Roth IRA for Kids? SEP IRA for Rental Income?

In this issue:

- News & Tips You Can Use: 5 Tax Tips For Tax Filing Season

- 6 Ways to Cope in Your Retirement Savings & Spending Under the Current DOGE, Tariff Regime

- Backdoor Roth IRA Pro-Rata Conversion Calculator

- Market Overview

Latest in Retirement Savings & Personal Finance: 5 Tax Tips For Tax Filing Season

The following 5 tax tips could be timely for the tax filing season:

- Child Tax Credit: This tax season, the Child Tax Credit (CTC) remains a valuable benefit for families. For 2024 taxes filed in 2025, the credit is worth up to $2,000 for each qualifying dependent child. Additionally, the Additional Child Tax Credit (ACTC) has increased to $1,700 per qualifying child for 2025. Be sure to check if you qualify based on your income and family situation to maximize this credit.

- 1099-K Higher Limit: There’s important news regarding the 1099-K reporting threshold. For the 2025 tax year, the reporting threshold for third-party settlement organizations (TPSOs) has been set at $2,500, offering relief to taxpayers who would face more reporting obligations under a lower threshold. By 2026, this limit will decrease further back to $600, so it’s wise to prepare for these changes in advance.

- Inflation Adjustment for Standard Deduction: Thanks to inflation adjustments, taxpayers can benefit from an increased standard deduction for the 2025 tax year. Single taxpayers and those married filing separately will see their standard deduction rise to $15,000, up by $400. Heads of household will have a standard deduction of $22,500, up from $21,900. These increases can help reduce taxable income, potentially lowering your overall tax bill.

- Extended Deadlines for Several States: Due to the devastating wildfires in southern California, both federal and state authorities have extended tax filing and payment deadlines. Residents and businesses in affected areas now have until October 15, 2025, to file their 2024 California tax returns and make any tax payments that would have been due between January 7, 2025, and October 15, 2025. This extension applies to various individual and business tax returns and payments, providing much-needed relief during recovery efforts.

- Free Tax Filing with Limitations: Many taxpayers can take advantage of free tax filing services offered by the IRS and several states, including California’s CalFile program. These services are designed to simplify the filing process for eligible individuals, helping them avoid costly preparation fees. The IRS Free File program is available to taxpayers with an adjusted gross income of $79,000 or less, while CalFile offers free e-filing for California residents who meet specific criteria. Make sure to review the specific criteria for these free filing options to determine if you qualify, keeping in mind any limitations that may apply.

Roth IRA for Kids? SEP IRA for Rental Income?

We’ve heard various suggestions and discussions on the importance of starting savings early. One idea that stands out is opening a Roth IRA for your kids. It may seem unconventional, but it’s at least worth considering as a potential long-term strategy!

Start Early: Roth IRA for Kids

A Roth IRA can be a powerful tool for kids with earned income, allowing decades of tax-free growth. Even young children can qualify if they earn taxable income, such as from babysitting, dog walking, or working in a family business. Parents can also match contributions as long as they don’t exceed the child’s earned income or the annual limit ($7,000 in 2024 and 2025).

Examples:

- A child earning $2,000 babysitting can contribute up to $2,000 to a Roth IRA.

- A young actor earning income from a commercial can have that money contributed to a Roth IRA.

- Contributions as small as $1,000 annually from ages 7–14 could grow to over $160,000 by age 60 (assuming a 7% return). Adding $7,000/year from age 15 onward could result in over $2.5 million by retirement. Use Investment Calculator to play around.

Roth IRAs are flexible: contributions can be withdrawn anytime without penalties, and earnings can be used for education or a first home purchase after five years.

Rental Income and SEP IRA Eligibility: Material Participation Explained

Many people have had extra rental properties that earn them rental income. Rental income is generally considered passive and doesn’t qualify as earned income for SEP IRA contributions. However, if you materially participate in managing your rental properties, the income may qualify as non-passive and allow SEP IRA deductions. Of course, the SEP IRA annual deductions is $70,000 in 2025, ($69,000 for 2024), which is very generous.

Material Participation Tests (IRS Guidelines): To qualify, you must meet at least one of these tests:

- 500-Hour Test: Spend more than 500 hours annually on activities like property maintenance, tenant management, or bookkeeping.

- Substantial Activity Test: Regularly perform significant management tasks (e.g., advertising vacancies or negotiating leases).

- Greater Participation Test: Spend more than 100 hours annually and more time than any other individual involved.

- Significant Participation Test (SPA): Combine hours across multiple rental properties to meet a threshold of 500 hours.

Examples of qualifying activities:

- Screening tenants and negotiating leases.

- Managing finances, such as collecting rent or paying bills.

- Advertising vacancies through platforms or local listings.

- Performing repairs or overseeing contractors.

- Record-Keeping Tip: Maintain detailed logs of hours worked and tasks performed (e.g., calendars or summaries) to substantiate your participation with the IRS.

Consult a tax professional to assess your eligibility.

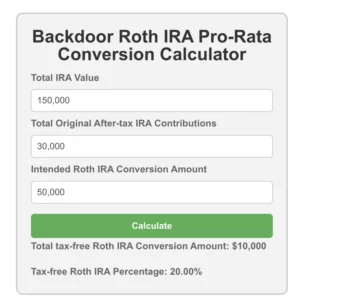

Tools & Tips: Backdoor Roth IRA Pro-Rata Conversion Calculator

When it comes to retirement planning, many people are familiar with the Roth IRA’s benefits, including tax-free growth and tax-free withdrawals in retirement. However, for individuals who have both pre-tax and after-tax (also called non-deductible) contributions in their IRA accounts, converting funds to a Roth IRA can be more complicated. There is this peculiar pro-rata rule that states that, if your IRA contains both pre-tax and after-tax contributions, the IRS will treat all funds in all of your IRA accounts as one pool. This means that when you convert part of your IRA to a Roth IRA, the amount that is converted will consist of both pre-tax and after-tax funds, according to their proportion in the total IRA balance. Basically, the IRS doesn’t want you to be able to designate your conversion from all of the after-tax contributions if you have pre-tax IRA contributions. Remember, when you convert from a pre-tax contribution, you’ll need to pay income tax.

Example

Let’s consider a practical example. Suppose you have:

- Total IRA Value: $150,000 (including both pre-tax and after-tax funds)

- After-Tax Contributions: $30,000

- Intended Roth IRA Conversion: $50,000

The pro-rata rule states that the tax-free portion of your conversion will be calculated based on the proportion of after-tax funds in your total IRA balance. In this case, 20% of your IRA balance is after-tax contributions ($30,000 ÷ $150,000).

So, when you convert $50,000 to a Roth IRA, 20% of the conversion ($10,000) will be tax-free, and the remaining 80% ($40,000) will be taxable. You still have $20,000 in after-tax contributions left, unconverted, after deducting the $10,000. Unfortunately, you can’t just simply first use all of $30,000 after-tax contribution as part of the Roth conversion. In fact, in this case, you can only convert $10,000!

The Backdoor Roth IRA Pro-Rata Conversion Calculator helps you determine the tax-free portion of your Roth IRA conversion based on the pro-rata rule. By entering the total value of your IRA, your original after-tax contributions (excluding earnings), and your intended Roth IRA conversion amount, you can quickly calculate how much of your conversion will be tax-free and what percentage of your conversion is tax-exempt.

The following shows the above example in the calculator:

Market Overview

As expected, market volatility increased last week amid a flurry of the administration’s policy actions and some negative economic indicators. Among them:

-

February consumer confidence nosedived. The Expectations Index, which gauges short-term outlooks for income, business, and labor market conditions, fell by 9.3 points to 72.9—dipping below the critical threshold of 80 that often signals a forthcoming recession.

Consumers have begun worrying about tariffs, federal workforce reductions, reduced government spending, and persistently high inflation. Furthermore, major retailers like Walmart and Lowe’s have issued cautious annual forecasts.

- As of March 3, 2025, the Federal Reserve Bank of Atlanta’s GDPNow model estimates a 2.8% annualized contraction in U.S. real GDP for the first quarter of 2025. This marks a significant downward revision from the previous estimate of a 1.5% decline on February 28.

Fasten your seatbelt and stay the course to ride out the fluctuations. To do so, ensure you have a solid investment plan and a well risk-managed portfolio strategy that you’re comfortable with.

The following table shows the major asset price returns and their trend scores, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | -1.0% | -1.3% | -1.0% | 6.0% | 17.3% | 4.0% |

| Foreign Stocks | -1.1% | 1.8% | 0.8% | -1.8% | 6.3% | 1.2% |

| US REITs | 2.5% | 3.6% | -4.2% | -0.5% | 11.7% | 2.6% |

| Emerging Market Stocks | -3.7% | 0.2% | -2.0% | -0.4% | 7.7% | 0.4% |

| Bonds | 1.1% | 1.8% | 0.0% | 0.0% | 4.3% | 1.4% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?