-

William Bernstein Sheltered Sam 60/40 Allocation desc

William Bernstein, a renowned financial author and investment advisor, provides valuable insights into building winning portfolios in his book “The Four Pillars of Investing: Lessons for Building a Winning Portfolio.” One of the portfolio strategies he advocates is known as the Sheltered Sam portfolio. This portfolio is designed to offer diversification and asset allocation using a combination of low-cost index funds and ETFs (exchange-traded funds). The rationale behind the Sheltered Sam portfolio is to achieve a balanced mix of asset classes that can withstand market volatility while delivering satisfactory long-term returns. Bernstein emphasizes the importance of diversifying across various asset classes to reduce risk and enhance overall portfolio performance. The portfolio allocations are structured based on different risk tolerances and desired asset allocations, ranging from conservative to aggressive. Below is a table illustrating the asset allocations for the Sheltered Sam portfolio with a 60/40 allocation: Asset Class Allocation US Large Cap Value (VTV) 15.00% US Large Cap (VV) 12.00% US Small Cap Value (VIOV) 9.00% US Small Cap (VIOO) 3.00% REITs (VNQ) 6.00% Emerging Markets (VWO) 3.00% Pacific Stocks (VPL) 3.00% European Stocks (VGK) 3.00% International Large Cap Value (EFV) 4.20% Short-Term Treasuries (VGSH) 24.00% Precious Metals (GLTR) 1.80% TIPS (VTIP) 16.00% In this allocation, 60% of the portfolio is allocated to stocks, while 40% is allocated to bonds. The stock portion comprises a mix of US large-cap and small-cap stocks, international stocks, emerging market stocks, and real estate investment trusts (REITs). The bond portion consists of short-term treasuries and Treasury Inflation-Protected Securities (TIPS). By following this asset allocation, investors can benefit from broad diversification across different market segments and asset classes. The use of low-cost index funds and ETFs helps keep expenses down while providing exposure to the overall market performance. The Sheltered Sam portfolio approach offers a long-term investment strategy suitable for those seeking a balanced, low-maintenance, and cost-effective investment solution.

-

William Bernstein Cowards desc

William Bernstein Cowards Portfolio: A Simple Choice for 401(k) and IRA Investors Investing, you know, it’s one of those things that sounds simple but gets messy fast. Everyone’s got an opinion. Everyone’s got a hot tip. But what if you just want something that works, something that doesn’t need you to check the market every day? That’s where the William Bernstein Cowards Portfolio comes in. It’s not flashy. It’s not trying to beat the market. It’s just, well, sensible. And for folks saving for retirement in a 401(k) or an IRA, or even a taxable brokerage account, sensible can be enough. William Bernstein, if you haven’t come across him, is a thinker who’s been around the block. He’s a neurologist turned investment writer, which is an odd path, but it gives him a certain clarity. His books, like The Intelligent Asset Allocator, they cut through the noise. The Cowards Portfolio, it’s his way of saying, you don’t need to be a hero to invest well. You just need a plan that’s diversified, low-cost, and built for the long haul. Is it popular? Hard to say. It’s not the kind of thing that gets hyped on social media, but it’s got a quiet following among people who like to keep things simple. William Bernstein Cowards Portfolio Holdings Let’s break down what’s in this portfolio. It’s a mix of funds, each doing a specific job. Here’s the lineup: So what’s the deal here? You’ve got U.S. stocks, international stocks, and bonds, which cover the major asset classes. There’s also a nod to REITs for inflation protection, and that hefty cash allocation, which is unusual. No gold or commodities, so it’s not quite like the Harry Browne Permanent Portfolio, which uses gold to fight inflation. No long-term bonds either, so you’re not getting that deflation hedge Browne talks about. The cash, though, that’s a standout. It’s like Bernstein’s saying, sometimes it’s okay to just sit tight. In fact, this is mostly likely where the word ‘Cowards’ came from. Diversification is solid. You’ve got exposure to large and small companies, value stocks, developed and emerging markets, real estate, and short-term bonds. Risk? It’s moderate. The 40% in stocks and 5% in REITs give you growth potential, but the 40% in bonds and 25% in cash keep things from getting too wild. If markets tank, you’re not going to lose your shirt. But if stocks soar, you might lag a bit. That’s the trade-off. It’s for people who want growth but can’t stomach big swings. Retirees, maybe, or folks who just don’t trust the market’s mood swings. Using the Cowards Portfolio in 401(k) and IRA Accounts Now, how do you actually use this in a 401(k) or IRA? First, check your 401(k) plan’s fund options. You’re looking for index funds that match the asset classes in the Cowards Portfolio. For U.S. stocks, a total market fund like VTI or an S&P 500 fund is fine. For value or small-cap, you might need to dig. If your plan doesn’t have exact matches, say, no small-cap value fund, look for a diversified active fund. Check its expense ratio and diversification on Morningstar.com. High fees or narrow focus? Pass. Rule of thumb: for stock funds, prioritize index funds, especially low-cost ones. For bonds, go for core bond funds or high-quality actively managed total return bond funds (see here). If your 401(k) doesn’t have emerging market funds, map that 5% to international stocks. Small-cap missing? Shift to large-cap stocks. REITs not there? Use U.S. stocks. Cash can be a money market fund or even a stable value fund if your plan has one. In an IRA, it’s easier. You can buy the exact ETFs listed: VTI, VTV, and so on. No need to compromise. The portfolio’s risk level suits conservative investors or those nearing retirement. If you’re younger and want more risk, you can scale up the stock allocation. How do you know your risk tolerance? Try an Asset Allocation Calculator like MyPlanIQ’s. Answer a few questions, and it’ll tell you how much to put in stocks versus bonds. Then adjust the Cowards Portfolio accordingly. Maybe bump stocks to 50% and cut cash to 15%. It’s flexible. Using the Cowards Portfolio in Taxable Accounts For taxable brokerage accounts, the Cowards Portfolio is a good fit. Why? It’s built on index ETFs, which are tax-efficient. They don’t churn their holdings much, so you’re not hit with big capital gains distributions. The buy-and-hold nature of the portfolio also helps. You’re not trading in and out, so you’re not triggering taxes every year. Rebalance once a year, maybe, and call it a day. Tax-loss harvesting? It’s an option. If VWO (emerging markets) takes a dip, you could sell it, book the loss for tax purposes, and buy a similar fund (not identical, to avoid wash-sale rules). But don’t overdo it. The Cowards Portfolio is about simplicity, not gaming the tax code. Keep it straightforward, and you’ll keep Uncle Sam at bay. Final Thoughts The William Bernstein Cowards Portfolio, it’s not going to make you rich overnight. It’s not trying to. It’s for people who’ve seen a market cycle or two, who know that slow and steady usually wins. Is it perfect? Probably not. That big cash allocation, it might drag returns in a bull market. But when things get rough, you’ll be glad it’s there. For 401(k) or IRA investors, it’s a blueprint you can tweak to fit your plan. For taxable accounts, it’s low-maintenance and tax-friendly. Maybe it’s not the only way to invest, but it’s a way that makes sense. And sometimes, that’s enough.

-

Armstrong Ideal Index desc

Armstrong Ideal Index: Comprehensive Overview 1. Background and Philosophy The Armstrong Ideal Index was created by Frank Armstrong, a renowned financial advisor and author of The Informed Investor. Armstrong advocates for a passive, low-cost investing approach, emphasizing diversification across asset classes and reliance on index funds to eliminate manager risk. His philosophy centers on: 2. Asset Allocation Analysis The portfolio is allocated as follows: Risk Level: Aggressive (70% equities), suitable for long-term investors with higher risk tolerance. 3. Practical Application for Retirement Accounts For 401(k) Plans: For IRAs: Investors can directly replicate the portfolio using the suggested ETFs (e.g., SCZ, SPY, BND) for greater flexibility and lower costs. Key Takeaway: The Armstrong Ideal Index is a low-maintenance, diversified portfolio ideal for investors seeking long-term growth with a tilt toward small-cap and value stocks. Its simplicity makes it adaptable to most retirement accounts.

-

P Andrew Tobias Three Fund Lazy Portfolio Annual Balance desc

Comprehensive Overview of the P Andrew Tobias Three Fund Lazy Portfolio 1. Background and Philosophy Andrew Tobias is a renowned financial author and investor, best known for his book “The Only Investment Guide You’ll Ever Need.” His philosophy centers on simplicity, low costs, and long-term investing. The Three Fund Lazy Portfolio reflects his belief that most investors can achieve success with minimal effort by using low-cost ETFs or index funds. Tobias advocates for dollar-cost averaging (regular, consistent investments) and periodic rebalancing to maintain the portfolio’s target allocation. This approach minimizes fees, reduces emotional decision-making, and leverages broad market diversification. 2. Asset Allocation Analysis The portfolio is evenly split into three funds: Risk Level and Pros/Cons Risk Level: Moderate. The portfolio is heavily weighted toward equities (66.6% stocks), which introduces market volatility, but the 33.3% bond allocation mitigates risk. Pros: Cons: 3. Practical Application for Retirement Accounts For 401(k) Accounts: Investors should: For IRA Accounts: Investors can directly replicate the portfolio by purchasing the three ETFs or their mutual fund equivalents (e.g., VTI for VTSMX, VXUS for VGTSX, and VTIP for VIPSX). IRAs offer greater flexibility, allowing for precise adherence to the lazy portfolio’s structure.

-

Israelsen 7Twelve Portfolio desc

Comprehensive Overview of the Israelsen 7Twelve Portfolio 1. Background and Philosophy The Israelsen 7Twelve Portfolio was created by Craig Israelsen, a financial expert and professor at Utah State University. Israelsen designed this portfolio to emphasize broad diversification across multiple asset classes, reducing reliance on any single market segment. The name “7Twelve” refers to the portfolio’s original structure of 7 asset classes and 12 sub-asset classes, though the version analyzed here includes 11 asset classes. The philosophy behind this lazy portfolio is rooted in modern portfolio theory, aiming to balance risk and return by spreading investments across uncorrelated assets. Israelsen advocates for equal-weight allocation (approximately 8.33% per asset class) to avoid overexposure to any single area, which can enhance long-term stability. 2. Asset Allocation Analysis The portfolio is divided into 11 equally weighted asset classes, each represented by a low-cost ETF: Key Aspects: 3. Practical Application for Retirement Accounts For 401(k) Accounts: Investors can replicate the 7Twelve Portfolio by mapping available funds to the ETF categories: For IRA Accounts: Investors have more flexibility to purchase the exact ETFs listed. They can: Note: If a 401(k) lacks specific options, prioritize broad asset class coverage (e.g., combine mid/small caps into a single “U.S. extended market” fund). The goal is to approximate the portfolio’s diversification, even if exact holdings aren’t available.

-

Special Issue: Staying the Course Amid Market Turmoil

In this special issue:

- Latest in Retirement Savings & Personal Finance: Market Turmoil, Majority of Americans Invest in Stocks, …

- Staying the Course Amid Market Turmoil

- Tools & Tips: Longest S&P 500 Losses (Drawdowns)

- Market Overview

-

A Step-by-Step Guide to Finding Your Old 401(k) Account

If you’ve lost track of an old 401(k) account due to job changes, mergers, or simply forgetting about it, don’t worry—there are several steps you can take to locate your funds. Whether your former employer was a large corporation like Bloomberg L.P. or a smaller company, the process remains largely the same. Below is a detailed guide to help you find your forgotten 401(k). 1. Gather Your Information Before diving into the search, gather as much relevant information as possible to streamline the process. 2. Check Your Old Records Your personal records may hold valuable clues to locating your old 401(k). In case you don’t have old records or simply have incomplete information, you can utilize MyPlanIQ’s comprehensive database of retirement plans to search for your old plans. We have one of the most comprehensive retirement plan databases, which even includes some old plans that have ceased to exist. You can visit the MyPlanIQ Retirement Plan Search/Browse page. If you find that the contact information is no longer valid, it’s likely your old company might have been acquired or ceased operations. You can find more information by searching Google using phrases like “ACME acquired,” “ACME Inc. merged,” or “ACME Inc. bankrupt.” These searches will provide more clues on how to track down the old company. 3. Contact Former Employers Your former employer’s HR department is often the first point of contact when searching for a lost 401(k). 4. Use Online Resources Several online databases and services specialize in helping individuals locate lost retirement accounts. 5. Utilize Financial Institutions Sometimes, old 401(k) accounts are transferred to financial institutions or custodians after a company dissolves or merges. 6. Explore Additional Options If the above steps don’t yield results, consider these additional strategies: What to Do Once You Find Your Old 401(k)? Once you’ve located your old 401(k), you’ll need to decide what to do with it. Here are some options: By following these steps, you can successfully locate and reclaim your forgotten 401(k) account. Remember, the key is persistence and thoroughness—retirement accounts can easily slip through the cracks, but they’re never truly lost forever. It’s your money, you should claim it back!

-

Ted Aronson Family Taxable Portfolio, desc

The Aronson Family Taxable Portfolio: A Quietly Interesting Lazy Strategy for Taxable and Retirement Accounts Ted Aronson probably doesn’t ring a bell for most casual investors. But he’s well-known in the institutional world — ran AJO Partners, a quant shop that managed billions before winding down. What’s maybe more interesting (at least for individual investors) is that he publicly shared the investment strategy used in his own family’s taxable account. That’s rare. Most pros don’t talk about their own money. Anyway, his family’s portfolio got picked up by Paul Farrell at MarketWatch, and since then it’s been tracked as part of their “lazy portfolio” series. Even though it holds more funds than most lazy portfolios, it still fits the spirit — broad diversification, low maintenance, no need to guess what markets are going to do next. The portfolio was designed for taxable accounts, but honestly it works just as well in an IRA or 401(k) with a few tweaks. We’ll get into that. Aronson Family Taxable Portfolio Holdings Here’s how the portfolio breaks down: Breakdown: So yes, more holdings than most lazy portfolios. But that’s not necessarily a bad thing. It’s still simple to manage — just takes a bit more setup up front. Asset Allocation Notes This portfolio covers almost everything. You’ve got U.S. stocks in all sizes and styles. International developed is split into Europe and Pacific, which is a bit unusual (most people use a single international fund). Emerging markets have their own big allocation (20%), which gives this portfolio a lot of global exposure. On the bond side, you get a mix — long-term Treasuries for safety and deflation hedge, TIPS for inflation protection, and some high-yield corporate bonds for income. It’s not just “bonds for ballast” — each one plays a role. There’s a tilt toward growth and small caps, plus heavy international exposure. It’s definitely not a plain vanilla 60/40. That said, it’s not too aggressive either. 70% equity, 30% fixed income is reasonable for a long-term investor. It has some volatility, sure. But nothing outrageous. Probably not a great fit for someone retiring next year. But for most working investors, it’s fine. How to Use This in a 401(k) or IRA In a 401(k) Not every 401(k) will have all these options. But here’s a rough guide: Rule of thumb: If something isn’t available, just map to the broader asset class. Small-cap value missing? Just use U.S. small-cap. No TIPS? Use your regular bond fund. No Pacific or European fund? Use total international. In an IRA Much easier here. Just build it directly with ETFs: Put the bond-heavy or income-heavy stuff (like TIP, VGLT, JNK) in the IRA side if possible. Leave the equity ETFs in your taxable account — they’re more tax-efficient. Final Notes This is a thoughtful, globally diversified, slightly quirky portfolio. Not cookie-cutter. But not overly complicated either. It’s a good fit for people who want more exposure than a typical 3-fund portfolio gives you, but still want something passive and relatively easy to maintain. Probably best for folks with moderate risk tolerance — not too conservative, not overly aggressive. Annual rebalancing should be enough. Semi-annual if you really want to be precise. Either way, don’t overdo it.

-

How Paying Credit Card Interest Often Hurts Your Credit Score

It turns out that the number one mistake people make is that they mistakenly think they need to build up their credit card balances and then pay interest to gradually boost their credit scores.This couldn’t be further from reality!

-

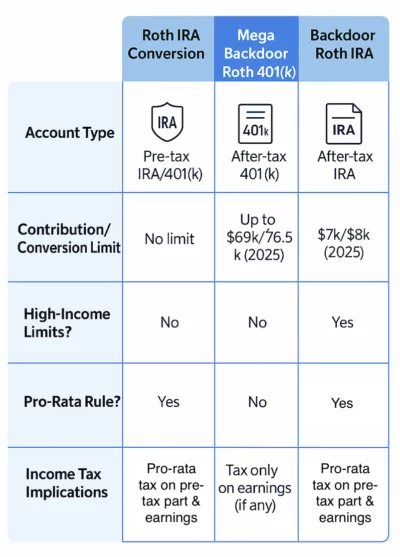

The ABCs of Roth Conversions: Backdoor, Mega Backdoor, and More

In this issue:

- Latest in Retirement Savings & Personal Finance: Tariff Liberation Day, Beefing Up Emergency Savings, and Consumer Confidence at Its Lowest

- The ABCs of Roth Conversions: Backdoor, Mega Backdoor, and More

- Tools & Tips: Social Security Income Calculation Infographic

- Market Overview

-

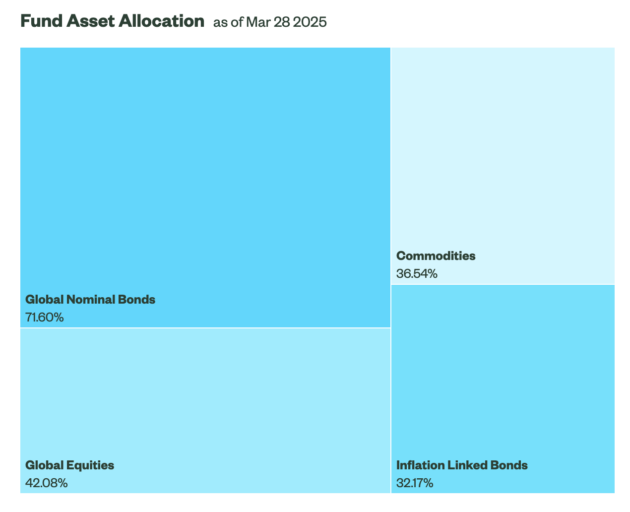

April 2025 MyPlanIQ Portfolio Update

In this issue:

- 1970s Redux: Why the Smithsonian Era Feels Strangely Familiar in 2025

- Fund Analysis: All Weather ETF ALLW

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

- Market Overview

-

Warren Buffett’s 90/10 Portfolio description

Warren Buffett Index Portfolio: A Simple Choice for 401(k) and Novice Investors Investing doesn’t have to be a maze, does it? Warren Buffett, the man who’s seen markets twist and turn for decades, once suggested a dead-simple approach to building wealth. In his 2013 letter to Berkshire Hathaway shareholders, Buffett revealed instructions he had left for the trustee managing his wife’s inheritance. He said 90% of the money should go into a low-cost S&P 500 index fund, and the other 10% into short-term government bonds. This idea, often called the Warren Buffett Index Portfolio, is so straightforward you might wonder why we bother with anything else. But is it really enough for your 401(k), IRA, or taxable account? Let’s dig in, not pretending we’ve got all the answers, but curious to see what this portfolio’s about. Buffett’s philosophy comes from a place of trust in the U.S. economy over the long haul. He’s not chasing hot sectors or trying to time the market. (Who can, anyway?) The man’s been clear: most investors, including the pros, can’t beat the market consistently. So why not just own it? His portfolio reflects that. It’s not about being flashy or clever. It’s about sticking to what’s worked for ages: buy low-cost index funds, hold them forever, and let time do the heavy lifting. Sounds almost too simple, right? Yet, this approach has a quiet confidence, like someone who’s weathered a few storms and knows the sun comes up eventually. Warren Buffett Index Portfolio Holdings Let’s break down the pieces. The portfolio’s got two parts, nothing fancy: Does this cover the bases? Well, it’s got U.S. stocks, sure, and a sprinkle of bonds. But it’s missing a lot: no international stocks, no emerging markets, no small caps, no REITs, no commodities. Gold? Nope. Long-term bonds? Not here either. It’s lean, maybe too lean for some. If you’re looking for diversification across every asset class, this isn’t it. It’s like ordering a plain burger when the menu’s got chili fries and milkshakes. Still, there’s something to be said for keeping it simple. Buffett’s betting on the U.S. market’s long-term growth, and history’s mostly on his side. Risk-wise, this is no sleepy portfolio. With 90% in stocks, it’s got some spice. When markets tank, like in 2008 or 2020, you’re feeling the pain. The 10% in bonds helps, but it’s not a big cushion. Compare that to, say, the Harry Browne Permanent Portfolio, which spreads things out with gold and long-term bonds to hedge inflation and deflation. Buffett’s portfolio doesn’t bother with that. It’s bold, maybe a bit stubborn, banking on stocks climbing back up over time. But for young investors or those with decades until retirement, that risk might be just fine. If you’re closer to cashing out, though? Maybe you’d want more bonds. What stands out? The sheer simplicity. Two funds, that’s all. No rebalancing headaches, no chasing exotic assets. But the flip side is you’re all-in on the U.S. If the S&P 500 stumbles for a decade, you’re along for the ride. And those short-term bonds? They’re safe, but they won’t keep up with inflation like gold or long-term bonds might, as Browne’s portfolio suggests. It’s a tradeoff: clarity versus coverage. Using This in Your 401(k) or IRA So, how do you make this work in a 401(k) or IRA? First, check your plan’s fund lineup. You’re looking for something close to VFINX, like an S&P 500 index fund. Most 401(k)s have one—Vanguard, Fidelity, Schwab, they all offer low-cost versions. For the bond piece, find a short-term Treasury or government bond fund similar to VFISX. If your plan’s got nothing exact, don’t sweat it. A core bond fund or a high-quality actively managed bond fund (check out total return bond funds) can work. Just peek at the expense ratio on Morningstar.com and make sure it’s diversified, not some narrow corporate bond fund. If your 401(k) is missing an S&P 500 fund (rare, but it happens), grab a diversified active U.S. stock fund. Same goes for bonds: no short-term Treasuries? An intermediate bond fund will do. Rule of thumb: stick to index funds for stocks, low-cost if you can. For bonds, core or high-quality active funds are fine. Don’t overcomplicate it. In an IRA, it’s even easier—use ETFs like SPY for stocks or SHY for bonds. Brokerages like Fidelity or Schwab let you trade those for free. Who’s this for? Investors who like to set it and forget it. If you’re in your 30s or 40s, with 20 years or more until retirement, the 90% stock allocation matches that long horizon. But it’s aggressive. If markets dip, you’re stomach’s gotta handle a 30% drop. Nervous types might want less stock. Head to MyPlanIQ’s Asset Allocation Calculator to figure out your risk tolerance. Answer a few questions, and it’ll tell you how much to put in stocks versus bonds. If 90% stocks feels wild, dial it back—maybe 70% stocks, 30% bonds. Keep the same funds, just tweak the split. Taxable Accounts: Keeping It Tax-Efficient Now, what about taxable brokerage accounts? Good news: this portfolio’s built for tax efficiency. Index funds like VFINX (or its ETF cousin, SPY) don’t churn their holdings much, so they spit out minimal capital gains. Same with VFISX—short-term bonds don’t move a lot, keeping taxes low. You’re mostly dealing with dividends, which are taxed, but it’s not like you’re flipping stocks every month. The buy-and-hold nature is a tax win: you only pay when you sell, ideally years down the road. Tax-loss harvesting? Sure, you could do it. If stocks dip, sell VFINX, buy a similar fund (like a total market fund, VTSMX), and book the loss for your taxes. Just don’t trip over the wash-sale rule—wait 31 days before buying VFINX back. It’s a nice trick, but honestly, this portfolio’s so hands-off, you might not bother. The tax savings are real, though, especially in high-income years. Takeaway The Warren Buffett Index Portfolio isn’t trying to win a complexity contest. It’s just two funds, a big bet on U.S. stocks, and a nod to safety with bonds. Is it perfect? Probably not. It skips a lot of assets that could spread risk better, like international stocks or gold. But there’s something refreshing about its clarity. You don’t need a PhD to understand it, and maybe that’s the point. For 401(k) or IRA investors who want to keep things simple, or taxable account holders who hate tax headaches, it’s worth a look. Just know your risk tolerance, because this one’s got some kick. We’re not saying this is the only way to go. Markets surprise us all the time, don’t they? But Buffett’s been around the block, and his logic’s got weight. If you’re tired of chasing trends or second-guessing, maybe this is your kind of lazy. Set it, forget it, and trust the long game. Will it work forever? Who knows. But it’s got a decent shot, and that’s more than most strategies can say.

-

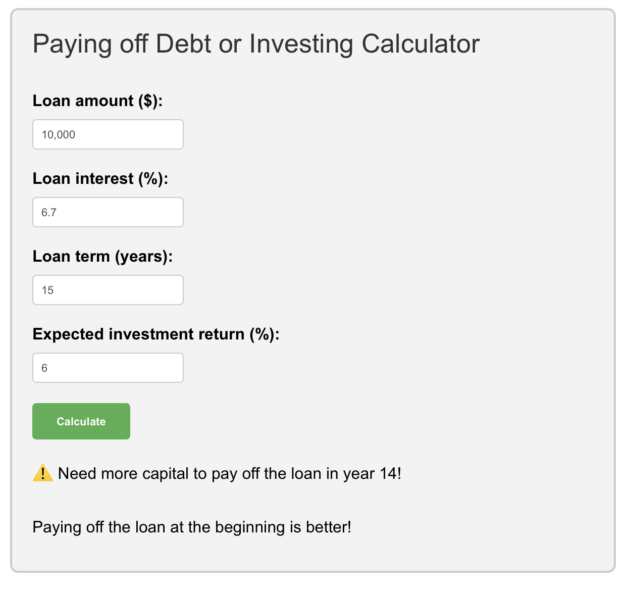

Paying Off Debt or Funding Retirement? How to Decide When Every Dollar Counts

In this issue:

- Latest in Retirement Savings & Personal Finance: 401(k) Millionaires Save More, Spring Financial Cleaning

- Paying Off Debt or Funding Retirement? How to Decide When Every Dollar Counts

- Paying off Debt or Investing Calculator

- Market Overview

-

subscribe verify email

Dear {{ email }}: Welcome to MyPlanIQ! We’re excited to have you join our community of savvy retirement investors. Here’s what you can expect:

- Every two weeks, we’ll send you expert insights on optimizing your retirement portfolio.

- You’ll learn strategies for balancing risk and reward in your investments.

- We’ll keep you updated on the latest trends in retirement planning and market analysis.

To ensure you receive our valuable content, please take these quick actions:

- Move this email to your “Primary” inbox.

- Reply “YES” to this email. This tells email providers you want our content.

{% if password %}As a welcome gift, we’ve prepared a FREE account for you to backtest your personal portfolio. Click the button below to access it! Username: {{ email }} Password: {{ password }} Access Your Free Account {% endif %}

-

Tim Maurer Simple Money Portfolio description

Tim Maurer Simple Money Portfolio Overview Background and Philosophy The Simple Money Portfolio was created by Tim Maurer, a wealth advisor and Director of Personal Finance for Buckingham and the BAM ALLIANCE. Maurer is a well-known financial expert, author, and speaker who advocates for simplicity, behavioral finance awareness, and evidence-based investing. His book, Simple Money: A No-Nonsense Guide to Personal Finance, emphasizes the importance of aligning financial decisions with personal values while avoiding unnecessary complexity. The philosophy behind this lazy portfolio is rooted in a 60/40 stocks/bonds allocation, but with intentional tilts toward value and small-cap stocks to potentially enhance returns over the long term. Maurer’s approach is designed to be low-maintenance, diversified, and suitable for investors who prefer a hands-off strategy while still capturing market premiums associated with value and small-cap equities. Asset Allocation and Analysis The portfolio consists of the following ETFs: Diversification and Risk Level This portfolio is well-diversified across: The risk level is moderate, given the 60/40 split, but the tilts toward small-cap and value stocks introduce slightly higher volatility compared to a traditional 60/40 portfolio. The bond allocation (IEI) provides stability and reduces overall portfolio risk. Pros and Cons Pros: Cons: Application for Retirement Accounts (401(k) and IRA) Investors can implement this portfolio in their 401(k) or IRA accounts by selecting funds that closely match the ETFs listed. Here’s how: Note: Many 401(k) plans lack specific value or small-cap international funds. In such cases, investors can substitute with broader international equity funds or allocate the missing portion to U.S. equities or bonds, depending on their risk tolerance. Rule of Thumb:

-

Pinwheel Portfolio description

The Pinwheel Portfolio is a lazy portfolio designed by Tyler from PortfolioCharts.com. Tyler is known for his research on asset allocation strategies that balance performance, risk, and simplicity. The portfolio is built on the philosophy of equal-weighting the four core asset classes—U.S. stocks, international stocks, bonds, and real estate—while incorporating performance tilts to enhance returns and reduce volatility. This approach aims to provide a diversified, low-maintenance investment solution for long-term investors. Asset Allocation and Diversification The Pinwheel Portfolio allocates its holdings across eight ETFs, each representing a distinct segment of the market: This allocation provides broad diversification across geographies, sectors, and asset classes, reducing concentration risk. The inclusion of small-cap value (SLYV) and gold (IAU) adds a performance tilt, historically known to outperform in certain market conditions. Risk Level and Pros & Cons Risk Level: Moderate. The portfolio balances growth (stocks, real estate) with stability (bonds, gold), making it suitable for investors with a medium risk tolerance. Pros: Cons: Application for Retirement Accounts (401(k) and IRA) The Pinwheel Portfolio can be adapted for retirement accounts like 401(k)s and IRAs. Here’s how: For IRAs, investors have more flexibility to directly purchase the ETFs listed in the Pinwheel Portfolio, making implementation straightforward. In summary, the Pinwheel Portfolio offers a balanced, diversified approach for retirement investors seeking a hands-off strategy with moderate risk. By adapting it to available 401(k) options or using it directly in IRAs, investors can build a resilient long-term portfolio.

-

Scott Burns Margaritaville Portfolio description

Overview of the Scott Burns Margaritaville Portfolio Background and Philosophy The Margaritaville Portfolio was created in 2004 by Scott Burns, a well-known financial columnist for the Dallas Morning News. Burns is a proponent of simple, low-cost, and diversified investment strategies. The portfolio’s name is inspired by the classic margarita cocktail, which consists of equal parts tequila, triple sec, and lime juice—mirroring the portfolio’s equal allocation to three core asset classes. Burns designed this lazy portfolio to provide broad diversification with minimal maintenance, making it ideal for investors seeking a hands-off approach. Asset Allocation and Holdings The Margaritaville Portfolio consists of three equally weighted assets: Diversification and Risk Level This portfolio achieves strong diversification across: The risk level is moderate, balancing growth potential (equities) with stability (bonds). However, the 33% allocation to international stocks may introduce currency and geopolitical risks. Pros and Cons Pros: Cons: Application for Retirement Accounts (401(k) and IRA) Investors can implement the Margaritaville Portfolio in their 401(k) or IRA accounts by selecting equivalent funds: Note: If a 401(k) lacks exact matches, investors can approximate allocations by using broader categories: Rule of Thumb: This flexibility ensures the portfolio remains viable even with limited 401(k) fund choices.

-

Larry Swedroe Minimize FatTails Portfolio description

Larry Swedroe Minimize Fat Tails Portfolio Overview 1. Background and Philosophy The Larry Swedroe Minimize Fat Tails Portfolio is designed by Larry Swedroe, a renowned financial author, researcher, and principal at Buckingham Strategic Wealth. Swedroe is a proponent of evidence-based investing, emphasizing low-cost, passive strategies grounded in academic research. His philosophy focuses on minimizing risk, particularly the impact of extreme market events (“fat tails”), while still capturing long-term returns through diversification and factor-based investing (e.g., small-cap value and emerging markets). This portfolio reflects Swedroe’s conservative approach, prioritizing capital preservation and reducing volatility through a heavy allocation to fixed income (70%) while still maintaining exposure to equities (30%) for growth potential. The strategy is ideal for risk-averse investors or those nearing retirement who want to mitigate downside risk without sacrificing all growth opportunities. 2. Asset Allocation, Diversification, and Risk Asset Allocation:– Equities (30%): – Fixed Income (70%): Diversification: The portfolio spans U.S. small-cap value, emerging markets, short-term Treasuries, and inflation-protected bonds, reducing concentration risk. The heavy bond allocation dampens equity volatility. Risk Level: Low to moderate. The 70% bond allocation significantly reduces risk, but the equity portion (especially emerging markets) introduces some volatility. The focus on small-cap value and TIPS adds inflation and factor risk. Pros: Cons: 3. Application for Retirement Accounts (401(k) and IRA) This portfolio is well-suited for conservative retirement investors, particularly those in or near retirement who prioritize capital preservation. Here’s how to implement it in a 401(k) or IRA: 401(k) Implementation:Many 401(k) plans lack specific ETFs like IJS or VWO. In such cases: Note: If a 401(k) lacks specific options (e.g., commodities), reallocate to the nearest asset class (e.g., stocks for missing commodity exposure). Rule of Thumb: IRA Implementation:IRAs offer more flexibility. Investors can directly purchase the ETFs (IJS, VWO, SHY, TIP) to match the portfolio exactly. Rebalancing: Annually rebalance to maintain the 30/70 equity/bond split and adjust sub-allocations as needed.

-

Aronson Family Taxable Portfolio description

1. Background and Philosophy The Aronson Family Taxable Portfolio was created by Ted Aronson, a renowned asset manager and founding partner of AJO Partners, a Philadelphia-based investment firm. Aronson is a pioneer in quantitative investing and has been recognized for his expertise in systematic, rules-based investment strategies. His philosophy emphasizes diversification, low costs, and tax efficiency, which is reflected in this portfolio’s construction. The portfolio is designed for long-term growth while managing risk through broad asset class exposure. 2. Asset Allocation, Diversification, and Risk The portfolio consists of 11 ETFs spanning four major asset classes: Diversification: The portfolio is well-diversified across geographies (US, developed international, and emerging markets) and market capitalizations (large-cap, small-cap, value, and growth). It also includes a mix of bonds (Treasuries, TIPS, and high-yield) for stability. Risk Level: Moderate to moderately aggressive. The 30% fixed-income allocation provides some downside protection, while the small-cap and emerging market exposures add growth potential (and volatility). Pros: Cons: 3. Application for Retirement Accounts (401(k) and IRA) This portfolio can be adapted for retirement accounts with minor adjustments: For 401(k) Investors: For IRA Investors: This portfolio is suitable for investors seeking a balanced, long-term strategy with moderate risk. Regular rebalancing (annually or semi-annually) is recommended to maintain the target allocations. Rule of Thumb:

-

Moderate Portfolio description

Moderate Portfolio Overview The Moderate Portfolio is a well-balanced investment strategy designed for investors seeking a mix of stability, income, and moderate growth potential. This portfolio is part of the broader “lazy portfolio” philosophy, which emphasizes simplicity, diversification, and long-term investing. Lazy portfolios are typically constructed with a small number of low-cost index funds or ETFs, requiring minimal maintenance and rebalancing. The Moderate Portfolio aligns with this philosophy by offering a diversified mix of equities and fixed-income assets, making it suitable for investors with a moderate risk tolerance. Asset Allocation and Diversification The Moderate Portfolio allocates 60% to equities and 40% to fixed income, striking a balance between growth and stability. The equity portion is split between domestic and international markets, with 39% in VTI (Vanguard Total Stock Market ETF) and 21% in VEA (Vanguard FTSE Developed Markets ETF). This provides broad exposure to U.S. and international developed markets, reducing concentration risk and enhancing diversification. The fixed-income portion includes 32% in BND (Vanguard Total Bond Market ETF) and 8% in IGOV (iShares International Treasury Bond ETF), offering stability, interest income, and exposure to both U.S. and international bonds. Diversification: The portfolio is highly diversified across asset classes, geographies, and sectors, reducing the impact of market volatility on overall returns. The inclusion of international bonds (IGOV) further enhances diversification by mitigating risks associated with U.S.-centric fixed-income investments. Risk Level: The Moderate Portfolio is designed for investors with a moderate risk tolerance. The 40% allocation to fixed income provides a cushion during market downturns, while the 60% allocation to equities offers growth potential. However, it is not immune to market fluctuations, and investors should be prepared for moderate volatility. Pros:

- Balanced approach with a mix of growth and stability.

- Low-cost, diversified ETFs reduce expenses and enhance returns over time.

- Minimal maintenance required, aligning with the lazy portfolio philosophy.

- Suitable for long-term investors, including those saving for retirement.

Cons:

- Moderate volatility due to equity exposure.

- Limited exposure to emerging markets and alternative assets.

- Fixed-income returns may be impacted by rising interest rates.

Application for Retirement Accounts (401(k) and IRA) The Moderate Portfolio is an excellent choice for retirement investors, particularly those with a moderate risk tolerance and a long-term investment horizon. For 401(k) accounts, investors can replicate this portfolio by selecting funds that closely match the ETFs in the allocation. Here’s how:

- VTI (U.S. Total Stock Market): Look for a total U.S. stock market index fund or an S&P 500 index fund in your 401(k) plan.

- VEA (International Developed Markets): Choose an international stock index fund that focuses on developed markets.

- BND (U.S. Total Bond Market): Select a total bond market index fund or an intermediate-term bond fund.

- IGOV (International Treasury Bonds): If your 401(k) plan does not offer international bond funds, consider using a global bond fund or allocating more to BND.

For IRA accounts, investors can directly purchase the ETFs (VTI, VEA, BND, and IGOV) to replicate the Moderate Portfolio. This approach offers greater flexibility and lower costs compared to 401(k) plans. In summary, the Moderate Portfolio is a versatile and well-diversified investment strategy that aligns with the lazy portfolio philosophy. Its balanced allocation makes it suitable for retirement investors seeking a mix of growth, income, and stability. By carefully selecting corresponding funds in 401(k) plans or directly investing in ETFs in IRAs, investors can effectively implement this strategy to achieve their long-term financial goals.