-

May 2025 MyPlanIQ Portfolio Update

In this issue:

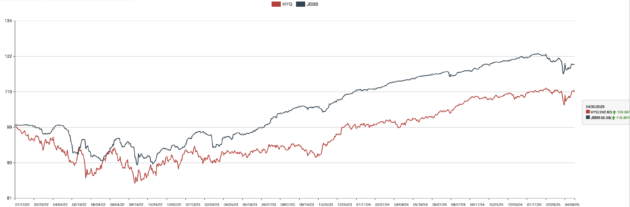

- Major Asset Trends Review: International Stocks Shined and TIPS Disappointed

- Fund Analysis: All Weather Fund ALLW and CLO ETF JBBB Follow up

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

- Market Overview

-

One Fund Does It All

In this issue:

- Latest in Retirement Savings & Personal Finance: US Food & Engergy Inflation Charts, Empty Shelfs Coming? Part-time Contractors Rejoin on 401(k) Eligibility

- One Fund Does It All: Savings & Investing in 401(k) Might Not Be That Intimidating

- Tools & Tips: Retirement Spending Calculator

- Market Overview

-

Target Date Funds for Young Professionals

We review top 9 popular target date funds for young professionnals. We look at their stock/bond allocations and recent returns.

-

Top 10 Target Date Fund Providers for Retirement Investing

Target date funds are becoming more and more popular. We review the top 10 target date fund providers and discuss index-based and actively-manged.

-

The One-Fund 401(k) Portfolio: Simple Yet Does Its Job

One-fund portfolio, either a target-date fund or just a balance index fund, does a good job for retirement plan investors who have little experience or who don’t want to mess around.

-

Roth IRAs for Retirees

Roth IRAs can be very useful for retirees in terms of medicare premiums, estate planning and other benefits.

-

Lazy Portfolios Aren’t Lazy in Growing Wealth

In this issue:

- Latest in Retirement Savings & Personal Finance: Golden Rule and The Roth IRA Evangelist

- Lazy Portfolios Aren’t Lazy in Growing Wealth

- Tools & Tips: Investment Arithmetic

- Market Overview

-

William Bernstein Smart Money desc

Background Information on the Author and Philosophy The William Bernstein “Smart Money” Lazy Portfolio is a one of Bernstein’s lazy portfolios that people constructed based on his writings. The “Smart Money” is also pretty balanced in terms of its allocations to US stocks, internaitonal stocks, emerging market stocks and bonds. It’s a 60% stocks 40% bonds portfolio. Asset Allocation and Holdings Analysis Asset Allocation Breakdown: Diversification: This portfolio achieves excellent diversification across asset classes, geographies, and investment styles: Pros and Cons: 3. Application for Retirement Investors (401(k) and IRA) The following shows how to apply the William Bernstein Smart Money lazy portfolio to retirement accounts, For 401(k) Accounts: Many employer-sponsored 401(k) plans offer a selection of mutual funds or target-date funds, but they may not include all the exact funds listed in the Smart Money Lazy Portfolio. Here’s how an investor can approximate the holdings: For IRAs: IRAs typically offer greater flexibility, allowing direct purchase of Vanguard funds or equivalent ETFs. An investor could replicate the portfolio exactly using the specified funds or their ETF equivalents (e.g., VTI for VTSMX). Online brokerage platforms like Fidelity, Schwab, or Vanguard make it straightforward to implement this strategy. Summary The Bernstein Smart Money Lazy Portfolio works best for people who want something steady and hands-off. It’s simple four fund portfolio is good enough for most average investors. Make sure to scale up or down of your stock exposure based on your age, your return expectation and your financial situation.

-

Lazy Portfolios in Different Market Conditions

Understanding how lazy portfolios perform under different circumstances and concepts like maximum drawdown , rolling returns , and asset allocatio can help you navigate through various market cycles.

-

Tax-Efficient Lazy Portfolios

Lazy portfolio tax strategy can help to enhance after-tax returns for taxable investment accounts. While tax-deferred accounts like IRAs or 401(k)s eliminate immediate tax concerns, taxable accounts require careful consideration of tax efficiency to maximize long-term wealth accumulation.

-

Lazy Portfolios for Retirement Investing

For retirement investors, lazy portfolios can serve as a good tool for their IRAs, 401(k) and taxable investment accounts. This article discusses how to utilize lazy portfolios for these retirement investing accounts.

-

How to Implement a Lazy Portfolio

Implementing a lazy portfolio doesn’t require advanced knowledge or constant attention. Whether you choose mutual funds or ETFs, rebalance annually or less frequently, or tweak allocations based on changing needs, the principles remain the same: keep costs low, stay diversified, and let time work in your favor.

-

What Are Lazy Portfolios?

Investing can be intimidating. It’s a complex and time-consuming endeavor. This is especially true for beginners. , Lazy portfolios offer an appealing solution for this group of people. A lazy portfolio is a straightforward investment strategy designed to require minimal effort and oversight while aiming to deliver solid long-term returns.

-

IRAs as One of the Emergency Fund Sources

In this issue:

- Latest in Retirement Savings & Personal Finance: Back-and-forth Tariff Policies, Stock Market Swings, and Low Retirement Savings Rates

- IRAs as One of the Emergency Fund Sources

- The Gotcha in Maximum Solo 401(k) or SEP IRA Contribution Limits

- Market Overview

-

Burton Malkiel Mid-Fifties Portfolio desc

As people move into their 50s, retirement planning tends to shift from something abstract into something that actually matters — you start to feel the weight of the timeline. The “plenty of time” mindset starts to fade. You’re no longer just accumulating. You’re thinking, maybe quietly at first, about how to protect what you’ve built. And how to make it last. Burton Malkiel — who wrote A Random Walk Down Wall Street, a popular investing book — has a version of the lazy portfolio meant for people right in this stage of life. Late 40s, mid-50s. Somewhere in that zone where the clock starts ticking a little louder. His take on the lazy portfolio keeps the familiar rhythm — diversified, low-cost, no unnecessary trading — but with a tilt that reflects the needs of this age group. That means not just U.S. equities but international and emerging markets too. It’s not just a growth bet — it’s partly a hedge. And on the bond side, you see some interesting choices: long-term corporates, inflation-protected securities. These are moves meant to defend against erosion. Not flashy, but sensible. Asset Allocation: Bond Allocation: Other: This lazy portfolio for mid-fifties investors is designed to provide a balanced mix of assets, including domestic and international stocks, real estate, and various types of bonds. The strategy aims for long-term growth while managing risk through diversification and periodic rebalancing. This portfolio is annually rebalanced.

-

How to Borrow From an IRA?

There are several ways to take money out for short-term emergency purposes. This article explores some of those options.

-

Doug Ramsey All Asset No Authority (AANA) Lazy Portfolio desc

Doug Ramsey All Asset No Authority (AANA) Lazy Portfolio: A Simple Choice for 401(k) and Novice Investors Investing can feel like a maze, can’t it? You look at all the choices, the funds, the market noise, and you wonder what’s actually worth your time. The Doug Ramsey All Asset No Authority (AANA) Lazy Portfolio is one of those ideas that sounds almost too simple to work. Yet, it’s been around, quietly doing its job for those who don’t want to micromanage their money. Let’s talk about this portfolio, its holdings, and how it fits into something like a 401(k), an IRA, or even a taxable brokerage account. Maybe it’s not perfect, but maybe it’s enough? Doug Ramsey, the mind behind this portfolio, isn’t some Wall Street guru shouting predictions. He’s more of a thinker, someone who’s watched markets cycle through booms and busts. From what’s out there, Ramsey’s philosophy leans on diversification and simplicity. No chasing hot stocks, no timing the market. Just a mix of assets that, together, aim to weather whatever the economy throws at you. The AANA portfolio reflects that: spread your bets, keep it low-maintenance, and let time do the heavy lifting. It’s not flashy, and neither is Ramsey. That’s probably why it resonates with people who just want a plan they can stick to. Doug Ramsey is the Chief Investment Officer at Leuthold Group, known for his rigorous research and data-driven investment insights. Doug Ramsey regularly revisits his “All Asset No Authority” (AANA) portfolio as part of Leuthold Group’s annual asset allocation review. Why “No Authority”? The portfolio’s name, “All Asset No Authority,” humorously reflects its hands-off, no-expert-required approach. The term “No Authority” suggests that the portfolio is designed to be simple and accessible, requiring no specialized knowledge to manage. Its equal allocation across the seven assets reinforces this by ensuring that no single asset class is given more emphasis than others, maintaining a balanced and straightforward structure. Ramsey designed it with simplicity in mind, making it accessible for individual investors who prefer an evenly distributed asset allocation strategy without actively managed oversight. Doug Ramsey All Asset No Authority (AANA) Lazy Portfolio Holdings Here’s what the portfolio looks like, broken down by its pieces: Asset Class Allocation (Approx. 14.3% each) U.S. Large-Cap Stocks 14.3% U.S. Small-Cap Stocks 14.3% U.S. Real Estate (REITs) 14.3% International Developed Stocks 14.3% Emerging Markets Stocks 14.3% U.S. Long-Term Treasury Bonds 14.3% U.S. TIPS (Treasury Inflation-Protected Securities) 14.3% This is a portfolio that doesn’t put all its eggs in one basket. You’ve got US stocks, both large and small, international stocks, real estate through REITs, long-term Treasuries, commodities, and even gold. It’s like a buffet of assets, each serving a purpose. The question is, does it cover enough ground? Well, it hits the major bases: US stocks, international stocks, and bonds. That’s a good start. Then it goes further, adding small caps, REITs, commodities, and gold. No emerging markets, though. That’s a gap, maybe, if you think those markets are worth the extra risk. Let’s talk about gold and long-term Treasuries, because they stand out. Gold, as folks like Harry Browne pointed out in his Permanent Portfolio, is a hedge against inflation. When prices rise, when currencies wobble, gold tends to hold its ground. It’s not perfect, but it’s something. Long-term Treasuries, like VUSTX, also play a role in Browne’s thinking. They’re a buffer during deflation or market crashes. When stocks tank, long-term bonds often rally as investors flock to safety. This mix gives the portfolio a kind of balance, a way to zig when the market zags. But equal weighting across seven assets? That’s bold. It’s saying no single asset class is the star. Some might call it overly cautious, others might say it’s brilliantly simple. The pros? Diversification is the big one. You’re not betting the farm on tech stocks or hoping bonds never falter. If one piece struggles, others might pick up the slack. The risk level feels moderate, not too aggressive but not sleepy either. Small caps and commodities add some spice, while Treasuries and gold keep things grounded. The cons? Well, it’s not optimized for growth. If the S&P 500 goes on a tear, this portfolio might lag. Gold and commodities can sit dormant for years. And managing seven funds might feel like a chore for someone who wants a true “set it and forget it” plan. Using the AANA Portfolio in 401(k) and IRA Accounts So, how do you make this work in a 401(k) or IRA? First, check your plan’s fund lineup. Look for index funds that match these asset classes. For VTSAX, you want a total US stock market fund. For NAESX, a small-cap index. VGTSX needs an international developed market fund. And so on. If your 401(k) doesn’t have exact matches, don’t panic. Find diversified active funds instead. Check their expense ratios and diversification on something like Morningstar.com. Rule of thumb: for stocks, prioritize low-cost index funds. For bonds, go for core bond funds or high-quality actively managed ones, like those discussed at MyPlanIQ. What if your 401(k) is missing something, like commodities or REITs? Map them to US stocks. It’s not ideal, but it keeps things simple. Same for long-term bonds—intermediate bond funds can work if that’s all you’ve got. In an IRA, you’ve got more freedom. ETFs like GLD or DBC are easy to grab at a brokerage. Just stick to the same allocation: 14.3% each, or as close as you can get. This portfolio suits folks who want balance without too much fuss. It’s not for the aggressive types chasing 15% annual returns. It’s better for someone with a 10- to 20-year horizon, maybe a bit risk-averse but still wanting growth. To scale it, figure out your risk tolerance first. Use a tool like MyPlanIQ’s Asset Allocation Calculator. Answer a few questions, and it’ll tell you how much to put in stocks versus bonds. If you’re conservative, lean heavier on VUSTX. If you’re bolder, bump up the stock and commodity portions. Just don’t stray too far from the equal-weight spirit. Using the AANA Portfolio in Taxable Accounts Taxable accounts are trickier, but this portfolio plays nice. Most of its funds, like VTSAX or VGTSX, are index funds, which are tax-efficient. They don’t churn holdings, so you’re not hit with constant capital gains taxes. ETFs, like GLD, are even better for this. The buy-and-hold nature of the AANA portfolio helps too. You’re not trading in and out, so you defer taxes until you sell. If you want to get fancy, consider tax-loss harvesting. If DBC dips, sell it, grab a similar commodity ETF, and book the loss for tax purposes. Just don’t overcomplicate it—simplicity is the point. Final Thoughts The Doug Ramsey AANA Lazy Portfolio isn’t going to make headlines. It’s not trying to. It’s for people who’ve seen a market cycle or two, who know that chasing trends often ends in tears. Is it perfect? Probably not. The equal weighting might feel arbitrary to some, and the lack of emerging markets might bug others. But it’s diversified, it’s thoughtful, and it’s built to last. Whether you’re stuffing it in a 401(k), an IRA, or a taxable account, it’s a plan you can set and mostly forget. And isn’t that what most of us want, deep down? A strategy that works without needing to watch the market every day?

-

Paul Farrell Second Grader’s Starter Portfolio desc

1. Background and Philosophy The Second Grader’s Starter Portfolio was created by Paul B. Farrell, a former investment columnist for MarketWatch and author of multiple books on lazy investing. Farrell advocated for simple, low-cost, and hands-off strategies that even a second grader could understand. His philosophy emphasized broad diversification, minimal maintenance, and long-term growth through index funds. This portfolio is designed to be a foundational strategy for beginners or those who prefer a passive approach. 2. Asset Allocation Analysis The portfolio consists of three ETFs: Key Aspects: 3. Practical Application in Retirement Accounts For 401(k) Accounts: Investors can replicate this portfolio by identifying equivalent funds in their 401(k) plan: If exact matches aren’t available: For IRA Accounts: Investors can directly purchase the ETFs (VTI, VEU, BND) or their mutual fund equivalents. IRAs offer more flexibility, allowing for precise allocation. Note: Since commodities are rarely available in 401(k)s, investors can allocate that portion to stocks or omit it entirely.

-

Larry Swedroe Conervative Lazy Portfolio desc

Larry Swedroe’s lazy portfolio is carefully designed for conservative investors seeking lower volatility while maintaining exposure to growth. Swedroe, a well-regarded financial expert and author, emphasizes diversification through low-cost index funds and is known for advocating small-cap value stocks due to their historically strong performance. This portfolio is structured with 30% in small-cap value stocks and 70% in intermediate-term treasuries, aiming to deliver long-term returns similar to stock-heavy portfolios but with less volatility. The small-cap value portion is further diversified as follows: This allocation provides a unique balance between domestic and international small-cap stocks, enhancing diversification and potential returns. The 70% intermediate-term treasury bond allocation adds stability, especially during market downturns, making it a low-risk choice for investors. This portfolio stands out for its exclusive stock exposure to small-cap value stocks. Larry Swedroe firmly believes that, over the long term, small-cap value stocks deliver the best returns compared to other asset classes. This conservative allocation can be compared to funds like the Vanguard Wellesley Income Fund (VWINX), a balanced mutual fund known for its conservative mix of stocks and bonds. However, while the Wellesley fund has a more traditional equity mix, Swedroe’s portfolio is tilted specifically toward small-cap value stocks, which can offer additional growth potential but come with somewhat higher volatility than the large-cap focus of Wellesley. Here’s an itemized breakdown of Swedroe’s portfolio: Asset Class Allocation US Small-Cap Value 15% Developed Market Small-Cap Value 7.5% Emerging Market Small-Cap Value 7.5% Intermediate-Term Treasuries 70% This portfolio aligns well with risk-averse investors looking for growth and stability, delivering a strategic mix between equities and bonds tailored to offer consistency across different economic cycles.

-

P David Swensen Yale Individual Investor Portfolio Annual Rebalancing desc

Background and Philosophy David Swensen (the longtime Yale Endowment CIO) proposed this “one size fits all” model for individual investors in his book Unconventional Success: A Fundamental Approach to Personal Investment. Unlike many conventional models, this one leaned heavily into global diversification — not just U.S. and developed international, but also emerging markets and real estate. The big missing piece? Commodities. Which is kind of interesting, since many other diversified portfolios include them as an inflation hedge. But Swensen didn’t like commodities for individuals. Instead, he leaned into TIPS and REITs for inflation protection. One small side note that tends to confuse people: Swensen talked about rebalancing. He said that Yale did it daily, and by his estimate, that added maybe 1% or 2% in extra return versus annual rebalancing. But for individual investors, the assumption is annual rebalance. And that’s fine. Also worth noting — he made a strong comment in the book that long-term Treasury bonds were the best diversifier: “The purity of noncallable, long-term, default-free Treasury bonds provides the most powerful diversification.” That’s a pretty strong endorsement. But later, someone claimed he clarified (in a Morningstar forum post reply) that average duration Treasuries were fine. So it’s still unclear. We’ll stick with long-term Treasuries here, but just be aware that there’s some ambiguity. Swensen’s core ideas are: It’s not flashy. But there’s logic behind each part. Asset Allocation Analysis Here’s what the portfolio actually looks like, broken down by fund: Pros Diversification is strong. You’re spread across U.S. and international stocks, real estate, and two different kinds of bonds (one focused on inflation protection, the other on deflation or flight-to-safety scenarios). The REIT and TIPS combo makes it pretty inflation resilient too. And the simplicity is hard to beat. Five or six funds total. Easy to manage. Cons It’s still 70% equities, so it’s not low-volatility. That might feel like too much if you’re closer to retirement or just naturally risk-averse. Also, no commodities. That could hurt if we enter a long commodity bull cycle. Lastly, long-term Treasuries (VUSTX) come with interest rate risk — when rates rise, they can fall fast. So this piece helps with crisis periods but may hurt in rising rate environments. Practical Application in Retirement Accounts In a 401(k) Step 1: Look at what’s available Step 2: Adjust if something’s missing Rule of thumb for selecting funds: In a brokerage IRA This is the easiest setup. You can use Vanguard’s original mutual funds, or their ETF versions: Rebalancing? Swensen recommended annual rebalancing. Some folks argue that quarterly is better — and maybe it reduces volatility a little. Maybe. But to be honest, annual is more than enough for most people. Simpler. Less temptation to tinker. And let’s face it — tinkering is where most people go wrong. Taxable Accounts This portfolio isn’t bad in a taxable setting, especially if you stick to ETFs. VTI, VXUS, and even TIP are relatively tax efficient. VNQ and the bond funds might throw off more taxable income, so you may want to keep those in an IRA or 401(k) if you can. That’s basic asset location. Also worth mentioning: tax-loss harvesting. You can harvest losses on VTI and swap into something like SCHB or ITOT. Just keep in mind the 30-day wash sale rule. Most brokers help with that now. Final Thoughts Swensen’s lazy portfolio is one of the best well known lazy portfolios that have attracted large following. The diversification into REITs and TIPs is unique when it was first proposed. It’s been well time tested and a good choice to follow, whether it’s in your retirement 401(k) accounts or taxable investment accounts.