![]()

Layoff & Your Rights

In this issue:

- Latest in Retirement Savings & Personal Finance

- Layoff & Your Rights

- Tools & Tips: Very Long-Term Stock and Bond Return Data

- Market Overview

Latest in Retirement Savings & Personal Finance

Trump Proposed to Expand Retirement Savings for Those without Employer-Sponsored Plans

President Trump proposed during his State of the Union address to give the roughly 56 million workers without employer sponsored retirement plans access to a new savings account with a federal match of up to $1,000 per year. The match builds on the Saver’s Match provision in SECURE 2.0 (set to take effect in 2027), which offers a 50% government match on the first $2,000 of annual contributions for individuals earning under $35,500 (or couples under $71,000). The important distinction from the old Saver’s Credit: this would be actual dollars deposited into your account, not a nonrefundable tax credit on paper.

The accounts would be modeled after the federal Thrift Savings Plan (TSP), offering a small menu of low cost index funds (S&P 500, small cap, international, bonds, government securities) with expense ratios around 0.05% or less. The accounts would be portable, following workers from job to job. Details remain thin on whether contribution limits would be raised beyond the current $7,000 IRA cap, and the White House claims much of this can be done without Congress, though that’s debatable.

The Federal Thrift Savings Plan (TSP) Long Term Returns

Speaking of TSP that’s for about 7.3 million federal employees, a simple plan with index funds of ultra low fees (0.05% or less), it has performed exceptionally well in the long term.

Individual Funds (Core TSP Funds)

|

Fund

|

10-Year Annualized

|

Since Inception Annualized

|

Inception Date

|

|---|---|---|---|

|

G Fund(Gov’t Securities)

|

2.8%

|

4.7% (since Apr 1987; ~39 years)

|

Apr 1, 1987

|

|

F Fund(U.S. Bond Index)

|

2.1%

|

5.3% (since Apr 1987)

|

Apr 1, 1987

|

|

C Fund(S&P 500)

|

15.4%

|

10.8% (since Apr 1987)

|

Apr 1, 1987

|

|

S Fund(Small/Mid U.S. Stocks)

|

12.4%

|

10.0% (since 2001)

|

May 1, 2001

|

|

I Fund(International Stocks)

|

10.9%

|

7.0% (since 2001)

|

May 1, 2001

|

In February 2026:

- I Fund (international stocks): +6.05% in February, +12.34% YTD.

- S Fund (small/mid-cap U.S.): +1.08% in Feb.

- F Fund (fixed income): +1.63%.

- G Fund (government securities): +0.33%.

- C Fund (large-cap U.S.) and most L (lifecycle) funds were essentially flat.

This underscores the value of diversification in retirement portfolios amid U.S. market choppiness.

Layoff & Your Rights

Last week, Block Inc. made a big announcement to lay off its 40% workers. It blamed AI efficiency, though some people pointed out it also had a lot to do with its over hiring during the Covid period.

In light of the increasing number of layoff events, we summarize the key benefits and rights for those who are laid off to help them navigate this difficult period. Below is a brief overview of the main items. For more details, please refer to the full article.

- The WARN Act: If your employer did not provide required notice before a mass layoff, you may be entitled to up to 60 days of back pay and benefits under federal and some state WARN laws.

- Severance Pay: Severance is not legally required but often offered in exchange for a release of claims, and many terms like weeks per year of service or equity vesting are negotiable.

- COBRA: You can continue your health insurance for up to 18 months through COBRA but must pay the full premium plus a 2% fee, and marketplace plans may be cheaper.

- Unemployment Benefits: You should file immediately since benefits begin when you file and generally replace 40% to 60% of prior wages, subject to state rules.

- Your 401(k): Your vested contributions are yours, and you have rollover options, but unvested match may be forfeited unless a partial plan termination rule applies.

- Flexible Spending Account (FSA): FSAs are “use it or lose it,” and unused balances typically disappear when coverage ends, though COBRA continuation may be possible.

- Stock Options, RSUs, and ESPP: Vested shares/options remain yours but unvested awards usually expire; exercise windows (often 90 days) matter.

- Deferred Compensation: Nonqualified deferred comp is unsecured and may trigger immediate distribution with tax implications following layoff.

- Bonuses and Earned Compensation: Employers may owe earned bonuses and accrued vacation/PTO depending on plan terms and state law.

- Student Loan Deferment: Federal student loan unemployment deferment or income-driven repayment plans are options to lower or pause payments.

- Life and Disability Insurance: Group life/disability usually ends at separation, but conversion or portability options may be available.

- Non-Compete Clauses: Non-competes in severance or employment agreements may limit future work and are negotiable in many cases.

- First 72 Hours: Save all HR documents, file unemployment, get equity details, and compare COBRA vs marketplace before deciding.

Worried About Big Loss That Might Derail Your Retirement Investments?

MyPlanIQ tactical asset allocation strategies utilize economic and financial market indicators to gauge investment risk and tactically reduce stock exposure if it deems necessary.

Our model portfolios have had more than a decade track record. Our well received monthly newsletters give informative insights into investment portfolios, funds and market conditions.

Paid subscription has 30-day free trial

(Expert tier: 14 days). Cancel anytime for a prorated refund.

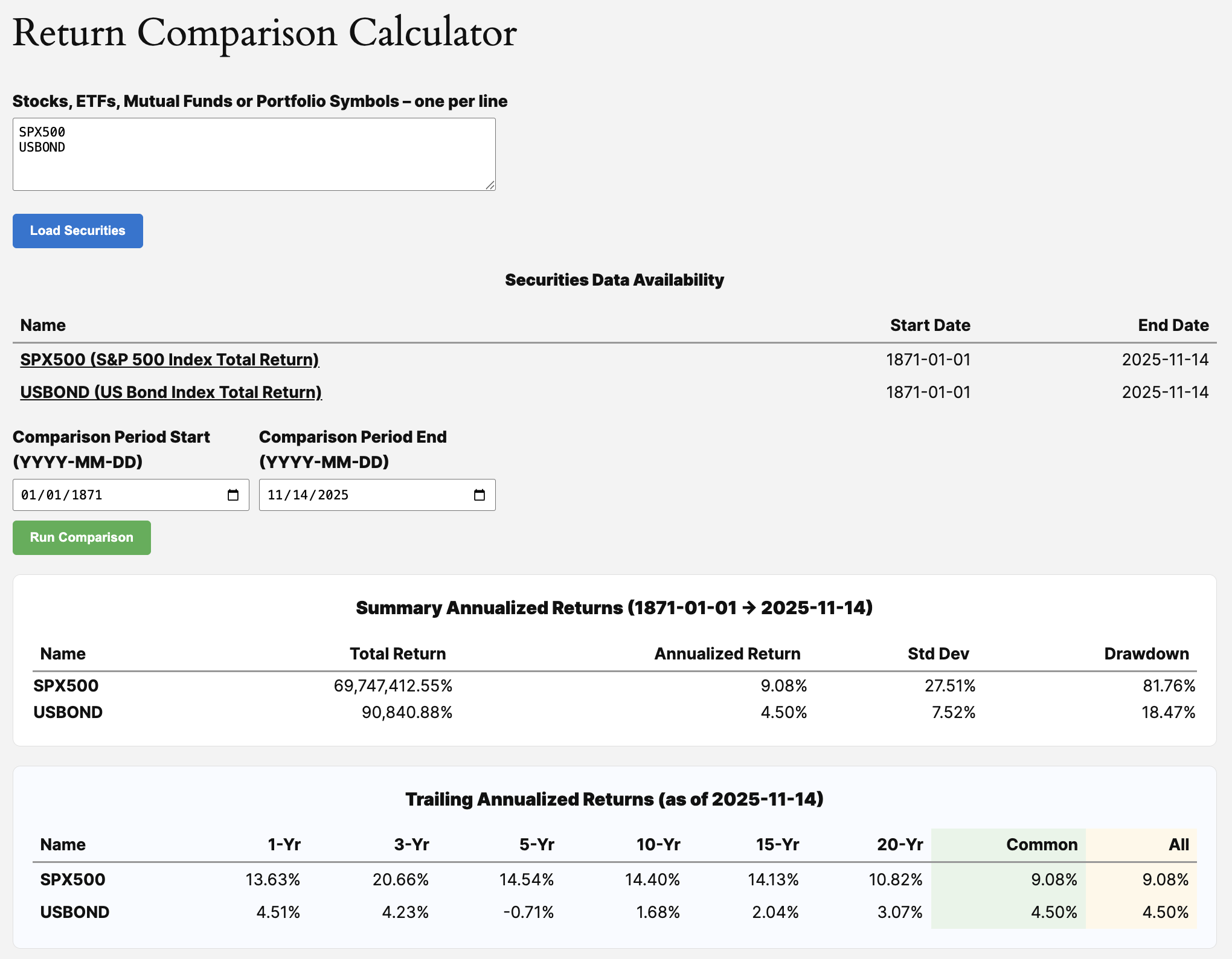

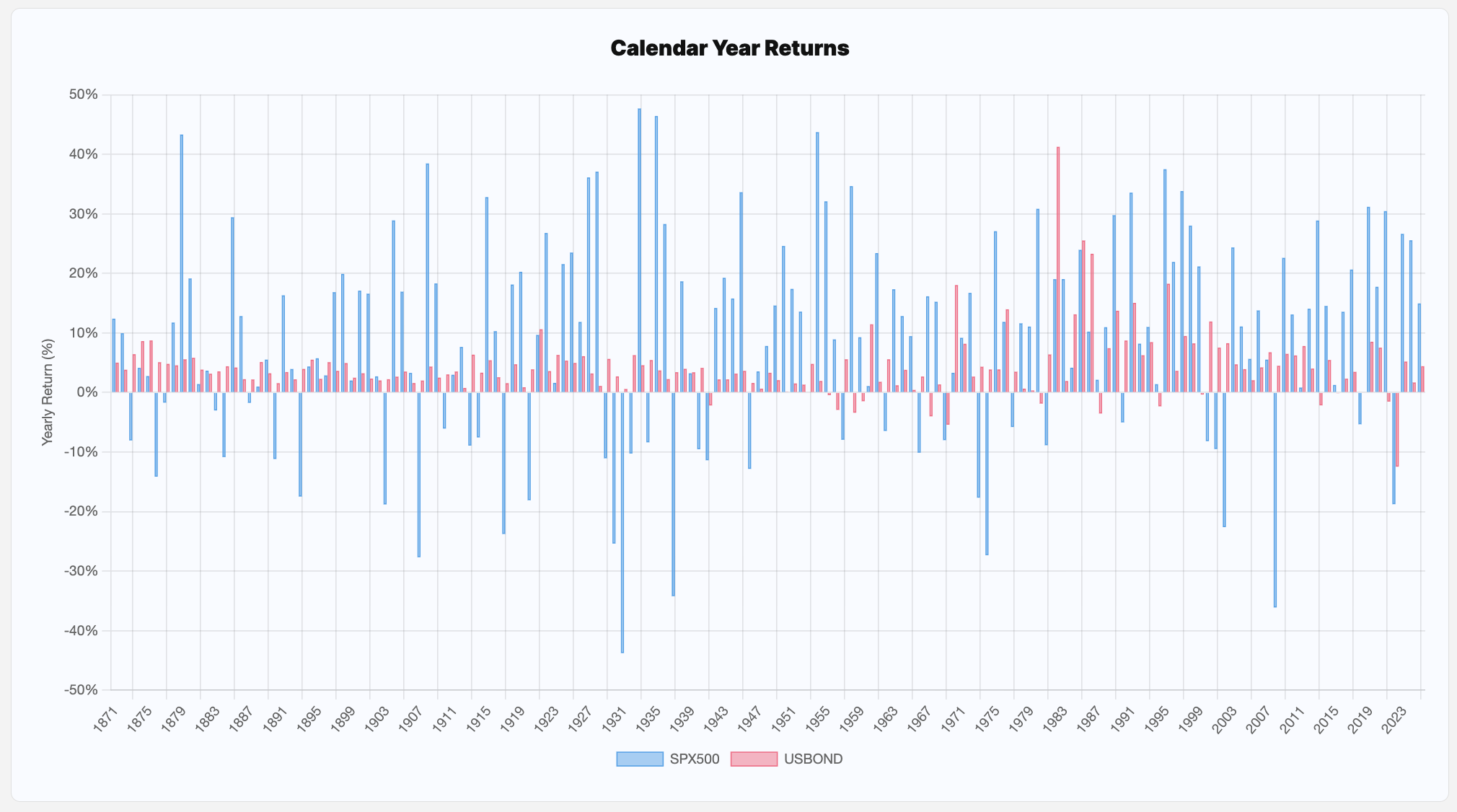

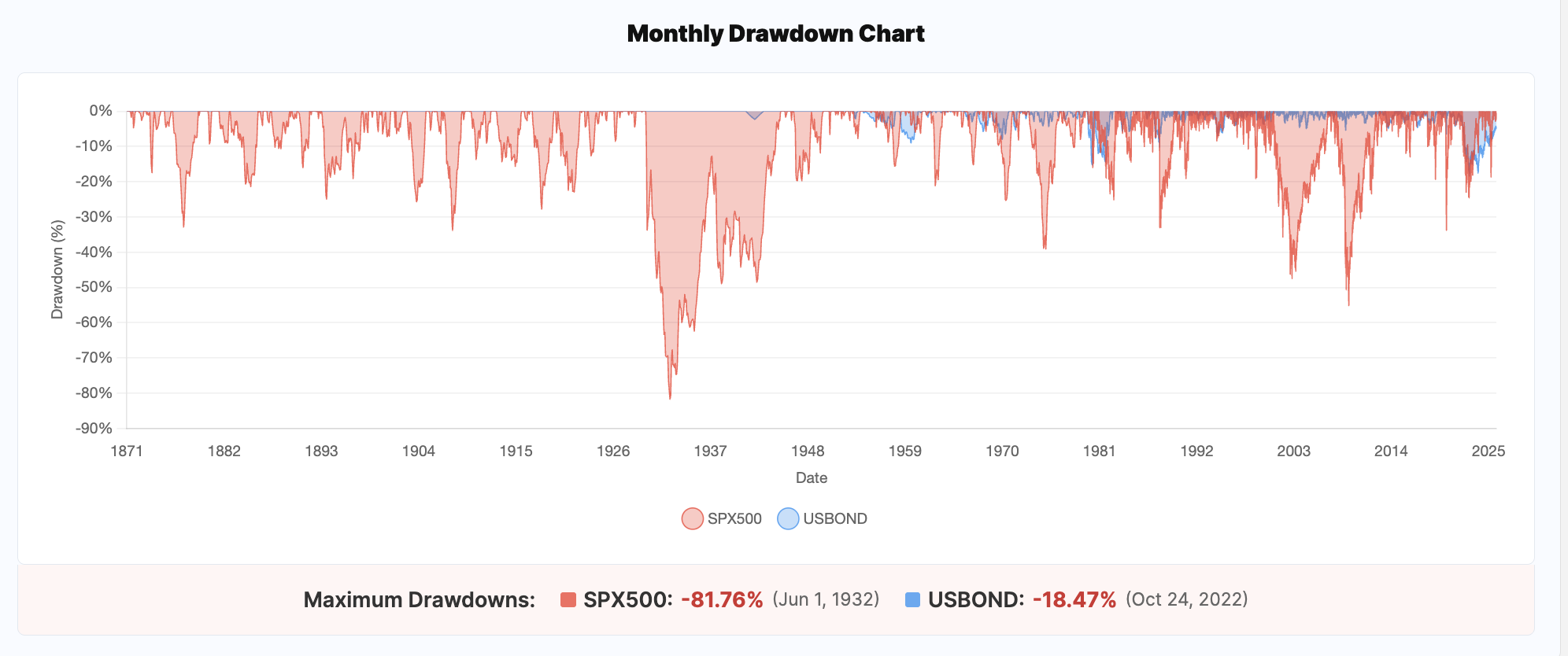

Tools & Tips: Very Long-Term Stock and Bond Return Data

MyPlanIQ has maintained some of the longest stock and bond return data: since 1871. The following are the annualized returns, calendar returns and maximum drawdown for both US stock index (S&P 500) and total bond index since 1871. You can use our Return Calculator as follows:

The above could be helpful to visualize returns and volatility (maximum loss or maximum drawdown, for example). Note at one time, S&P 500 lost more than 80% from its previous peak!

Market Overview

Investors are rotating to international stocks.

| Asset Class | 1W | 4W | 13W | 26W | 52W | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 0.7% | -1.3% | 1.3% | 7.1% | 19.0% | 5.4% |

| Foreign Stocks | 1.4% | 5.0% | 14.3% | 20.6% | 39.7% | 16.2% |

| US REITs | 1.1% | 6.8% | 6.0% | 5.9% | 5.5% | 5.1% |

| Emerging Market Stocks | -1.3% | 1.2% | 7.9% | 14.2% | 32.8% | 11.0% |

| Bonds | 0.2% | 1.4% | 1.6% | 3.5% | 5.5% | 2.4% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

Upgrade to strengthen your

retirement savings while managing risk

Use our tactical asset allocation strategies in your retirement portfolio to seek stronger long-term returns while reducing exposure to frothy markets and potential economic slowdowns.

Or choose our fixed income model portfolios, which have outperformed leading bond funds for over a decade,

Or our smart factor and sector rotation portfolios that consistently beat S&P 500 stock index with less risk.

stocks and any other securities could lose money over any period of time. All investments involve risk.

Losses may exceed the principal invested. Past performance is not an indicator of future performance. There

is no guarantee for future results in your investment and any other actions based on the information

provided on the website including, but not limited to, strategies, portfolios, articles, performance data

and results of any tools. All rights are reserved and enforced. By accessing the website, you agree not to

copy and redistribute the information provided herein without the explicit consent from MyPlanIQ.