-

A 6% Default Retirement Savings Rate Is Becoming the Standard—But Is It Enough?

In this issue:

- A 6% default retirement savings rate Is becoming the standard—but Is It enough?

- Bonds for the long-term: why a 60% stock/40% bond portfolio?

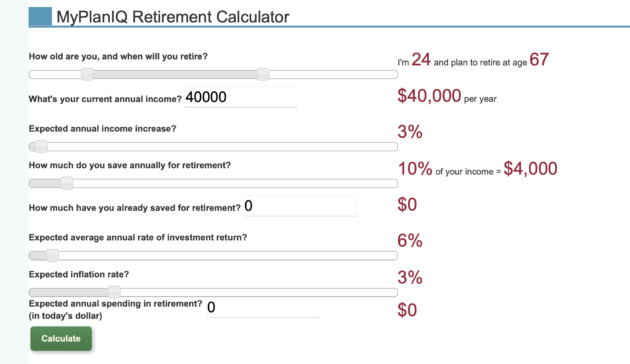

- Retirement calculator: why a 12% to 15% savings rate

- Top 15 employers with the highest employer match per employee

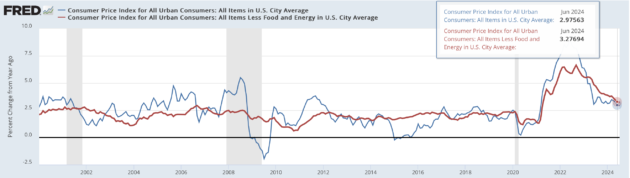

- Market overview: renewed inflation threats

-

How to Maximize Tax-Deferred Retirement Savings Beyond the $69,000 ($70,000 for 2025) IRS Limit

For individuals with multiple income streams, such as physicians, small business owners, startup founders, entrepreneurs, and consultants in tech or other fields, it’s possible to exceed the IRS’s annual limit for tax-deferred retirement savings ($69,000 for 2024 and $70,000 for 2025).

-

Stocks for The Long Term: Why They Outperform Bonds

In this issue:

- Retirement savings: what Morningstar retirement model reveals

- Stocks for the long-term: why they outperform bonds

- Investment arithmetic: investment calculator

- The billion-dollar employer contribution club

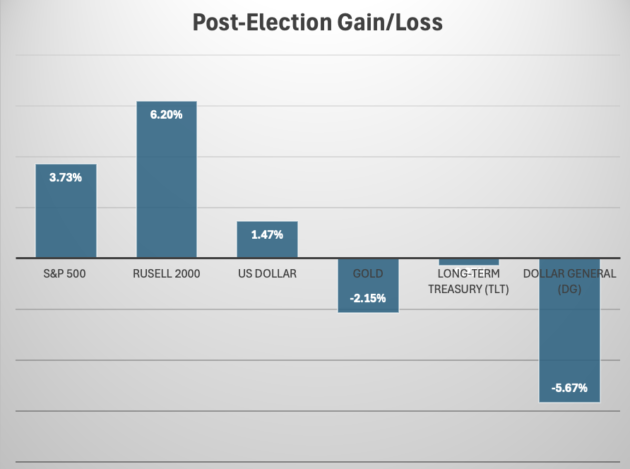

- Market overview: post-election stock rally, inflation …

-

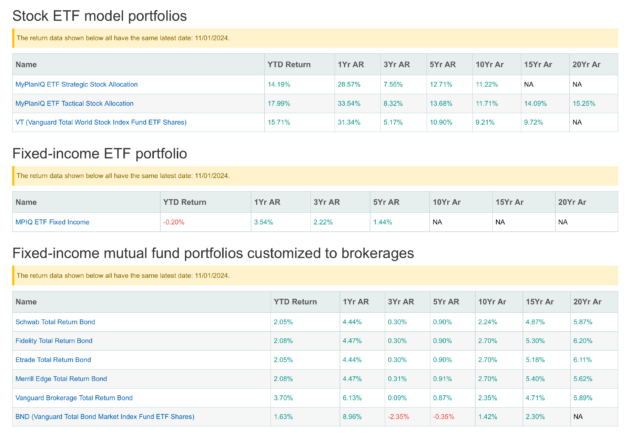

MyPlanIQ Monthly Portfolio Update

We explain our premium portfolios and discuss their holdings. We further discuss several funds that are related to our portfolios. Current economic and financial conditions are also discussed.

-

When to Retire Matters—A Lot!

Retiring at the peak of a bull market or right after a bear market can significantly impact your retirement finances.

-

the-home-depot-futurebuilder Investments

In the following, we show how to construct a balanced, diversified asset allocation portfolio using the investment options available in your plan. We’ll be following the four-step RAID approach: Risk Assessment, Asset Allocation, Investment Selections, and Disciplined Rebalancing. This method ensures your portfolio is well-diversified and aligns with your risk tolerance. Investment Options Available:

- LifePath Retirement Portfolio Fund (BlackRock)

- LifePath 2025 Portfolio Fund (BlackRock)

- LifePath 2030 Portfolio Fund (BlackRock)

- LifePath 2035 Portfolio Fund (BlackRock)

- LifePath 2040 Portfolio Fund (BlackRock)

- LifePath 2045 Portfolio Fund (BlackRock)

- LifePath 2050 Portfolio Fund (BlackRock)

- LifePath 2055 Portfolio Fund (BlackRock)

- LifePath 2060 Portfolio Fund (BlackRock)

- Stable Value Fund (JP Morgan Stable Value)

- Bond Fund (BlackRock Debt Index)

- Balanced Fund (BlackRock Balanced)

- Large Cap Value Fund (Dodge & Cox Stock)

- Large Cap Index Fund (BlackRock Equity Index)

- Large Cap Growth Fund (T.Rowe Price Institutional Large Cap Growth)

- Small-Mid Cap Value Fund (Wedge Capital Management Small/Mid Cap Value)

- Small-Mid Cap Index Fund (BlackRock Extended Equity Market Index)

- Small-Mid Cap Growth Fund (TimesSquare Small/Mid Cap Growth Strategy)

- International Value Fund (Dodge & Cox International Stock)

- International Index Fund (BlackRock MSCI ACWI ex U.S. IMI Index)

- International Growth Fund (GQG Partners)

- Home Depot Stock Fund

The major asset classes covered by these investment options are: US stocks, international stocks and bonds. Each major asset class has index funds represented. It also features two excellent active stock funds from Dodge & Cox. Step 1: Risk Assessment Before deciding on how much to allocate to stocks and bonds, you need to evaluate your risk profile. This involves examining your risk tolerance, age, job stability, and growth expectations. For a comprehensive guide on determining how much should be allocated to stocks, visit MyPlanIQ: Get Started Now. Step 2: Asset Allocation Next, decide on the allocation to each major asset class. Based on the provided investment options, we have US stocks, international stocks and bonds available. For a moderate asset allocation portfolio using only these options, we recommend the following allocation:

- 42% US Stocks

- 18% International Stocks

- 40% Bonds

For more details on asset allocation templates, you can refer to Asset Allocation Portfolio Templates. Step 3: Investment Selections After determining the asset allocation, select specific funds for each asset class. Since we only have US stocks and bonds available, your selections should focus on low-cost index funds if they are available. Here’s an example:

- US Stocks (42%): Allocate 42% of your total investment to Large Cap Index Fund (BlackRock Equity Index) on US stocks or Dodge & Cox Stocks

- International Stocks (18%): Allocate 18% to International Index Fund (BlackRock MSCI ACWI ex U.S. IMI Index) or Dodge & Cox International Stocks

- Bonds (40%): Allocate 40% of your total investment to Bond Fund (BlackRock Debt Index) focusing on bonds.

Step 4: Disciplined Rebalancing Regular monitoring and rebalancing of your portfolio are crucial to maintaining your desired asset allocation. We recommend reviewing your portfolio at least annually. During this review, ensure that the proportions of stocks and bonds remain consistent with your original plan. Adjustments might be necessary to realign with your risk tolerance and financial goals. By following the RAID approach, you’ll be well on your way to building a balanced and diversified portfolio aligned with your risk tolerance and long-term financial goals. Remember, the key to successful investing is staying disciplined and maintaining a long-term perspective.

-

How to Become a 401(k) Millionaire?

Save & invest consistently, dollar-cost average your way to be a 401k millionaire.

-

Introducing the Save More, Grow Wise Newsletter

Introducing Save More, Invest Wise Newsletter that focuses on retirement savings, retirement investments, etirement planning, personal finance topics such as debts and spending, and tools.

-

Comparing Yields on Various Types of Personal Loans: Should You Pay Off or Invest?

Comparing Yields on Various Types of Personal Loans: Should You Pay Off or Invest? Loans are a big part of managing your money, and it’s important to get a handle on how their interest rates work so you can make smart choices. Whether you’re buying a house, getting a car, paying for school, or just covering your expenses, it’s all about knowing when it’s okay to borrow, when to focus on paying things off, and what to do with any extra cash. Don’t forget—sometimes safe investments like Treasury bonds or short-term bond funds might be a better option for your money than paying down certain types of debt if those debts’ interest rates are lower than what’s paid by these safe bond investments! Let’s explore the common types of personal loans—mortgages, credit card debt, car loans, student loans, and other personal loans—and discuss when paying off loans makes sense compared to safe investment options. Loan Types and Their Yields 1. Mortgage Loans

- Yield Range: 2-7% annually

- Purpose: Used to finance the purchase of a home.

- Features:

- Mortgages tend to have the lowest interest rates among personal loans, especially with a fixed-rate, 30-year term.

- Interest may be tax-deductible.

- Consideration: With low interest rates, paying off a mortgage early often isn’t necessary, particularly if you can earn more by investing elsewhere. However, the funds you have allocated to pay off the mortgage should not be touched for other purposes, as it ensures your ability to meet future obligations.

2. Credit Card Debt

- Yield Range: 15-25% annually

- Purpose: Typically used for everyday expenses, emergencies, or convenience.

- Features:

- Credit card debt has one of the highest interest rates, quickly accumulating if not paid off monthly.

- Consideration: This is the type of debt you should pay off as quickly as possible. The interest rates are far too high to justify holding onto the debt while investing elsewhere.

3. Car Loans

- Yield Range: 4-10% annually

- Purpose: Used to finance the purchase of a vehicle.

- Features:

- These loans usually come with fixed rates over a term of 3-7 years.

- Cars depreciate quickly, which makes financing them costly in the long run.

- Consideration: Depending on the interest rate, paying off a car loan early could save you on interest, but it may not be the best move if your loan rate is low.

4. Student Loans

- Yield Range: 4-8% annually

- Purpose: Helps finance higher education.

- Features:

- These loans often come with favorable repayment terms, including deferment and income-based repayment options.

- Consideration: Paying off student loans isn’t urgent if your interest rates are low, especially when other higher-interest debts or better investment opportunities are available.

5. 401(k) Loans

- Yield Range: Prime rate + 1% to 2% (e.g., if the prime rate is 7.5%, the loan’s interest rate will be 8.5% to 9.5%).

- Purpose: Allows borrowing against your retirement savings for emergencies or significant expenses.

- Features:

- Repayments consist of principal and interest, typically made monthly or bi-weekly via payroll deductions.

- Interest repaid goes back into your 401(k), effectively “paying yourself.”

- No credit checks or third-party lender involvement.

- Consideration:

- Reduces the growth potential of your retirement savings during the loan period.

- Leaving your job could require repaying the balance as a lump sum, typically within 60 to 90 days. Failure to do so may result in taxes and penalties.

- Best used as a last resort to avoid jeopardizing long-term retirement goals.

6. Other Personal Loans

- Yield Range: 6-15% annually

- Purpose: Used for a variety of personal expenses, such as medical bills or debt consolidation.

- Features:

- These loans tend to have higher interest rates than secured loans like mortgages but lower than credit card debt.

- Consideration: Paying off high-interest personal loans can be financially wise, but if your rate is closer to the lower end, safe investments may outperform.

Example 1: Should You Pay Off or Invest? Let’s say you have $50,000 in cash and are trying to decide whether to pay off your mortgage with a 4% interest rate or invest in a low-risk option like U.S. Treasury bonds yielding 4.5%.

- Paying Off the Mortgage: If you pay off your mortgage, you effectively “earn” a 4% guaranteed return, which is the interest you won’t have to pay.

- Investing in Treasuries: By investing in Treasury bonds at 4.5%, you’d earn a slightly higher return—$2,250 annually compared to the $2,000 saved by paying off the mortgage.

Conclusion: In this scenario, investing in U.S. Treasuries offers a marginally higher return with the same level of safety. However, the decision may hinge on factors like personal comfort with debt and liquidity needs. If being debt-free provides peace of mind, the difference might not be worth it. Example 2: Why You Shouldn’t Pay Off a 2.2% Mortgage Early Now let’s say you’ve got a 30-year fixed mortgage at 2.2%, one of the lowest rates seen in recent years. Should you use extra cash to pay it off early?

- Paying Off a 2.2% Mortgage: Paying off the mortgage would save you 2.2% annually in interest payments—a low return considering the alternatives.

- Investing in Ultra-Safe Bonds: With U.S. Treasury bonds or ultra-short-term bond funds currently yielding 4-5%, you could almost double your return by investing the cash instead of paying off your mortgage. These investments are also very low-risk, making them an attractive alternative.

Conclusion: In this case, it doesn’t make much sense to pay off a mortgage with such a low interest rate. By investing in safe options like Treasury bonds, you can achieve a higher return with minimal risk. However, it’s crucial that you don’t use the funds intended to pay off the mortgage for anything other than investing. The funds should remain liquid and accessible in case you need them for your mortgage payments down the road. Rules of Thumb to Manage Personal Loans

-

Pay Off High-Interest Loans First

- Example: It’s a no-brainer to first manage your credit card debt that obviously has the highest interest rate! If you have a credit card debt with a 20% APR and a car loan with a 6% interest rate, prioritize paying off the credit card to save on interest costs.

-

Consider Loan Advantages

- Example: A 401(k) loan allows you to repay yourself with interest, which can be more advantageous than taking out a personal loan with higher interest rates. Similarly, some mortgages or student loans offer tax benefits worth retaining.

-

Refinance to Lower Interest Rates

- Example 1: Switch your credit card debt to another credit card debt that has lower interest rate or borrow from your 401(k) to pay off the highest interest rate credit card debt if necessary!

- Example 2: If you’re repaying a 10% personal loan, consider consolidating it into a 6% home equity loan to lower your interest expenses.

Other Key Considerations

- Current Loan Interest vs. Investment Return: If your loan’s interest rate is significantly lower than what you can earn with a safe investment, investing the cash is usually the smarter move.

- High-Interest Debt: Always pay off high-interest debt first (e.g., credit card debt). The interest rates are far higher than what you could safely earn through investments.

- Emergency Fund: Always maintain an emergency fund before paying off debt or investing. This ensures that you have liquidity for unexpected expenses.

- Mortgage Payoff Strategy: While paying off a mortgage can be a guaranteed return, low-rate mortgages (like the 2.2% example) shouldn’t be paid off early if you have access to higher-yielding, low-risk investments. But remember, the funds should remain liquid and be used only for their intended purpose.

- Personal Peace of Mind: If being debt-free offers you significant emotional relief, it may outweigh the financial benefits of investing, even if the math favors the latter.

By carefully balancing loan interest rates with safe investment opportunities, you can maximize your financial outcomes while maintaining security. Safe investments like U.S. Treasury bonds or ultra-short-term bond funds often provide better returns than low-interest loans, but high-interest debt should always be addressed first.

-

Berkshire Hathaway — A Conglomerate of Diversified Holdings as a Fund

In this newsletter, we unveil the ‘best’ long-term stock mutual fund! We discuss its investment methodology and use our own unique tools to measure it against other excellent long-term stock funds.

-

Lessons From the Investment Options Selection of Savvy Investment Companies’ 401(k) Plans

We examine the 401(k) retirement plans from several savvy investment and financial service companies. In particular, we look at their investment options offered in the plans and discuss some of the funds briefly.

-

TIGER GLOBAL MANAGEMENT LLC 401(K) PROFIT SHARING PLAN & TRUST Investments

Constructing a Balanced Asset Allocation Portfolio for TIGER GLOBAL MANAGEMENT LLC 401(K) PROFIT SHARING PLAN & TRUST As a participant in the TIGER GLOBAL MANAGEMENT LLC 401(K) PROFIT SHARING PLAN & TRUST, it’s essential to construct a balanced and diversified asset allocation portfolio to achieve your long-term financial goals. In this article, we’ll guide you through the four-step RAID approach to help you create a well-structured portfolio using the available investment options. Available Investment Options The following investment options are available in the TIGER GLOBAL MANAGEMENT LLC 401(K) PROFIT SHARING PLAN & TRUST:

- Fidelity 500 Index Mutual Fund

- JPMorgan Equity Income Fund Class R6

- Pioneer Fundamental Growth Fund Class Y

- Vanguard Mid-Cap Index Fund Admiral Shares

- BlackRock LifePath Index 2060 K

- Janus Henderson Triton Fund Class N

- BlackRock LifePath Index 2055 K

- Vanguard Information Technology Index Fund Admiral Shares

- BNY Mellon International Stock Fund Class I

- BlackRock LifePath Index 2045 K

- PGIM Total Return Bond Fund – Class Z

- Fidelity Small Cap Index Mutual Fund

- Victory Sycamore Small Company Opportunity Fund Class I

- BlackRock Global Allocation Fund, Inc. Institutional Shares

- BlackRock LifePath Index 2050 K

- BlackRock LifePath Index 2065 K

- Martin Currie Emerging Markets Fund Class I

- MFS Mid Cap Growth Fund Class R3

- BlackRock LifePath Index 2040 K

- BlackRock LifePath Index 2030 K

- BlackRock LifePath Index 2035 K

- BlackRock LifePath Index 2025 K

- BNY Mellon Global Fixed Income Fund – Class I

- John Hancock Funds Disciplined Value Mid Cap Fund Class R6

- Virtus Emerging Markets Opportunities Fund Class A

Major Asset Classes Covered The available investment options cover the following major asset classes: US Stocks: Fidelity 500 Index Mutual Fund, JPMorgan Equity Income Fund Class R6, Pioneer Fundamental Growth Fund Class Y, Vanguard Mid-Cap Index Fund Admiral Shares, Fidelity Small Cap Index Mutual Fund, Victory Sycamore Small Company Opportunity Fund Class I, John Hancock Funds Disciplined Value Mid Cap Fund Class R6International Stocks: BNY Mellon International Stock Fund Class I, Martin Currie Emerging Markets Fund Class I, Virtus Emerging Markets Opportunities Fund Class A Emerging Market Stocks: Martin Currie Emerging Markets Fund Class I, Virtus Emerging Markets Opportunities Fund Class A Real Estate Investments (REITs): None Bonds: PGIM Total Return Bond Fund – Class Z, BNY Mellon Global Fixed Income Fund – Class I Step 1: Risk Assessment Before constructing your portfolio, it’s essential to determine your risk tolerance, age, job stability, and growth expectation. You can use the MyPlanIQ Risk Assessment Tool to help you decide how much to allocate to stocks and bonds. Step 2: Asset Allocation Once you’ve determined your risk profile, you can use the MyPlanIQ Asset Allocation Templates to decide on the optimal allocation to each major asset class. For this example, we’ll use the moderate asset allocation template, which allocates: 42% to US Stocks 18% to International Stocks 0% to REITs (since there are no REIT options available) 40% to Bonds Step 3: Investment Selections Based on the asset allocation template, we can select the following funds for each asset class: US Stocks: Fidelity 500 Index Mutual Fund (24%) and Vanguard Mid-Cap Index Fund Admiral Shares (18%) International Stocks: BNY Mellon International Stock Fund Class I (18%) Bonds: PGIM Total Return Bond Fund – Class Z (30%) and BNY Mellon Global Fixed Income Fund – Class I (10%) Step 4: Disciplined Rebalancing It’s essential to regularly monitor and rebalance your portfolio to ensure it remains aligned with your target asset allocation. You can set a rebalancing schedule, such as quarterly or semi-annually, to review and adjust your portfolio as needed. Example Portfolio Here’s an example of a moderate asset allocation portfolio using the selected funds: Fund Allocation Fidelity 500 Index Mutual Fund 24% Vanguard Mid-Cap Index Fund Admiral Shares 18% BNY Mellon International Stock Fund Class I 18% PGIM Total Return Bond Fund – Class Z 30% BNY Mellon Global Fixed Income Fund – Class I 10% By following the four-step RAID approach and using the available investment options, you can construct a balanced and diversified asset allocation portfolio that aligns with your risk profile and financial goals. Remember to regularly monitor and rebalance your portfolio to ensure it remains on track. Note: The above example is for illustrative purposes only and should not be considered as investment advice. It’s essential to consult with a financial advisor or conduct your own research before making investment decisions.

-

Economic And Financial Market Trends Review

We review the latest economy and financial market trends. We also discuss their impact on investments.

-

aqr-capital-management-llc-401k-plan Investments

Constructing a Balanced, Diversified Asset Allocation Portfolio for AQR Capital Management, LLC 401(K) Plan Participants Creating a balanced and diversified asset allocation portfolio is crucial for long-term financial success. This article will guide you through the four-step RAID approach to help you construct a well-diversified portfolio using the investment options available in the AQR Capital Management, LLC 401(K) Plan. Available Investment Options

- AQR RISK PARITY COLLECTIVE INVESTMENT

- AQR DIVERSIFYING STRG CIF CL G

- PUTNAM STABLE VALUE FUND

- BLACKROCK LIQUIDITY FUNDS FEDFUND

- VANGUARD FEDERAL MONEY MARKET

- VANGUARD TOTAL BOND

- VANGUARD MID CAP INDEX FUND

- VANGUARD INSTITUTIONAL INDEX

- VANGUARD SMALL CAP INDEX ADM

- VANGUARD TOTAL INTL STOCK ADM

- VANGUARD EMERGING MRKTS ADM

- VANGUARD 2055 TARGET RETIREMNT

- VANGUARD 2050 TARGET RETIREMNT

- VANGUARD 2045 TARGET RETIREMNT

- VANGUARD 2040 TARGET RETIREMNT

- VANGUARD 2035 TARGET RETIREMNT

- VANGUARD 2030 TARGET RETIREMNT

- VANGUARD 2025 TARGET RETIREMNT

- VANGUARD 2020 TARGET RETIREMNT

- VANGUARD 2060 TARGET RETIREMNT

- VANGUARD 2065 TARGET RETIREMNT

- FIDELITY INFLATION PROT BD INX

Major Asset Classes Covered

- US Stocks: VANGUARD MID CAP INDEX FUND, VANGUARD INSTITUTIONAL INDEX, VANGUARD SMALL CAP INDEX ADM

- International Stocks: VANGUARD TOTAL INTL STOCK ADM

- Emerging Market Stocks: VANGUARD EMERGING MRKTS ADM

- Bonds: VANGUARD TOTAL BOND, FIDELITY INFLATION PROT BD INX

Step 1: Risk Assessment Determining your risk profile is the first step in constructing your portfolio. Your risk tolerance, age, job stability, and growth expectations are key factors to consider. For a detailed guide on assessing your risk profile, visit MyPlanIQ Risk Assessment Guide. Step 2: Asset Allocation Once you have assessed your risk profile, the next step is to decide how much to allocate to each major asset class. Utilize the allocation templates discussed in MyPlanIQ Asset Allocation Templates to guide your decisions. Example: Moderate Asset Allocation Portfolio Given the available investment options, we can construct a moderate asset allocation portfolio as follows:

- US Stocks: 42% (VANGUARD MID CAP INDEX FUND, VANGUARD INSTITUTIONAL INDEX, VANGUARD SMALL CAP INDEX ADM)

- International Stocks: 18% (VANGUARD TOTAL INTL STOCK ADM)

- Bonds: 40% (VANGUARD TOTAL BOND, FIDELITY INFLATION PROT BD INX)

Step 3: Investment Selections After deciding on the asset allocation, the next step is to select specific funds for each asset class. Emphasize low-cost index funds, especially for the stock portion of your portfolio.

- US Stocks:

- VANGUARD INSTITUTIONAL INDEX (Large Cap)

- VANGUARD MID CAP INDEX FUND (Mid Cap)

- VANGUARD SMALL CAP INDEX ADM (Small Cap)

- International Stocks: VANGUARD TOTAL INTL STOCK ADM

- Bonds:

- VANGUARD TOTAL BOND

- FIDELITY INFLATION PROT BD INX

Step 4: Disciplined Rebalancing Regular monitoring and rebalancing of your portfolio are essential to maintain your desired asset allocation. Rebalance your portfolio at least annually or whenever your asset allocation deviates significantly from your target. Conclusion Constructing a balanced and diversified asset allocation portfolio involves careful planning and disciplined execution. By following the RAID approach and utilizing the available investment options, you can build a portfolio that aligns with your risk tolerance and financial goals. For more detailed guidance, refer to the resources provided by MyPlanIQ.

-

amazon-401k-plan Investments

How to Construct a Balanced, Diversified Asset Allocation Portfolio in Your Amazon 401(k) Plan Participating in the Amazon 401(k) Plan is a great step towards securing your financial future. One of the key aspects of maximizing your retirement savings is constructing a balanced, diversified asset allocation portfolio. This article will guide you through the four-step RAID approach to help you achieve this goal. Investment Options Available in the Amazon 401(k) Plan Before diving into the RAID approach, let’s list the available investment options:

- PIMCO TOTAL RTN II COLLECTIVE TRUST FUND

- VANGUARD TARGET INC COLLECTIVE TRUST FUND

- VANGUARD TARGET 2020 COLLECTIVE TRUST FUND

- VANGUARD TARGET 2025 COLLECTIVE TRUST FUND

- VANGUARD TARGET 2030 COLLECTIVE TRUST FUND

- VANGUARD TARGET 2035 COLLECTIVE TRUST FUND

- VANGUARD TARGET 2040 COLLECTIVE TRUST FUND

- VANGUARD TARGET 2045 COLLECTIVE TRUST FUND

- VANGUARD TARGET 2050 COLLECTIVE TRUST FUND

- VANGUARD TARGET 2055 COLLECTIVE TRUST FUND

- VANGUARD TARGET 2060 COLLECTIVE TRUST FUND

- VANGUARD TARGET 2065 COLLECTIVE TRUST FUND

- HARRIS OAKMRK INTL 3 COLLECTIVE TRUST FUND

- VANG RET SVNG TR II COLLECTIVE TRUST FUND

- VANGUARD TARGET 2070 COLLECTIVE TRUST FUND

- VANG SM VAL IDX INST MUTUAL FUND

- VANG FTSE SOC IDX IS MUTUAL FUND

- VG IS TL INTL STK MK COLLECTIVE TRUST FUND

- VG IS TOT BD MKT IDX COLLECTIVE TRUST FUND

- VANG INST 500 IDX TR COLLECTIVE TRUST FUND

- VANG EXPLORER ADM MUTUAL FUND

- VANG VMMR-FED MMKT MONEY MARKET MF

- AF EUROPAC GROWTH R6 MUTUAL FUND

- AMAZON.COM STOCK

The major asset classes covered by these investment options include:

- US Stocks

- International Stocks

- Bonds

Step 1: Risk Assessment The first step in constructing your portfolio is to assess your risk tolerance. This involves examining factors such as your age, job stability, growth expectations, and overall risk tolerance. Younger investors with a longer time horizon can typically afford to take on more risk, while those closer to retirement may prefer a more conservative approach. To help decide how much of your portfolio should be allocated to stocks versus bonds, you can refer to the guidelines provided by MyPlanIQ. Step 2: Asset Allocation Once you have assessed your risk tolerance, the next step is to decide how much to allocate to each major asset class. A balanced portfolio typically includes a mix of US stocks, international stocks, emerging market stocks, REITs, and bonds. You can utilize the allocation templates discussed in MyPlanIQ’s Asset Allocation Portfolio Templates to guide your decisions. Step 3: Investment Selections After determining your asset allocation, the next step is to select specific funds for each asset class. It’s important to emphasize low-cost index funds whenever possible, as they tend to have lower fees and can provide broad market exposure. Here is an example of how to construct a moderate asset allocation portfolio using the available investment options:

- 42% US Stocks: VANG INST 500 IDX TR COLLECTIVE TRUST FUND (Index Fund)

- 18% International Stocks: VG IS TL INTL STK MK COLLECTIVE TRUST FUND (Index Fund)

- 40% Bonds: VG IS TOT BD MKT IDX COLLECTIVE TRUST FUND (Index Fund)

We note that the plan’s investment options include an excellent active bond fund, the PIMCO Total Return II Collective Trust Fund, which could be used in conjunction with the Vanguard Total Bond Market Index Collective Trust Fund to provide bond exposure. Furthermore, the plan also offers a strong international stock fund, the American Funds EuroPacific Growth R6 Mutual Fund from Capital Group. This fund serves as a good substitute for, or complement to, the VG IS TL INTL STK MK COLLECTIVE TRUST FUND in the international stock asset class. Step 4: Disciplined Rebalancing The final step is to regularly monitor and rebalance your portfolio. Over time, the value of your investments will change, which can cause your asset allocation to drift from your original plan. Rebalancing involves adjusting your portfolio back to your target allocation, which can help manage risk and ensure that your investments remain aligned with your goals. Target Date Funds as an Easy Alternative If you prefer a simpler approach, you can consider investing in target date funds. These funds automatically adjust their asset allocation based on your expected retirement date. For example, if you plan to retire around 2040, you could choose the VANGUARD TARGET 2040 COLLECTIVE TRUST FUND. This fund will gradually become more conservative as you approach retirement. Conclusion Constructing a balanced, diversified asset allocation portfolio in your Amazon 401(k) Plan is a crucial step towards achieving your retirement goals. By following the RAID approach—Risk Assessment, Asset Allocation, Investment Selections, and Disciplined Rebalancing—you can create a portfolio that aligns with your risk tolerance and investment objectives. Remember to utilize low-cost index funds whenever possible and consider target date funds for a simpler investment strategy.

-

Mega Backdoor Roth Explained

The Mega Backdoor Roth 401(k) or Mega Backdoor Roth Conversion is a powerful tool for high-income earners who want to maximize their retirement savings and enjoy tax-free withdrawals. By leveraging this strategy, you can compound your savings dramatically over time, providing significant long-term financial benefits.

-

harris-associates-lp-profit-sharing-and-savings-plan Investments

Constructing a Balanced, Diversified Asset Allocation Portfolio: A Guide for Participants in Harris Associates L.P. Profit Sharing and Savings Plan Learning how to construct a balanced and diversified asset allocation portfolio is crucial for achieving your long-term financial goals. This article offers a systematic four-step RAID approach (Risk Assessment, Asset Allocation, Investment Selections, and Disciplined Rebalancing) to help you navigate your investment options effectively. Available Investment Options

- SCHWAB FUNDS SELF-DIRECTED BROKERAGE ACCOUNTS

- OAKMARK SELECT REGISTERED INVESTMENT COMPANY

- OAKMARK GLOBAL SELECT REGISTERED INVESTMENT COMPANY

- OAKMARK INTERNATIONAL SMALL CAP REGISTERED INVESTMENT COMPANY

- HARRIS ASSOCIATES OAKMARK CIT COLLECTIVE INVESTMENT TRUST

- HARRIS ASSOCIATES OAKMARK EQUITY & INCOME CIT COLLECTIVE INVESTMENT TRUST

- HARRIS ASSOCIATES OAKMARK GLOBAL CIT COLLECTIVE INVESTMENT TRUST

- HARRIS ASSOCIATES OAKMARK INTERNATIONAL CIT COLLECTIVE INVESTMENT TRUST

- VANGUARD SM CAP INDEX ADM REGISTERED INVESTMENT COMPANY

- VANGUARD TGT RMT INC INV FUND REGISTERED INVESTMENT COMPANY

- VANGUARD TGT RMT 2020 INV FUND REGISTERED INVESTMENT COMPANY

- VANGUARD TGT RMT 2025 INV FUND REGISTERED INVESTMENT COMPANY

- VANGUARD TGT RMT 2030 INV FUND REGISTERED INVESTMENT COMPANY

- VANGUARD TGT RMT 2035 INV FUND REGISTERED INVESTMENT COMPANY

- VANGUARD TGT RMT 2040 INV FUND REGISTERED INVESTMENT COMPANY

- VANGUARD TGT RMT 2045 INV FUND REGISTERED INVESTMENT COMPANY

- VANGUARD TGT RMT 2050 INV FUND REGISTERED INVESTMENT COMPANY

- VANGUARD TGT RMT 2055 INV FUND REGISTERED INVESTMENT COMPANY

- VANGUARD TGT RMT 2060 INV FUND REGISTERED INVESTMENT COMPANY

- VANGUARD TGT RMT 2065 INV FUND REGISTERED INVESTMENT COMPANY

- VANGUARD TTL BD MKT IDX ADM FUND REGISTERED INVESTMENT COMPANY

- VANGUARD INST IDX INST FUND REGISTERED INVESTMENT COMPANY

- VANGUARD TTL INTL STK INDEX ADM FUND REGISTERED INVESTMENT COMPANY

- VANGUARD TREASURY MONEY MARKET FUND REGISTERED INVESTMENT COMPANY

Major Asset Classes Covered The investment options provided cover the following major asset classes:

- US Stocks

- International Stocks

- Emerging Market Stocks

- Real Estate Investments (REITs)

- Bonds

Step 1: Risk Assessment Your risk profile will guide how much of your portfolio should be allocated into stocks versus bonds. Key questions to consider include:

- What is your risk tolerance?

- How old are you?

- What is your current job stability?

- What are your growth expectations?

To help you construct your own risk profile and decide your stock allocation, please refer to this resource. Step 2: Asset Allocation Your next step is to determine how to allocate your investments across major asset classes. Based on various risk profiles (conservative, moderate, aggressive), templates are available to guide your decisions. You can find allocation templates here. Step 3: Investment Selections Once you have determined your asset allocation, it’s time to select specific funds for each asset class. Low-cost index funds are particularly important for the stock portion of your portfolio. Among the available options, consider using:

- US Stocks: VANGUARD INST IDX INST FUND

- International Stocks: VANGUARD TTL INTL STK INDEX ADM FUND

- Bonds: VANGUARD TTL BD MKT IDX ADM FUND

Step 4: Disciplined Rebalancing Regularly monitor your portfolio and rebalance it to maintain your desired asset allocation. This involves buying or selling assets to ensure your portfolio stays aligned with your original asset allocation strategy. Example: Constructing a Moderate Asset Allocation Portfolio Let’s assume you’re constructing a portfolio using the asset allocation of 36% US Stocks, 18% International Stocks, 6% REITs, and 40% Bonds. For this allocation, you would use:

- 36% US Stocks: VANGUARD INST IDX INST FUND

- 18% International Stocks: VANGUARD TTL INTL STK INDEX ADM FUND

- 6% REITs: (If applicable, REIT options are limited here)

- 40% Bonds: VANGUARD TTL BD MKT IDX ADM FUND

In conclusion, a balanced and diversified asset allocation portfolio can pave the way for financial stability and growth. Use the RAID approach outlined in this article to take charge of your retirement planning through the Harris Associates L.P. Profit Sharing and Savings Plan.

-

value-line-inc-profit-sharing-and-savings-plan Investments

Constructing a Balanced, Diversified Asset Allocation Portfolio for VALUE LINE, INC. PROFIT SHARING AND SAVINGS PLAN Participants Creating a balanced and diversified asset allocation portfolio is crucial for long-term financial success. This article will guide you through the four-step RAID approach to help you construct a well-rounded portfolio using the investment options available in the VALUE LINE, INC. PROFIT SHARING AND SAVINGS PLAN. Investment Options Here are the available investment options:

- MASSMUTUAL GUARANTEED INTEREST ACCOUNT

- AMERICAN FUNDS AMER FUNDS BALANCED FUND

- AMERICAN FUNDS AMERICAN FUNDS NEW WORLD FUND

- BLACKROCK BLACKROCK GLOBAL ALLOCATION FUND

- BNY MELLON BNY MELLON BOND MARKET INDEX FUND

- LEGG MASON CLEARBRIDGE MID CAP FUND

- WILMINGTON TRUST WILMINGTON TRUST AMRCN FD 2030 CIT

- GOLDMAN SACHS GOLDMAN SACHS SMCAP GR INSIGHTS FD

- INVESCO INVESCO GOLD & SPECIAL MINERALS FD

- INVESCO INVESCO OPPENHEIMER INTL GROWTH FD

- INVESCO INVESCO REAL ESTATE FUND

- WELLS FARGO ALLSPRING SPEC MID CP VAL FD

- NATIXIS FUNDS LOOMIS SAYLES STRATEGIC INCOME FUND

- MASSMUTUAL SELECT MASSMUTUAL BLUE CHIP GROWTH FUND

- MASSMUTUAL PREMIER MASSMUTUAL CORE BOND FUND

- MASSMUTUAL SELECT MASSMUTUAL DIVERSIFIED VALUE FUND

- MASSMUTUAL PREMIER MASSMUTUAL GLOBAL FUND

- MASSMUTUAL PREMIER MASSMUTUAL HIGH YIELD FUND

- MASSMUTUAL PREMIER MASSMUTUAL INF-PRO AND INC FUND

- MASSMUTUAL SELECT MASSMUTUAL MID CAP GROWTH FUND

- MASSMUTUAL SELECT MASSMUTUAL OVERSEAS FUND

- MASSMUTUAL SELECT MASSMUTUAL SM CAP VALUE EQUITY FD

- MASSMUTUAL SELECT MASSMUTUAL SMALL COMPANY VALUE FUND

- MFS INVESTMENT MANAGEMENT MFS UTILITIES FUND

- MASSMUTUAL SELECT MM MSCI EAFE INTL INDX FD (NRTN TR)

- MASSMUTUAL SELECT MM RSL 2000 SMCAP INDX FD (NRTN TR)

- MASSMUTUAL SELECT MM S&P 500 INDEX FD (NORTHERN TRUST)

- MASSMUTUAL SELECT MM S&P MID CAP INDEX FUND (NRTN TR)

- PARNASSUS PASNASSUS CORE EQUITY FUND

- FRANKLIN/TEMPLETON TEMPLETON GLOBAL TOTAL RETURN FUND

- PIMCO FUNDS TOTAL RETURN FUND (PIMCO)

- WELLS FARGO ALLSPRING INTERNATIONAL EQ FD

Major Asset Classes Covered The major asset classes covered by these investment options are:

- US Stocks

- International Stocks

- Emerging Market Stocks

- Real Estate Investments (REITs)

- Bonds

Step 1: Risk Assessment Before constructing your portfolio, it’s essential to assess your risk profile. This involves determining how much you should allocate to stocks and bonds based on your risk tolerance, age, job stability, and growth expectations. For a detailed guide on how to decide your stock allocation, refer to MyPlanIQ’s guide. Step 2: Asset Allocation Once you’ve assessed your risk profile, the next step is to decide how much to allocate to each major asset class. Utilize the allocation templates discussed in MyPlanIQ’s asset allocation templates for 401(k) investments. Step 3: Investment Selections After deciding on your asset allocation, the next step is to select specific funds for each asset class. It’s crucial to emphasize low-cost index funds, especially for the stock portion of your portfolio. Step 4: Disciplined Rebalancing Regular monitoring and rebalancing of your portfolio are essential to maintain your desired asset allocation. This involves periodically reviewing your portfolio and making necessary adjustments to ensure it aligns with your risk profile and investment goals. Example: Constructing a Moderate Asset Allocation Portfolio Given the available investment options, let’s construct a moderate asset allocation portfolio. Since we have US stocks, international stocks, REITs, and bonds covered, we’ll use the following allocation:

- 36% US Stocks

- 18% International Stocks

- 6% REITs

- 40% Bonds

US Stocks (36%)

- MASSMUTUAL SELECT MM S&P 500 INDEX FD (NORTHERN TRUST)

- MASSMUTUAL SELECT MASSMUTUAL BLUE CHIP GROWTH FUND

- MASSMUTUAL SELECT MASSMUTUAL DIVERSIFIED VALUE FUND

International Stocks (18%)

- MASSMUTUAL SELECT MM MSCI EAFE INTL INDX FD (NRTN TR)

- WELLS FARGO ALLSPRING INTERNATIONAL EQ FD

REITs (6%)

- INVESCO INVESCO REAL ESTATE FUND

Bonds (40%)

- BNY MELLON BNY MELLON BOND MARKET INDEX FUND

- PIMCO FUNDS TOTAL RETURN FUND (PIMCO)

By following these steps and utilizing the available investment options, you can construct a balanced and diversified asset allocation portfolio that aligns with your risk profile and investment goals. Regular monitoring and disciplined rebalancing will help ensure your portfolio remains on track for long-term financial success.

-

llama3.1 Calculator Example

Contributions: Participants can contribute between 6% and 20% of their eligible pay to the Plan. Company match: The Company matches the minimum 6% contribution with an amount equal to 7% of the participant’s eligible pay. However, Company matching contributions were suspended from October 1, 2020, until they were reinstated on October 1, 2021. Participants who are 50 or older during the plan year and have maximized their regular pretax and Roth contributions can make additional contributions. Vesting: Participants are immediately vested in their own contributions and all associated earnings. Company contributions vest at 100% after 3 years of service, upon reaching age 65 while employed, or upon death while still an employee. 401(k) Contribution Calculator Bi-Weekly Pay Amount: Age: Calculate function calculateMatch() { const payAmount = parseFloat(document.getElementById(‘payAmount’).value); const age = parseInt(document.getElementById(‘age’).value); const annualLimit = 23000; const catchUpLimit = 7500; let contributionLimit = annualLimit; if (age >= 50) { contributionLimit += catchUpLimit; } const numPayPeriods = 26; // Bi-weekly pay periods in a year const maxContributionPerPaycheck = contributionLimit / numPayPeriods; // Contribution between 6% and 20% of pay const minContributionPercentage = 0.06; const maxContributionPercentage = 0.20; // Company match policy const minMatchPercentage = 0.07; // To maximize the match, we need to contribute at least 6% of pay const minimumContribution = payAmount * minContributionPercentage; const matchPerPaycheck = Math.min(minimumContribution * minMatchPercentage, payAmount * minMatchPercentage); const annualMaxMatch = matchPerPaycheck * numPayPeriods; // Output results document.getElementById(‘contributionAmount’).innerText = `Each Paycheck Contribution Amount: $${minimumContribution.toFixed(2)}`; document.getElementById(‘paycheckMatch’).innerText = `Each Paycheck Match Amount: $${matchPerPaycheck.toFixed(2)}`; document.getElementById(‘annualMaxMatch’).innerText = `Annual Maximum Match Amount: $${annualMaxMatch.toFixed(2)}`; document.getElementById(‘annualContribution’).innerText = `Annual Contribution Amount: $${Math.min(contributionLimit, minimumContribution * numPayPeriods).toFixed(2)}`; }

-

Constructing a Balanced, Diversified Asset Allocation Portfolio for Blue Shield of California Tax Deferred Salary Investment Plan Participants

Participating in the Blue Shield of California Tax Deferred Salary Investment Plan offers a solid foundation for your retirement savings. To maximize the potential of your retirement plan, understanding how to construct a balanced and diversified asset allocation portfolio is crucial. This article will guide you through a structured four-step RAID approach: Risk assessment, Asset allocation, Investment selections, and Disciplined rebalancing. Investment Options Below are your available investment options within the plan:

- FIDELITY BROKERAGELINK MUTUAL FUNDS

- FIDELITY EXTENDED MARKET INDEX FUND MUTUAL FUNDS

- FIDELITY GOVERNMENT CASH RESERVES MUTUAL FUNDS

- FIDELITY U.S. BOND INDEX FUND MUTUAL FUNDS

- BLACKROCK TOTAL RETURN BOND FUND M

- DIAMOND HILL LARGE CAP PORTFOLIO FEE CLASS L

- FIDELITY GROWTH COMPANY COMINGLED POOL CLASS 3

- GALLIARD STABLE VALUE FUND X

- HARDING LOEVNER INTERNATIONAL EQUITY – CLASS BN

- SPARTAN 500 INDEX POOL CLASS E

- STATE STREET TARGET RETIREMENT INCOME FUND CLASS IV

- STATE STREET TARGET RETIREMENT 2020 FUND CLASS IV

- STATE STREET TARGET RETIREMENT 2025 FUND CLASS IV

- STATE STREET TARGET RETIREMENT 2030 FUND CLASS IV

- STATE STREET TARGET RETIREMENT 2050 FUND CLASS IV

- STATE STREET TARGET RETIREMENT 2055 FUND CLASS IV

- STATE STREET TARGET RETIREMENT 2060 FUND CLASS IV

- THE PRINCIPAL DIVERSIFIED REAL ASSET COLLECTIVE INVESTMENT FUND

- VANGUARD INSTITUTIONAL TOTAL INTERNATIONAL STOCK MARKET INDEX TRUST

- WTC-CIF II SMID-CAPE RESEARCH EQUITY SERIES 4

These options cover the following major asset classes:

- US stocks: FIDELITY EXTENDED MARKET INDEX FUND, DIAMOND HILL LARGE CAP PORTFOLIO, FIDELITY GROWTH COMPANY COMINGLED POOL, SPARTAN 500 INDEX POOL, WTC-CIF II SMID-CAPE RESEARCH EQUITY SERIES

- International stocks: HARDING LOEVNER INTERNATIONAL EQUITY, VANGUARD INSTITUTIONAL TOTAL INTERNATIONAL STOCK MARKET INDEX TRUST

- REITs: THE PRINCIPAL DIVERSIFIED REAL ASSET

- Bonds: FIDELITY GOVERNMENT CASH RESERVES, FIDELITY U.S. BOND INDEX FUND, BLACKROCK TOTAL RETURN BOND FUND, GALLIARD STABLE VALUE FUND

Four-Step RAID Approach 1. Risk Assessment Determining your risk profile is the first step. Consider factors such as your age, risk tolerance, job stability, and growth expectations. This comprehensive guide on how to decide your stock allocation can assist in defining your risk profile. Generally, younger investors with longer investment horizons and higher risk tolerance can allocate a larger portion of their portfolio to stocks. Conversely, older investors closer to retirement might prefer a higher allocation to bonds for capital preservation. 2. Asset Allocation Next, decide on the allocation to each major asset class. You can refer to these asset allocation templates for guidance based on your risk profile. Given the available investment options, we cover portfolios for the following major asset classes: US stocks, international stocks, REITs, and bonds. Example of a Moderate Asset Allocation Portfolio:

- 36% US stocks

- 18% International stocks

- 6% REITs

- 40% Bonds

3. Investment Selections Select funds for each asset class:

- US Stocks (36%): Allocate to Spartan 500 Index Pool Class E, Fidelity Growth Company Commingled Pool Class 3, Diamond Hill Large Cap Portfolio Fee Class L

- International Stocks (18%): Allocate to Vanguard Institutional Total International Stock Market Index Trust, Harding Loevner International Equity Class BN

- REITs (6%): The Principal Diversified Real Asset Collective Investment Fund

- Bonds (40%): Fidelity U.S. Bond Index Fund, BlackRock Total Return Bond Fund M

4. Disciplined Rebalancing Regularly monitor your portfolio and rebalance it to maintain your desired asset allocation. Over time, asset performance will cause your allocations to drift. Rebalancing ensures you stay on track to achieve your long-term investment goals. Prioritize low-cost index funds where possible, particularly for the stock portion of your portfolio, to maximize returns by minimizing fees. By following the RAID approach and using the recommended resources, you can effectively construct a balanced and diversified asset allocation portfolio. This will help you achieve your retirement goals in a disciplined and structured manner.