Gone Fishin' Lazy Portfolio Compared with Tactical Asset Allocation

10/08/2010

Alexander Green proposed this

The Gone Fishin' Portfolio which was outlined in his book '

The Gone Fishin' Portfolio'. Based on the book, the following is the allocation using Vanguard low cost index funds (in the Bogleheads forum, there is a discussion

thread devoted to this portfolio):

- Total Stock Market Index (VTSMX) - 15% VTI

- Small-Cap Index (NAESX) - 15% VB

- European Stock Index (VEURX) - 10% VEA

- Pacific Stock Index (VPACX) - 10% VEA

- Emerging Markets Index (VEIEX) - 10% VWO

- Short-term Bond Index (VFSTX) - 10% SHY

- High-Yield Corporates Fund (VWEHX) - 10% HYG

- Inflation-Protected Securities Fund (VIPSX) - 10% TIPS

- REIT Index (VGSIX) - 5% RWX

- Precious Metals Fund (VGPMX) - 5% GLD

The asset classes represented and their weights are

- US Equity 30%

- International equity 20%

- Emerging markets 10%

- REIT 5%

- Commodities 5%

- Fixed income 30%

This portfolio has six asset classes which is good – it should have good performance. It is overweighted in US equity and underweighted in commodities and real estate. This probably will put its performance closer to four or five asset portfolios.

With 30% of the assets in fixed income and with 10% of that in high yield corporate funds, this would be an aggressive portfolio.

We will compare this lazy portfolio with strategic and tactical asset allocation of the same asset base. We will also compare the results with a six asset SIB that has been discussed in a previous article. Intuitively we would expect the six asset class SIB to outperform the Gone Fishin’ portfolio.

The original lazy portfolio performs as well as strategic asset allocation that is rebalanced monthly using the funds as stated. If you are looking for a lazy portfolio, 5% over five years is reasonable

The six asset class strategic asset allocation has higher performance based on more balanced portfolio

Both tactical asset allocation portfolios outperform buy and hold consistently – the six asset SIB coming top of the performance table.

There is a 7% gap between the strategic and tactical asset allocation portfolios and a 10% difference between the tactical and strategic asset allocation on the SIBs. This would suggest that moving to tactical asset allocation will have a significant long term payoff

Takeaways

- Tactical Asset Allocation reduces downside risk and that wins in the current uncertain environment

- The Gone Fishin’ lazy portfolio has satisfactory returns but can be beaten

- ETF’s can readily be used to implement these portfolios with good performance

labels:

investment,

Symbols,

ACWI,

ACWX,

ADRE,

AGG,

BIV,

BLV,

BND,

BSV,

BWX,

CFT,

CIU,

CSJ,

DBC,

DBV,

DIA,

DVY,

EDV,

EEM,

EFA,

EFG,

EFV,

EMB,

ETF,

GLD,

GOOG,

GSG,

GXC,

HPQ,

HYG,

ICF,

IEF,

IEI,

IFGL,

IGOV,

IGR,

IJH,

IJJ,

IJK,

IJR,

IJS,

IJT,

IVE,

IVV,

IVW,

IWB,

IWC,

IWD,

IWF,

IWM,

IWN,

Portfolio-Building,

with,

ETFs,

Closed-End,

Funds,

Commodity,

ETFs,

Currency,

ETFs,

Developed,

Market,

ETFs,

comments(0)

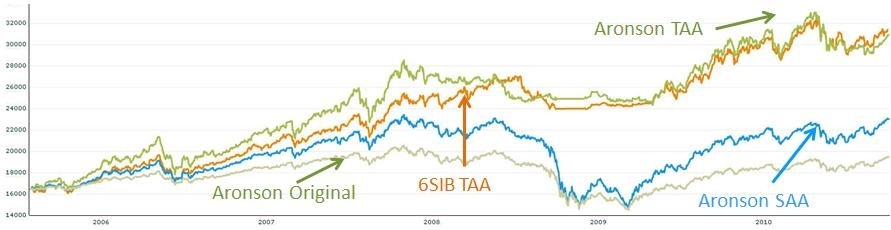

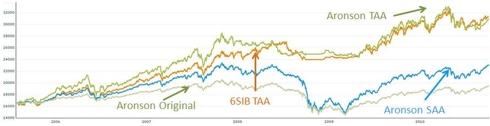

Aronson Family Portfolio Reviewed and Compared

10/08/2010

Ted Aronson and his AJO Partners manage about $25 billion of institutional assets. Aronson puts his family's taxable money in this well-diversified portfolio of no-load index funds.

| Fund |

Weight |

Ticker |

ETF |

| US Equities |

40% |

VFINX, VEXMX, VISGX, VTSMX, VISXX |

VTI, TMW, VBK, VBR |

| International Equity |

20% |

VPACX, VEURX |

VEA |

| Emerging Markets |

10% |

VEIEX |

EEM |

| US Bonds |

30% |

VIPSX, VUSTX, VWEHX |

TIP, LQD, HYG |

This is a well diversified four asset class portfolio with an aggressive profile. The US equities are broadly diversified. Asia Pacific is put above Europe for developed markets. There is a diversified set of fixed income with VWEHX and VUSTX being relatively high risk. The long term treasury bond has proved to be a good diversifier in recent history.

The US component is possibly over-weighted and emerging markets could be increased or, even better, some real estate assets could be added.

This lazy portfolio will be compared with the same funds with a balanced (i.e. all equity asset classes equally weighted) buy and hold with monthly rebalancing and the ability to rotate styles within the asset classes. This will look at what difference alternative fund balances contribute to the results. We will look at a Six asset class portfolio with Strategic Asset Allocation that will shed light on the benefits of extra asset classes.

Then we will compare the impact of tactical asset allocation on the Aronson funds and also a six asset class SIB to examine the returns delivered by a TAA strategy applied to Aronson and broader funds.

The original lazy portfolio performs in a satisfactory manner. The 1 year returns top the table but that is coming from the worst three and five year results. The balanced buy and hold gives better long term results and six asset class SIB has even better results. This is expected as diversification normally beats more funds in fewer asset classes.

Tactical asset allocation delivers the best results and, again, more diversification beats more funds in fewer asset classes.

The tradeoff is being involved monthly with your portfolio to squeeze out better returns compared to an annual review; once a month seems a reasonable level of effort to put extra money in your pocket. The spread of 5 year returns is around 11% which is significant in terms of having a bigger nest egg.

Takeaways

- Tactical Asset Allocation reduces downside risk and that wins in the current uncertain environment

- The Aronson lazy portfolio has satisfactory returns but can be beaten

- ETF’s can readily be used to implement these portfolios with good performance

- A 11% spread means that it’s worth looking at alternatives

labels:

investment,

Symbols,

VTSMX,

VTI,

TMW,

VBK,

VBR,

VEA,

EEM,

TIP,

LQD,

HYG,

Aronson,

Lazy,

portfolio,

investing,

portfolio,

building,

comments(0)

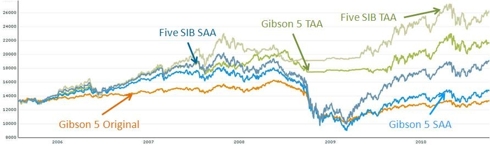

Gibson's 5 Lazy Portfolio Returns Measured and Compared

10/08/2010

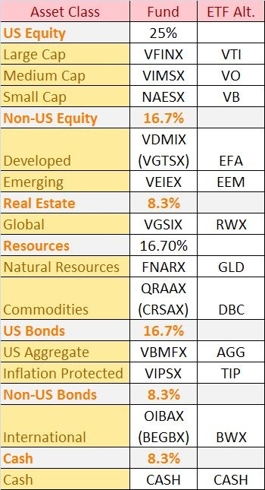

Gibson's 5 Equal Asset Allocation Strategy comes from Roger Gibson’s widely read "Asset Allocation: Balancing Financial Risks." In it, Gibson outlined a simple yet diversified asset allocation model: putting equal amount of investment into 5 asset classes: US Equity, International Equity, REIT, Commodity, Fixed Income. For Fixed Income, he further outlined a 70%/30% US domestic/international bond investment.

The most noticeable feature in this model portfolio is its heavy weight into commodity asset class.

Recent studies suggest that managed futures in commodity could be an excellent diversifier with equity like positive returns. The recent representative study is a research paper by Yale Professors.

| Fund |

Weight |

Ticker |

ETF |

| US Equity |

20% |

VFINX |

VTI |

| International Equity |

20% |

VDMIX |

EFA |

| Real Estate |

20% |

VGSIX |

RWX |

| Commodity |

20% |

CRSAX |

DBC |

| US Bonds |

14% |

VBMFX |

AGG |

| International Bonds |

6% |

OIBAX |

BWX |

This is a well diversified four asset class portfolio with an aggressive profile. It is a little unusual to have commodities as an asset class before emerging markets,

This lazy portfolio will be compared with the same funds with a balanced (i.e. all equity asset classes equally weighted) buy and hold with monthly rebalancing and the ability to rotate styles within the asset classes. This will look at what difference alternative fund balances contribute to the results. We will look at a Five asset class SIB with Strategic Asset Allocation that will shed light on the benefits of extra asset classes.

Then we will compare the impact of tactical asset allocation on the Aronson funds and also a five asset class SIB to examine the returns delivered by a TAA strategy applied to Aronson and broader funds.

We would expect the performance of this portfolio to match the 5 asset SIB reasonably closely as they have the same weights.

Notable elements of the results

The original lazy portfolio has relatively low volatility but the returns are disappointing. Using the same funds with a more traditional spread gives a better return. This is one data point that balanced assets make a better portfolio. The five asset class SIB has even better results. The five asset SIB has emerging markets rather than commodities which has been a better selection in recent history. From previous articles a six asset SIB will also have good returns and that includes both emerging markets and commodities.

Tactical asset allocation delivers the best results and, again, the asset class selection of the SIB beats the Gibson choice (and again the six SIB which combines both is even better).

The tradeoff is being involved monthly with your portfolio to squeeze out better returns compared to an annual review; once a month seems a reasonable level of effort to put extra money in your pocket. The spread of 5 year returns is around 14% which is significant in terms of having a bigger nest egg.

Takeaways

- Tactical Asset Allocation reduces downside risk and that wins in the current uncertain environment

- The Gibson five lazy portfolio has returns that can be improved upon

- ETF’s can readily be used to implement these portfolios with good performance

- A 14% spread means that it’s worth looking at alternatives

labels:

investment,

Symbols,

ACWI,

ACWX,

ADRE,

AGG,

BIV,

BLV,

BND,

BSV,

BWX,

CFT,

CIU,

CSJ,

DBC,

DBV,

DIA,

DVY,

EDV,

EEM,

EFA,

EFG,

EFV,

EMB,

ETF,

GLD,

GOOG,

GSG,

GXC,

HPQ,

HYG,

ICF,

IEF,

IEI,

IFGL,

IGOV,

IGR,

IJH,

IJJ,

IJK,

IJR,

IJS,

IJT,

IVE,

IVV,

IVW,

IWB,

IWC,

IWD,

IWF,

IWM,

IWN,

Portfolio-Building,

with,

ETFs,

Closed-End,

Funds,

Commodity,

ETFs,

Currency,

ETFs,

Developed,

Market,

ETFs,

comments(0)

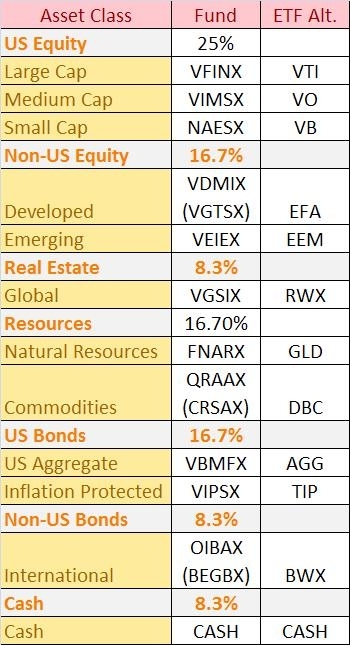

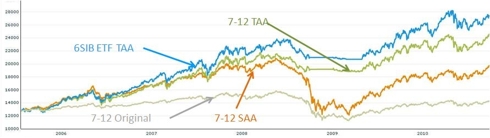

Israelsen Seven Twelve Portfolio

10/08/2010

Craig L. Israelsen, Ph.D., is an Associate Professor at Brigham Young University in Provo, Utah where he teaches Personal and Family Finance to over 1,200 students each year. The Israelsen Seven Equally Weighted is aimed to protect the portfolio against losses.

The portfolio has seven different asset classes and twelve different funds. Each fund has the same weight 8.3% so each asset class has a different weighting. The table below provides the weightings for each asset class, the funds that will be used to review performance and the ETF equivalent.

The highly diversified portfolio with low aggregate correlation avoids losses effectively, reducing the standard deviation of return, maximum portfolio drawdown in any single year and frequency of losses.

The original portfolio calls for annual rebalancing. The historical returns will be compared with three similar portfolios

- The same portfolio with tactical asset management

- The same portfolio with monthly strategic asset management with the ability to shift funds in each class

- A six asset ETF portfolio with tactical asset management

With a well diversified non correlated portfolio, we expect to see good returns with low volatility from the original portfolio. The low volatility is certainly delivered but the returns are lower than would be hoped. The strategic asset allocation has a rich set of funds and while the overall asset class weights remain constant, the ability to move weights in the styles shows significant benefits at the cost of some volatility.

The tactical asset allocation portfolios fare better. As in a previous article where the lighter 6SIB outperformed a rich set of funds, the movement towards reducing risk curtailed returns while reducing volatility

Takeaways

- Having a well diversified non correlated set of funds is key to good returns with low risk

- Tactical Asset Allocation reduces downside risk and that wins in the current uncertain environment

- ETF’s perform very well against any other portfolio with the benefits of low cost and flexibility

labels:

investment,

Symbols,

ACWI,

ACWX,

ADRE,

AGG,

BIV,

BLV,

BND,

BSV,

BWX,

CFT,

CIU,

CSJ,

DBC,

DBV,

DIA,

DVY,

EDV,

EEM,

EFA,

EFG,

EFV,

EMB,

ETF,

GLD,

GOOG,

GSG,

GXC,

HPQ,

HYG,

ICF,

IEF,

IEI,

IFGL,

IGOV,

IGR,

IJH,

IJJ,

IJK,

IJR,

IJS,

IJT,

IVE,

IVV,

IVW,

IWB,

IWC,

IWD,

IWF,

IWM,

IWN,

Portfolio-Building,

with,

ETFs,

Closed-End,

Funds,

Commodity,

ETFs,

Currency,

ETFs,

Developed,

Market,

ETFs,

comments(0)

Bernstein's No Brainer and Smart Money Portfolios Reviewed

10/08/2010

Dr. William Bernstein is the author of the "Intelligent Asset Allocator" and "The Four Pillars of Investing." He's also a physician, neurologist and financial adviser to high-net-worth individuals.

He has proposed a number of lazy portfolios. There are two that will be examined today.

The no-brainer portfolio comprises the following fund allocation

- 25% in Vanguard 500 Index VFINX (IVW)

- 25% in Vanguard Small Cap NAESX or VTMSX (VB)

- 25% in Vanguard Total International VGTSX or VTMGX (EFA, VEA)

- 25% in Vanguard Total Bond VBMFX or VBISX (BND)

Things to note about the portfolio:

- Heavily weighted towards domestic equities

- Similar to a three asset SIB with domestic, international and fixed income

- It would be better to have some REIT or emerging markets exposure

- We will compare the no brainer portfolio to a three and four asset SIB

The Bernstein no-brainer tracks very closely with the four asset SIB. It’s interesting to note that the three asset Bernstein tracks closer to the four asset SIB than expected. So as a lazy portfolio, it performs satisfactorily. Year to date, however, the four asset SIB has better performance.

The tactical asset allocation strategies deliver better results with higher returns and lower volatility. The no brainer funds outperform the 3 asset SIB but underperform the 4 asset SIB which is to be expected.

The smart money portfolio comprises the following fund allocation

- 40% Vanguard Short Term Investment Grade VFSTX (SCJ, SHY)

- 15% Vanguard Total Stock Market VTSMX (VTI)

- 10% Vanguard Small Cap Value VISVX (VBR)

- 10% Vanguard Value Index VIVAX (VTV)

- 5% Vanguard Emerging Markets Stock VEIEX (VWO)

- 5% Vanguard European Stock VEURX (VEU)

- 5% Vanguard Pacific Stock VPACX (VPL)

- 5% Vanguard REIT Index VGSIX (RWX, VNQ)

- 5% Vanguard Small Cap Value NAESX or VTMSX (VB)

To summarize:

- 40% in US equities

- 10% in international equities

- 5% in emerging market equities

- 5% in REIT

- 40% in fixed income

Although the smart money portfolio has five asset classes, international, emerging markets and real estate are so under-weighted that they act as if they are a single class so, again, it’s more like a three asset class portfolio. The five asset SIB with strategic asset allocation has similar behavioral properties but clearly delivers better results based on superior diversification.

One the strategy is moved over to tactical asset allocation, there are enough asset classes in the Bernstein portfolio for the

Larger Chartresults to be clearly superior than a four asset SIB and close to the five asset SIB

We look at the two portfolios as a final comparison

They are remarkably close to each other full comparison

Takeaways

- Tactical Asset Allocation reduces downside risk and that wins in the current uncertain environment

- Both Bernstein portfolios perform satisfactorily for a lazy portfolio – it is surprising that the no-brainer performs so well against it’s more diversified smart-money cousin

- ETF’s can readily be used to implement these portfolios with good performance

labels:investment,

Symbols:BND,BWX,CIU,CSJ,DBC,DVY,EFA,EFG,EFV,EMB,GLD,HYG,IEF,IEI,IJJ,IJK,LQD,MBB,QQQQ,RWX,SCZ,SHY,TIP,VB,VBK,VBR,VEA,VNQ,VO,VTI,VTV,VUG,VWO,WIP,Portfolio-Building,with,ETFs,Closed-End,Funds,Commodity,ETFs,Currency,ETFs,Developed,Market,ETFs,

comments(0)

Diversification, Style AND Asset Rotation Improve Portfolio Performance without Incurring Extra Risk

10/08/2010

Three Asset Class Lazy Portfolios Reviewed

09/29/2010

Diversification and Style Rotation Improve Portfolio Performance without Incurring Extra Risk

09/29/2010

Stan Druckenmiller is Leaving

09/28/2010

Google’s 401K Plan: Another Good Employee Benefit

09/26/2010

Is Free 401(k) Advice Worth the Money?

09/25/2010

Armstrong Index Based Lazy Portfolio Returns Study

09/17/2010

Getting Most out of Your Retirement Plan: A Case Study on Hewlett Packard 401K Plan

09/16/2010

How Does Your Garden Grow?

09/16/2010

Is Following the Fed Smart?

09/16/2010

John Wasik’s Nano Portfolio Performance Scrutinized

09/14/2010

To Roth or Not to Roth

09/11/2010

Americans in their 50s especially hard-hit by recession

09/10/2010

The Economy is in a Modern Day Depression

09/09/2010

Gen Y Must Take Control of Financial Future

09/09/2010

First

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

Last