Savings Hacks

In this issue:

- Latest in Retirement Savings & Personal Finance: Crypto in 401(k), Private Investments in Target Date Funds, BNPL Credit Score Impact

- Savings Hacks Using BNPL & Others

- Tools & Tips: Money Market Fund Center

- Market Overview

Latest in Retirement Savings & Personal Finance: Crypto in 401(k), Private Investments in Target Date Funds, BNPL Credit Score Impact

Crypto in 401(k)

Recently, the U.S. Department of Labor officially rescinded its 2022 guidance urging plan fiduciaries to exercise “extreme care” when adding cryptocurrencies to 401(k) menus. That earlier stance had warned of crypto’s extreme volatility, custody difficulties, fraud risks, valuation uncertainty, and evolving regulations. It suggested that fiduciaries might even face investigations if they offered direct crypto exposure. The new guidance returns to a “neutral” position: neither endorsing nor opposing crypto in retirement plans and leaving it up to fiduciaries to evaluate prudently under ERISA standards.

We are actually very encouraged with the blockchain and stablecoins promises to streamline payments and cut costs, among other benefits. For example, it’s been reported that major retailers like Walmart and Amazon have started to explore how to issue and incorporate stablecoins into their payment and supply chain system. Using these stablecoins can cut down payment cost and also improve their supply chain management. As more governments around the worl, including the current administration in the US, are embracing or warming up to these new currencies, it’s likely that cryptocurrency will increasingly play an important role in the economy.

However, both participants and fiduciaries (sponsors) should be aware that crypto remains highly speculative, its prices often driven by momentum—or occasionally driven by scams. Experts caution that while younger investors might stomach the volatility, those approaching retirement cannot afford sudden market swing: Bitcoin has swung 50‑100% in days. And while a handful of providers (e.g. Fidelity) are considering or offering crypto access via self-directed “brokerage windows,” this invites heightened fiduciary risk and oversight burdens. Plan sponsors must still ensure due diligence, guard against scams, verify custody arrangements, control the portion allocated to crypto, and be ready for participant losses and potential legal pushback.

Private Investments in Target Date Funds

Similar to the crypto in retirement 401(k) plans, firms like BlackRock’s and State Street are exploring private-market-enhanced strategies for defined contribution plans. It’s said that about 87 percent of firms with more than $100 million in revenue are privately held, leaving vast opportunity outside public markets. With many companies staying private far longer, investors may miss out on growth if confined to public stocks and bonds. Private credit and private equity offer access to that growth.

BlackRock plans to roll out a target-date vehicle by mid-2026 that will allocate between 5–20 percent of assets to private credit and private equity, with heavier allocations for younger participants. They estimate that this private asset inclusion could boost long-term returns by roughly 0.5 percent annually. With target date funds accounting for around 59–60 percent of 401(k) assets and participants, the private investments (credits and equity) could have some real sizable impact.

However, beware that private assets are often less liquid, more complex to value, and typically charge higher fees, which may erode net returnswsj.com. Additionally, the valuation process for private investments lacks the transparency and frequency of public markets.

BNPL Credit Score Impact

Fair Isaac Corp (FICO) announced this summer that starting in fall 2025, BNPL (Buy Now, Pay Later) loans will finally be factored into credit scores. This is a big change for the 90 million+ Americans using these services. Previously, BNPL accounts were omitted from credit reports, so missed payments didn’t show up. That ends now. If you pay on time, BNPL activity may even help build or stabilize your score, especially for those with thin credit histories—but if you miss payments, your score could take a hit.

While this change brings more transparency and could help responsible users, it also raises flagging concerns. Late BNPL payments rose from 18% in 2023 to nearly 25% in 2024. Experts are warning about “phantom debt”: multiple small BNPL loans that consumers may not see coming, and the absence of typical protections like grace periods or real-time alerts. BNPL has also been criticized for encouraging spending beyond one’s means.

Savings Hacks Using BNPL or Others

Timing, discipline, and stacking, this is how you can take a $1,000 purchase and squeeze extra value out of it. Let’s break down the main strategies and quantify the benefits. You’ll be surprised to know that there can be many ‘hacks’ to help reduce spending or save money.

1. BNPL + High‑Yield Cash

- Item price: $1,000 → Let’s say you want to purchase some like a refrigerator that costs $1,000. You wait for sale price: $900 (10% off)

- Use 0% BNPL (Buy Now, Pay Later), you invest your $900 cash outlay to some high yield cash account. Examples, just simply buy USFR (WisdomTree Floating Rate Treasury Fund) that currently yields 4.3% (7-day SEC yield) for 6 months, before you need to pay.

- Interest earned in 6 months: $900 × 4% × 0.5 = $18

- Net cost: $900 − $18 = $882

- Total discount vs list: 11.8%

You can further stack up savings by using Credit Card Rewards:

2. BNPL + Credit‑Card Rewards

You put the purchase on a 2% cashback card in the above:

- Cashback bonus: $900 × 2% = $18

- Total savings: $18 (yield) + $18 (cashback) = $36

- Net cost: $900 − $36 = $864

- Total discount: 13.6%

If you wait for 15% off deeper sale, which is not unheard of, you can further get your discount to 18.4%! Now you have saved $186 off $1,000

3. Gift‑Card + BNPL + Rewards (Using Costco Gift Cards)

Costco often offers gift cards at ~10% discount, e.g., $500 Southwest card for $450.You can use similar savings for retail gift cards. You can get $1,000 face value gift cards for: $900 (10% off) and then use the gift card to pay BNPL. You can further stack on your invest yield gain $18 on top of your $100 (roughly) gift card savings. So now we are talking about paying about $1,000-100 (discount)-18-100=$782 purchase price. This is a 21.8% savings!

4. Max-Stack: Gift-Card + BNPL + Bonus Rewards (Credit card)

You can max up your savings by paying your gift card using some credit cards with good rewards such as another 3% cash back. Now you can push your savings to 25%!

The point in the above is that, if you are disciplined and resourceful: wait for sales, use BNPL to delay the charge, invest the cash, purchase discounted gift cards with credit card cash back etc., you can save a lot. Note here: we know that BNPL traps quite some people to encourage those who don’t have money or don’t have need to spend, but you can be smart to turn the table around to your advantage.

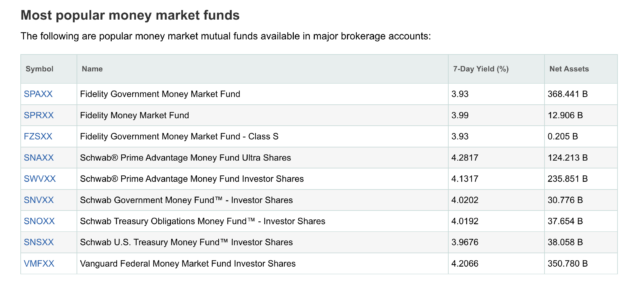

Tools & Tips: Money Market Fund Center

MyPlanIQ maintains one of the most comprehensive and timely money market fund pages, tracking most money market mutual funds along with a few key ETFs that can be viewed as ‘Treasury money market funds’.

On this page, you can find some of the most popular money market funds in major brokerages like Schwab, Vanguard and Fidelity.

It also has identified some popular and excellent Treasury money market like ETFs:

The good thing here is that these ETFs are available virtually in any discount brokerage commission free. They offer some of the best yields because of their low expense ratios. For example, as stated in the above, USFR (WisdomTree Floating Rate Treasury Fund) is now yielding 4.3%, which is higher than all of the money market mutual funds’ yields right now. This 4.3% is also one of the best rates you can find in any US bank’s savings account. The other good thing: there is no gimmick or limited period of high yields like many banks offer.

Market Overview

Nothing seems to be able to derail the current rally in stocks. US stocks reached all time high recently.

The following table shows the major asset price returns and their trend scores, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 3.0% | 4.6% | 10.9% | 5.7% | 14.7% | 7.8% |

| Foreign Stocks | 3.1% | 2.9% | 12.1% | 18.1% | 17.9% | 10.8% |

| US REITs | -1.3% | 0.5% | -0.7% | 2.8% | 11.3% | 2.5% |

| Emerging Market Stocks | 3.3% | 4.6% | 9.5% | 11.6% | 15.2% | 8.8% |

| Bonds | 0.7% | 1.6% | 1.0% | 3.8% | 6.3% | 2.7% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

Try to Find Your Old Retirement Accounts?

Find Tools and Calculators That Provide Quick Help