The amount you need to save for retirement depends on several factors, including your current age, expected retirement age, expected retirement expenses, lifestyle goals, and expected retirement income from sources such as Social Security, pensions, and investments. Furthermore, your profession can have a significant impact on your retirement savings, as average incomes can vary widely between professions.

Rule of thumb: As a general rule of thumb, financial advisors often recommend saving 10-15% of your income for retirement throughout your working years. However, this is not a one-size-fits-all approach, and your personal circumstances and goals may require a different approach.

It’s also important to consider inflation and the potential for unexpected expenses, such as healthcare costs and long term care, in retirement.

Here are some numbers based on several surveys:

Tech workers

According to a survey by online lender SoFi, the average savings rate for tech workers is around 8% of their annual income. However, this figure can vary widely depending on individual circumstances such as age, income, debt, and financial goals.

This number is surprising as tech workers typically have higher income and not that much work related expenses.

Physicians

According to a survey conducted by Medscape, the average physician salary in the United States in 2020 was $243,000 per year. The recommended savings rate for physicians is generally around 20-25% of their income, but this may vary depending on individual financial goals and circumstances.

Physicians often have high levels of student loan debt and may also face high expenses associated with running a medical practice. However, their high incomes can also allow for significant savings opportunities.

Average Americans

According to a survey by financial services provider Charles Schwab, the average savings rate among Americans in 2021 was 14.8%. However, this figure can vary widely depending on individual circumstances such as age, income, debt, and financial goals.

According to Vanguard Group’s 2022 “How America Saves” report, the average savings rate for participants in employer-sponsored defined contribution retirement plans was 8.4% in 2020. The report notes a slight increase from the 8.1% savings rate observed in 2010.

The report also highlights the trend of increased savings rates among participants, particularly for those in plans that feature automatic enrollment and escalation. Among participants in automatic enrollment plans, the average savings rate was 6.9% in 2020, up from 6.5% in 2010. Similarly, participants in plans that feature automatic escalation saw their average savings rate increase from 6.9% in 2010 to 8.5% in 2020.

Notice the Vanguard report is only based on retirement plans. It doesn’t include data for other taxable savings that include taxable stock, bond and cash investments or even real estate investments. Adding this up, it’s possible that a typical Vanguard client might reach 10-15% savings rate, recommended by financial advisors.

Can you preserve your retirement life quality if you save at the average rate?

Naturally, you would ask if I save just like an average American at an annual rate 10%-15%, how much would I accumulate by the time I retire? Will that be enough to preserve my quality of life in retirement?

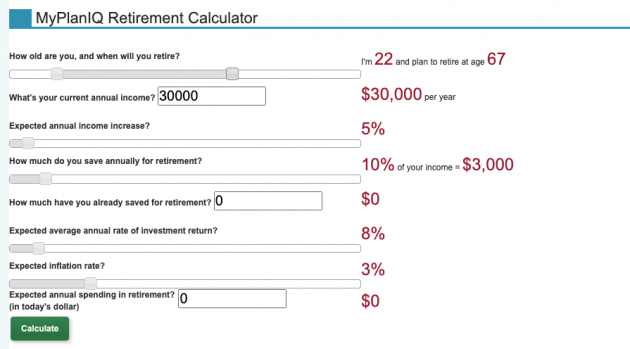

We use our Retirement Calculator and assume the following:

The following is the annual income and investment balance:

| Age | Annual Income ($) | Investment Balance ($) |

| 22 | 30,000 | 0 |

| 23 | 31,500 | 3,000 |

| 24 | 33,075 | 6,390 |

| 25 | 34,729 | 10,209 |

| 26 | 36,465 | 14,499 |

| 27 | 38,288 | 19,305 |

| 28 | 40,203 | 24,678 |

| 29 | 42,213 | 30,673 |

| 30 | 44,324 | 37,348 |

| 31 | 46,540 | 44,768 |

| 32 | 48,867 | 53,003 |

| 33 | 51,310 | 62,130 |

| 34 | 53,876 | 72,231 |

| 35 | 56,569 | 83,397 |

| 36 | 59,398 | 95,726 |

| 37 | 62,368 | 109,324 |

| 38 | 65,486 | 124,307 |

| 39 | 68,761 | 140,800 |

| 40 | 72,199 | 158,940 |

| 41 | 75,809 | 178,875 |

| 42 | 79,599 | 200,766 |

| 43 | 83,579 | 224,787 |

| 44 | 87,758 | 251,128 |

| 45 | 92,146 | 279,994 |

| 46 | 96,753 | 311,608 |

| 47 | 101,591 | 346,212 |

| 48 | 106,670 | 384,068 |

| 49 | 112,004 | 425,460 |

| 50 | 117,604 | 470,697 |

| 51 | 123,484 | 520,113 |

| 52 | 129,658 | 574,070 |

| 53 | 136,141 | 632,961 |

| 54 | 142,948 | 697,212 |

| 55 | 150,096 | 767,284 |

| 56 | 157,600 | 843,676 |

| 57 | 165,480 | 926,930 |

| 58 | 173,754 | 1,017,632 |

| 59 | 182,442 | 1,116,418 |

| 60 | 191,564 | 1,223,976 |

| 61 | 201,143 | 1,341,050 |

| 62 | 211,200 | 1,468,448 |

| 63 | 221,760 | 1,607,044 |

| 64 | 232,848 | 1,757,784 |

| 65 | 244,490 | 1,921,692 |

| 66 | 256,715 | 2,099,876 |

| 67 | 269,550 | 2,293,538 |

You can be a multi-millionaire ($2.3 million rich) when you retire if you just consistently save 10% annually and invest in a diversified portfolio that’s assumed to achieve an average annual return of 8%, a very reasonable assumption!

On the other hand, if you save 15% annually, your investment balance by age 67 would be 3,440,315, a 50% increase!

Now, if you use somewhat sophisticated Social Security Income (SSI) calculation formula (see the following explanation), we can estimate that by the time you retire at age 67, your annual SSI would be about $28k.

Social security calculation:

To calculate your Social Security income, we calculate your average indexed monthly earnings (AIME) which is based on your highest 35 years of earnings, adjusted for inflation. Once we have your AIME, we can calculate your primary insurance amount (PIA), which is the amount you would receive if you start claiming benefits at your full retirement age (FRA).

Assuming you work continuously until your full retirement age (FRA) of 67 and earn a 5% annual raise, your AIME would be approximately $73,554.

To calculate your PIA, we use a formula that takes into account your AIME and factors in adjustments for the year you turn 62 (the earliest you can claim benefits), the year you reach full retirement age, and the cost of living adjustments (COLA) in subsequent years.

Based on this formula, your estimated Social Security income would be approximately $2,362 per month, or $28,344 per year, in today’s dollars. Please note that this is just an estimate, and your actual Social Security income may vary based on your actual earnings history and other factors.

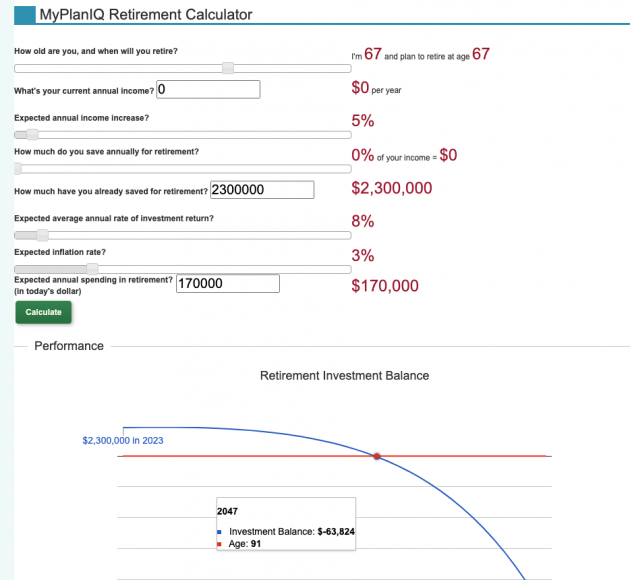

Another rule of thumb is that once you retire, you can expect to spend up to 70%-80% of your annual income to maintain a similar quality of life. This ratio is usually called retirement income replacement ratio. You can read here for a more detailed discussion on this topic.

If you expect to spend 75% of your annual income in retirement, in this case, you would expect to spend about $200k annually. Since you already have about $28k SSI, you will spend about $170k at the first year of your retirement. The following picture shows that you are likely deplete your account by age 91:

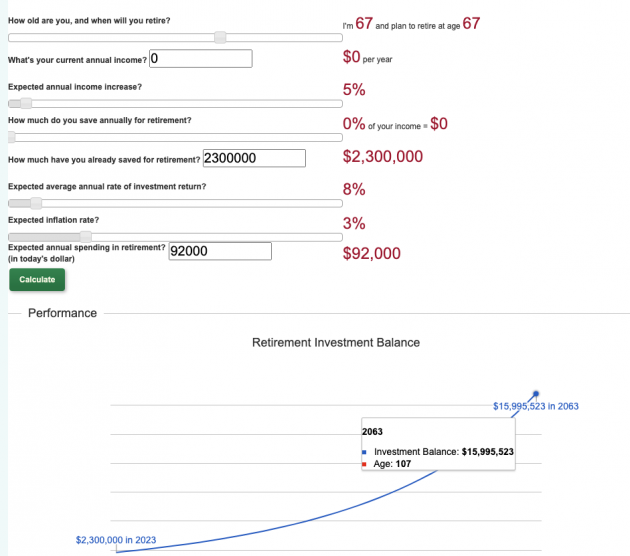

That’s still not quite satisfactory. On the other hand, if we use 4% withdrawal rule, you would expect about 2,300,000*4%=$92k per year withdrawal from your investments, or adding $28k SSI, you can expect $120k annual spending, which is about 50% of your last year’s income before you retire.

Note if you save 15% annually, 4% of your last investment balance $3,400,000 would be $138K, adding $28k SSI, you’ll get to spend $166K or very close to $170K or 75% of your pre-retirement annual income!

The nice thing here is that, by reducing your spending to be about 50% of your last year’s income before your retirement or 4% of your nest egg, you can preserve or even grow your estate even when you are over 100 year old!

Conclusions

There are various factors to consider when determining how much to save for a comfortable retirement. The above exercise provides a basic understanding that consistent saving of 10% or even better, 15%, as suggested by many financial advisors, along with investment in a diversified portfolio, can lead to a financially secure retirement.

Some factors that can significantly impact retirement savings include:

- Savings Rate: Saving at a rate of 10% versus 15% can make a big difference. A 15% savings rate is likely to enable retirees to maintain their pre-retirement quality of life. Therefore, the more savings, the better.

- If you save less but still aim to sustain your pre-retirement quality of life, it may be achievable in your lifetime. However, this may not leave much to your children or relatives.

- If you are willing to moderately reduce your expenses, you may be able to find a middle ground, which is the case for most people.