Variable Annuity vs 401(k) vs IRA: A Beginner’s Guide

Variable annuities get marketed as “tax-deferred alternatives” to 401(k)s. The pitch: invest without annual tax drag on dividends and capital gains. But the reality is more complicated. This guide breaks down when a variable annuity actually makes sense … and when you’re better off with a taxable account.

Bottom line: Variable annuities are rarely a substitute for 401(k)s and IRAs. They work best only after you’ve maxed out your employer plan and IRA, have a specific need (creditor protection, RMD avoidance), and are willing to pay higher fees for tax-deferred growth. For most investors, a taxable brokerage account with index funds beats a variable annuity on an after-tax, after-fee basis.

What Is a Plain Vanilla Variable Annuity?

A variable annuity is a contract with an insurance company. You invest in sub-accounts (similar to mutual funds). Your returns fluctuate with the market, hence “variable.”

Plain vanilla means no income riders, no guaranteed returns, no complex insurance wrappers. Just tax-deferred investing inside an insurance chassis.

Vanguard Personal Annuity: The Exception That Proves the RuleVanguard’s variable annuity is the closest thing to a “good” variable annuity for DIY investors:

- Total expense ratio: ~0.50% annually (M&E charges + underlying fund expenses)

- Investment options: 20+ Vanguard funds including Total Stock Market, Total Bond Market, Total International Stock, Wellington, Windsor, and target-date options … broader than most small-business 401(k) plans

- No surrender charges: Unlike industry-standard 5-7 year surrender periods, Vanguard doesn’t lock up your money

- Minimum investment: $5,000 to open

Even this low-cost option rarely beats a taxable brokerage account with index funds. But if you’re determined to use a variable annuity, Vanguard’s version minimizes the damage.

Quick Comparison: 401(k), IRA, and Variable Annuity

| Feature | 401(k) | Traditional IRA | Variable Annuity |

|---|---|---|---|

| 2025 Contribution Limit | $23,500 ($31,000 if 50+) | $7,000 ($8,000 if 50+) | Unlimited |

| Tax Deduction | Yes (pre-tax) | Yes (income limits) | No |

| Employer Match | Often yes | No | No |

| Typical Fees | 0.5% – 1.0% | 0.03% – 0.20% | 0.50% – 2.5%+ |

| Surrender Charges | None | None | Typically 5-7 years (Vanguard: none) |

| RMDs Required | Yes (age 73) | Yes (age 73) | No |

| Withdrawal Taxation | Ordinary income | Ordinary income | Ordinary income (gains only) |

| Early Withdrawal Penalty | 10% before 59½ | 10% before 59½ | 10% on gains before 59½ |

The Fee Reality: Why Costs Matter

Most variable annuities charge 1.5% – 2.5% annually in total fees (M&E charges + administrative fees + investment management). Vanguard’s 0.50% is the outlier.

Here’s what that costs you over 30 years, assuming $10,000 annual contributions and 7% gross returns:

| Account Type | Annual Fee | Ending Balance | Total Fees Paid |

|---|---|---|---|

| IRA (Index Funds) | 0.10% | ~$945,000 | ~$35,000 |

| Vanguard Variable Annuity | 0.50% | ~$875,000 | ~$105,000 |

| Typical Variable Annuity | 2.00% | ~$680,000 | ~$300,000 |

The Nondeductible Problem: When 401(k) and IRA Lose Their Edge

Here’s where the comparison gets interesting. Variable annuities compete not with deductible 401(k)s and IRAs (those win handily), but with nondeductible options.

When Your 401(k) Contributions Are After-Tax

Some investors face situations where traditional 401(k) contributions don’t reduce taxable income:

- You’re a high earner in a plan that only allows Roth contributions

- You’re making after-tax contributions for a Mega Backdoor Roth strategy

- You’re in a non-qualified plan

When Your IRA Contributions Are Nondeductible

If your income exceeds IRS limits ($79,000+ single / $123,000+ married for 2025), traditional IRA contributions are nondeductible. You put after-tax money in, but gains are still taxed as ordinary income at withdrawal. This is the scenario where variable annuities enter the conversation.

| Feature | Nondeductible IRA | Vanguard Variable Annuity | Taxable Brokerage (Index Funds) |

|---|---|---|---|

| Contribution | After-tax | After-tax | After-tax |

| Annual Fee | ~0.10% | ~0.50% | ~0.10% |

| Tax on Gains | Ordinary income | Ordinary income | Long-term capital gains (0%/15%/20%) |

| RMDs Required | Yes (age 73) | No | No |

| Step-Up in Basis at Death | No | No | Yes (heirs get stepped-up basis) |

| Annual Tax Drag | None | None | Yes (dividends, some cap gains) |

The capital gains advantage is decisive. Even with annual tax drag from dividends, a taxable brokerage account with index funds usually wins because:

- Long-term capital gains rates are lower than ordinary income rates

- Index funds generate minimal taxable distributions

- You control when to realize gains

- Heirs get a stepped-up basis at death (eliminating embedded gains)

When Does a Variable Annuity Actually Make Sense?

Rarely. But here are the specific situations where it could work:

1. You’ve Maxed Everything Else and Want RMD Avoidance

If you’ve filled your 401(k), IRA, HSA, and still want tax-deferred growth without RMDs at 73, a variable annuity offers that. The question is whether RMD avoidance is worth the higher fees and ordinary-income taxation.

2. You Need Creditor Protection

Annuities often receive favorable creditor protection under state law. If you’re a physician, business owner, or in a litigation-prone field, this matters. Check your state’s specific protections. Some treat annuities better than taxable accounts.

3. You’re in a High Tax Bracket with a Very Long Horizon

The tax-deferral benefit compounds over time. If you’re in the 35%+ bracket and 30+ years from retirement, the math shifts closer … but still rarely beats a taxable account with tax-efficient index funds.

4. Behavioral Lock-In

The surrender charges (with most providers, not Vanguard) and insurance wrapper make it harder to panic-sell during market crashes. If you know you’re prone to behavioral mistakes, the friction might be worth the cost.

Action steps:

- Calculate your effective tax drag on a taxable index fund portfolio (typically 0.3% – 0.5% annually for high-income investors)

- Compare that to the variable annuity’s extra fees (0.40%+ for Vanguard, 1.5%+ for typical products)

- If the fee difference exceeds your tax drag, skip the annuity

- Check your state’s creditor protection laws for taxable accounts vs. annuities

The Funding Priority Order

For most investors, follow this order:

- 401(k) to employer match – Free money. Always take it.

- HSA (if eligible) – Triple tax advantage.

- Roth or Traditional IRA – $7,000 in low-cost index funds.

- Max out 401(k) – Up to $23,500.

- Taxable brokerage account – Tax-efficient index funds (Total Stock Market, Total International, Tax-Managed funds).

- Variable annuity – Only if you specifically need RMD avoidance or creditor protection, and only the low-cost version (Vanguard).

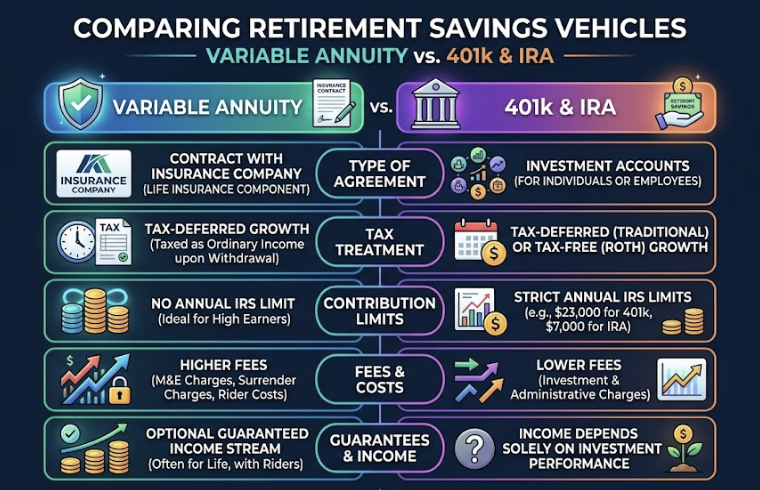

Here is the infographic for comparing variable annuities with 401(k)/IRA:

Vanguard Personal Annuity: The Specifics

If you’re considering a variable annuity despite the cautions above, here’s what Vanguard offers:

Investment Options (More Than Most Small-Business 401(k)s)

- Vanguard Total Stock Market Index

- Vanguard Total Bond Market Index

- Vanguard Total International Stock Index

- Vanguard Wellington (balanced)

- Vanguard Windsor (value)

- Vanguard Primecap

- Vanguard Target Retirement funds (2020-2070)

- Vanguard LifeStrategy funds

- Money market and short-term bond options

Fee Structure

- Mortality & Expense (M&E): ~0.29%

- Administrative: ~0.10%

- Fund expense ratios: 0.04% – 0.14% for index options

- Total: ~0.45% – 0.55% depending on fund mix

No Surrender Charges

You can withdraw anytime without penalties from Vanguard (though the IRS imposes 10% on gains before age 59½). This is a major differentiator from industry-standard products that lock you up for 5-10 years.

The Tax Trap: Ordinary Income vs. Capital Gains

Here’s what many annuity sellers don’t emphasize: all gains in a variable annuity are taxed as ordinary income, even if they came from long-term stock appreciation.

| Account Type | Contribution | Gains Taxed As | Top Federal Rate |

|---|---|---|---|

| Variable Annuity | After-tax | Ordinary income | 37% |

| Taxable Brokerage (LT) | After-tax | Long-term capital gains | 20% (plus 3.8% NIIT) |

The spread is 13.2 percentage points at the top bracket. Over decades, that tax differential compounds powerfully in favor of the taxable account.

Bottom Line

For beginners: Skip variable annuities entirely. Max out your 401(k) and IRA first. If you still have money to invest, open a taxable brokerage account at Vanguard, Fidelity, or Schwab and buy low-cost index funds.

For high earners who’ve maxed out everything: The choice is between a taxable account (taxed at capital gains rates, stepped-up basis at death) and a Vanguard variable annuity (tax-deferred growth, no RMDs, taxed as ordinary income). Run the numbers for your tax bracket and time horizon … but lean toward the taxable account unless you specifically need creditor protection.

Avoid: Any variable annuity with total fees above 0.75%, any product with surrender charges longer than 2 years, and any annuity with income riders or guaranteed benefits you don’t fully understand.

Action steps before buying any variable annuity:

- Confirm you’ve maxed out 401(k) ($23,500) and IRA ($7,000)

- Get the total fee breakdown (M&E + admin + investment expenses)

- Calculate the fee drag vs. tax drag in a taxable account

- Check surrender charges and withdrawal rules

- Verify your state’s creditor protection laws

- Confirm the insurance company’s financial strength rating (A.M. Best, Moody’s)

This article is for educational purposes only. Investment and tax decisions depend on your specific situation. Consult a fee-only financial advisor or tax professional before purchasing annuity products.