-

Option-Based Income Funds: Pros and Cons

Option-based income funds can be a valuable tool for income-focused investors, particularly in low-yield environments. However, their higher expenses, potential underperformance, and tax implications necessitate a cautious approach.

-

9 Lessons From Retirees’ Biggest Retirement Regrets

In this issue:

- 9 Lessons From Retirees’ Biggest Retirement Regrets

- Returns of MyPlanIQ Core Model Portfolios

- Portfolio Simulator (Calculator)

- Lazy Portfolios: Simple Templates for 401(k) and IRA Investments

- Market Overview

-

Top 15 ETFs for Self-Directed Brokerage Accounts or Brokerage Window in 401(k) Plans

Top 15 ETFs that average 401(k) investors can use to construct a solid asset allocation portfolio for their self-directed brokerage accounts.

-

Top 15 Large Companies with the Highest Employer Match Rate per Employee

Top 15 Large Companies with the Highest Employer Match Rate per Employee: this group of companies have the highest matching rates to reward their employees’ retirement savings.

-

Top 15 Large Companies Offering the Most Generous Employer Matches

Top 15 Large Companies Offering the Most Generous Employer Matches: this group includes airline pilots, physicians, consultants and transportation companies.

-

Top 7 Companies with Billion-Dollar Contributions to Employee Retirement Plans

Top 7 Companies with Billion-Dollar Contributions to Employee Retirement Plans, compared with only 5,000 U.S. companies that have more than a billion dollar annual revenue.

-

January 2025 MyPlanIQ Portfolio Update

In this issue:

- 2024 Review

- Fund Analysis: Be Cautious with Options-Based Income Funds

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

- Expect a Bumpy Ride: Outlook for Stocks and Bonds in 2025

-

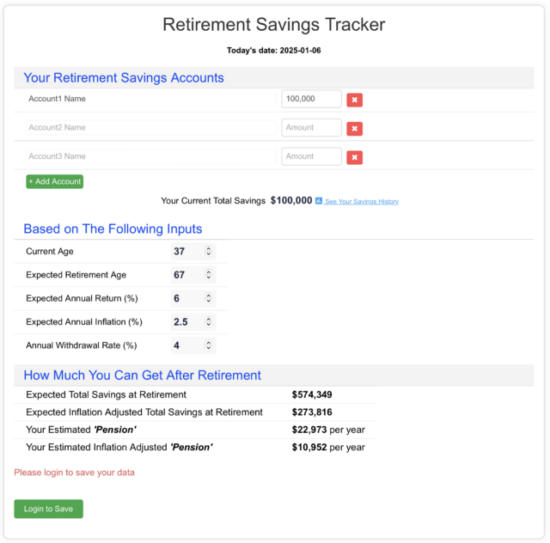

Retirement Savings Tracker and Future ‘Pension’ Estimator

In this issue:

- Gen X’s Retirement Savings Shortfall

- Introducing Retirement Savings Tracker & Future ‘Pension’ Estimator

- Retirement Savings Tracker

- Most Popular Bond Funds in 401(k) Plans

- Market Overview

-

Certificates of Deposit (CDs) vs. Treasuries: The Key Pros and Cons Explained

In this article, we summarize the pros and cons between CDs and Treasuries for fixed-income investors. Key Differences Between Certificates of Deposit (CDs) and Treasuries Factor CDs Treasuries Security – FDIC-insured up to $250,000 per depositor per bank. + Backed by the full faith and credit of the U.S. government, Treasuries are considered among the safest investments, with security that surpasses even FDIC insurance. – Limited insurance coverage for amounts above $250,000 at each bank. + No limit to the amount of protection. Yield + Generally higher yields for maturities of 1 year or longer. – Typically lower yields for maturities over 1 year. – Lower yields for shorter maturities compared to Treasuries. + Higher yields for short-term maturities (less than 1 year). Note: this could possibly change so double check yields before purchase. Taxes – Subject to both federal and state income taxes. + Exempt from state income taxes. – State tax impact can reduce effective yield, especially in high-tax states. + More tax-efficient, especially in high-tax states. Maturities – Limited availability for maturities beyond 5 years. + Wide range of maturities (4 weeks to 30 years). – Flexibility can be restricted depending on the bank’s capital needs and availability of brokered CDs in a brokerage like Schwab or Fidelity. + Extensive maturity options between 2023–2053. Liquidity – Less liquid, may involve fees or uncertainty of receiving original principal if sold early. + More liquid, with an active secondary market for easy resale. – Brokered CDs can be sold in secondary markets but may involve a fee. + Easier to sell with tighter bid/ask spreads. Strategy Considerations – Fewer maturity options for building a maturity CD ladder. + Easier to build a flexible bond ladder portfolio. Convenience + Banks often promote CDs with lower yields. – Has to rely on Brokerage to purchase/sell Treasuries most times Detailed Tax Impact Comparison: State Tax Impact CDs Treasuries For High-Tax States – State income taxes can reduce yield significantly (e.g., California, New York). + State income tax exemption offers a clear tax benefit. Example – In California, a 3-year CD yielding 3.90% after state taxes drops to 3.38%. + A 3-year Treasury yielding 3.51% remains unaffected by state taxes. Breakeven Tax Rate – For a CD to equal a Treasury’s yield, a state tax rate of ~10% or more may be required. + More tax-efficient for investors in high-tax states. Conclusion In summary:

-

Top 9 Most Popular Stock Funds in 401(k) Retirement Plans

Top 9 Most Popular Stock Funds in 401(k) Retirement Plans include actively managed funds by excellent managers and several ultra-low cost Vanguard stock index funds. It also features their latest return figures.

-

Top 11 Most Popular Bond Funds in 401(k) Retirement Plans

Top 11 Most Popular Bond Funds in 401(k) Retirement Plans include actively managed funds by award winning managers and ultra-low cost bond index funds. It also has its latest return figures.

-

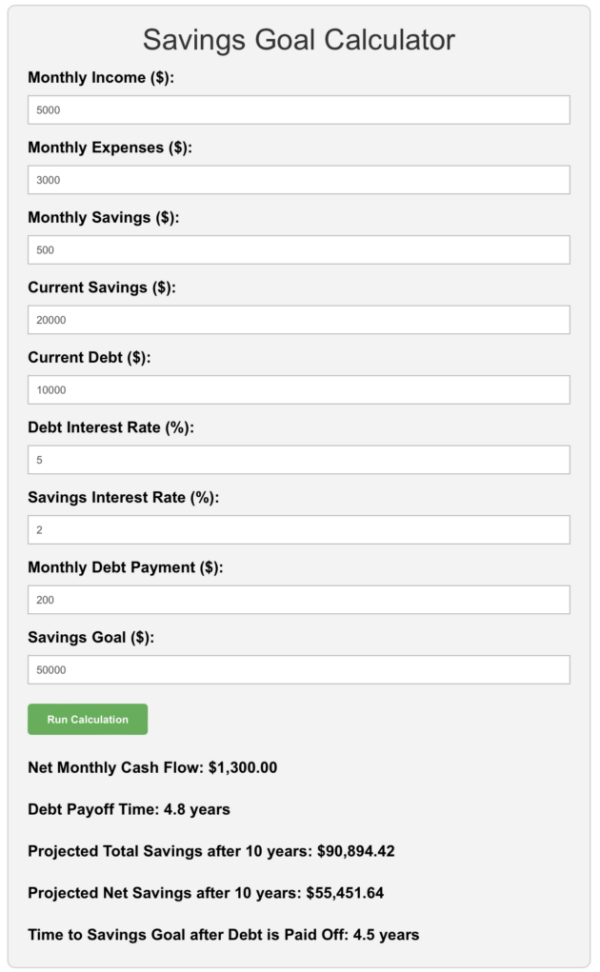

Smart Rules of Thumb to Manage Your Personal Debts

In this issue:

- Student Loan Payoff and 401(k) Match

- Smart Rules of Thumb to Manage Your Personal Debts

- Savings Goal Calculator: Payoff Debt and Save More

- Most Popular Bond Funds in 401(k) Plans

- Market Overview

-

Health Insurance Costs Far Outpace Inflation: How to Protect Your Retirement Savings

In this issue:

- Medicare Cost Increases for 2025 & Ever Rising Health Insurance Cost

- How to Safeguard Your Retirement Savings from Increasing Health Care Costs

- Investment Return Calculators for Funds, Portfolios or Stocks

- Most Popular Stock Funds in 401(k) Plans

- Market Overview

-

December 2024 MyPlanIQ Portfolio Update

In this issue:

- Tactical Asset Allocation Portfolios In-Depth Update

- Fund analysis: U.S. stock momentum factor ETFs

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

-

The Four Essential Steps for 401(k) Investments

In this issue:

- Leaving your company: things to consider for your company 401(k) account

- The Four Essential Steps for 401(k) Investments

- How to Determine the Amount to Contribute to Maximize Your Company Match

- Thrift Savings Plan: The Largest Public Sector Workers’ Retirement Savings Plan

- Market overview: Enjoy the season but don’t be complacent

-

Solo 401(k) vs. SEP IRA: Which is Better for the Self-Employed?

This article compares Solo 401(k) and SEP IRA retirement plans. It discusses the pros and cons of both plans.

-

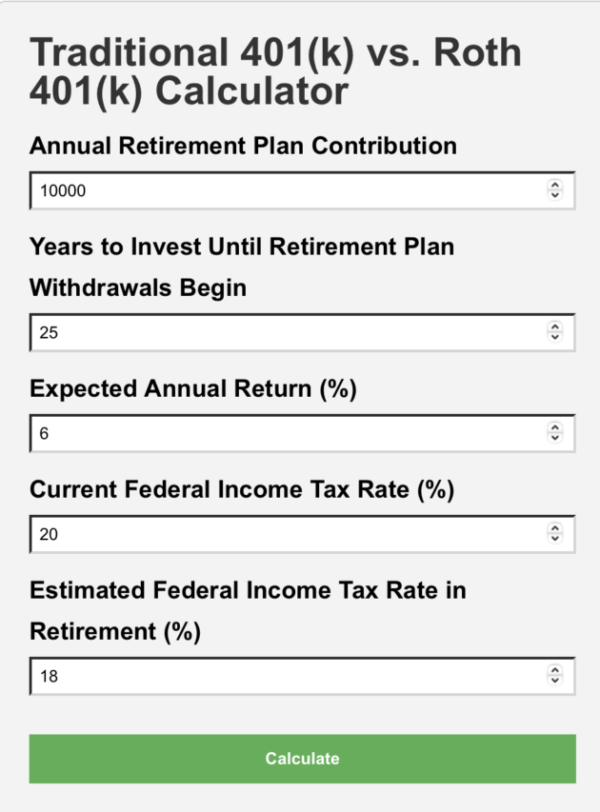

Roth 401(K): A Retirement Savings Option You Shouldn’t Ignore

In this issue:

- Retirees’ credit card debt increased!

- Roth 401(K): A Retirement Savings Option You Shouldn’t Ignore

- Traditional 401(k) vs. Roth 401(k) Calculator

- Top 15 employers with the highest employer match rate per employee

- Market overview: Year-end stock rally?

-

Solo 401(k) Annual Contribution Limits: Employee and Employer Contributions

This article discusses Solo 401(k) Annual Contribution Limits for both Employee and Employer Contributions. It further presents a simple strategy to decide the maximum contribution for Solo 401(k) and Solo Roth 401(k).

-

IRA and Roth IRA Contribution Limits: Annual Caps, Income Restrictions, and 401(k) Considerations

When planning your retirement savings, understanding the annual contribution limits for Individual Retirement Accounts (IRAs), Roth IRAs, and how these interact with 401(k) contributions is essential. Below is an itemized breakdown of contribution limits, income caps, and key considerations. 1. Traditional IRA Contribution Limits (2024) 2. Roth IRA Contribution Limits (2024) 3. Non-Deductible Traditional IRA Contributions 4. Considerations When You Also Contribute to a 401(k) 5. Caution: Pro-Rata Rule for Roth IRA Conversions If you plan to make non-deductible IRA contributions and later convert them to a Roth IRA (commonly known as a “backdoor Roth IRA”), be aware of the pro-rata rule. This rule requires you to calculate taxes on the conversion based on the proportion of pre-tax and after-tax funds across all your traditional IRAs. By balancing 401(k) and IRA contributions, you can maximize tax benefits and long-term retirement growth. If income caps restrict your IRA options, consider strategies like non-deductible IRA contributions or a Roth IRA conversion. In terms of non-deductible IRA contributions, you’ll need to track its basis for tax purposes.

-

YieldMax ETFs Returns & Comparison

This page tracks YieldMax ETFs Total Returns (Price Appreciation and Dividend Reinvested). It also compares each ETF with its underlying stock.