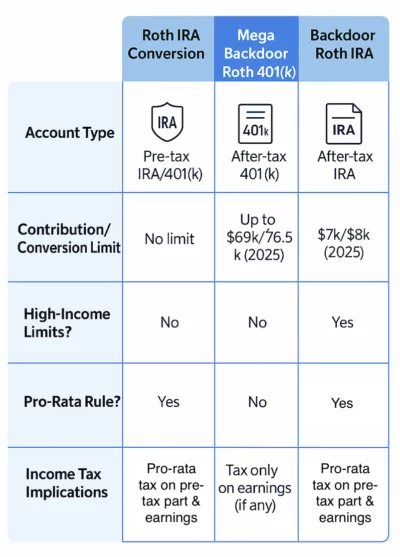

The ABCs of Roth Conversions: Backdoor, Mega Backdoor, and More

In this issue:

- Latest in Retirement Savings & Personal Finance: Tariff Liberation Day, Beefing Up Emergency Savings, and Consumer Confidence at Its Lowest

- The ABCs of Roth Conversions: Backdoor, Mega Backdoor, and More

- Tools & Tips: Social Security Income Calculation Infographic

- Market Overview

-

Retirement Plan Contribution Limits in 2025

Comprehensive retirement plans (401(k), 403(b, 457(b), Solo 401(k), SEP IRA, SIMPLE IRA, IRA, Roth IRA, TSP, HSA etc.) contribution limits for 2025