![]()

Last Quarter Checklist for 2025

In this issue:

- Latest in Retirement Savings & Personal Finance: All the Glittering Gold, Highest Household Credit Card Debt, More PE Funds Than McDonald’s

- Last Quarter Checklist for 2025

- Tools & Tips: Solo 401(k) Maximum Contribution Calculator

- Market Overview

Latest in Retirement Savings & Personal Finance: All the Glittering Gold, Highest Household Credit Card Debt, More PE Funds Than McDonald’s

All the Glittering Gold

Last week we saw something quite striking. Both gold and silver prices surged to new heights, moving in what felt like a relentless fashion toward their strongest levels in years. Gold has risen roughly 60% year to date, now hovering above 4,300 dollars per ounce. Silver followed closely, up more than 70% for the year, testing the 50-dollar mark and refusing to settle down. The movement has been steady, almost stubborn, as more investors piled in and momentum itself became the story. It is a reminder that once a trend in metals starts to run, it often runs farther than anyone expects.

Many see the rapid rise in gold as a reflection of eroding trust in the US dollar and other paper currencies. With large and structural government debts, ballooning deficits, and a still-closed US government, confidence is fragile. People turn to gold and silver not for quick profit but to preserve what they already have, to protect wealth from inflation and the uncertainty that keeps piling up. When the system feels stretched and promises start to sound hollow, hard assets feel safer. It is not so much greed as it is self-defense.

Even Ray Dalio, founder of the largest hedge fund Bridge Water Associates, has suggested that individuals can consider holding up to around 15 percent of their portfolios in gold, or gold plus bitcoin. The idea is not new but maybe more relevant now than it has been for a long while. Gold is not about timing or excitement, it is about balance. About holding something real when the rest feels a little less so.

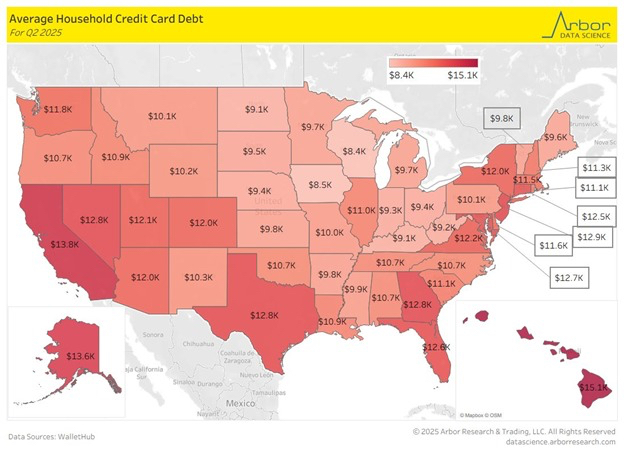

Highest Household Credit Card Debt

If you’re feeling the weight of credit card debt, you’re not alone. In August, US household credit card debt reached an all-time high of $1.33 trillion. The average American household is now carrying $10,668 in credit card balances, a number that keeps climbing higher. This isn’t just a statistic; it’s a real burden affecting millions of families trying to make ends meet.

Where you live can make a big difference in how much debt you’re likely carrying. If you’re in Hawaii, you might be facing the highest average debt at $15,100 per household. California comes in second at $13,800, followed by Alaska at $13,600. New York ($12,900), Texas ($12,800), and Florida ($12,600) also rank among the states with the heaviest credit card burdens. The trend is clear: across the country, credit card debt just keeps growing.

More PE Funds Than McDonald’s

Per Bloomberg: “There are 19,000 private equity funds in the US. There are 14,000 McDonald’s in the US. How are there more private equity funds than McDonald’s? That’s actually crazy, right?” KKR & Co. partner Alisa Wood said on Wednesday at Bloomberg’s Women, Money and Power event in London. It’s the kind of line that makes you pause a bit. Because it sounds like a joke at first, until you realize she’s completely serious. There really are more private equity funds than McDonald’s. Which says something about how much money is sloshing around, how every corner of the market has been financialized, how everyone seems to want a slice of something “alternative.” It also says a lot about how long this cycle of cheap capital and abundant liquidity has lasted.

Her follow-up line hit even closer to home. “Capital coming back is really important. The mark-to-market paper gains only take you so far.” In other words, all those impressive valuations, all that dry powder and unrealized gains sitting on spreadsheets—it only means something when investors actually see cash returned. And right now, many funds are sitting on years of paper profits with few real exits.

Maybe we outght to seriously think about taking some money off the table, especially from the hefty gains in those bubbly AI and other plays? We are not suggesting a wholesale liquidation, just a sensible rebalance!

Last Quarter Checklist for 2025

Speaking of investment portfolio rebalancing, we are now officially in the last quarter of 2025. We create the following checklist for your financial well beings. Many people are busy or lazy to think about these until it’s too late.

– Backdoor Roth:

Verify traditional IRA balances are rolled into a 401(k) before year-end so the pro-rata rule doesn’t dilute your conversion, then execute the nondeductible contribution and Roth conversion while tracking tax basis on Form 8606. Calendar a reminder to send any withholding or estimated tax tied to the conversion before mid-January.

– Tax-Loss Harvesting:

Review high-cost-lot positions for harvesting opportunities, capturing losses to offset 2025 gains while minding the 30-day wash-sale window around replacement securities. Document each trade’s cost basis adjustment so next spring’s Schedule D is clean.

– Portfolio Rebalance:

Compare current weights versus targets after this year’s rally and use new cash, dividends, or strategic sales to restore your risk mix without triggering unnecessary capital gains. Lock in the updated policy statement so you have a compass when volatility returns.

– Holiday Budget:

Map all year-end spending—travel, gifting, entertaining—and cap the total against cash on hand so January’s credit-card bill doesn’t cannibalize 2026 savings plans. Automate transfers into a designated “festive fund” to keep day-to-day cash flow untouched.

– High-Interest Debt Payoff:

Tally credit-card and personal-loan balances, prioritize anything north of single digits, and redirect windfalls or bonus income to clear them before rate resets hit. Ask lenders for hardship or lower-rate options now rather than after a payment slips.

– Required Minimum Distributions:

Confirm RMD amounts for IRAs and employer plans, including inherited accounts, and schedule withdrawals or qualified charitable distributions ahead of December 31 to avoid the 25% excise penalty. Coordinate with taxes so withholding covers fourth-quarter liabilities.

– Health Benefits Tune-Up:

Use open enrollment to evaluate 2026 medical, dental, and vision coverage, update dependents, and confirm FSA deferrals will be spent before the plan deadline. Maximize HSA contributions if you’re HDHP-eligible—every dollar added before April 15 still counts for 2025.

– Charitable Giving Strategy:

Decide whether to bunch deductions, gift appreciated securities, or fund a donor-advised account while markets are high, and obtain written acknowledgments for gifts above IRS thresholds. If you’re 70½ or older, coordinate QCDs with your RMD to double-count the benefit.

– Estimated Tax Checkup:

Run a quick projection using pay stubs, investment income, and side-hustle receipts to ensure safe-harbor coverage on Form 1040-ES payments. Adjust December payroll withholding or January estimates if capital-gains distributions or Roth conversions tip the scale.

– Insurance and Estate Review:

Confirm life, disability, homeowners, and umbrella limits still match assets and obligations, then check beneficiaries, POAs, and wills for births, deaths, marriages, or new states of residence. Store updated documents where your executor and financial team can find them.

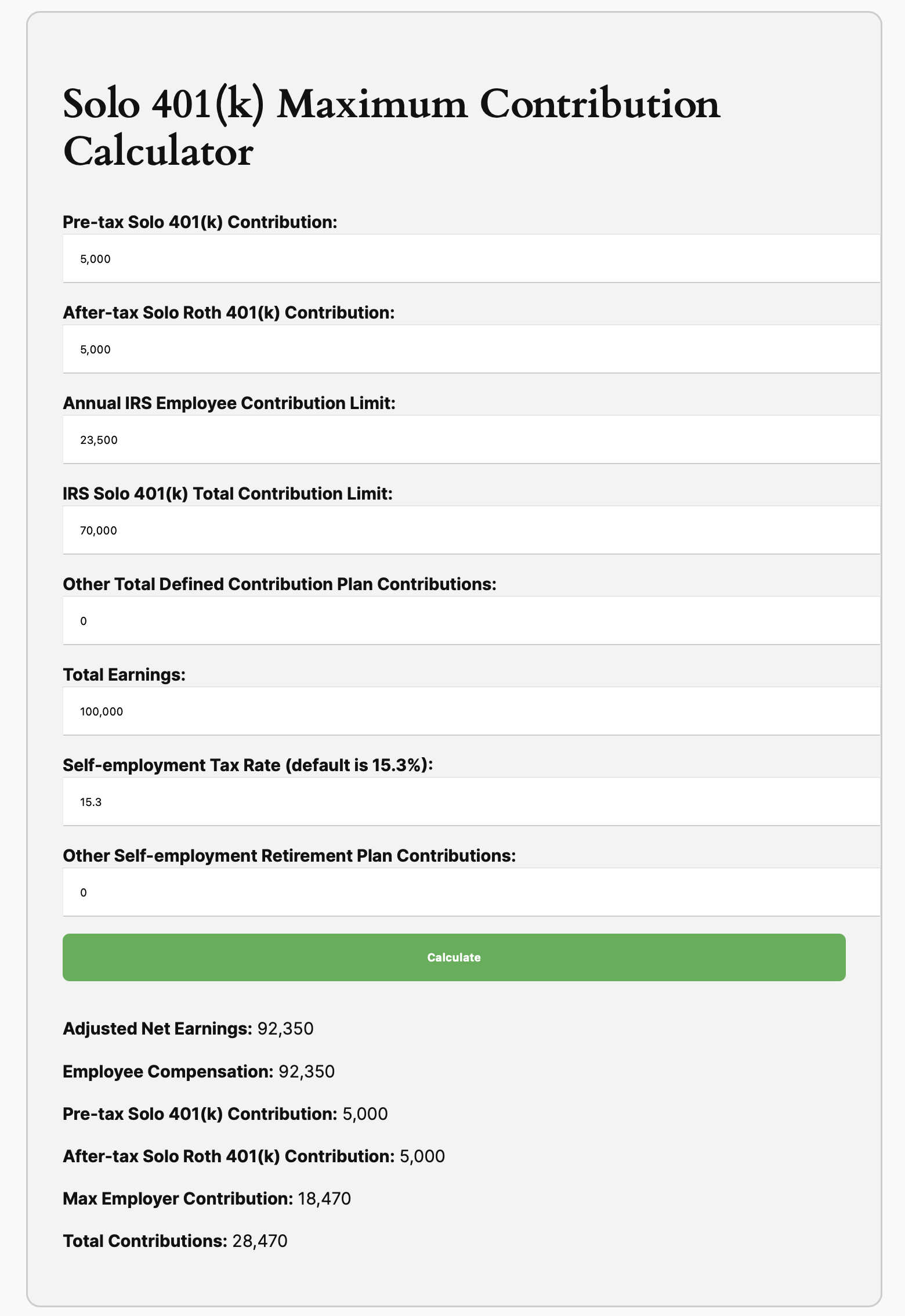

Tools & Tips: Solo 401(k) Maximum Contribution Calculator

Well, as a sole proprietor or contractor, you actually can have a better chance to make most of the tax deferred benefits in so called Solo 401(k). You can setup solo 401(k) account in brokerages like Schwab and Fidelity free of charge. In the following, we present Solo 401(k) Maximum Contribution Calculator.

The inputs and outputs:

A few notes:

- The most common mistake is misunderstanding that the employer contribution amount in Solo 401(k) contribution limit is up to 20% of adjusted net earnings, not 25% as stated in the usual IRS instructions. This is because, in the IRS instructions, adjusted net earnings must first subtract the employer contribution before applying the 25%. When solved algebraically, this results in a 20% effective rate instead of 25%.

- Employer’s contribution is also your own contribution as you are your own employer. That’s the power of solo 401(k) here.

Well, again, we urge those who are self-employed to review your tax deferred savings now as it fast approaching the end of the year.

Market Overview

Last week, stocks recovered from the previous week’s losses and are once again hovering near all-time highs. Investors seemed to shrug off the government shutdown and the absence of key economic reports such as CPI. Actually, they don’t mind flying blindly without macro economic data for a while! Overall, the financial markets remain bullish.

The following table shows the major asset price returns and their trend scores, as of this Monday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 1.2% | 0.7% | 7.1% | 31.3% | 16.4% | 11.3% |

| Foreign Stocks | 2.1% | 1.9% | 8.2% | 23.5% | 21.9% | 11.5% |

| US REITs | 3.8% | 1.4% | 3.0% | 10.3% | 0.1% | 3.7% |

| Emerging Market Stocks | 1.5% | 1.6% | 8.8% | 27.1% | 18.6% | 11.5% |

| Bonds | 0.4% | 1.2% | 3.6% | 5.7% | 6.1% | 3.4% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

|