We at MyPlanIQ wish everyone a wonderful Thanksgiving!

Roth 401(K): A Retirement Savings Option You Shouldn’t Ignore

In this issue:

- Retirees’ credit card debt increased!

- Roth 401(K): A Retirement Savings Option You Shouldn’t Ignore

- Traditional 401(k) vs. Roth 401(k) Calculator

- Top 15 employers with the highest employer match rate per employee

- Market overview: Year-end stock rally?

Retirees’ credit card debt increased!

According to Investment News and other news sources, there has been a significant increase in credit card debt among retirees recently. This isn’t surprising, as the recent surge in inflation has taken its toll. Even though inflation has slowed down recently, prices remain high. A slowdown in inflation means the rate of price increases has decreased, not that prices themselves have gone down.

- Rising Debt Levels: In 2024, 68% of retirees reported having outstanding credit card debt, a substantial rise from 40% in 2022 and 43% in 2020. This trend indicates an alarming shift in financial stability for many older Americans

- Financial Strain: Many retirees are struggling to manage their expenses. Approximately 31% stated they are spending more than they can afford, nearly doubling from 17% in 2020. This financial strain is exacerbated by ongoing inflation and high living costs, despite some easing compared to previous years

- Early Retirement and Insufficient Savings: Surveys showed that nearly 60% of retirees retired earlier than planned, often due to health issues or job-related changes. Additionally, about half reported not saving enough for retirement, with many relying heavily on Social Security as their primary income source

- Emergency Savings Decline: The number of retirees maintaining three months’ worth of emergency savings has decreased from 69% in 2022 to 59% in 2024, indicating a growing vulnerability among this population

These findings highlight the growing reliance on credit cards among retirees as they struggle with fixed incomes and rising expenses, raising concerns about their financial stability in retirement. As many of our long-term readers know, we strongly advise avoiding credit card debt whenever possible, as it often carries some of the highest interest rates, frequently exceeding 20%. For a detailed discussion on various types of debts, see Comparing Yields on Various Types of Personal Loans: Should You Pay Off or Invest?

Roth 401(K): A Retirement Savings Option You Shouldn’t Ignore

One of the most frequently asked questions we got is whether it’s a good idea to invest in a Roth 401(k), the after-tax contribution option available in many 401(k) plans. In recent years, Roth 401(k) options have gained significant popularity. According to Fidelity, more than 80% of the retirement plans it administers now include Roth 401(k) contribution options. High-tech startups are also increasingly adopting this feature. For example, Guideline, a leading 401(k) platform for tech startups, offers a Roth 401(k) option as part of its plans.

Despite this growing availability, Fidelity reports that only 14.8% of participants utilize the Roth 401(k) option. Interestingly, most contributors are young professionals aged 25 to 29. This suggests a missed opportunity for workers in other age groups to take advantage of the Roth 401(k)’s benefits.

Tax-Free Returns: A Major Draw

One of the most attractive features of a Roth 401(k) is its tax-free growth and withdrawals. Since contributions are made with after-tax dollars, you won’t owe taxes on your savings—or their growth—when you withdraw in retirement. This eliminates future tax liability, offering peace of mind and financial predictability.

The following are well-recognized advantages of each option:

Roth 401(k): Ideal for Lower Current Tax Rates

If you’re currently in a low tax bracket (around 15% or less), a Roth 401(k) is often the smartest choice:

-

- Locking in Today’s Rates: By paying taxes upfront while rates are low, you can secure tax-free withdrawals later, potentially saving significantly in retirement when rates could be higher.

- Perfect for Early Career Professionals: Younger workers typically have lower incomes and tax rates, making this a prime opportunity to lock in today’s low rates while enjoying tax-free growth.

Traditional 401(k): Better for Higher Current Tax Rates, But There’s a Catch

If you’re in a higher tax bracket (20% or more), a Traditional 401(k) offers immediate tax savings by reducing your taxable income. This can be especially beneficial if:

-

- You expect to be in a lower tax bracket in retirement.

- You want to reinvest the tax savings for additional growth in taxable accounts.

However, if your retirement tax rate is likely to be similar or higher than your current rate, the Roth 401(k) might still be a better option. By paying taxes now, you avoid a potentially larger tax burden later, especially if tax rates rise over time.

Why Roth 401(k) Stands Out

- Predictable Tax Savings: You lock in today’s tax rate and avoid worrying about future rate hikes.

- Ideal for High Earners in Retirement: If you anticipate substantial income from pensions, Social Security, or other investments, the Roth 401(k) ensures tax-free withdrawals won’t push you into a higher bracket.

- Estate Planning Benefits: Roth 401(k) balances can be rolled into a Roth IRA upon retirement, offering heirs tax-free distributions without required minimum distributions (RMDs).

The Hybrid Approach: Best of Both Worlds

For those unsure about their future tax situation, or are simply confused, splitting contributions between a Roth and a Traditional 401(k) can provide flexibility:

- Tax Diversification: This strategy allows for tax-free withdrawals from the Roth 401(k) and taxable withdrawals from the Traditional 401(k), giving you options to optimize taxes in retirement.

- Employer Match Benefits: Employer contributions, regardless of whether you contribute to a Roth or Traditional 401(k), are made pre-tax and grow tax-deferred, ensuring you maximize employer match benefits.

- Flexibility in Withdrawals: Withdraw from the Roth 401(k) during high-tax years and the Traditional 401(k) in low-tax years to optimize your tax strategy.

In the following, we will go through a few scenarios using our calculator for this purpose.

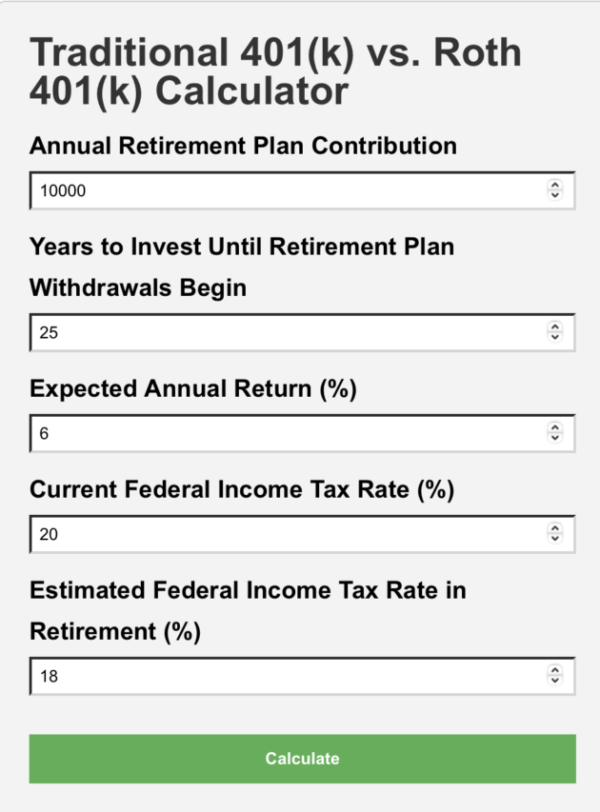

Tools & Tips: Traditional 401(k) vs. Roth 401(k) Calculator

Our Traditional 401(k) vs. Roth 401(k) Calculator is available on our Resources > Calculators page. This calculator helps you determine whether investing in an after-tax Roth 401(k) option is more advantageous than a traditional pre-tax 401(k) option. It evaluates the tax savings and potential growth of those savings when invested under the pre-tax 401(k) option and compares them with the benefits of the Roth 401(k).

Inputs include your current annual contributions, the number of years you plan to invest before retirement, the expected annualized return for tax-deferred pre-tax 401(k) investments, tax-free Roth 401(k) investments, and taxable investments (derived from the tax savings of the pre-tax 401(k) option). The taxable investment calculation assumes an optimistic scenario with no taxes incurred until withdrawal, implying a buy-and-hold portfolio strategy.

You can play with the calculator. For example, in the following scenario, the estimated tax rate at retirement withdrawal time is slightly lower than the current tax rate (18% vs. 20%):

The outputs are:

- Traditional 401(k) Balance at Retirement:$581,563.83

- Tax-Savings Investment Balance at Retirement (from Traditional 401(k) option): $116,312.77

After-Tax Total Traditional 401(k) and Tax-Savings at Retirement: $581,258.81 (sum of the above) vs.

Roth 401(k) Balance at Retirement:$581,563.83

Roth 401(k) achieves higher retirement savings.

The top 15 large employers with the highest average employer match rate per employee

In our previous newsletter, we shared a ranking of the top 15 large companies (with more than 1,000 employees) offering the highest average employer match per employee. This time, we present a new ranking featuring the top 15 large companies (with more than 10,000 employees) with the highest average employer match rate per employee. While the list has changed somewhat, a few airline companies remain.

- PIPE FITTERS ASSOCIATION L.U. 597, U.A. 401(K) PLAN: 438%

- NUCOR CORPORATION PROFIT SHARING AND RETIREMENT SAVINGS PLAN: 353%

- GEORGETOWN UNIVERSITY DEFINED CONTRIBUTION RETIREMENT PLAN: 337%

- KAISER PERMANENTE SUPPLEMENTAL SAVINGS AND RETIREMENT PLAN: 282%

- ELEVATOR CONSTRUCTORS ANNUITY AND 401(K) RETIREMENT PLAN: 278%

- THE UNIVERSITY OF CHICAGO RETIREMENT INCOME PLAN FOR EMPLOYEES: 258%

- THE PROFIT SHARING AND SAVINGS PLAN OF GRAYBAR ELECTRIC COMPANY, INC.: 247%

- VANDERBILT UNIVERSITY MEDICAL CENTER RETIREMENT PLAN: 233%

- NORTHWESTERN UNIVERSITY RETIREMENT PLAN: 230%

- DELTA 401(K) RETIREMENT PLAN FOR PILOTS: 225%

- HNI CORPORATION PROFIT-SHARING RETIREMENT PLAN: 220%

- UNITED AIRLINES PILOT RETIREMENT ACCOUNT PLAN: 219%

- HENRY FORD HEALTH SYSTEM RETIREMENT SAVINGS PLAN: 211%

- DEFERRED SALARY PLAN OF THE ELECTRICAL INDUSTRY: 210%

- DIRECTORS GUILD OF AMERICA-PRODUCER PENSION PLAN SUPPLEMENTAL BENEFIT PLAN: 183%

These companies offer generous employer matches to their employees. As always, you can search for these companies on the Retirement Plan page for more detailed information.

Market Overview

The following table shows the major asset price returns, as of last Friday:

| Asset Class | 1 Week | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 1.7% | 2.9% | 6.3% | 13.2% | 32.6% | 11.3% |

| Foreign Stocks | 0.5% | -2.6% | -2.8% | 0.4% | 13.0% | 1.7% |

| US REITs | 3.3% | 1.5% | 3.9% | 21.6% | 26.8% | 11.4% |

| Emerging Market Stocks | -0.1% | -3.5% | 1.9% | 3.4% | 15.7% | 3.5% |

| Bonds | 0.8% | 0.5% | -1.1% | 4.1% | 6.8% | 2.2% |

Investors are eager to get back to the post-election rally.

Year-end Rally?

The table below presents historical return data for the S&P 500 from Thanksgiving to January 5 of the following year, focusing on years when the index had already gained more than 20% by Thanksgiving. The data indicate that the index often continues to perform strongly through the end of the year.

| Year | S&P 500 Gain by Thanksgiving | Performance (Thanksgiving to Jan 5) | Annual Return |

|---|---|---|---|

| 1954 | +45.02% | +3.5% | +52.62% |

| 1958 | +38.06% | +2.8% | +43.36% |

| 1961 | +23.13% | +1.2% | +26.89% |

| 1975 | +31.55% | +4.1% | +37.20% |

| 1985 | +26.33% | +2.5% | +31.73% |

| 1989 | +27.25% | +3.0% | +31.69% |

| 1995 | +34.11% | +2.7% | +37.58% |

| 1997 | +31.01% | +1.8% | +33.36% |

| 1998 | +26.67% | +2.9% | +28.58% |

| 2013 | +29.60% | +2.5% | +32.39% |

| 2019 | +28.88% | +3.1% | +31.49% |

Observations:

- In each of these years, the S&P 500 continued to rise between Thanksgiving and January 5.

- The additional gains during this period ranged from approximately 1.2% to 4.1%.

- The strong year-end performance contributed to substantial annual returns, all exceeding 25%.

To summarize, historically, when the S&P 500 has gained over 20% by Thanksgiving, it has tended to continue its upward trajectory through the end of the year, resulting in significant annual returns. While past performance does not guarantee future results, these patterns suggest a propensity for year-end rallies following strong gains by Thanksgiving.

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?