-

What $1 Million Really Buys You in Retirement: Annuity vs. Investment Strategy

Most investors think about returns first. But what gets less attention, and probably deserves more, is volatility. Risk adjusted returns matter more. Being comfortable with portfoiio swings is the key to investment success.

-

Public Pay Might Be Higher Than You Think (Once You Do the Math)

In this issue:

- Latest in Retirement Savings & Personal Finance: High 401(k) Savings Rate, The Big Beautiful Bill’s Deficit Increase & Who Are Affected by the BBB

- Public Pay Might Be Higher Than You Think (Once You Do the Math)

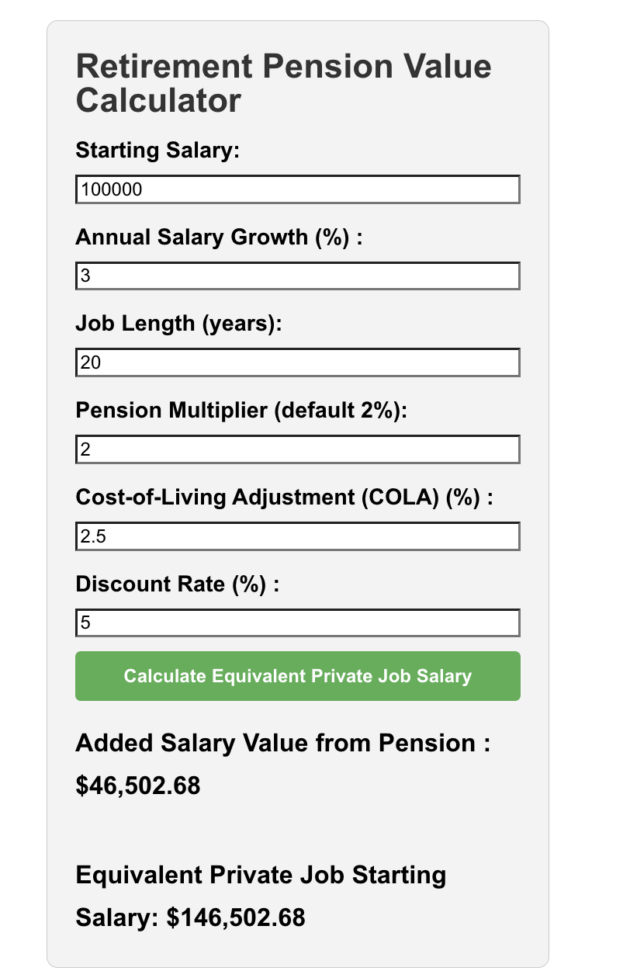

- Tools & Tips: Retirement Pension Value Calculator

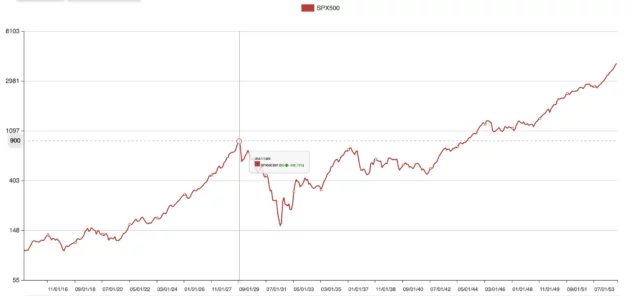

- Market Overview

-

Why Managing Volatility Matters

Most investors think about returns first. But what gets less attention, and probably deserves more, is volatility. Risk adjusted returns matter more. Being comfortable with portfoiio swings is the key to investment success.

-

Stock Compensation 101: How People Build Wealth (or Blow It)

In this issue:

- Latest in Retirement Savings & Personal Finance: Review and Get Rid of Your Unused Subscriptions, Private Equity & Crypto Investments in Your Retirement Accounts, Germany’s Early Start Pension

- Stock Compensation 101: How People Build Wealth (or Blow It)

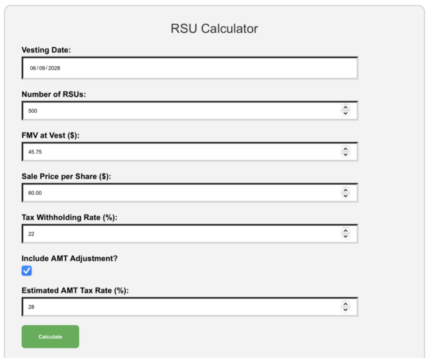

- Tools & Tips: RSU Calculator

- Market Overview

-

Retirement Plan Contribution Limits in 2024

2024 Retirement Plan Contribution Limits 1. 401(k), 403(b), and 457(b) Plans Employee Contributions: Up to $23,000 (under age 50) Catch-up contribution: $7,500 (ages 50+) Total Combined Limit (Employee + Employer): $69,000 Roth Options: Available for 401(k), sometimes for 403(b) and 457(b) Plan Details: 401(k): Primarily for for-profit companies; includes Roth (after-tax) options. 403(b): For public schools and nonprofits; Roth-style options less common. 457(b): For state/local government and some tax-exempt organizations; Roth availability varies. 2. Solo 401(k) and SEP IRA Solo 401(k): For self-employed individuals/business owners without employees.

- Employee contributions: $23,000, plus $7,500 catch-up (ages 50+)

- Employer contributions: up to 25% of compensation

- Total combined limit: $69,000 or 25% of compensation, whichever is less

SEP IRA: Employer contributes up to 25% of compensation, up to $69,000. No catch-up contribution. 3. SIMPLE IRA

- Employee contribution: up to $16,500

- Catch-up contribution: $3,500 (50+)

- Employer must match dollar-for-dollar up to 3% of employee salary

- Immediate vesting

4. Traditional and Roth IRAs

- Annual contribution: $7,000

- Catch-up: additional $1,000 (50+)

Traditional IRA: Pre-tax contributions, taxable upon withdrawal Roth IRA: After-tax contributions, tax-free withdrawals 5. Thrift Savings Plan (TSP)

- Federal and uniformed services employees only

- Employee contributions: up to $23,000 (under age 50), plus catch-ups ($7,500 at 50+)

- Employer matches up to 5% of salary

- Total Combined Limit (Employee + Employer): $69,000

- Pre-tax (traditional) and Roth contributions allowed

6. Payroll Deduction IRA

- Annual limit: $7,000; catch-up of $1,000 (age 50+)

- Pre-tax or Roth contributions

- No employer matching

7. Health Savings Account (HSA)

- Individual coverage: $4,150

- Family coverage: $8,300

- Catch-up contribution: additional $1,000 for age 55+

- Must have a high-deductible health plan

- Tax-free growth; penalty-free medical withdrawals; penalty-free non-medical withdrawals after age 65 (taxable)

8. Self-Directed IRA (SDIRA)

- Contribution limits same as IRAs ($7,000 + $1,000 catch-up age 50+)

- Allows alternative investments (real estate, precious metals, crypto)

- Requires IRS-approved custodian

9. Nondeductible IRA

- Same limits as traditional IRAs ($7,000 + $1,000 catch-up age 50+)

- Contributions not tax-deductible; earnings taxable at withdrawal

10. Annuities and Pension Plans (Brief Overview)

- Annuities: Insurance-based retirement products, providing guaranteed income. High fees, limited liquidity.

- Pension Plans: Employer-funded defined-benefit plans providing guaranteed lifetime income. Limited investment control.

11. Flexible Spending Account (FSA) Limits for 2024

- The maximum employee contribution to a health care FSA for 2024 is $3,200.

- If the FSA plan allows for carryover, the maximum amount that can be carried over to 2025 is $640.

- For Dependent Care FSAs, the maximum remains $5,000 per household (single or married filing jointly) or $2,500 if married and filing separately.

12. Health Savings Account (HSA) Limits for 2024 Coverage Type 2024 Contribution Limit Catch-Up (Age 55+) Minimum Deductible Out-of-Pocket Max Self-only $4,150 +$1,000 $1,600 $8,050 Family $8,300 +$1,000 (per eligible spouse, each in own HSA) $3,200 $16,100

- Individuals age 55 or older can contribute an additional $1,000 as a catch-up contribution.

- HSA contributions can be made until the tax filing deadline (April 15, 2025, for tax year 2024).

- To be eligible for HSA contributions, you must be enrolled in a high-deductible health plan (HDHP) meeting the minimum deductible and out-of-pocket maximum requirements above.

-

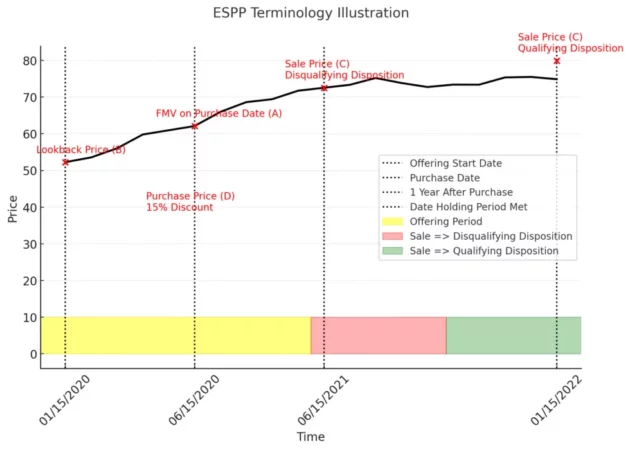

How to Take Advantage of Your ESPP (Employer Stock Purchase Plan)

In this issue:

- Latest in Retirement Savings & Personal Finance: Workplace Benefits like Flexible Spending & Telemedicine, AI Taking over Jobs?

- How to Take Advantage of Your ESPP (Employer Stock Purchase Plan)

- Tools & Tips: ESPP Tax and Cost Basis Calculator

- Market Overview

-

June 2025 MyPlanIQ Portfolio Update

In this issue:

- MyPlanIQ Composite Allocation Indicator & Applications

- Fund Analysis: Factor Funds & Healthcare Industry Trend

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

- Market Overview

-

How to Benefit from Your ESPP (Employer Stock Purchase Plan)

This article explains how to benefit from your ESPP (Employer Stock Purchase Plan) by looking at both short and long terms.

-

Simple 401(k) Investment Guide

In this issue:

- Latest in Retirement Savings & Personal Finance: College Education Affordability Declined, Rising Debt Puts Your 401(k) Retirement Savings in a Pickle

- Simple 401(k) Investment Guide

- Tools & Tips: 401(k) Investment Assistant

- Market Overview

-

Why Actively Managed Bond Funds Outperform Index Funds More Often Than Stocks

Multiple research results now point to what seems like a consistent pattern: active bond funds tend to outperform their passive peers more often than stock funds do.

-

Income Growth, Historical 401(k) Contribution Limit Data

In this issue:

- Latest in Retirement Savings & Personal Finance: Interest Rates Rise Again, Rising Home Insurance Cost, …

- Historical Income Growth, 401(k) Contribution Limit Growth

- Tools & Tips: 401(k) Maximum Match Calculator — Marvell Semiconductor

- Market Overview

-

How Much Should I Save for Retirement By Age? A Realistic Reference

In this issue:

- Latest in Retirement Savings & Personal Finance: Medicare Rude Surprise, Scoop to Be a Millionaire

- How Much Should I Save for Retirement By Age? A Realistic Reference

- Tools & Tips: Retirement Savings by Age Calculator

- Market Overview

-

Historical Year-by-Year Annual 401(k) Contribution Limits

Year-by-Year Annual 401(k) Contribution Limits since 1978. Also we include CPI inflation increase as a reference

-

Year-by-Year Income Levels in the U.S.

Year-by-Year Income Levels for Low, Middle and Upper Income Tiers in the U.S. since 1977

-

Realistic Reference Data on Retirement Savings by Age in 2025

A realistic accumulated savings figures by age in 2025 for various income level people.

-

Navigating the ExxonMobil Savings Plan: A Guide to Low-Cost Index Investing

ExxonMobil Savings Plan has simplest investment options lineup. Yet their expenses are extremely low, in fact the lowest among all.

-

Cadence Design Systems Inc. 401(k): A Plan with Low-Cost Target Date and Index Funds

Cadence Design Systems 401(k) Plan includes mainly ultra low-cost target date and index funds. We show these are good enough for its participants, experienced or novice.

-

Talmud desc

Talmud Portfolio for 401(k) and IRA Investors Investing for retirement, you know, it’s one of those things that sounds simple but gets messy fast. The Talmud Portfolio, well, it’s an old idea, rooted in Jewish wisdom, or so they say. It’s about splitting your money three ways, equal parts, into stocks, real estate, and bonds. Not too fancy, right? But there’s something about its balance that makes you pause. Is it too simple for today’s markets? Or maybe that’s the point? The Talmud, it’s a big deal in Jewish tradition, a collection of writings, debates, laws, and stories from centuries ago, like 3rd to 6th century or so. It’s got two parts, the Mishnah, which is like the core rulebook of Jewish law, and the Gemara, where rabbis argue and dig into what those rules mean. Think of it as a massive conversation, written down, about how to live right, covering everything from farming to ethics to marriage. The Babylonian Talmud, that’s the one most folks mean when they say “Talmud,” compiled in what’s now Iraq. It’s not just a book, it’s a way of thinking, questioning, balancing practical and spiritual. See more here. The portfolio, it supposedly comes from this one line about diversifying your assets, though I couldn’t pin down the exact quote. Point is, it’s about not betting everything on one horse, which feels like it fits today’s markets, no? Not much can be found on who exactly named this portfolio “Talmud,” just that it’s tied to that ancient advice. Diversify, don’t put all your eggs in one basket, that kind of thing. No flashy origin story, no guru preaching it on X. It’s just been around, quietly, like a recipe your grandma swears by. Its popularity? Hard to pin down. You don’t see it trending, but it pops up in forums, blogs, for folks who like straightforward plans. Talmud Portfolio Holdings Here’s how it breaks down:

- Stocks: VTMSX (33.4%)

- REITs: VGSIX (33.3%)

- Debt: VBMFX (33.3%)

Let’s look at this mix. Stocks, that’s your VTMSX, it’s a small-cap stock fund, which is interesting. Not your typical broad market index like the S&P 500. Small caps, they can be volatile, sure, but they’ve got growth potential over time. Historically, they’ve done well in recoveries, though they can take a beating in downturns. Then you’ve got REITs, VGSIX, real estate investment trusts. Real estate, it’s tangible, gives you income from rents, dividends. Bonds, VBMFX, that’s your total bond market fund, mostly intermediate-term, high-quality stuff. It’s the steady part, the one that keeps things from swinging too wild. Does it cover the big assets? Well, not quite. You’ve got US stocks, but only small caps. No international stocks, no emerging markets, no large caps either. Bonds are there, but nothing long-term like VUSTX or TLT, which, by the way, the Harry Browne Permanent Portfolio uses for deflation hedges. Long-term bonds, they tend to shine when markets tank or deflation hits, because their prices go up as yields drop. This portfolio skips that. No commodities either, no gold, which Harry Browne liked for inflation protection. Gold, it’s not everyone’s thing, but it can hold value when prices spike. REITs, though, they’re a standout here. Not every lazy portfolio leans into real estate like this. It’s a diversifier, sure, but tied to property cycles, which can be a rollercoaster. Pros? It’s dead simple. Three funds, equal weights, rebalance once a year, maybe. Diversification is decent, you’re not all-in on stocks or bonds. Small caps and REITs give you some growth and income potential, bonds keep it grounded. Cons? It’s light on global exposure. No international stocks, that’s a gap in a world where US markets don’t always lead. Small caps can be riskier than large caps, and REITs, well, they’re sensitive to interest rates. If rates rise, those dividends might not look so hot. Risk level? I’d say moderate. Not as sleepy as a 60/40 stock-bond mix, but not a crypto gamble either. It’s for someone who wants growth but can stomach some bumps. Using the Talmud Portfolio in 401(k) and IRA Accounts So, how do you make this work in a 401(k) or IRA? First, check your 401(k) plan. Most plans have a small-cap stock fund, maybe not VTMSX, but something close. Look for index funds first, low-cost ones. If you can’t find a small-cap index, pick a diversified actively managed small-cap fund. Go to Morningstar.com, check its diversification, expense ratio. Rule of thumb: keep fees low, make sure it’s not too concentrated in one industry. For REITs, it’s trickier. Some 401(k)s have real estate funds, but if not, you might map REITs to US stocks, maybe a total market fund. Not ideal, but it keeps you diversified. Bonds are easier, most plans have a total bond fund like VBMFX. If not, grab an intermediate-term bond fund, high-quality, or a total return bond fund if it’s actively managed. In an IRA, you’ve got more freedom. You can buy ETFs, like VB for small caps, VNQ for REITs, BND for bonds. ETFs are cheap, liquid, and track the same stuff as mutual funds. If your 401(k) is missing something, an IRA can fill the gap. Say your plan has no REITs, you could overweight REITs in your IRA to balance things out. Who’s this portfolio for? Investors who like simplicity, maybe don’t want to overthink things. It’s good for folks with 10, 20 years until retirement, who want some growth but not too much risk. If you’re younger, you might want more stocks. Older? Maybe more bonds. To scale it, figure out your risk tolerance first. Try MyPlanIQ’s Asset Allocation Calculator. Answer a few questions, it’ll tell you how much to put in stocks and REITs versus bonds. Say you’re conservative, you might go 20% small caps, 20% REITs, 60% bonds. Aggressive? Flip it, 40% each in small caps and REITs, 20% bonds. The equal-weight setup is just a starting point. Talmud Portfolio in Taxable Accounts Now, taxable accounts, that’s a different beast. The Talmud Portfolio, it’s got index funds, which are tax-efficient. ETFs like VB, VNQ, BND, they don’t churn holdings much, so capital gains distributions are low. You buy, you hold, you only pay taxes when you sell. REITs, though, they’re less tax-friendly. Those dividends, they’re often taxed as ordinary income, not qualified dividends. If you’re in a high tax bracket, that stings. Bonds in taxable accounts? Interest is taxed yearly, so keep an eye on that. Buy-and-hold is the name of the game here. Rebalance sparingly, maybe sell a bit when one asset gets too heavy. Tax-loss harvesting? It’s an option. If small caps dip, sell VB, buy a similar fund like IJR, book the loss for taxes, but stay in the market. Just watch the wash-sale rule, don’t buy the same fund back within 30 days. This portfolio’s simplicity makes that easier, fewer moving parts to track. Final Thoughts The Talmud Portfolio, it’s not perfect, but what is? It’s got this old-school vibe, like advice you’d hear from someone who’s been through a few market crashes. Diversify, keep it simple, don’t chase trends. For 401(k) or IRA investors, it’s a solid starting point, especially if you’re not into picking stocks or timing markets. Taxable accounts? It works, just mind the REITs and bonds. Markets will do what they do, whip around, scare everyone. But this portfolio, it’s like a house with a good foundation. Maybe it sways, but it’s built to last. Or at least, that’s the hope, right?

-

Rick Ferri Core Four Lazy Portfolio desc

Rick Ferri Core Four: A Solid Lazy Portfolio for Retirement Investors Investing for retirement can feel like a maze sometimes. You wonder, what’s the simplest way to build a portfolio that works for the long haul? Well, the Rick Ferri Core Four portfolio might just be one of those answers. It’s straightforward, it’s diversified, and it’s built for people who don’t want to spend their days glued to stock charts. Let’s take a look at what this portfolio is, why it makes sense for retirement accounts like 401(k)s or IRAs, and how it holds up for taxable accounts too. Rick Ferri, the guy behind this portfolio, is a name you might have come across if you’ve poked around in the world of low-cost investing. He’s a former Marine, a CFA, and someone who’s been preaching the gospel of index funds for years. His philosophy? Keep it simple, keep costs low, and let the market do its thing over time. The Core Four portfolio is his way of saying, you don’t need a hundred funds to build wealth. Four will do just fine. Is it popular? Hard to say exactly, but you see it mentioned often enough in forums like Bogleheads, where folks who love simple investing hang out. Rick Ferri Core Four Holdings Here’s what the Core Four portfolio looks like:

- VTSMX (US Stocks): 30.0%

- VGTSX (International Stocks): 24.0%

- VGSIX (REITs): 6.0%

- VBMFX (Bonds): 40.0%

This mix covers a lot of ground. You’ve got US stocks, international stocks, real estate through REITs, and bonds. It’s like a balanced meal, you know? Each part serves a purpose. The US stocks (VTSMX) give you exposure to the broad American market, everything from Apple to small-cap companies nobody’s heard of. International stocks (VGTSX) add some global flavor, which is nice because the US doesn’t always lead the pack. REITs (VGSIX) are there for real estate, which can zig when stocks zag. And bonds (VBMFX)? They’re the anchor, keeping things steady when markets get choppy. But does it cover everything? Well, it hits the major assets: US stocks, international stocks, bonds. REITs are a bonus, adding a bit of diversification since real estate doesn’t always move in lockstep with stocks. What’s missing? No emerging market stocks, no small-cap stocks as a standalone, no commodities or gold. If you’re thinking about inflation hedges like gold, you might look at something like the Harry Browne Permanent Portfolio. That one includes gold to protect against inflation, which can eat away at returns over time. The Core Four skips that, which might be a drawback if you’re worried about rising prices. On the other hand, it keeps things simpler. Risk-wise, this portfolio is moderate. The 40% in bonds gives it some cushion, but with 60% in stocks and REITs, it’s not exactly a sleepy conservative portfolio either. It’s suited for someone who’s okay with some ups and downs but doesn’t want to ride the full rollercoaster of an all-stock portfolio. If you’re younger, maybe in your 30s or 40s, this could work well for a 401(k) or IRA. If you’re closer to retirement, you might want to tilt it safer, maybe bump up the bonds. How do you know what’s right? A tool like MyPlanIQ’s Asset Allocation Calculator can help you figure out your risk tolerance. Answer a few questions, and it’ll tell you how much to put in stocks versus bonds. Using the Core Four in a 401(k) or IRA So, how do you actually use this portfolio in a 401(k) or IRA? First, check what funds your 401(k) offers. Most plans have something close to VTSMX, like an S&P 500 index fund or a total stock market fund. For international stocks, look for a broad international index fund. REITs might be trickier—some 401(k)s don’t offer them. If that’s the case, you could map REITs to US stocks, since they’re somewhat correlated. For bonds, find a total bond market fund or a core bond fund. If your 401(k) doesn’t have index funds, look for diversified active funds with low expense ratios. You can check diversification and fees on a site like Morningstar.com. The rule of thumb? Stick to index funds for stocks, and for bonds, go for core bond funds or high-quality actively managed ones (see fixed income investments for more). In an IRA, it’s easier. You can usually buy the exact ETFs or mutual funds, like Vanguard’s VTI (for VTSMX) or BND (for VBMFX). If you want to tweak the portfolio for risk, it’s simple. Say you’re more cautious, you might go 50% bonds, 25% US stocks, 20% international stocks, 5% REITs. More aggressive? Maybe 40% US stocks, 30% international, 10% REITs, 20% bonds. The key is to match your risk tolerance, which you can gauge with that calculator we mentioned. One thing stands out about the Core Four: it’s simple but not simplistic. Four funds, and you’re covering most of the bases. That 6% in REITs is a nice touch, giving you a slice of real estate without needing to buy properties. But the lack of emerging markets or commodities? It’s a trade-off. You’re betting on the big, broad markets to carry you through. Historically, that’s worked out, but no portfolio is bulletproof. Core Four in Taxable Accounts Now, what about taxable brokerage accounts? The Core Four shines here because it’s built on index funds, which are tax-efficient. Index funds like VTSMX or VGTSX don’t trade stocks often, so they generate fewer capital gains. ETFs like VTI or VXUS are even better for taxable accounts since they’re structured to minimize taxes. The buy-and-hold nature of this portfolio also helps. You’re not flipping funds every year, so you’re not triggering taxes constantly. Could you do tax-loss harvesting? Sure. If one fund dips, you could sell it, book the loss for tax purposes, and buy a similar fund (like swapping VTI for SCHB). Just be careful about wash-sale rules. But honestly, the Core Four is already tax-friendly because it’s so hands-off. One catch with taxable accounts is the REITs. VGSIX generates dividends that aren’t always tax-advantaged, so you might take a small tax hit there. If that bothers you, you could skip REITs in a taxable account and stick with the other three funds. But for most people, that 6% allocation won’t move the needle much tax-wise. Final Thoughts The Rick Ferri Core Four is one of those portfolios that feels like a warm blanket. It’s not flashy, it’s not trying to beat the market, but it gets the job done. For 401(k) or IRA investors, it’s a solid starting point, especially if you’re new to investing or just want something you can set and forget. In taxable accounts, it’s efficient, though you might tweak it slightly for taxes. Is it perfect? No portfolio is. If inflation spikes or emerging markets take off, you might wish you had a bit more exposure. But then again, chasing every possibility is how you end up with a portfolio that’s too complicated to manage. Maybe you’re wondering, will this portfolio hold up for the next 20 years? Nobody knows for sure. Markets are funny like that. But looking back, simple, diversified portfolios like this one have done pretty well over long periods. They’re like the tortoise in the race, slow and steady. And in investing, that’s often enough. What do you think, is simple better for you? Or are you tempted to add a little spice to the mix?

-

Warren Buffett’s Phenomenal Run: The Oracle May Retire, But His Legacy Endures

In this issue:

- Latest in Retirement Savings & Personal Finance: Social Security Early Claims Surge, Student Loan Collection Resumed, …

- Warren Buffett’s Phenomenal Run: The Oracle May Retire, But His Legacy Endures

- Tools & Tips: Rolling Return Calculator

- Market Overview