Paying Off Debt or Funding Retirement? How to Decide When Every Dollar Counts

In this issue:

- Latest in Retirement Savings & Personal Finance: 401(k) Millionaires Save More, Spring Financial Cleaning

- Paying Off Debt or Funding Retirement? How to Decide When Every Dollar Counts

- Paying off Debt or Investing Calculator

- Market Overview

Latest in Retirement Savings & Personal Finance: 401(k) Millionaires Save More, Spring Financial Cleaning

401(k) Millionaires Save More,

Recent Fidelity studies show that quite some members of millennials (those born between 1981 and 1996) have reached 401(k) millionaire status! Congratulations!

Here are some data:

- The average 401(k) millionaire has been contributing for 25.7 years!

- The annual contribution rate of their income is 17%, which is much higher than the typically suggested range of 10% to 15%.

Additional data on 401(k) millionaires:

- Among 401(k) millionaires, 41% are Baby Boomers (born 1946-1964), 57% are Generation X (born 1965-1980), and 2% are Millennials.

Saving more and saving consistently will serve you well.

Spring Financial Cleaning At Tax Filing Season

It’s that time of the year again: tax filing season. This Kiplinger article suggests the following:

- Reviewing and rebalancing investment portfolios

- Consolidating retirement accounts

- Updating estate planning documents

- Monitoring bank statements for unnecessary fees

- Canceling unneeded subscriptions

- Of course, we might add: reviewing your debts and consolidating or paying off them if necessary

Egg Price Chart

We hope the current downtrend continues:

Paying Off Debt or Funding Retirement? How to Decide When Every Dollar Counts

So you’re juggling $18k in student loans at 4%, a mortgage at 6.75%, or a surprise $12k credit card bill from a rogue family member. Or maybe you’re staring at a 2.7% private loan, wondering if paying it off is smarter than keeping cash in a savings account. These aren’t just math problems—they’re life problems. In the following section, we’ll examine recent discussions on Reddit and delve into a very common question: how to balance debt repayment and retirement savings when real-world challenges—such as job stress, family drama, or the constant worry of being one crisis away from disaster—complicate the equation. By the way, this question is also one of the most frequently asked ones directed to MyPlanIQ.

The Math vs. The Mind: Low-Interest Debt

If your debt has a low interest rate (2-3%), the math says invest. For example, a 2.7% loan vs. a 4-5% CD or Treasury fund? You’ll pocket the difference. But life factors in: What if your job security wobbles? Or if carrying debt keeps you up at night? A Reddit user with $30k at 2.7% opted to pay it off for peace of mind, even though the numbers slightly favored investing. If the loan is long-term (15+ years), you could split funds: park most in safe investments (CDs, bonds) and dabble in index funds like VOO for growth. But if uncertainty looms (e.g., a shaky economy), the mental relief of debt freedom might outweigh small gains.

High-Interest Debt: No Contest

Credit cards at 20%+? Pay them off now. Absolutely! The returns on eliminating toxic debt crush most investments. But what about “middle ground” rates (4-6%)? A user debating a 4% student loan vs. retirement contributions faced this. If the debt is short-term (e.g., 5 years), aggressive payments might win. But for a 30-year mortgage at 6.75%, investing might outpace interest over time by some margin —if you stomach market swings. Ask yourself: Can you handle a market dip? Are emergencies (medical bills, car repairs) already covered? If not, prioritize debt to avoid compounding stress. In general, peace of mind would say you should just payoff now.

The Gray AreaThat Demands Flexibility

What if you’re hit with a $12k unauthorized credit card charge or a $220 medication bill? Suddenly, “minimum payments” feel like a lifeline. Or maybe you’re a new parent wondering if raiding retirement to fund a home renovation is worth it. These scenarios demand flexibility:

- Emergency funds first: Before tackling debt or retirement, build a buffer (even $1k) to avoid spiraling.

- Balance emotion and logic: A user paying $700/month on student loans (vs. $140 minimum) cited job security but feared future stagflation. Their compromise? Overpay now while cash flow is stable, then pivot to retirement if the economy tanks.

- Family dynamics matter: If a loved one’s mismanagement affects your finances (like the sister-in-law who racked up $12k), prioritize damage control before long-term goals.

A Framework for Real Life

To summarize:

- Kill high-interest debt first (6%+). No exceptions.

- Invest in tax-advantaged accounts (e.g., 401(k) with employer match) while making minimum payments on low-interest debt.

- For middle rates (4-6%), ask:

- Can I invest without panic? If yes, consider growth.

- Is my life stable? Job security, health, and emergency savings matter.

- Will debt-free living improve my mental health? If so, pay it off.

A 23-year-old with a $53k windfall froze at investing advice—until realizing her Roth IRA could grow while she saved for a car. A 30-something debated draining retirement for real estate but paused to weigh risks. There’s no perfect answer, but the best choice balances spreadsheets with your sanity.

Tools & Tips: Paying off Debt or Investing Calculator

We continue our discussion on paying off debt versus investing. We have designed the Paying off Debt or Investing Calculator to help you compare two financial strategies: paying off debt versus investing while making payments. It shows whether maintaining investments while paying down debt could leave you with more capital at the end of your loan term, or if focusing solely on debt repayment would be the better option.

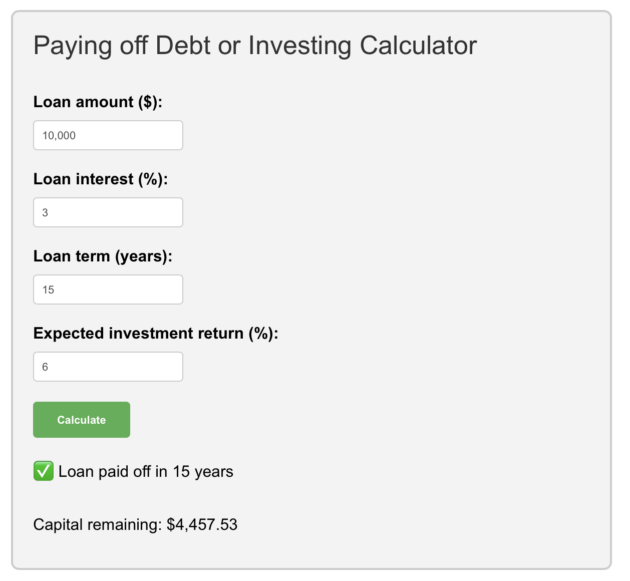

The following demonstrates the calculator’s results for a low-interest loan scenario:

In the above low-interest scenario, you could set aside and invest with 6% annual returns while making the required monthly loan payments for 15 years. After that period, you would still have $4,457 accrued.

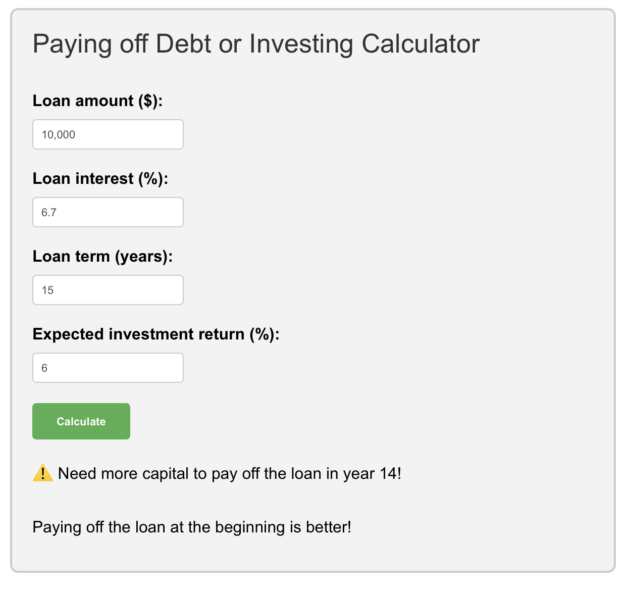

When your loan interest rate is 6.7%, the situation changes completely. You will need more money to cover the debt and interest by year 14. Of course, things can become even tougher if the interest rate is much higher or your investment returns are lower.

Market Overview

Here are some major developments in the economy and financial markets:

- Inflation Trend: Inflation moderated, with February’s core Consumer Price Index rising at an annual rate of 3.1%, down from January’s 3.3%.

- Interest Rates: The Fed held rates steady but maintained its forecast for two cuts later this year, citing slowing growth and mixed inflation pressures.

- Growth Outlook: Economic growth showed signs of cooling, with softer consumer spending and sentiment amid heightened policy uncertainty related to tariffs and government funding debates

- Investor Sentiment: Investors continued to exhibit bearish sentiment last week. The AAII Investor Sentiment Survey still showed a historically high bearish percentage at 58.1%, albeit slightly lower than the previous week.

- Financial Markets: US stocks edged out a slight gain last week, with the S&P 500 returning 0.5%, while almost all major asset classes delivered positive returns.

The following table shows the major asset price returns and their trend scores, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 0.5% | -5.6% | -4.1% | 0.0% | 9.6% | 0.1% |

| Foreign Stocks | 0.0% | 1.1% | 7.8% | 0.5% | 6.9% | 3.3% |

| US REITs | 0.1% | -1.5% | 1.0% | -6.9% | 8.9% | 0.3% |

| Emerging Market Stocks | 0.2% | -0.6% | 3.5% | 1.4% | 10.6% | 3.0% |

| Bonds | 0.4% | 0.8% | 1.6% | -1.8% | 3.9% | 1.0% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

Whether the current correction is over remains to be seen. Regardless, we advocate staying the course.

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?