Stocks for The Long Term: Why They Outperform Bonds

In this issue:

- Retirement savings: what Morningstar retirement model reveals

- Stocks for the long-term: why they outperform bonds

- Investment arithmetic: investment calculator

- The billion-dollar employer contribution club

- Market overview: post-election stock rally, inflation …

Older generations are more prone to retirement income shortfall

Based on Morningstar’s 2024 retirement model for U.S. retirement outcomes, we find the following:

- Older generations are more likely to experience retirement income shortfalls: 52% of Baby Boomers and 47% of Gen X face potential gaps. A likely cause is the shift from defined-benefit pensions to defined-contribution plans like 401(k)s and 403(b)s, which left these generations with less time to save.

- Nearly 54% of U.S. households could face retirement shortfalls if they retire at 62, compared with 45% if they retire at 65. This risk further improves with later retirement ages, dropping to 38% at age 67 and 28% at age 70.

- Disparities in socioeconomic status and gender also reveal varied retirement savings shortfalls.

Key takeaways: models are saying obvious things, Save more and start saving early. Consider working longer and retiring later. Furthermore, could we ask companies to do more to support lower-paid workers by enhancing retirement matching?

Stocks for the long-term: why they outperform bonds

When you start on your retirement savings and investing, you should focus on the long-term. This is especially true for young professionals. Often many retirement 401(k) plans provide investment options that include stock and bond funds. For many, why stocks can provide better long-term returns than bonds is still a puzzle. We try to answer this in the following:

1. Long-term data shows stocks outperforming bonds

Historical data dating back to 1871, like that from the Nobel laureate economist Robert Shiller, highlights a clear pattern: stocks consistently deliver higher returns than bonds over the long run. For the past 150 years, this trend has held up through various market cycles, recessions, and economic changes, underscoring the growth potential of stocks for long-term investors. For retirement savers, this long-term data is crucial—it shows that while stocks may be volatile in the short term, they’ve provided strong returns across many decades.

Here are some numbers from our newsletter 150+ Years of Long-Term Earnings and Stock Returns of the ‘Conglomerate’ of Collective S&P 500 Index Companies:

- A dollar invested in 1871, after 153 years, has grown to be roughly equivalent to $28,800 in 1871 dollars (28,800 times the original amount) or about $736,000 in today’s dollars—an annual growth rate of approximately 6.9%. This is known as the “real return,” which is the return after adjusting for inflation and reflects how well your purchasing power has been preserved and increased over time.

- Alternatively, if you started investing $1 in 1974, it would have grown to $36 in 1974 dollars or $100 in today’s dollars over the past 50 years. So if a young professional had started investing at age 22, their investment would have grown 100-fold over 50 years, when they reach age 72 now!

Here is the table that compares annualized returns between stocks and bonds

| Nominal Annual Return | Real Annual Return | |

| Stocks | 9.3% | 7% |

| 10-Year Treasury Bonds | 4.5% | 2.3% |

2. Stocks offer ‘risk premium’ over bonds

In any market, stocks are riskier than bonds because companies face competition, changing economic conditions, and the pressures of running a business. But that extra risk also comes with a reward called the “risk premium.” This means that, in exchange for accepting more ups and downs, stock investors are rewarded with the potential for higher returns. In a fair market, strong companies stay competitive, grow profits, and ultimately deliver better returns than safer, low-risk bonds. Over time, if returns aren’t high enough, compared with safer fixed-income bonds, many companies will exit while the remaining companies become more profitable. This profit potential brings new businesses back into the market, creating a cycle that should sustain the “risk premium” and keep stock returns attractive in the long term.

3. A fair and transparent market ensures the stock growth

Stock markets in democratic countries, particularly in Western nations like the United States and Europe, are generally considered fair, transparent, and protected by laws that prevent excessive manipulation. This regulatory environment fosters confidence in equity investments and supports the notion of a fair market, where companies can compete on a level playing field, thereby encouraging capital flows into businesses rather than just safe bonds. A fair and stable market system allows the risk premium to be sustained, reinforcing the long-term trend of stocks outperforming bonds. However, in countries where markets may be heavily influenced by government policies or lack transparency, this dynamic can break down, making bond investments more attractive.

4. Broad stock indexes filter out weak businesses

Investing in broad stock indexes like the S&P 500 or MSCI provides added security through a rigorous selection process that includes only the most financially sound companies. These indexes filter out weaker businesses and ensure that only strong, well-performing companies make the cut. Since many retirement plans offer diversified stock index funds, such as the Vanguard Total Stock Market Index Fund, investors in these funds are positioned to benefit from long-term market growth.

What this means for retirement investors

For retirement savers, the right mix of investments is essential. Bonds can provide stability, which is valuable for income and steady returns. But bonds alone may fall short when it comes to beating inflation or reaching ambitious retirement goals. Stocks, with their historical growth, offer the potential for substantial wealth-building over time. Adding a broad-based stock index to your retirement portfolio can give you exposure to this long-term growth while spreading risk across many companies. Diversified stock index funds should be considered a core component of most retirement savers’ portfolios.

Tools & Tips: Investment Arithmetic & Investment Calculator

Some simple yet useful investment arithmetics (see this and this):

- Rule of 72: to roughly double your money, it will take 72/percentage of growth number of periods. For example, if the investment grows at 10% per year, it would take 72/10=7.2 years to double the money. That would mean in 42 years, at 10% return, you would roughly accumulate 42/7.2=6 or 2^6 (2 to power 6) = 64 times money.

- A 50% loss requires 100% gain to just break even:

The asymmetric nature of loss and gain arithmetic is well-published. The following table shows how the arithmetic is heavily tilted to loss percentages:

Loss Gain needed to break even -10% 11.1% -20% 25.0% -30% 42.9% -40% 66.7% -50% 100.0% -60% 150.0%

So avoiding significant losses is crucial!

You can just simply use our Investment Calculator to play with various return/compounding numbers.

The billion-dollar employer contribution club

The following are the US employers that contributed more than a billion US dollars for their employee 401k(k) plan match:

- Walmart 401(k): $1.48 billion in employer contributions

- Boeing 401(k): $1.4 billion in employer contributions

- Bank of America 401(k): $1.2 billion in employer contributions

- National Electrical Annuity Plan: $1.1 billion in employer contributions

- Google 401(k): $1.07 billion in employer contributions

- Wells Fargo 401(k): $1.02 billion in employer contributions

- Microsoft 401(k): $1 billion in employer contributions

Considering that only about 5,000 of the 18 million U.S. businesses generated $1 billion or more in revenue (not profit) in 2023, the $1 billion these companies collectively spend on matching contributions for employee retirement plans is staggering. It’s also worth noting that tech giants like Google and Microsoft have relatively fewer employees compared to other companies on this list, as a result, their per-employee matches are significantly higher. To see how matching contributions vary per employee, you can explore the individual retirement plans linked above for a closer comparison.

Market Overview

The following table shows the major asset price returns, post the US election:

| Asset Class | 1 Week | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 4.7% | 3.2% | 12.5% | 15.5% | 37.5% | 14.7% |

| Foreign Stocks | 0.4% | -3.0% | 4.3% | 3.1% | 19.6% | 4.9% |

| US REITs | 3.0% | 1.2% | 6.1% | 18.1% | 32.0% | 12.1% |

| Emerging Market Stocks | 0.9% | -2.3% | 7.8% | 8.7% | 22.6% | 7.6% |

| Bonds | 0.7% | -0.6% | -0.1% | 4.2% | 8.6% | 2.6% |

Following the election, U.S. stocks surged, while long-term bonds initially weakened. However, after the Federal Reserve cut interest rates by a quarter point (0.25%) on Thursday, bonds showed some recovery.

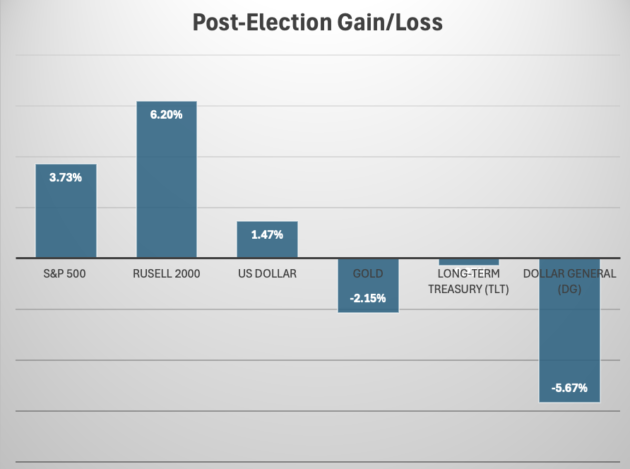

Another notable signal: the U.S. dollar strengthened (+1.47%), while gold weakened (-2.15%). This movement suggests that investors anticipate rising federal deficits and inflation as a result of potential tax cuts and increased tariffs on foreign goods (especially from China) under the new administration. Additionally, Dollar General’s stock price, along with other discount retailers like Dollar Tree, declined sharply, hinting that the cost of low-priced goods may increase. This trend could pose challenges for low-income and rural communities, where access to affordable goods is crucial.

We also observed a sharp rise in U.S. small-cap stocks (Russell 2000 +6.2%), suggesting investors’ optimism that the new administration will strengthen the domestic economy through tax cuts, increased tariffs on foreign goods, and potentially even stimulus measures.

We certainly live in an interesting time.

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?