Stock Compensation 101: How People Build Wealth (or Blow It)

In this issue:

- Latest in Retirement Savings & Personal Finance: Review and Get Rid of Your Unused Subscriptions, Private Equity & Crypto Investments in Your Retirement Accounts, Germany’s Early Start Pension

- Stock Compensation 101: How People Build Wealth (or Blow It)

- Tools & Tips: RSU Calculator

- Market Overview

Latest in Retirement Savings & Personal Finance: Review and Get Rid of Your Unused Subscriptions, Crypto Investments in Your Retirement Accounts, Germany’s Early Start Pension

Your Old Subscriptions

Turns out, unused subscriptions quietly eat up way more money than most people realize. A recent survey said over 85% of Americans have at least one paid subscription they’re not using each month. Sounds about right. You think you’re paying for Netflix or Amazon Prime because “you might use it next week” but next week becomes next month, and nothing changes.

On average, people are wasting around $33 a month on these — almost $400 a year. And usually it’s not just one or two. Most households have three or more that are just sitting there, auto-renewing in the background. This kind of slow bleed is sometimes called “subscription creep.” It’s especially common with younger folks, partly because there are so many services now, and partly because everything’s designed to make quitting a hassle.

The most common culprits? Not surprisingly, it’s the big names — Prime, Netflix, even gym apps or e-commerce perks. They’re easy to sign up for. But even easier to forget.

Private Equity & Crypto Investments in Your Retirement Accounts

There were talks a while back, first under President Trump, then again recently with firms like Empower, about letting 401(k) plans include private equity. On paper, that sounds like opening up new opportunities. In reality, private equity usually means higher fees, longer lockups, and more complexity than most retirement investors are used to. Not necessarily bad. Just not simple.

At the same time, the U.S. quietly rolled back its 2022 guidance that had warned against putting crypto in retirement accounts. So now, technically, you could have Bitcoin in your 401(k). Whether that’s smart or not is another story. But given how much money sits in retirement plans, trillions of dollars, even a small shift toward crypto or alternatives could move markets. Or at least change how people think about what belongs in a “safe” portfolio.

Our advices: if you’re experienced enough to understand the risks, these might be worth a look. Otherwise, probably better to avoid for now. No need to complicate your retirement when the basics still work.

Germany’s Early Start Pension

Germany is rolling out a new retirement initiative called “Frühstart-Rente,” or early start pension, beginning January 1, 2026. Under this plan, children aged 6 to 18 who are enrolled in school will receive 10 euros per month, or 120 euros per year, from the government into a special retirement account. Over 12 years, that adds up to 1,440 euros per child, not counting any investment growth.

Once the child turns 18, they can continue contributing to the account on their own, with some annual limits. Investment gains stay tax-free until retirement, which is currently age 67 in Germany. That means the funds could compound for more than 60 years if left untouched, giving these kids a rare head start on retirement savings.

Some of the details are still being finalized, like how the funds will be managed or what the investment options will be. But the goal is clear. The program is meant to promote long-term financial security and early financial awareness. Maybe you can also plan for your kids in this way, if the US government doesn’t have something similar. Furthermore, you could also setup so called kiddie IRA if your kid participates in some of your businesses, as simple as typing Excel data. We mentioned that in one of our previous newsletters. There are always ways to do better if you try harder.

Stock Compensation 101: How People Build Wealth (or Blow It)

Employee stock compensation can seem optional. Or mysterious. But once you understand the types and how they actually work, it becomes clearer why this might be the most important part of your pay package. Sometimes it makes people rich. Other times, not paying attention to it… well, let’s just say there are some painful stories too.

Let’s break down the basics first.

Types of Stock Compensation

| Type | What It Means | Key Feature |

|---|---|---|

| ESPP (Employee Stock Purchase Plan) | Lets you buy company shares at a discount using payroll deductions | Discounted purchase price, sometimes with a “lookback” on lower historical price |

| ESOP (Employee Stock Ownership Plan) | Company gives you shares inside a retirement account, often your 401(k) | Mostly passive, you don’t need to do anything |

| RSU (Restricted Stock Units) | You receive company stock after staying (vesting) for a period | Stock becomes yours at vesting, sometimes pays dividends |

| Stock Options | Gives you the right to buy company stock at a fixed “strike price” | High upside if stock rises, worthless if it doesn’t |

Comparing the Four at a Glance

| Category | ESPP | ESOP | RSU | Stock Options |

|---|---|---|---|---|

| Risk | Low | Very low | Medium | High |

| Cost to You | Payroll deduction | None | None | You pay to “exercise” at strike price |

| Potential Reward | Small edge, consistent gains | Long-term, steady growth | Strong upside if company grows | Big win if stock price rises well above strike price |

| Tax Timing | When sold | When withdrawn from 401(k) | When vested | When exercised plus sold |

| Common in | Public companies, especially tech | Larger or employee-owned firms | Tech, startups, big firms | Startups, high-growth companies |

Why This Matters: Real Stories

At one mid-sized biotech company in San Diego, an employee quietly maxed out her ESPP every cycle. She didn’t think much of it. Just treated it like forced savings. Over 7 years, the stock went from 20 to over 100. Her modest paycheck deductions added up to over 300K by the time she left, most of it from gains she barely noticed.

In contrast, another engineer at a fast-growing software firm was granted a large chunk of stock options in 2018. But he didn’t exercise them when they were in-the-money and the options were worth multi-millions, thinking the price would go even higher. It didn’t. In fact, the stock dropped below the strike price during COVID. By the time he left, the options were worth zero. Four years of vesting, gone.

There’s also a famous case from the early Google days. Someone in a non-tech role who never negotiated cash raises but just let the RSUs vest quietly. She retired in her 40s. No luck, no trading, just showed up and held her shares.

Takeaway

Stock compensation doesn’t need to be complicated. But it does need your attention. If you ignore it, you could be leaving life-changing wealth on the table. Or exposing yourself to risks you didn’t plan for.

This isn’t about timing the market. It’s about understanding your deal and having a plan. Because sometimes this is where real wealth is made. And if not? At least you won’t be the one staring at a worthless option grant wondering what went wrong.

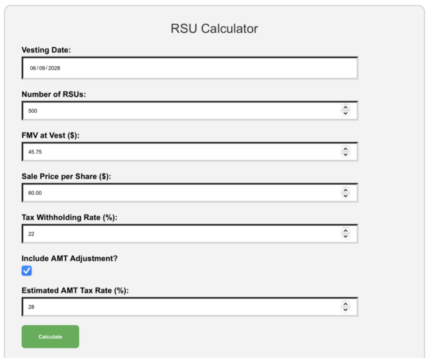

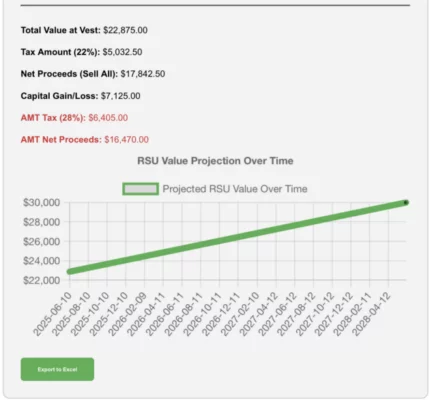

Tools & Tips: RSU Calculator

In addition to ESPP Tax and Cost Basis Calculator we introduced in our last newsletter, we look at the new RSU Calculator.

In the calculator, you input multiple vesting dates, include sale prices to calculate capital gains or losses, toggle AMT adjustments for pre-IPO scenarios, and visualize your results in an interactive chart.

Once you enter your inputs, press ‘Calculate’ button would yield:

The calculator also allows you to export to an Excel file.

Market Overview

US stocks continued to rise last week. Year to date, the S&P 500 has risen 2.3%. For Q1 2025, FactSet reported that the earnings growth rate for the S&P 500 is 13.3%, which is much better than expected. Investors have adopted a more relaxed attitude toward the tariff negotiations. Whether this is warranted remains to be seen, however.

The following table shows the major asset price returns and their trend scores, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 1.2% | 2.9% | 7.3% | -0.2% | 13.4% | 4.9% |

| Foreign Stocks | 0.9% | 3.9% | 9.6% | 11.1% | 14.6% | 8.0% |

| US REITs | 0.6% | 0.4% | -0.7% | -4.3% | 12.5% | 1.7% |

| Emerging Market Stocks | 2.6% | 2.2% | 8.2% | 5.0% | 14.1% | 6.4% |

| Bonds | 0.0% | 0.4% | -0.4% | 0.3% | 4.7% | 1.0% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

Try to Find Your Old Retirement Accounts?

Find Tools and Calculators That Provide Quick Help