November 11, 2019: Market Indicator And Momentum

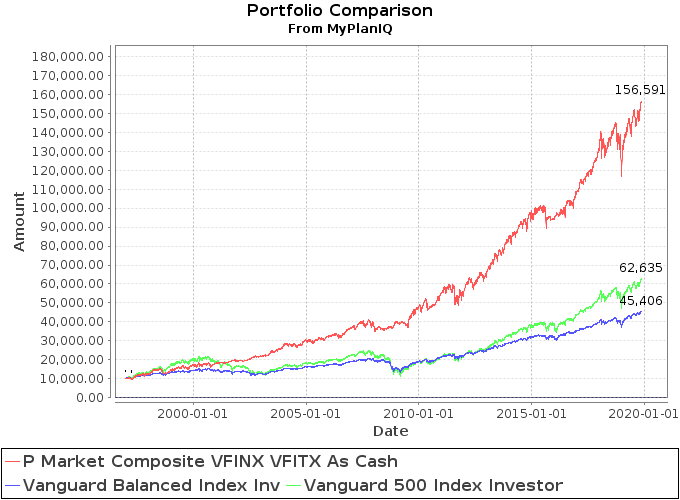

We introduce composite momentum that’s a combination of our market indicator and momentum. We show good improvement on portfolios’ returns.

We introduce composite momentum that’s a combination of our market indicator and momentum. We show good improvement on portfolios’ returns.

We introduce a factor ETF rotation portfolio based on momentum of these ETFs. The results show that the portfolio can improve static allocation portfolios.

We look at multi-factor (value, quality, low volatility and momentum) ETFs and portfolios. We believe factor ETFs can add good value to an asset allocation portfolio.

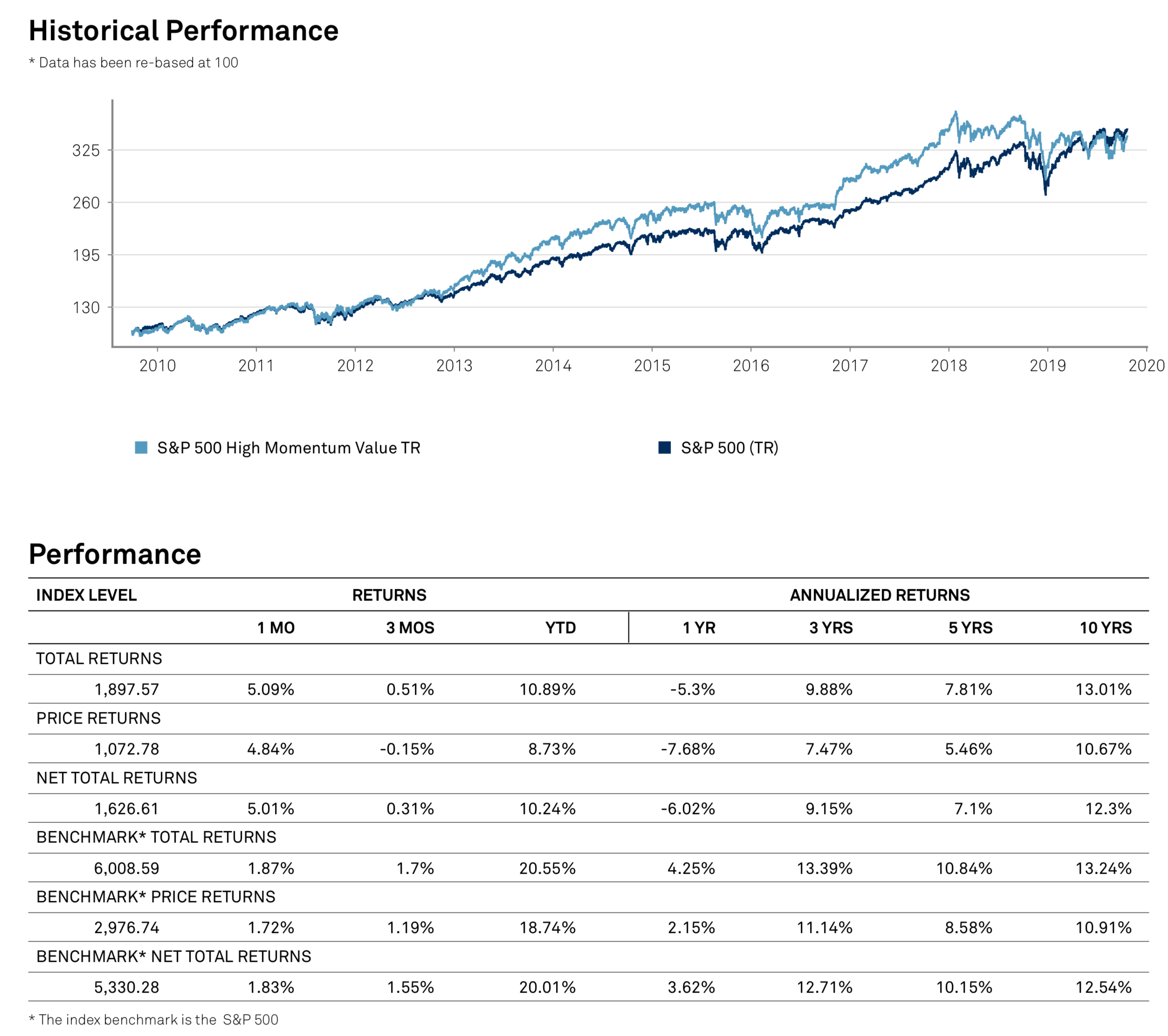

We look at value-momentum combined ETFs.

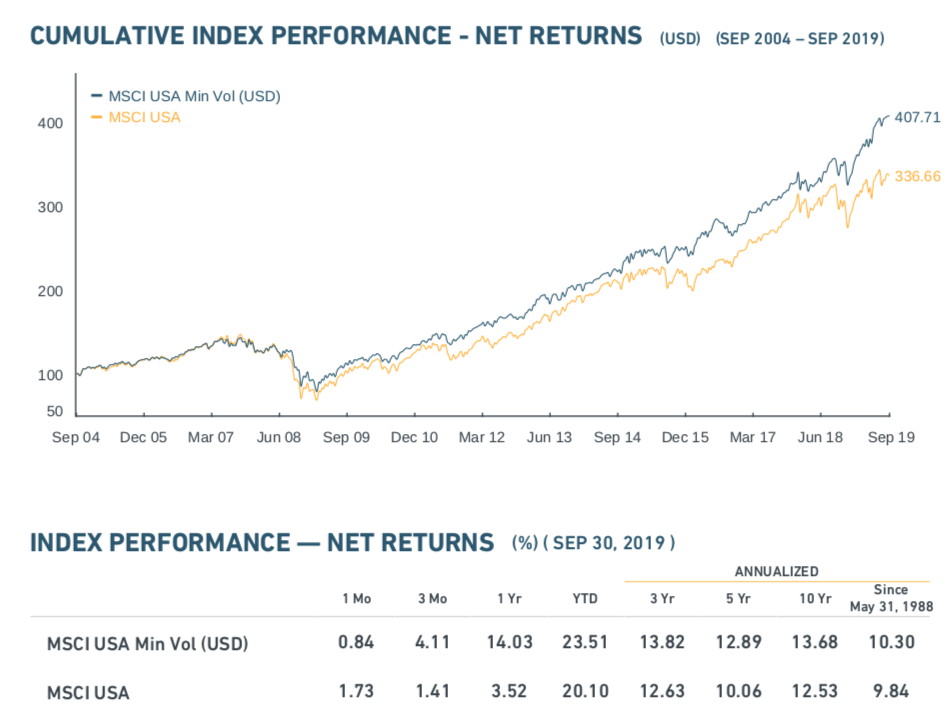

Low volatility factor can indeed outperform broad base stock indexes.