Strategic Asset Allocation (SAA) is based on the main stream Modern Portfolio Theory: an investor decides asset allocation among major asset classes, based on personal long term risk and asset return expectations. Such an allocation is called strategic as it is meant to be long term oriented and should be only adjusted when some major events such as job change, getting closer to retirement etc. happen. As any asset allocation strategy, two critical factors should be considered:

- Risk tolerance: Being too aggressive could have damaging psychological and financial effects when markets perform poorly: often, investors are too late to realize that the portfolio is severely damaged and cannot bear with the risk anymore. Changing the portfolio allocation mix during market bottoms can have long term damage. On the other hand, being too conservative may not achieve the long term investment goal. Investors should pay careful attention to deciding the risk tolerance.

- Diversification: It is critical to diversify a portfolio into various uncorrelated assets. Different assets behave differently during different economic and market cycles. As long as these assets have reasonable long term expected returns, the diversification smoothes out the volatility of a portfolio and helps the portfolio to achieve better risk-adjusted return.

Major assets include US equity (which could be further decomposed into small, mid and large cap with value and growth styles), International equity, emerging market equity, real estate investment trusts (REITs) (US and and international), commodities and fixed income (consisting of US corporate bonds with investment grade or high yield (junk), treasury bonds with short, intermediate and long term maturity, inflation protected treasury (TIPs), foreign and emerging market bonds).

MyPlanIQ Strategic Asset Allocation - Optimal first divides available funds in a plan into two major categories: risky assets and fixed income assets. Other than high yield bonds, all other fixed income funds (including money market funds) are classified as fixed income assets. The Risk profile number is used to determine the target allocation of the fixed income assets. Unlike Strategic Asset Allocation - Equal Weight, Strategic Asset Allocation - Optimal uses long term historical performance data, asset class correlation, secular economic trends and other quantitative data of asset classes to determine optimal weights of major asset classes among risk assets and fixed income assets. It strives to balance risks in growth/recession and inflation/deflation scenarios. These allocations will be changed only when secular major economic and market trends change.

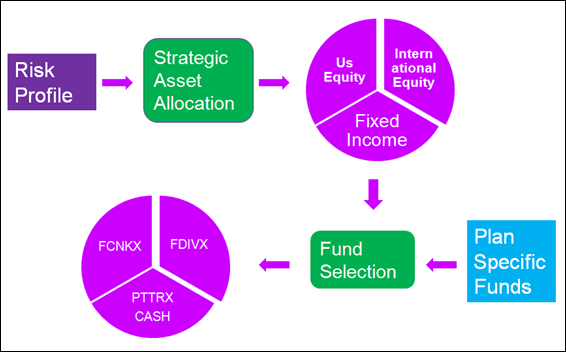

The following illustrates the process of this strategy:

In addition to the asset allocation, this strategy uses an advanced Fund Selection method to pick funds with the best risk-adjusted returns in an asset class from a plan when rebalancing.

A strategic asset allocation strategy is sometimes also called 'static', 'lazy' and 'buy and hold' strategy. Among them, there are several popular portfolios proposed by well known investors:

- Roger Gibson's diversified asset allocation portfolio

- David Swensen's Yale individual investor portfolio

- Ted Aronson's diversified portfolio

- William Bernstein four asset portfolio.

See Also

- Martin Gruber, Stephen Brown, William Goetzman, "Modern Portfolio Theory and Investment Analysis". Willey, 7th Edition, 2006.

- Roger Gibson. "Asset Allocation: Balancing Financial Risks". McGraw-Hill. 2007.

- William Bernstein, "The Four Pillars of Investing: Lessons for Building a Winning Portfolio". McGraw-Hill. 2002.

- Gary Gorton, Geert Rouwenhorst. "Facts and Fantasies about Commodity Futures".Yale University Research Paper. 2004.

- David Swesen, "Unconventional Success: A Fundamental Approach to Personal Investment". Free Press, Aug 2, 2005.

- Paul Farrell, "Marketwatch.com Lazy Portfolios". marketwatch.com. It maintains a list of lazy portfolios including the one called "Yale U's Unconventional" and "Aronson Family Taxable".

- William Bernstein, The July 1997 Coward's Portfolio. www.efficientfrontier.com, 1997.

Or Start FREE 30-day trial now >>