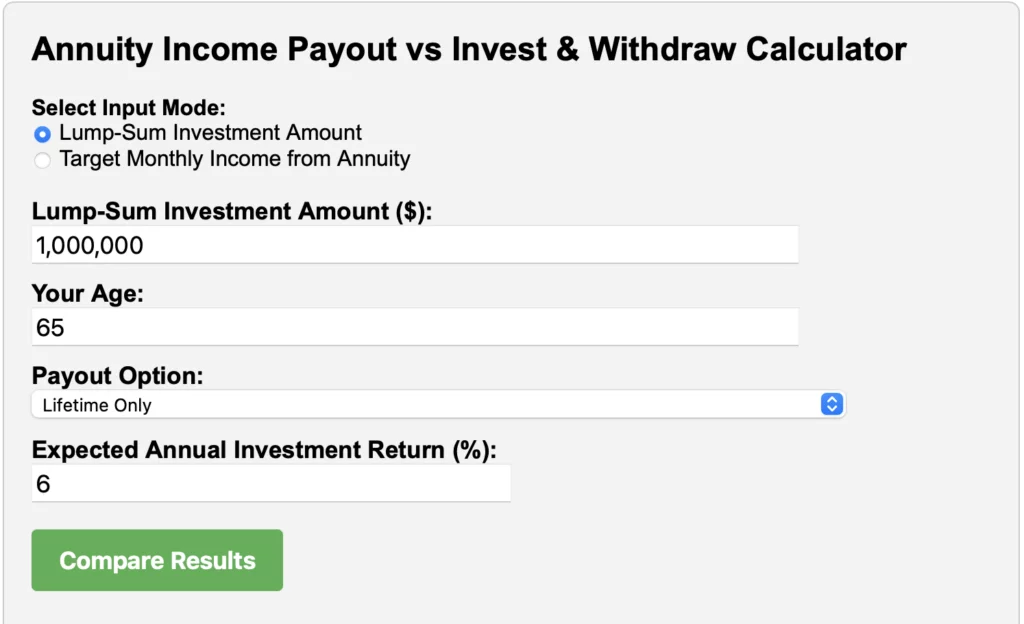

The calculator results below show something interesting. With a $1,000,000 lump sum and a 6% expected investment return, you could buy a lifetime annuity that pays about $5,416 per month. Or, you could try to self-manage and withdraw the same income amount each year from your own investment account.

By age 100, that second strategy would’ve depleted your portfolio. It runs out completely at around age 110. So, that’s the trade.

Reliability vs Flexibility

The main difference isn’t really about return. It’s about certainty.

Annuity gives you a guaranteed monthly income for life. It doesn’t matter how long you live or what the markets do. You won’t run out.

With a self-managed portfolio, nothing is guaranteed. Sure, the expected return is 6% in this simulation, and that’s not unreasonable for a balanced long-term portfolio. But in real life, markets are volatile, and return isn’t linear. If early years underperform or you live longer than expected, there’s a chance you outlive the portfolio.

Except, in this particular example, withdrawing that same $5,416 monthly amount would actually last until around age 105. Which is already well beyond average life expectancy. So if you pass away at 90 or 95, you’d still have hundreds of thousands left in the portfolio. That money stays with you or goes to your heirs. It doesn’t disappear.

Not so with the annuity shown here. This version is lifetime only, which means the checks stop when you do. There’s no residual value. No inheritance. That’s the price of certainty. You’ve handed over the principal in exchange for a guaranteed stream.

And part of that pricing includes the provider’s own cut. Because they’re not doing this for free.

Every annuity has built-in costs. Administrative fees, risk charges, profit margins. The difference between what the provider earns on your capital and what they pay you out is their markup. That’s how they stay in business. Some view that cost as too high. Others find it acceptable, even comforting, knowing that someone else is bearing the risk.

It really depends on your situation. If longevity risk is your top concern, then paying that markup might feel totally worth it. But if you’re healthy, have other sources of income, or want to leave something behind, it could feel steep.

How Much Can You Safely Spend?

Here’s another angle. The annuity is paying out over 6% of your original capital each year. That’s generous. It’s more than what’s generally considered sustainable from a long-term portfolio.

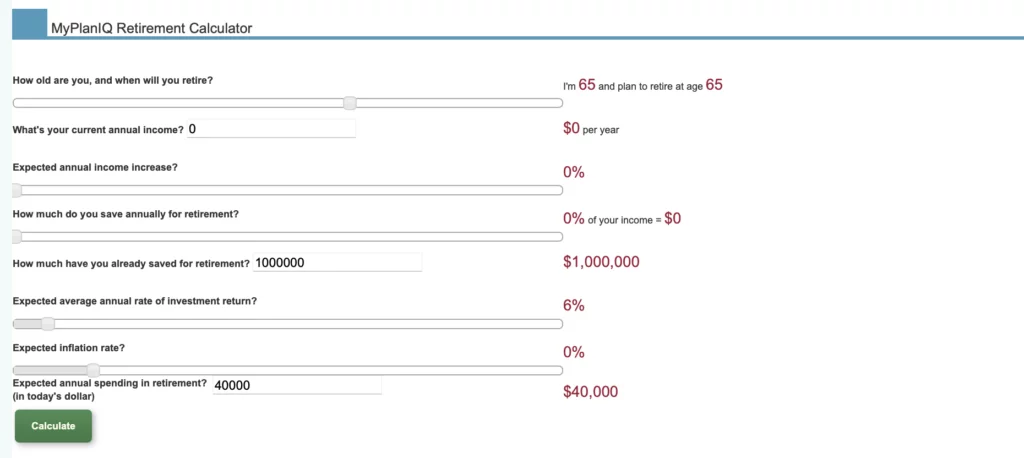

If instead you drew just 4%, you’d only be taking $3,333 per month. Not quite as exciting. But that amount could last decades longer. Possibly forever. The portfolio would likely survive into your 100s, even under mild market stress. And still leave something for heirs.

To be precise, we can pull up our Retirement Calculator and enter the numbers and here is the result:

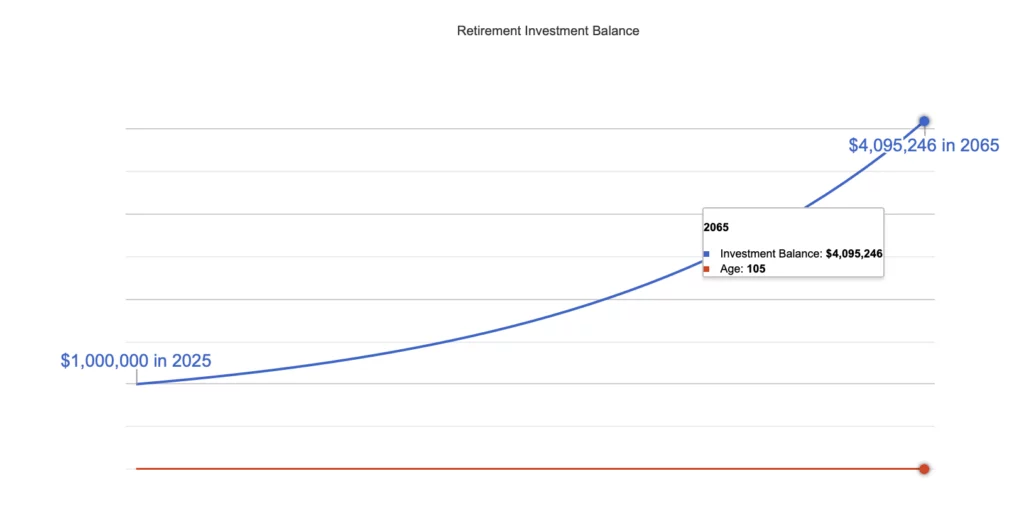

So, spending $40,000 or $3,3333 a month on a $1,000,000 investment portfolio with 6% annual return would actually get you $4 million left when you are 105 years old!

So yes, annuities offer more income. But investing gives you more flexibility. More control. More optionality.

That has its own value.

What If You Combine Both?

This doesn’t have to be binary.

You can annuitize part of your capital to guarantee a base income. Just enough to cover essentials. Then invest the rest for growth, liquidity, and optional needs. That blended approach gives you both reliability and flexibility.

It also gives you choices. Which is often the most underrated feature in any financial plan.

One More Thing to Think About

Longevity risk is real. And often overlooked.

If you’re in good health or have a family history of long lives, the argument for locking in some guaranteed income gets stronger.

At the same time, inflation is a long-term drag. Most annuities are fixed. Their purchasing power declines over time. A self-managed portfolio, even with modest withdrawals, has at least a chance to keep up.

So again, there’s no silver bullet. Only trade-offs.

Summary

This tool shows you the math. But real life doesn’t follow straight lines.

How long you live, how markets behave, what you actually spend. None of it is predictable. Which is why pure reliance on either side feels risky. Too much annuity, and you lose flexibility. Too much portfolio, and you carry all the risk.

Most people don’t need extremes. They just need enough to feel secure.

That’s why middle ground matters.