-

llama3.1 Calculator Example

Contributions: Participants can contribute between 6% and 20% of their eligible pay to the Plan. Company match: The Company matches the minimum 6% contribution with an amount equal to 7% of the participant’s eligible pay. However, Company matching contributions were suspended from October 1, 2020, until they were reinstated on October 1, 2021. Participants who are 50 or older during the plan year and have maximized their regular pretax and Roth contributions can make additional contributions. Vesting: Participants are immediately vested in their own contributions and all associated earnings. Company contributions vest at 100% after 3 years of service, upon reaching age 65 while employed, or upon death while still an employee. 401(k) Contribution Calculator Bi-Weekly Pay Amount: Age: Calculate function calculateMatch() { const payAmount = parseFloat(document.getElementById(‘payAmount’).value); const age = parseInt(document.getElementById(‘age’).value); const annualLimit = 23000; const catchUpLimit = 7500; let contributionLimit = annualLimit; if (age >= 50) { contributionLimit += catchUpLimit; } const numPayPeriods = 26; // Bi-weekly pay periods in a year const maxContributionPerPaycheck = contributionLimit / numPayPeriods; // Contribution between 6% and 20% of pay const minContributionPercentage = 0.06; const maxContributionPercentage = 0.20; // Company match policy const minMatchPercentage = 0.07; // To maximize the match, we need to contribute at least 6% of pay const minimumContribution = payAmount * minContributionPercentage; const matchPerPaycheck = Math.min(minimumContribution * minMatchPercentage, payAmount * minMatchPercentage); const annualMaxMatch = matchPerPaycheck * numPayPeriods; // Output results document.getElementById(‘contributionAmount’).innerText = `Each Paycheck Contribution Amount: $${minimumContribution.toFixed(2)}`; document.getElementById(‘paycheckMatch’).innerText = `Each Paycheck Match Amount: $${matchPerPaycheck.toFixed(2)}`; document.getElementById(‘annualMaxMatch’).innerText = `Annual Maximum Match Amount: $${annualMaxMatch.toFixed(2)}`; document.getElementById(‘annualContribution’).innerText = `Annual Contribution Amount: $${Math.min(contributionLimit, minimumContribution * numPayPeriods).toFixed(2)}`; }

-

Constructing a Balanced, Diversified Asset Allocation Portfolio for Blue Shield of California Tax Deferred Salary Investment Plan Participants

Participating in the Blue Shield of California Tax Deferred Salary Investment Plan offers a solid foundation for your retirement savings. To maximize the potential of your retirement plan, understanding how to construct a balanced and diversified asset allocation portfolio is crucial. This article will guide you through a structured four-step RAID approach: Risk assessment, Asset allocation, Investment selections, and Disciplined rebalancing. Investment Options Below are your available investment options within the plan:

- FIDELITY BROKERAGELINK MUTUAL FUNDS

- FIDELITY EXTENDED MARKET INDEX FUND MUTUAL FUNDS

- FIDELITY GOVERNMENT CASH RESERVES MUTUAL FUNDS

- FIDELITY U.S. BOND INDEX FUND MUTUAL FUNDS

- BLACKROCK TOTAL RETURN BOND FUND M

- DIAMOND HILL LARGE CAP PORTFOLIO FEE CLASS L

- FIDELITY GROWTH COMPANY COMINGLED POOL CLASS 3

- GALLIARD STABLE VALUE FUND X

- HARDING LOEVNER INTERNATIONAL EQUITY – CLASS BN

- SPARTAN 500 INDEX POOL CLASS E

- STATE STREET TARGET RETIREMENT INCOME FUND CLASS IV

- STATE STREET TARGET RETIREMENT 2020 FUND CLASS IV

- STATE STREET TARGET RETIREMENT 2025 FUND CLASS IV

- STATE STREET TARGET RETIREMENT 2030 FUND CLASS IV

- STATE STREET TARGET RETIREMENT 2050 FUND CLASS IV

- STATE STREET TARGET RETIREMENT 2055 FUND CLASS IV

- STATE STREET TARGET RETIREMENT 2060 FUND CLASS IV

- THE PRINCIPAL DIVERSIFIED REAL ASSET COLLECTIVE INVESTMENT FUND

- VANGUARD INSTITUTIONAL TOTAL INTERNATIONAL STOCK MARKET INDEX TRUST

- WTC-CIF II SMID-CAPE RESEARCH EQUITY SERIES 4

These options cover the following major asset classes:

- US stocks: FIDELITY EXTENDED MARKET INDEX FUND, DIAMOND HILL LARGE CAP PORTFOLIO, FIDELITY GROWTH COMPANY COMINGLED POOL, SPARTAN 500 INDEX POOL, WTC-CIF II SMID-CAPE RESEARCH EQUITY SERIES

- International stocks: HARDING LOEVNER INTERNATIONAL EQUITY, VANGUARD INSTITUTIONAL TOTAL INTERNATIONAL STOCK MARKET INDEX TRUST

- REITs: THE PRINCIPAL DIVERSIFIED REAL ASSET

- Bonds: FIDELITY GOVERNMENT CASH RESERVES, FIDELITY U.S. BOND INDEX FUND, BLACKROCK TOTAL RETURN BOND FUND, GALLIARD STABLE VALUE FUND

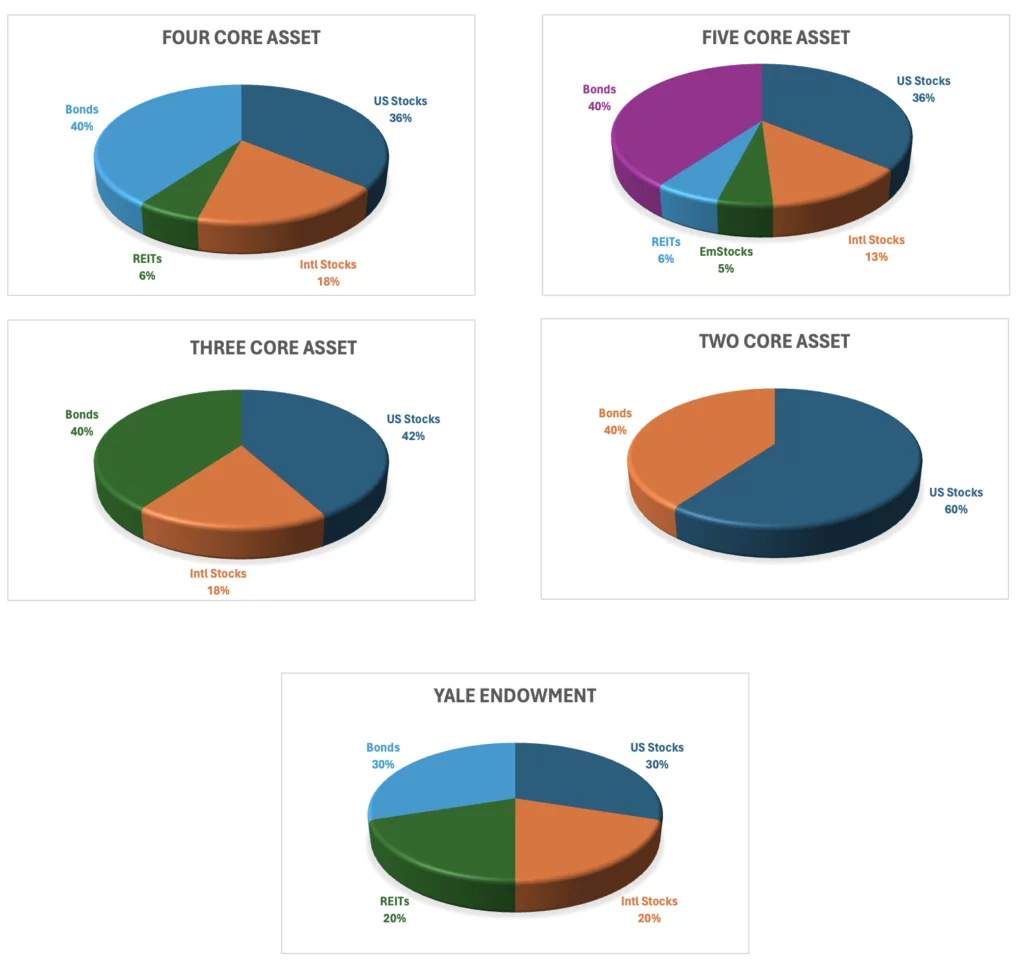

Four-Step RAID Approach 1. Risk Assessment Determining your risk profile is the first step. Consider factors such as your age, risk tolerance, job stability, and growth expectations. This comprehensive guide on how to decide your stock allocation can assist in defining your risk profile. Generally, younger investors with longer investment horizons and higher risk tolerance can allocate a larger portion of their portfolio to stocks. Conversely, older investors closer to retirement might prefer a higher allocation to bonds for capital preservation. 2. Asset Allocation Next, decide on the allocation to each major asset class. You can refer to these asset allocation templates for guidance based on your risk profile. Given the available investment options, we cover portfolios for the following major asset classes: US stocks, international stocks, REITs, and bonds. Example of a Moderate Asset Allocation Portfolio:

- 36% US stocks

- 18% International stocks

- 6% REITs

- 40% Bonds

3. Investment Selections Select funds for each asset class:

- US Stocks (36%): Allocate to Spartan 500 Index Pool Class E, Fidelity Growth Company Commingled Pool Class 3, Diamond Hill Large Cap Portfolio Fee Class L

- International Stocks (18%): Allocate to Vanguard Institutional Total International Stock Market Index Trust, Harding Loevner International Equity Class BN

- REITs (6%): The Principal Diversified Real Asset Collective Investment Fund

- Bonds (40%): Fidelity U.S. Bond Index Fund, BlackRock Total Return Bond Fund M

4. Disciplined Rebalancing Regularly monitor your portfolio and rebalance it to maintain your desired asset allocation. Over time, asset performance will cause your allocations to drift. Rebalancing ensures you stay on track to achieve your long-term investment goals. Prioritize low-cost index funds where possible, particularly for the stock portion of your portfolio, to maximize returns by minimizing fees. By following the RAID approach and using the recommended resources, you can effectively construct a balanced and diversified asset allocation portfolio. This will help you achieve your retirement goals in a disciplined and structured manner.

-

CADENCE DESIGN SYSTEMS, INC. 401(K) PLAN Contribution & Match Policies

CADENCE DESIGN SYSTEMS, INC. 401(K) PLAN Contribution & Match Policies Contributions Participants can contribute up to $23,500 in 2025, with an additional $7,500 catch-up contribution allowed if age 50 or older. Employer Match Employer contributions: The Company matches 50% of each eligible participant’s contribution up to a maximum of 6% of the participant’s eligible compensation. Discretionary company contributions and profit-sharing contributions are also allowed. Vesting Participants are immediately vested in their contributions and discretionary Company contributions. Participants are fully vested in employer matching and profit-sharing contributions allocated to their account after four years of credited service. CADENCE DESIGN SYSTEMS, INC. 401(K) PLAN Maximum Match Calculator This calculator helps to decide the minimum contribution you need to get the maximum employer match. Bi-weekly Pay Amount ($): Age: Calculate function calculateMatch() { const pay = parseFloat(document.getElementById(“payInput”).value); const age = parseInt(document.getElementById(“ageInput”).value); const resultsDiv = document.getElementById(“results”); if (isNaN(pay) || isNaN(age) || pay contributionLimit) { targetContribution = contributionLimit; } const biWeeklyContribution = targetContribution / payPeriods; // Match = 50% of employee contribution, capped at 3% of pay const maxEmployerMatch = annualPay * 0.03; const employerMatch = Math.min(targetContribution * 0.5, maxEmployerMatch); const biWeeklyMatch = employerMatch / payPeriods; document.getElementById(“biWeeklyContribution”).innerHTML = “Bi-weekly Minimal Contribution ($): ” + biWeeklyContribution.toFixed(2); document.getElementById(“annualContribution”).innerHTML = “Total Annual Minimal Contribution ($): ” + targetContribution.toFixed(2); document.getElementById(“biWeeklyMatch”).innerHTML = “Bi-weekly Employer Match ($): ” + biWeeklyMatch.toFixed(2); document.getElementById(“annualMatch”).innerHTML = “Total Annual Employer Match ($): ” + employerMatch.toFixed(2); }

-

The Best Stock Funds In The Long-Term

In this newsletter, we unveil the ‘best’ long-term stock mutual fund! We discuss its investment methodology and use our own unique tools to measure it against other excellent long-term stock funds.

-

test for dentons-cohen-grigsby-pc-pension-plan match

Nothing but example

-

How to Build a Balanced, Diversified Portfolio with the BLOODWORKS NORTHWEST RETIREMENT PLAN

How to Build a Balanced, Diversified Portfolio with the BLOODWORKS NORTHWEST RETIREMENT PLAN Constructing a balanced, diversified portfolio is essential for long-term financial health, especially when it comes to retirement planning. As a participant in the BLOODWORKS NORTHWEST RETIREMENT PLAN, you have a range of investment options available. In this article, we’ll guide you through the process of constructing a well-rounded portfolio using the four-step RAID approach: Risk Assessment, Asset Allocation, Investment Selections, and Disciplined Rebalancing. We’ll focus on utilizing the low-cost index funds available to you whenever possible. Investment Options Available in Your Plan Here are the investment options available to you: Step 1: Risk Assessment The first step in constructing your portfolio is assessing your risk tolerance. Risk tolerance is the degree to which you’re comfortable with the potential for losses in your investments in exchange for the possibility of higher returns. Your risk tolerance should be influenced by your age, job stability, financial goals, and time horizon. To help decide how much of your portfolio should be allocated to stocks versus bonds, you can refer to the MyPlanIQ Get Started Now guide. Typically, younger investors with longer time horizons can afford to take on more risk by allocating a higher percentage to stocks, while those nearing retirement may want to shift more towards bonds for stability. Step 2: Asset Allocation After determining your risk profile, the next step is to decide how to allocate your investments across various asset classes. The main asset classes available to you in the BLOODWORKS NORTHWEST RETIREMENT PLAN include: You can use asset allocation templates discussed in MyPlanIQ’s Asset Allocation Portfolio Templates. For example, a balanced portfolio for a moderate risk investor might allocate 42% to US stocks, 18% to international stocks, and 40% to bonds. Step 3: Investment Selections Once you’ve determined your asset allocation, you’ll need to select the specific funds that match each asset class. For example: Emphasizing low-cost index funds where possible will help you minimize expenses and maximize returns over the long term. Step 4: Disciplined Rebalancing Regular monitoring and rebalancing of your portfolio are crucial for maintaining your desired asset allocation. Over time, market fluctuations can cause your portfolio to drift from its original allocation. For instance, if stocks outperform bonds, your portfolio may become more stock-heavy, increasing your risk level. Periodically rebalancing—selling some of the better-performing assets and buying more of the underperforming ones—helps you stay on track with your investment strategy. Example Portfolio with Moderate Risk Using the principles above, here’s an example of how you might construct a moderate risk (60% stocks, 40% bonds) portfolio: This simple portfolio provides broad diversification across key asset classes while keeping costs low, helping you stay aligned with your retirement goals. Conclusion Constructing a balanced and diversified portfolio is an ongoing process that involves regular monitoring and adjustments. By following the RAID approach—Risk Assessment, Asset Allocation, Investment Selections, and Disciplined Rebalancing—you can build a portfolio that aligns with your risk tolerance, financial goals, and time horizon. Remember, the key to successful retirement investing is to start early, stay consistent, and remain disciplined in your approach. For more information, refer to the MyPlanIQ Four-Step Guide for 401k Retirement Investing and the Asset Allocation Portfolio Templates.

-

Asset Allocation Portfolio Templates for 401(k) Investments

This article shows the most popular asset allocation core portfolio templates for long-term investments such as a retirement investment account like 401(k) account, IRA or a taxable brokerage account.

-

Four-Step Guide for 401(k) Retirement Investing

Navigating the complex world of 401(k) retirement investing can be daunting, especially when faced with many investment options. However, by following these four simple steps, you can prudently construct your investment portfolios that suit your personal situation. These four steps are: Risk Assessment, Asset Allocation, Investment Selection, Disciplined Rebalancing & Staying the Course — RAID for short. Step 1: Risk Assessment Before delving into the array of investment options or funds given in your plan, it’s crucial to define your risk profile and investment horizon. Consider the following sub-steps: Once you have decided how much your risk asset allocation should be, the next step is to pick an asset allocation. Step 2: Asset Allocation Now that you’ve defined your risk profile, the next step is to determine the allocation of assets within your chosen risk profile. A straightforward yet effective approach to determining asset allocation is to select a template from various well-known lazy portfolios recommended by investment experts. These templates have been widely used by financial advisors and investment managers. Subsequently, adjust the risk asset allocation based on your risk profile. For further details, refer to Asset Allocation Portfolio Templates. Note: The asset allocation template you choose should align with the investment options available in your 401(k) plan. For instance, if your plan offers only US stock and bond funds, you will need to select a template that accommodates these two asset classes. Step 3: Investment Selection For each asset class you choose to invest, you’ll need to decide what funds in this asset class in your plan’s avaiable investment options to invest. There are several simple criteria one should follow: Step 4: Disciplined Rebalance & Stay the Course Set up a schedule for regular portfolio reviews and rebalancing to ensure that your asset allocation remains aligned with your long-term financial goals. It’s recommended to be cautious about excessive rebalancing, as it can potentially harm your investment returns, especially when done without a systematic and sound strategy. For the average investor, an annual rebalancing approach could be a prudent choice. Refer to the AAII (American Association for Individual Investors) article Selecting Asset Classes for Retirement Investments or this link on our site for more discussions on asset classes and fund choices. Disclaimer: The information provided above is for educational purposes only. If your specific situations require it, it is advisable to consult with a financial advisor or a professional to address your individual needs and circumstances.

-

Stock Seasonality Strategy: Consistency Leads to Long-Term Success

In this newsletter, we revisit a well-known stock anomaly: seasonality. We further demonstrate that this seasonality extends to other stock funds and balanced funds as well.

-

Quality Business Models Triumph: What Insurance Broker Stock Returns Can Teach Us

In this newsletter, we highlight stocks from a particularly excellent yet somewhat surprising industry—insurance brokers—that have consistently delivered higher returns compared to stock indexes such as the S&P 500.

-

Gold’s Long-Term Performance: Historical Returns and Key Drivers

We review gold’s long-term returns since 1971. We further examine key drivers that are behind gold returns and point out these factors, inflation, inflation expectation, interest rates, economic uncertainties, international demand and geopolitical events, have a more complex relationship with gold prices.

-

150+ Years of Long-Term Earnings and Stock Returns of the ‘Conglomerate’ of Collective S&P 500 Index Companies

We look at over 150 years data on S&P 500 earnings and total returns. We then study the rolling returns and compare it with a moving average based portfolio. We conclude that S&P 500 index represents a fantastic ‘business’ to own.

-

Factor ETFs For Diversification & Return Improvement

We review smart factor ETFs and a momentum portfolio based on these factor ETFs. We argue that major factor ETFs like Quality, Momentum, GARP, Minimum Volatility, Value and Size all have potential to outperform cap-weighted stock indexes such as S&P 500. These ETFs can be effective builindg components for a core portfolio.

-

Newsletter Collection Update

We list our latest newsletter articles since last update and briefly overview current market conditions

-

Total Return Investments vs. High Yields: Yield Chasing at Your Own Peril

We examine various high dividend ETFs and a closed end fund and discuss how they fare in terms of total returns that combine both capital appreciation and dividend income.

-

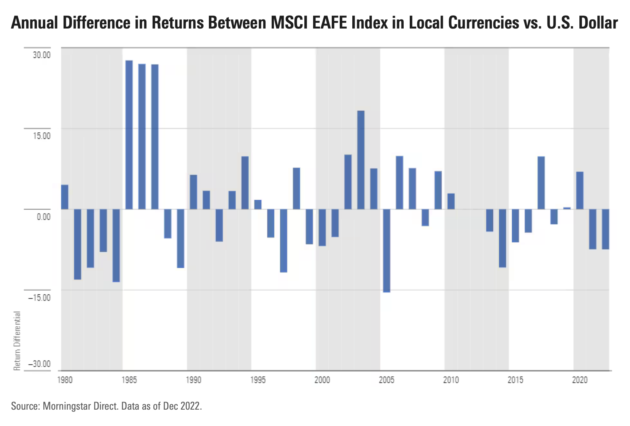

Foreign Stock Investments — Currency Hedged Or Not?

We delve into the details to examine the role of currency-hedged ETFs in international stock investing within an asset allocation portfolio.

-

Unlocking Investment Potentials With 401(k) Brokerage Link Accounts

We discuss the pros and cons of 401(k) brokerage link accounts

-

Ranking Biggest 401(K) Stock And Bond Funds

We discuss how to utilize our newly upgraded free comparison tool to better evaluate and compare ETFs, mutual funds and portfolios using rolling returns

-

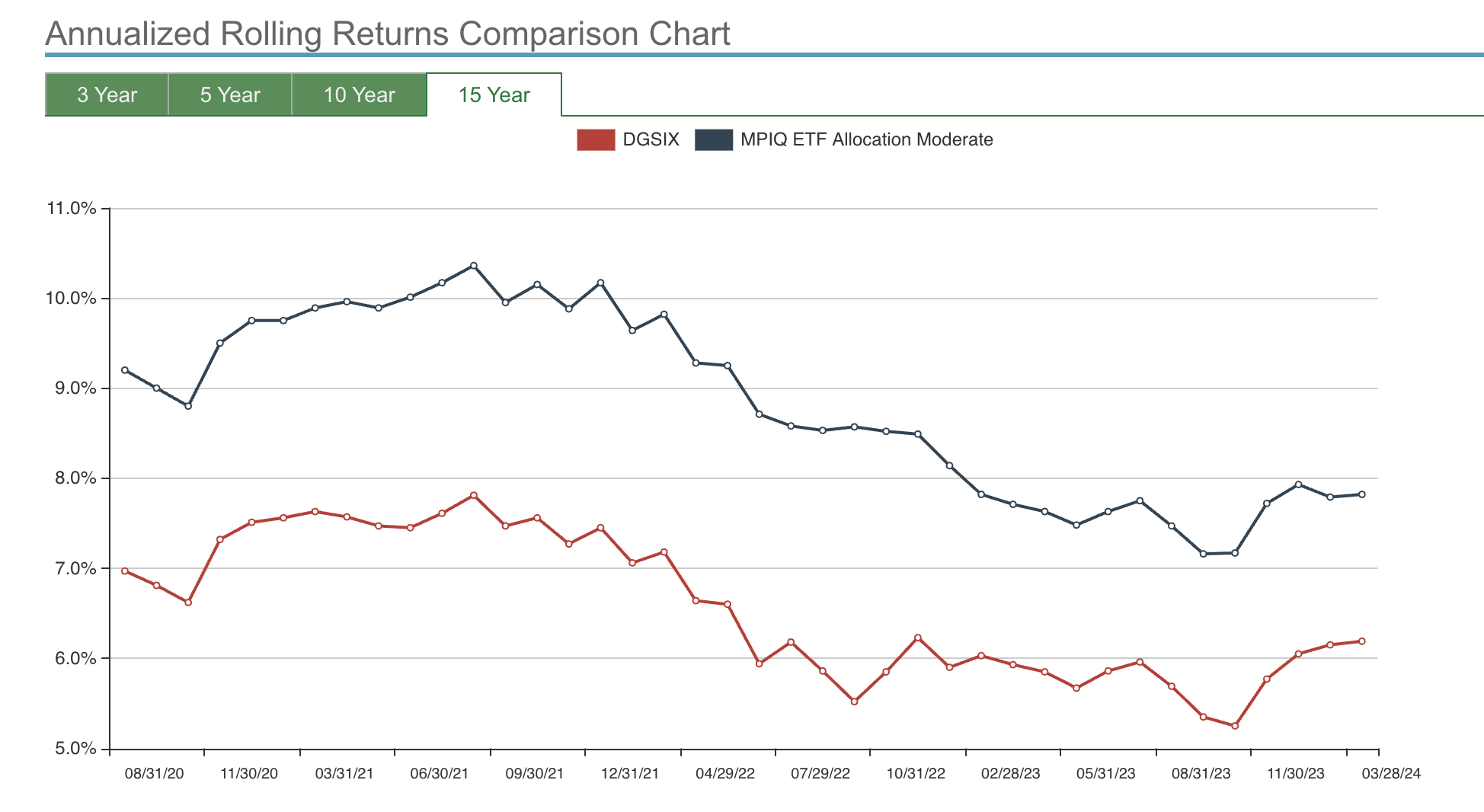

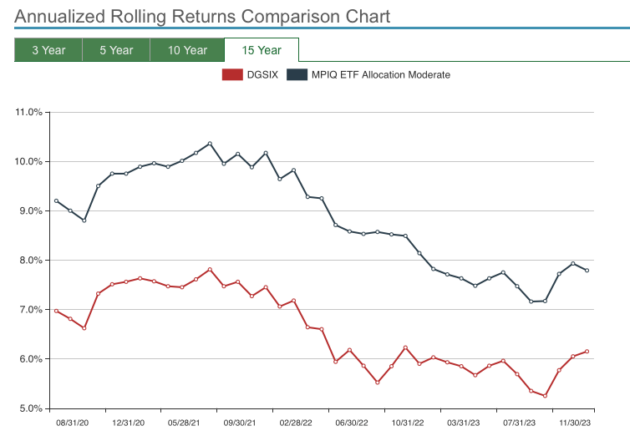

Rolling Returns: A Better Way To Evaluate & Compare Investments

We discuss how to utilize our newly upgraded free comparison tool to better evaluate and compare ETFs, mutual funds and portfolios using rolling returns

-

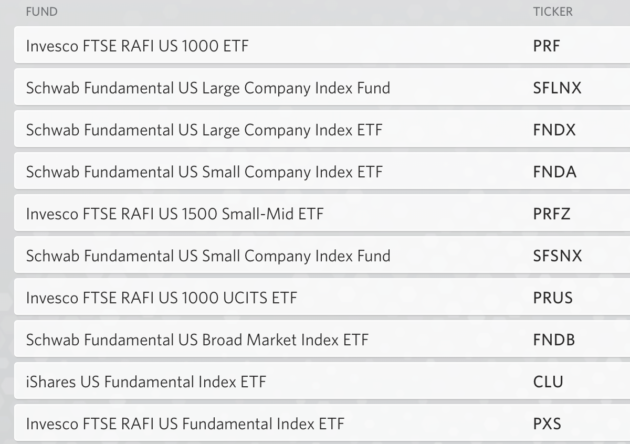

Index Funds As Businesses — Fundamental Indexing

Introducing fundamental index funds that align with business owner’s approach in investing. We also show how these funds have consistently outperformed.