How to Navigate Medicare Maze

In this issue:

- Latest in Retirement Savings & Personal Finance: Shutdown Showdown,Turning Fulough into an Opportunity,Subprime Auto Loan Trouble

- How to Navigate Medicare Maze

- Tools & Tips: Medicare Medigap vs. Medicare Advantage Total Cost Calculator

- Market Overview

Latest in Retirement Savings & Personal Finance: Shutdown Showdown,Turning Fulough into an Opportunity,Subprime Auto Loan Trouble

Shutdown Showndown

It’s not the first time we’ve seen this, but somehow each one feels heavier. According to CBS’s Jill Schlesinger, the current shutdown could sideline about 750,000 federal employees every day, freezing close to $400 million in pay. More than a million active-duty service members would still show up for work, only this time with no paycheck attached. The number sounds distant until you think about how many of them live paycheck to paycheck, or close to it.

The real damage though is not just the lost wages. The National Association of Realtors says around 1,300 home closings could stall each day if the National Flood Insurance Program lapses. That means actual families stuck in limbo, moving trucks waiting, contracts expiring, deposits hanging. Around the federal campuses, the small businesses that serve those workers are already feeling it. Cafeterias, dry cleaners, barbers, daycare centers. Once the flow of people stops, the cash stops too.

And the longer this goes on, the more permanent the cracks become. Each shutdown gets sold as temporary, but the losses never fully come back. Some wages get reimbursed later, but the missed meals, lost sales, and fading trust never do. At some point it stops feeling like a crisis and starts feeling like habit, which is maybe the most troubling part of all.

Turning Fulough into an Opportunity

It might sound odd, but for those who are furloughed, this period can actually turn out positive. The furlough may look like a punishment at first, yet it often works like a small sabbatical, especially since pay is usually guaranteed afterward, assuming Uncle Sam does not go completely off course. In that sense, it’s a rare moment of forced rest with some built-in safety net. You get time, which is usually the one thing missing. And with that time, you can test small ideas, or at the very least, find temporary income without losing the long-term benefits tied to your regular job.

If nothing else, you can pick up a simple gig to keep some cash flowing. Ride-share work still pays around $20 to $38 an hour, enough to cover roughly $2,000 a month in basic expenses. It is not glamorous work, but it keeps the bills paid and the routine intact. Many other short-term or part-time jobs are still out there if you look hard enough, from delivery apps to tutoring to seasonal retail. The point is not pride, but flexibility.

And once the basics are covered, that same window of time can be used to test something new. Maybe you try your hand at consulting, or build a small freelance skill set that could grow later. Maybe you start learning an online business model, even if it is just a side experiment. It does not have to be big or polished. The goal is simply to keep moving, to keep learning while the system sleeps. Those small steps, what Financial Samurai’s Sam Dogen calls “skill stacks,” tend to add up in quiet ways years later, long after the shutdown talk disappears.

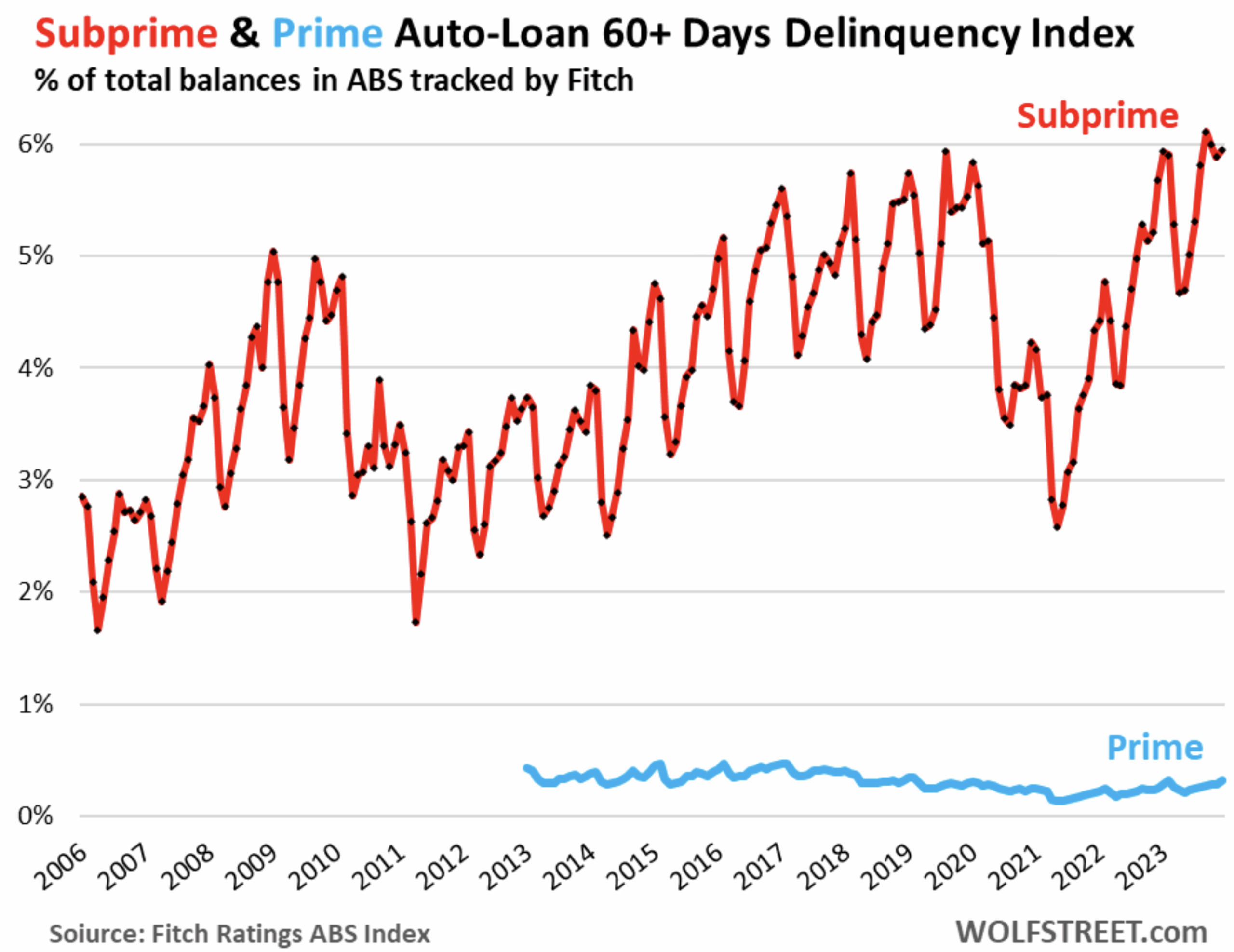

Subprime Auto Loan Trouble

Are we watching a replay of the 2008 real estate subprime mess, only this time in cars instead of houses? It feels a bit like it. The recent collapse of Tricolor Holdings is not just an isolated bankruptcy, it is a signal that something underneath is beginning to crack. Tricolor, a buy-here-pay-here dealership that also acted as its own lender for low-credit or no-credit customers, filed for Chapter 7 liquidation in September 2025. Reports mention irregular collateral pledging and even possible fraud. When a company like that, built entirely on subprime auto financing, falls apart so quickly, it raises the question of how healthy the broader ecosystem really is.

The stress may be more widespread than it looks. For a while, auto delinquencies stayed low and stable, helped by pandemic stimulus and strong labor markets. But that cushion is wearing thin. The 60-plus day delinquency rate for all auto loans reached around 1.44 percent in June 2025, a small rise from 1.40 percent a year earlier. It does not sound like much until you dig into the subprime segment. There, defaults are running in the 5 to 6 percent range according to Fitch data, which is near the highest levels since 2006. That is the kind of quiet pressure that can build for years before showing up all at once.

Not a crisis yet but something worth monitoring.

How to Navigate Medicare Maze

If you are near retirement or just plan or understand health care in retirement, this Traditional Medicare (Medigap) vs. Medicare Advantage can be a very good and helpful guidance. Here are some main points on how to choose among the two main options in Medicare.

After turning 65, Americans get government medical insurance, called Traditional Medicare. This is separate from what is called Medicare Advantage. The question is which one to choose?

Traditional Medicare Overview

When we work, our health insurance usually covers several parts: doctor visits, prescriptions, dental, and vision. Dental and vision coverage are often bought separately.

Traditional Medicare includes:

- Part A: Hospital coverage

- Part B: Doctor visits and outpatient care

- Part D: Prescription drugs

- Plan G: Medigap

Parts A and B are required for most people. Part D (drugs) is optional but most people buy it anyway. Traditional Medicare does not include dental or vision coverage.

Traditional Medicare also has a coinsurance part. For example, the government pays 80% and you pay 20%. The problem is that this personal portion has no upper limit. In some years it can be very high.

To control that cost, there is something called Medigap (or supplemental insurance). Medigap fills the gaps left by Medicare. There are many plans under Medigap. The most common one now is Plan G. Plan F used to be better, but it has been closed to new participants.

So for most people, the reasonable combination is Medicare Part A + Part B + Part D + Medigap Plan G.

Medicare Advantage Overview

Medigap is offered by private insurance companies but approved by the government. During your initial enrollment period (the 7 months around your 65th birthday), these companies must accept you, even if you have pre-existing conditions like diabetes, cancer, or kidney disease.

Now the government also works directly with private insurance companies to offer Medicare Advantage, also called Part C.

Part C usually combines everything from Parts A and B, may include Part D, and sometimes adds dental, vision, or even gym memberships. One appealing feature is the annual out-of-pocket maximum, which limits your yearly expenses.

This sounds beautiful. And that is why about half of retirees now choose an Advantage plan.

Compared with Traditional Medicare, Advantage removes the Medigap cost, still requires the Part B premium, and sometimes even pays for your gym membership.

But if you think Advantage is your best choice, you should be aware of the possible consequences. There is no free lunch. Insurance companies are not charities.

Which One to Choose?

To make long story short, the article concludes the following:

Medigap is usually more expensive at the beginning. But it buys stability and flexibility. Advantage looks cheaper, but the hidden costs show up later when you actually need medical care, and you know it’s very likely when you age.

The key is not just what you pay now, but how much control you will have when your health changes.

Advantage may work fine for people with good health and tight budgets. Well for tight budgets, that might be the only option.

Medigap works better for those who want predictable costs and the freedom to choose any doctor or hospital over the next 20 or 30 years.

Retirement healthcare planning is a personal decision. What I wrote above is just my own understanding and reflection on the topic. Hopefully it helps you think about your own options.

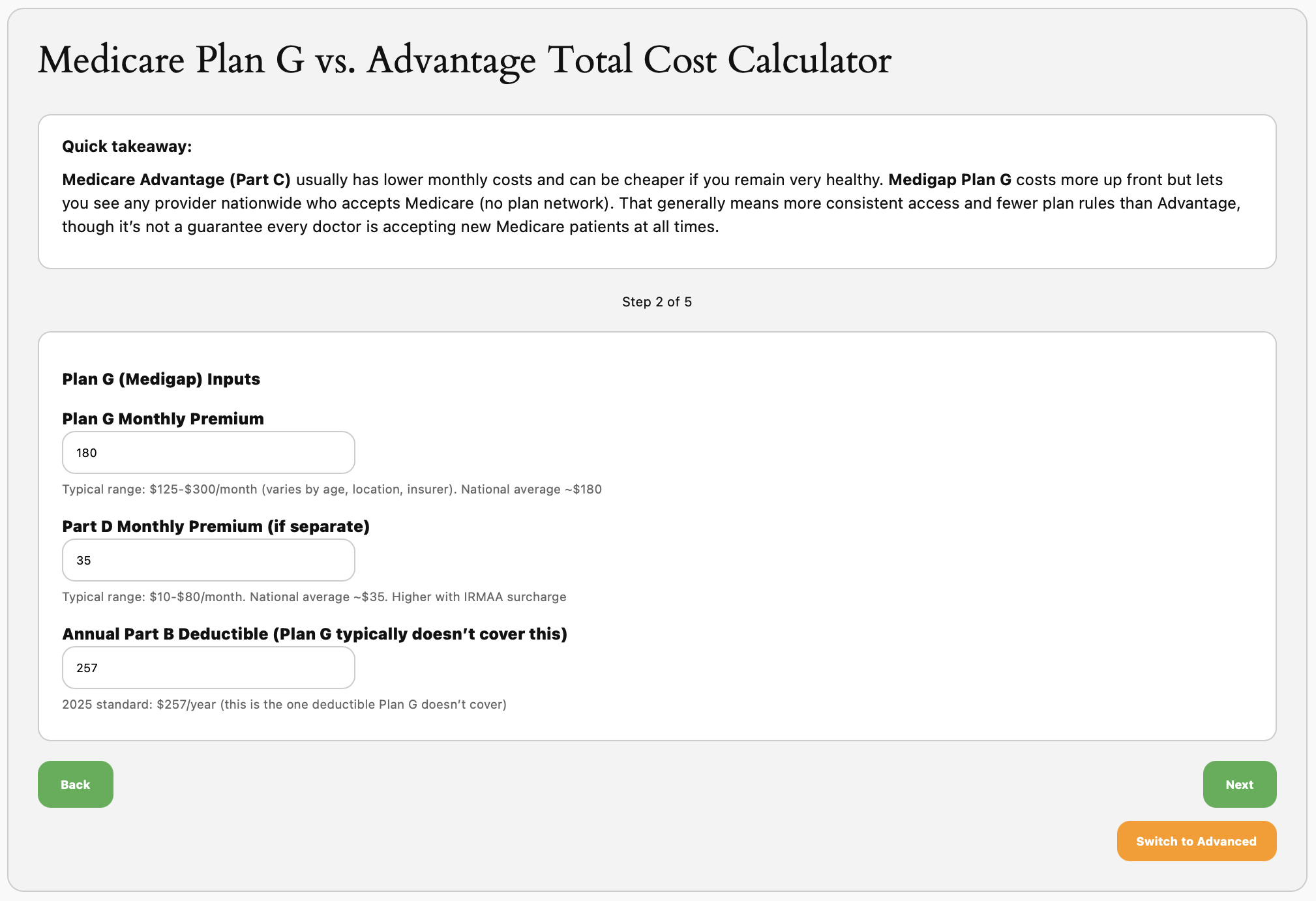

Also, go through the following detailed Medicare Medigap vs. Medicare Advantage Total Cost Calculator to understand nuances.

Tools & Tips: Medicare Medigap vs. Medicare Advantage Total Cost Calculator

The Medicare Medigap vs. Medicare Advantage Total Cost Calculator can be usefule for people are are planning for retirement to navigate the Medicare plan maze. This is especially helpful for people who are near retirement: they are often confused by so many parts/plans and options. The calculator gives some detailed costs for all of the parts.

The Calculator asks you a series of questions (with national averages of various parts):

and then it gives out outputs and guidance:

Nothing else, it gives you some basic understanding on the Medicare cost or the health insurance cost in retirement. This might be of interests to even younger people.

Market Overview

Well, it certainly becomes tiring to repeat everytime to tell people stocks are at all time highs. This is what actually happened for the past several months. But as the saying goes: as the saying goes: enjoy while it lasts! We just want to remind everyone that investing is a long term endeavor and currently, we are definitely at some peaks.

The following table shows the major asset price returns and their trend scores, as of this Monday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 1.2% | 3.9% | 8.5% | 33.9% | 19.7% | 13.4% |

| Foreign Stocks | 2.5% | 4.0% | 9.5% | 34.8% | 19.9% | 14.1% |

| US REITs | -0.6% | -0.5% | 2.4% | 12.6% | -0.3% | 2.7% |

| Emerging Market Stocks | 2.2% | 5.7% | 11.7% | 34.6% | 15.3% | 13.9% |

| Bonds | -0.1% | -0.5% | 2.4% | 3.2% | 3.8% | 1.8% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.