Tactical Asset Allocation (TAA) is based on major asset price trends. Major assets include US equity (which could be further decomposed into small, mid and large cap with value and growth styles), International equity, emerging market equity, real estate investment trusts (REITs) (US and and international), commodities and fixed income (consisting of US corporate bonds with investment grade or high yield (junk), treasury bonds with short, intermediate and long term maturity, inflation protected treasury (TIPs), foreign and emerging market bonds). Several academic and practical strategies have been published on the topic of TAA :

- Fama-French-Carhart 4 factor model on explaining a fund’s return; these include market return, size return (large/small), value return (value/growth) and momentum.

- Goldman Sachs Asset Management published and employed a so called global tactical asset allocation strategy in offshore and internal funds managed by Carhart and others.

- Global tactical asset allocation research paper by Blitz et. al.

- AQR (Applied Quantitative Research) funds such as recently launched AQR momentum fund.

The key is that economic and market forces often exhibit mega trends which may last for an extended period. Such mega trends in turn drive the corresponding asset prices.

As any asset allocation strategy, two critical factors should be considered:

- Risk tolerance: Risk tolerance: Being too aggressive could have a damaging psychological and financial effect when the markets perform poorly: often, investors are too late to realize that the portfolio is severely damaged and cannot bear with the risk anymore. Changing the portfolio allocation mix during market bottoms could have long term damage. On the other hand, being too conservative may not achieve the long term investment goal. Investors should pay careful attention to deciding the risk tolerance.

- Diversification: It is critical to choose a diversified array of assets. Different assets behave differently during different economic and market cycles. As long as these assets have reasonable long term expected returns, the diversification smoothes out the volatility of a portfolio and helps the portfolio to achieve better risk-adjusted return.

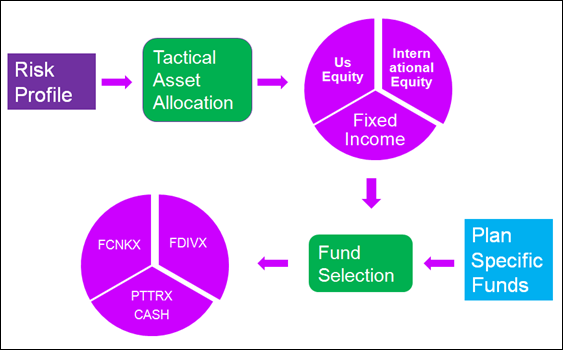

This strategy first divides funds available in a plan into two major categories: risky assets and fixed income assets. Other than high yield bonds, all other fixed income funds (including money market funds) are classified as fixed income assets. The Risk profile number is used to decide the target allocation to the fixed income assets. In each of the two major classes, it then uses price momentum to rank asset classes and then chooses top performing asset classes. After asset classes are chosen, the proprietary Fund Selection method is used to pick funds with the best risk adjusted returns from the available funds in the plan.

The following illustrates the process.

See Also

- Carhart, Mark, M. “On Persistence in Mutual Fund Performance“, Journal of Finance, Vol. 52 No. 1, March 1997.

- Blitz, David and Van Vliet, Pim, “Global Tactical Cross-Asset Allocation: Applying Value and Momentum Across Asset Classes“. Journal of Portfolio Management, May 2008.

- Asness, Clifford S., Moskowitz, Tobias J. and Pedersen, Lasse Heje, Value and MomentumEverywhere (March 6, 2009). AFA 2010 Atlanta Meetings Paper.

- Asness, Clifford, “The Power of Past Stock Returns to Explain Future Stock Returns”, Goldman Sachs Asset Management, 1995.

- Narasimhan Jegadeesh & Sheridan Titman, “Momentum“, SSRN Working Paper, 2001

- Doron Avramov, Russ Wermers, “Investing in mutual funds when returns are predictable”. Journal of Financial Economics 81 (2006) 339–377. For asset and industry rotation and fund selection.