March 9, 2020: Risk And Reward

We examine popular risk and reward notion and discuss under the current market condition.

We examine popular risk and reward notion and discuss under the current market condition.

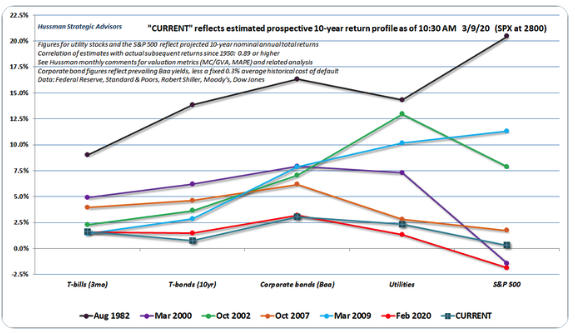

We examine the risk of the new coronavirus outbreak and discuss its impact on economy and financial markets.

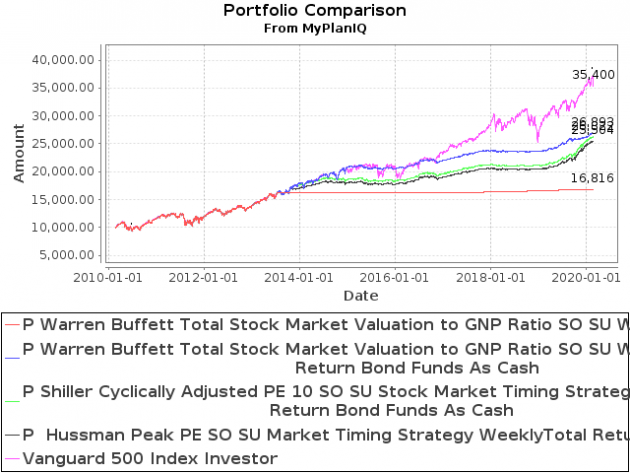

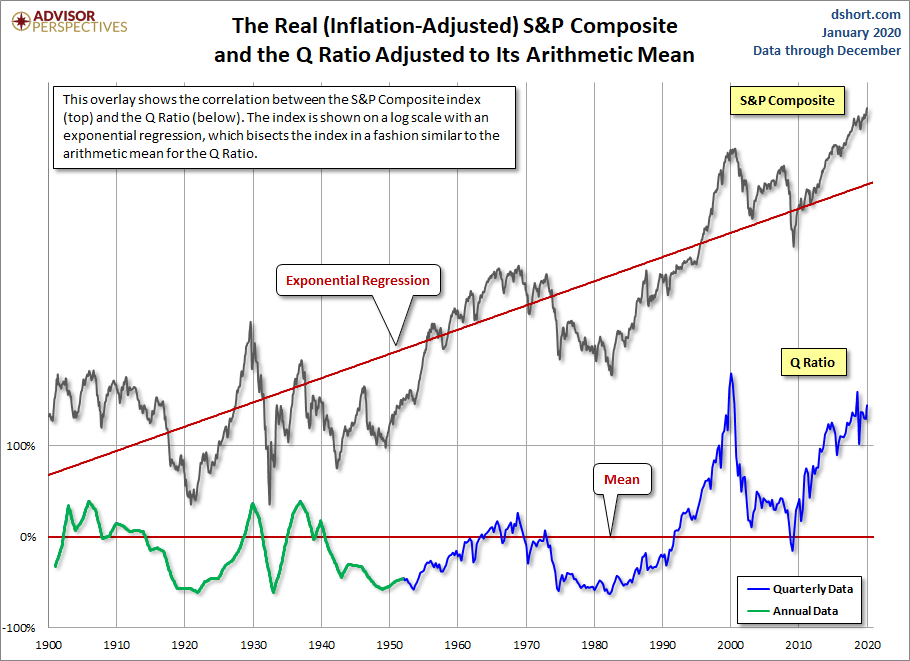

We examine closely long term stock valuation metric strategies and show that some improvements of a simple strategy can drastically improve returns.

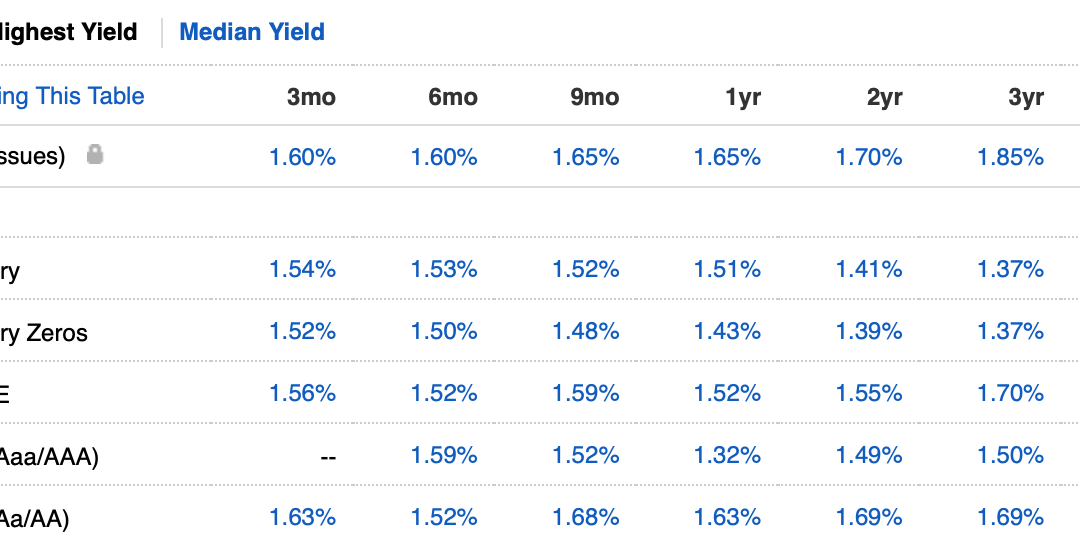

We review the latest interest rates of money market funds, bank cash, Treasury bills and brokered CDs.

We look at stock investing strategies for retirees.

We look at fixed income investing strategies for retirees.

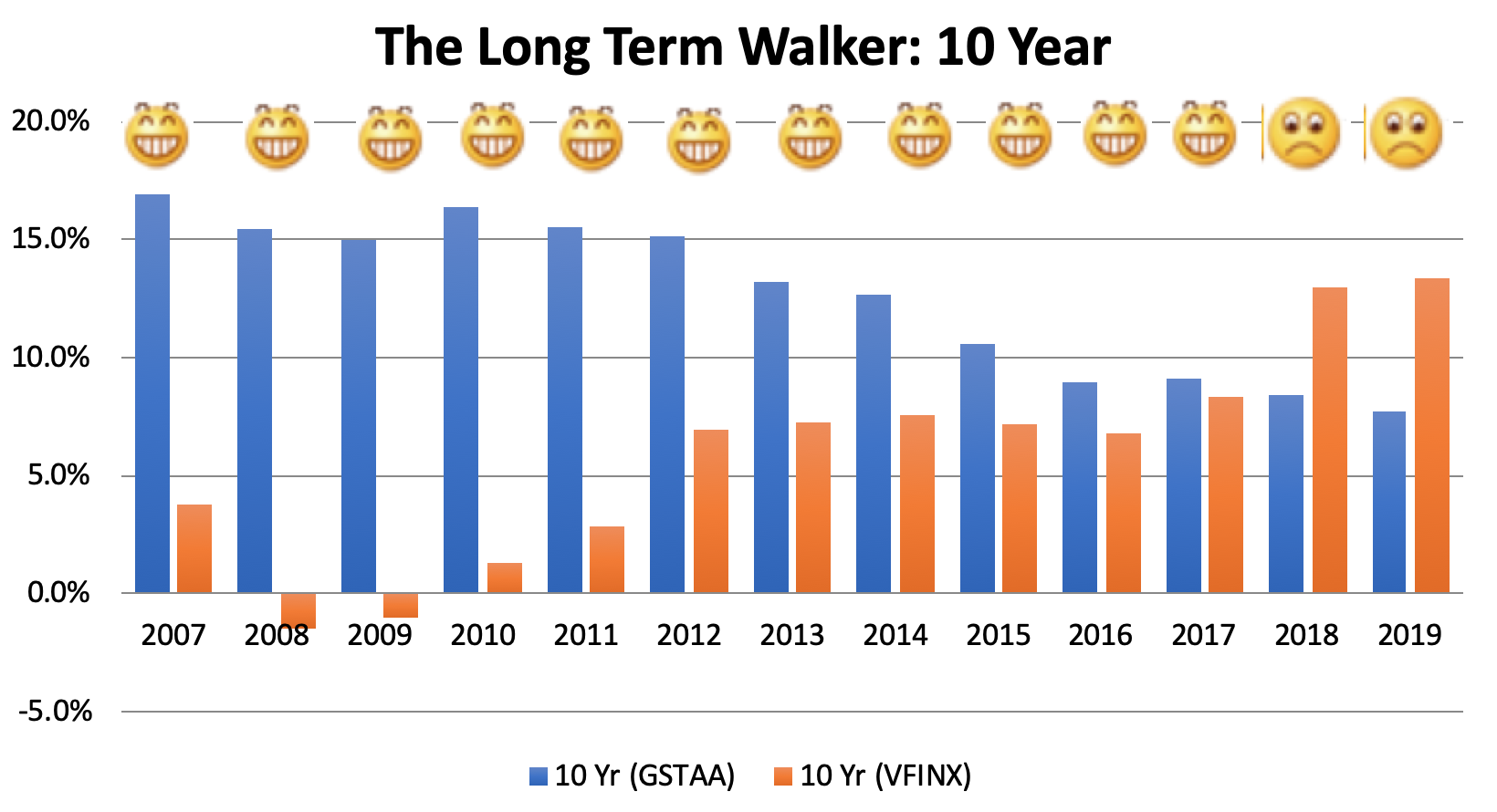

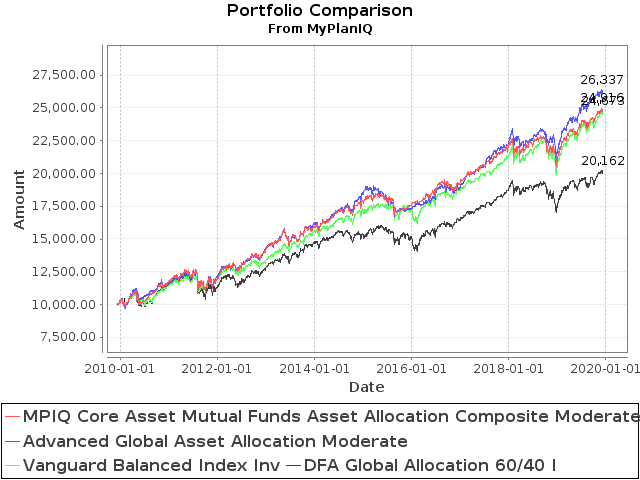

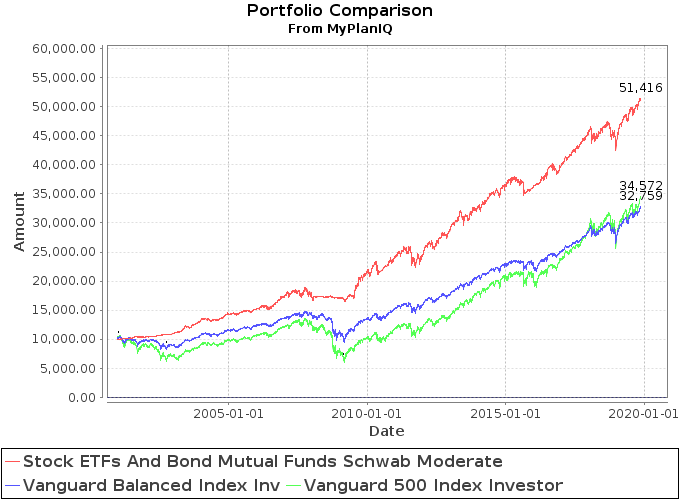

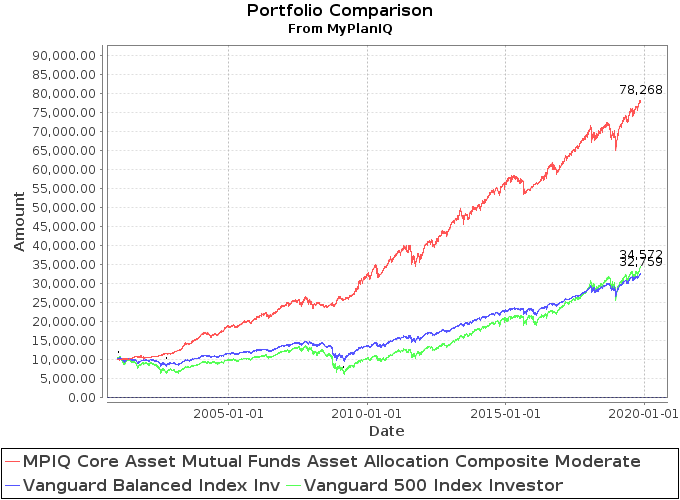

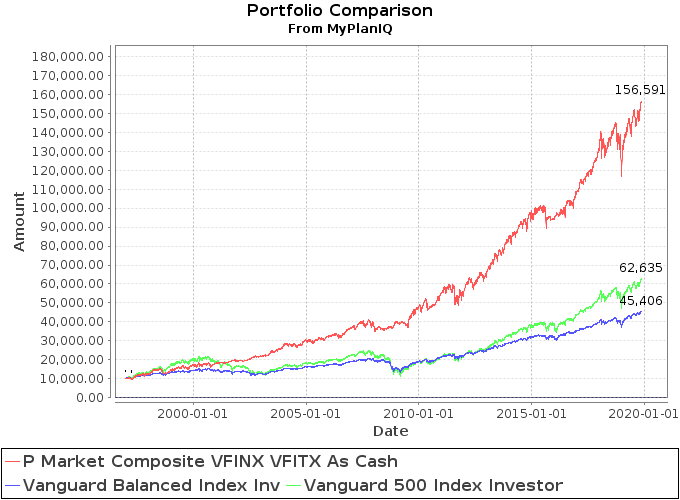

We revisit walk in the past to look at portfolio returns in history.

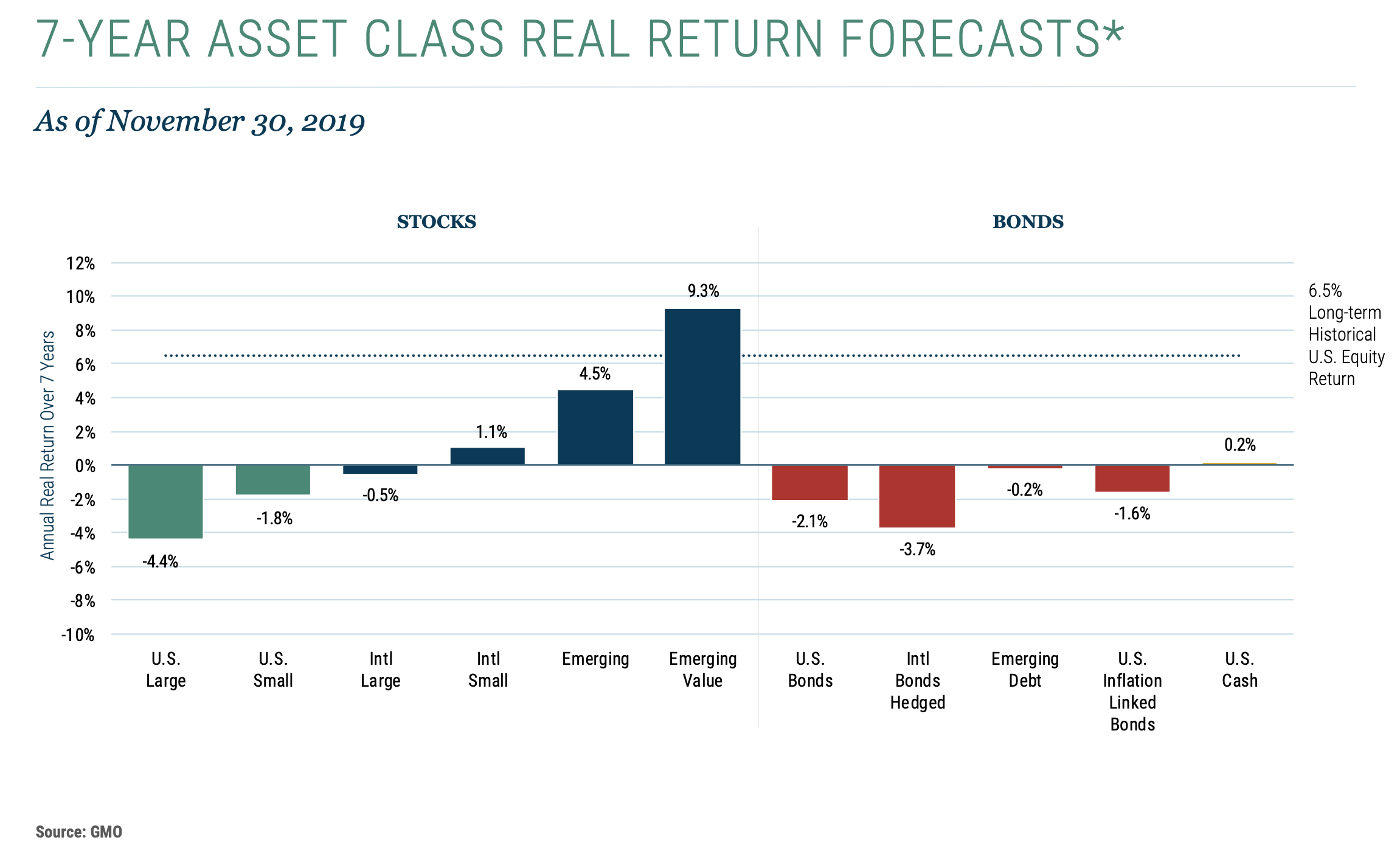

We discuss our asset outlook and point out that it’s more important to adopt an active (tactical) portfolio strategy from now on as risk is rising.

We again answer some of our users’ recent questions.

We clarify our offerings and discuss how to utilize practical advanced portfolios.

We have the latest update on the recent published newsletters.

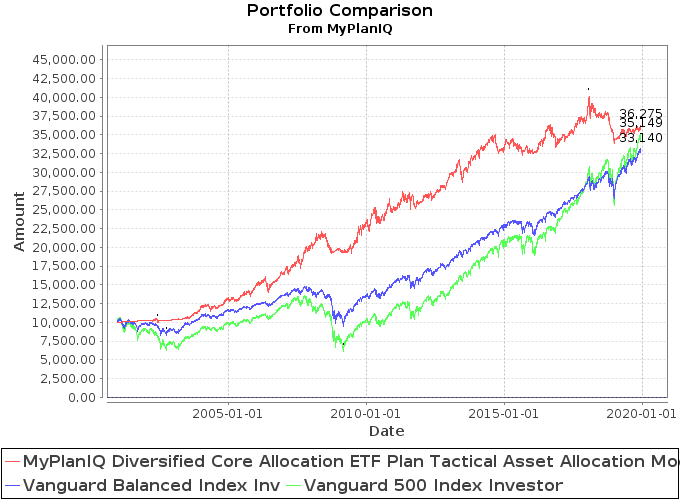

We discuss a hybrid ETF and mutual fund portfolio.

We introduce our new Asset Allocation Composite strategy and discuss its brokerage based model portfolios.

We introduce composite momentum that’s a combination of our market indicator and momentum. We show good improvement on portfolios’ returns.

We introduce a factor ETF rotation portfolio based on momentum of these ETFs. The results show that the portfolio can improve static allocation portfolios.

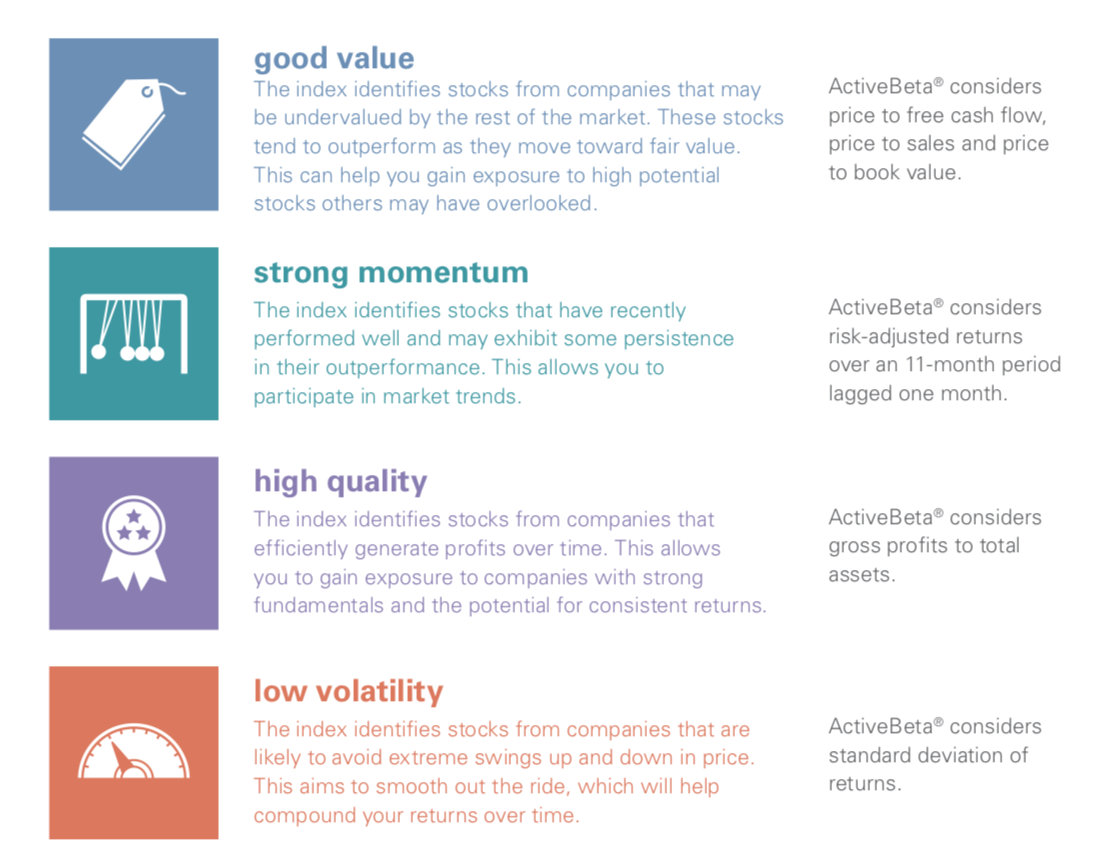

We look at multi-factor (value, quality, low volatility and momentum) ETFs and portfolios. We believe factor ETFs can add good value to an asset allocation portfolio.

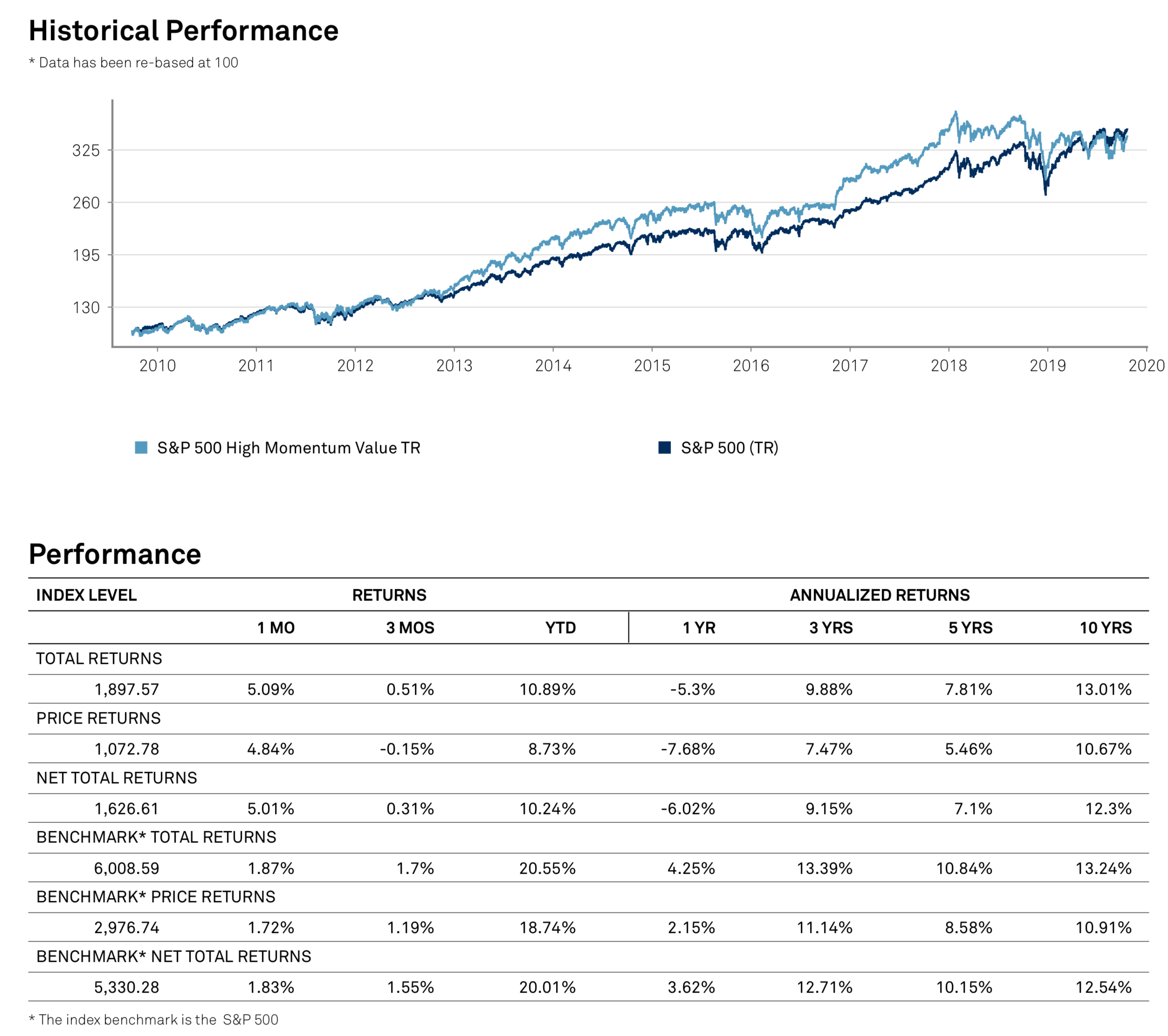

We look at value-momentum combined ETFs.

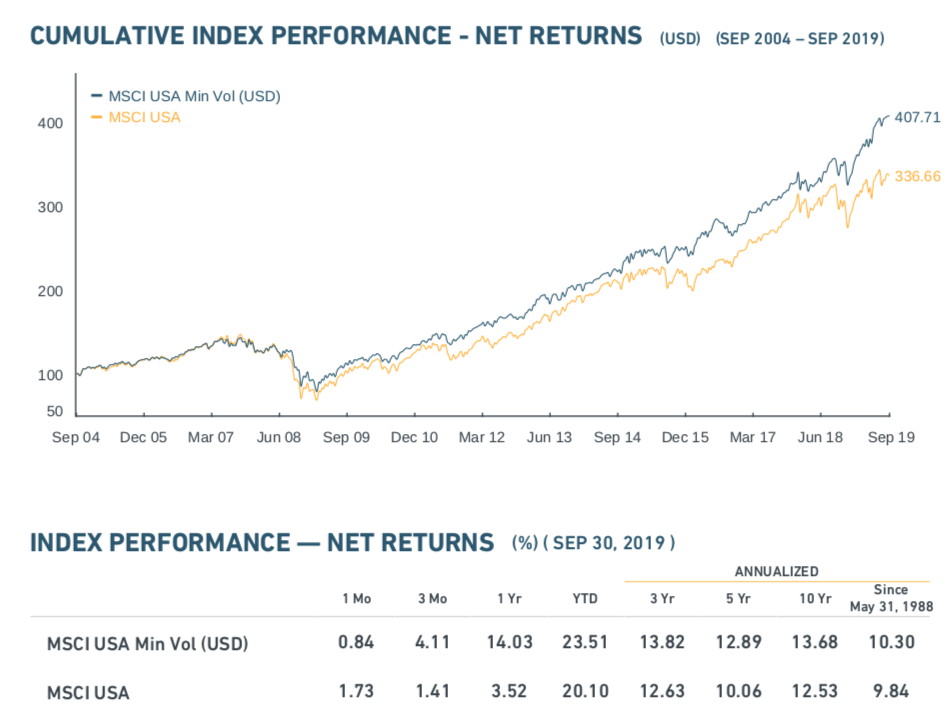

Low volatility factor can indeed outperform broad base stock indexes.

Many brokerages are now offering unlimited commission free stock and ETF trades. But that doesn’t necessarily bode well to investment cost improvement.

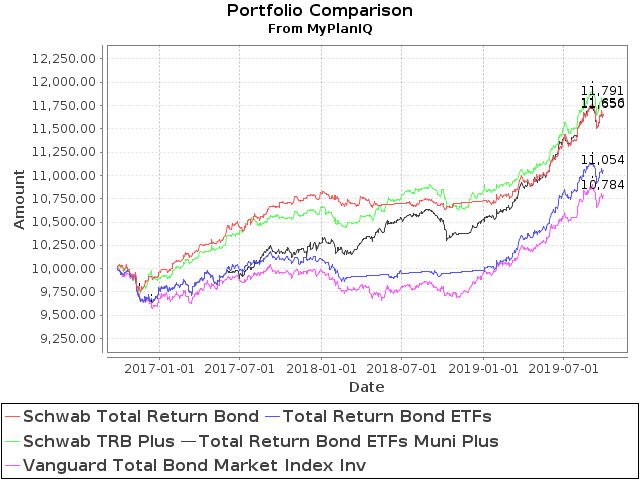

We explore a bond ETF portfolio that includes muni bond funds and show that it can probably match returns of mutual fund based portfolios.