![]()

Making Sense of Mixed Signals

In this issue:

-

- Latest in Retirement Savings & Personal Finance

- Reading Between the Headlines

- Monte Carlo Retirement Simulator: Plan for Uncertainty

- Market Overview

Latest in Retirement Savings & Personal Finance

1. A Strong Jobs Report, but Is It Really That Strong?

The May jobs report came in at 172,000 new hires, more than double the 80,000 that economists had forecast. Markets sold off hard in response, the S&P 500 dropped and the semiconductor ETF SMH fell more than 9 percent on Friday alone. The logic was straightforward: if the labor market is still this strong, the Fed has no reason to cut rates at its June meeting.

But the headline number does not tell the whole story. About 70,000 of those new hires were in leisure and hospitality, more than five times the monthly average of 14,000 for that sector, driven by stadium staffing, food service, and event preparation for the FIFA World Cup that starts this week. Those jobs are temporary and will largely roll off once the tournament ends. Together with government hiring, those two sectors accounted for 73 percent of the month’s total gain. Wage growth was modest, up just 0.3 percent month over month and 3.4 percent year over year. That is not an overheating labor market. But on Friday traders were not in the mood for nuance.

2. Retirement Confidence Is Down, but Account Balances Are Up. What Gives?

EBRI’s 2026 Retirement Confidence Survey, released in late April, found that only 61 percent of workers feel confident about having a comfortable retirement, down from 67 percent a year ago. Among retirees the number fell to 73 percent from 78 percent. Yet at the same time, the average 401(k) balance hit a record $146,400 according to Fidelity, up more than 11 percent in 2025 thanks to strong market returns. The combined employee-plus-employer savings rate reached 14.4 percent, just shy of the recommended 15 percent.

So why the disconnect? The survey points to fears about Social Security solvency and potential changes to the retirement system, seven in ten retirees and four in five workers said they are worried the government will alter the rules. Markets have also been volatile, and the daily noise makes people forget that their long term numbers are actually improving. We see this pattern often, people feel worse when markets are choppy, even if the trend is in their favor. Our view has not changed: confidence should come from a long term plan, not from checking your balance every day.

3. Housing in Transition: Renters Gain Leverage, Buyers Find Data on Their Side

The housing market is shifting in ways that matter for household budgets. On the rental side, the national vacancy rate reached 6.3 percent in the first quarter, giving tenants more negotiating room than they have had in years. Concessions are creeping back, a free month here, a waived fee there. For anyone who has been squeezed by rent increases since 2021, this is a welcome change.

On the buying side, the 30-year fixed mortgage rate sits at 6.48 percent according to Freddie Mac, down from the 7 percent range last year but still high enough to keep many would-be buyers on the sidelines. Sellers are feeling it: the national median list price fell 2.4 percent year over year to $429,500, the seventh straight month of decline and the largest annual drop since Realtor.com started tracking in 2017. Active listings are up 4.2 percent, and 17.3 percent of listings have price cuts. Neither renters nor buyers have a decisive edge yet, but the balance is slowly tilting. The days of offering twenty percent over asking before the open house are probably behind us, at least for now.

Reading Between the Headlines

We spend a lot of time looking at data, because data is what grounds us. But raw data without context can be dangerously misleading, and last week was a perfect example. A strong jobs report that was not really that strong. Rising account balances paired with falling confidence. A housing market where both sides think they are losing.

Put it in another way, the world is complicated, and the headlines almost always oversimplify. Our job, whether as investors, savers, or just people trying to make good decisions, is to look past the surface. The 70,000 World Cup hires, which were more than five times the monthly average for that sector, will roll off once the tournament ends. Retirement confidence will recover when markets stabilize, it always does. And the housing market will find its new equilibrium, as markets tend to do. What matters is not reacting to every data point, but having a framework that works across different conditions.

As always, we admit that we have no ability to predict near term market movements. What we can do is to adopt a risk managed approach and let prevailing market conditions and actions guide us further. That means staying diversified, keeping costs low, and not letting a single jobs report, or a single market selloff, knock you off course.

In a word, stay the course.

Worried About Big Loss That Might Derail Your Retirement Investments?

MyPlanIQ tactical asset allocation strategies utilize economic and financial market indicators to gauge investment risk and tactically reduce stock exposure if it deems necessary.

Our model portfolios have had more than a decade track record. Our well received monthly newsletters give informative insights into investment portfolios, funds and market conditions.

Paid subscription has 30-day free trial (Expert tier: 14 days). Cancel anytime for a prorated refund.

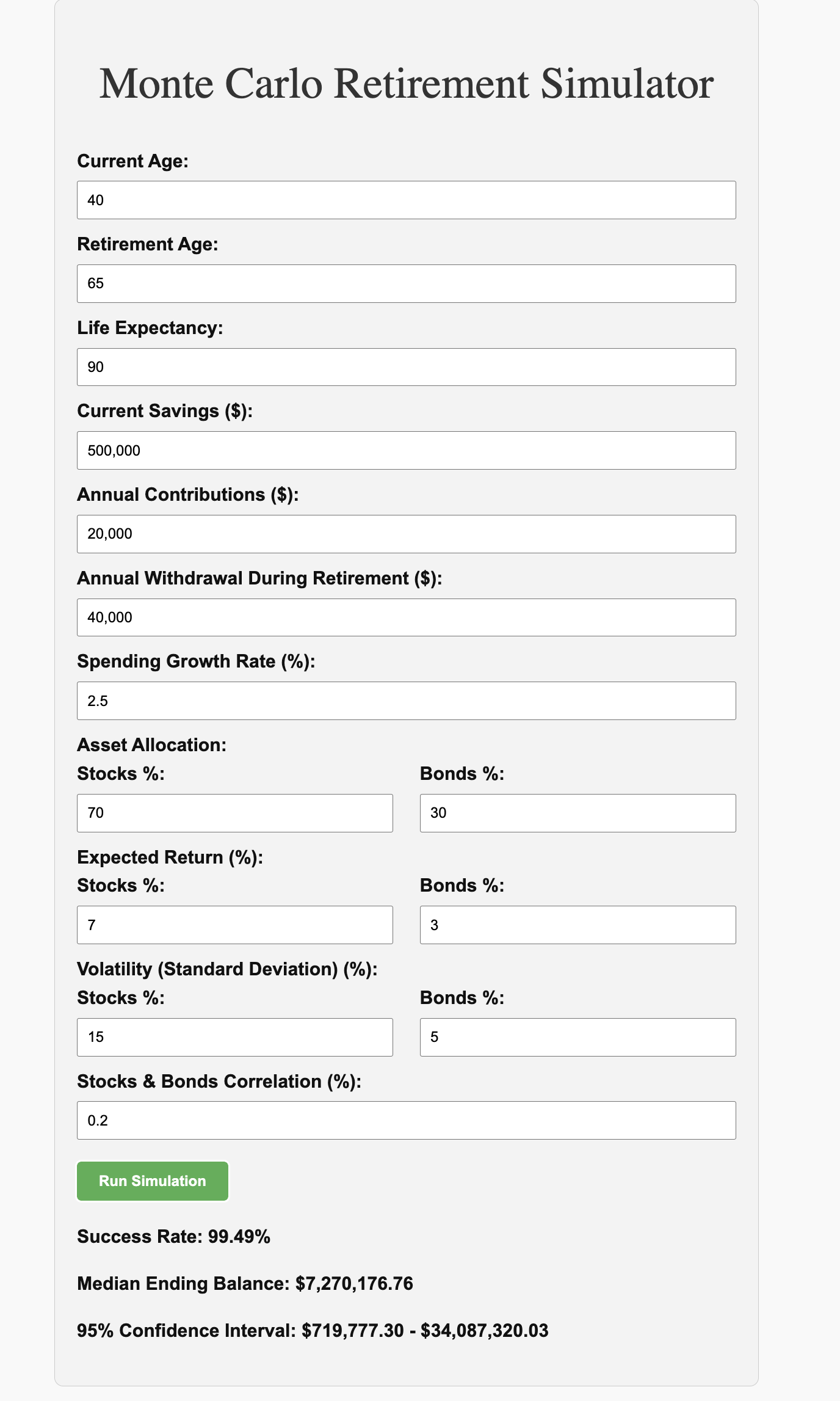

Monte Carlo Retirement Simulator: Plan for Uncertainty

Retirement planning is full of unknowns. How long will you live? What will markets return? Will inflation eat away at your savings? No spreadsheet can answer these questions with certainty, but a Monte Carlo simulation can show you the range of possible outcomes.

Our Monte Carlo Retirement Simulator runs thousands of scenarios using historical market data, varying returns, inflation rates, and life expectancy, to show you the probability of your money lasting through retirement. Instead of giving you a single number that might be wrong, it gives you odds. A seventy percent chance of success means something very different from a ninety five percent chance, and that difference can guide your decisions today.

The other interesting variant is our Historical Data-Driven Monte Carlo Simulator: it uses historical stocks and bonds returns as basis to do all the extensive simulations. This simulator offers a more realistic picture that can be used together with a pure random monte carlo simulator to help you further assess your retirement success rates.

If you have been feeling uncertain about your retirement readiness, this is a good tool to spend some time with. It does not predict the future, nothing can. But it can help you understand the risks you are taking and whether you need to save more, work longer, or adjust your investments. Try it at the link above, it is free to use.

Last week, the good news became bad news: a strong May jobs report drove stocks down sharply. The high flying semiconductor stock ETF SMH was down more than 9% on Friday alone, as investors worried that a robust labor market would keep the Federal Reserve from cutting rates. Whether this is the beginning of a bigger correction remains to be seen.

| Asset Class | 1W | 4W | 13W | 26W | 52W | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | -2.5% | -0.0% | +11.6% | +11.6% | +11.6% | Strong Up |

| Foreign Stocks | -2.8% | -1.4% | +9.5% | +9.5% | +9.5% | Up |

| US REITs | +1.5% | -1.3% | +3.6% | +3.6% | +3.6% | Up |

| Emerging Market Stocks | -3.5% | -3.4% | +8.0% | +8.0% | +8.0% | Up |

| Bonds | -0.5% | -0.8% | -1.0% | -1.0% | -1.0% | Down |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

Upgrade to strengthen your retirement savings while managing risk

Use our tactical asset allocation strategies in your retirement portfolio to seek stronger long-term returns while reducing exposure to frothy markets and potential economic slowdowns.

Or choose our fixed income model portfolios, which have outperformed leading bond funds for over a decade,

Or our smart factor and sector rotation portfolios that consistently beat S&P 500 stock index with less risk.