MyPlanIQ Fixed Income Strategy: White Paper

Overview of the Strategy

MyPlanIQ fixed income investment strategy is built on the observation that bond funds, especially total return bond funds, often exhibit strong price return momentum. Total return bond funds are the intermediate bond funds that have flexibility (with constraints, of course) to invest various bond segments (ranging from Treasury bonds to some high yield or low grade bonds to some international bonds). Some of these funds are also called multi-sector bond funds or strategic income funds.

Unlike stock investments, research and past investment records have shown that actively managed bond funds are more likely to outperform passive index bond funds. We can further limit ourselves to a list of candidate bond funds that have had excellent long term track records and are managed by reputable managers, among other criteria.

Read More

A tactical approach that utilizes momentum, coupled with changing economic conditions, financial market conditions as well as credit and interest rate risk could improve returns while reducing risk.

Similar to MyPlanIQ tactical asset allocation strategy (see TAA white paper), the fixed income strategy also utilizes the composite allocation indicator. It integrates a broad set of macroeconomic and market signals—employment trends, inflation, retail data, bond market price movements, and credit spreads. All of these are processed into a single output that classifies the environment as either risk-on or risk-off. When conditions are favorable, the strategy invests in the highest momentum total return bond fund that’s selected from a subset of candidate funds (see below). When risk-off is signaled , the strategy rotates into a more defensive bond fund or even a money market fund or cash.

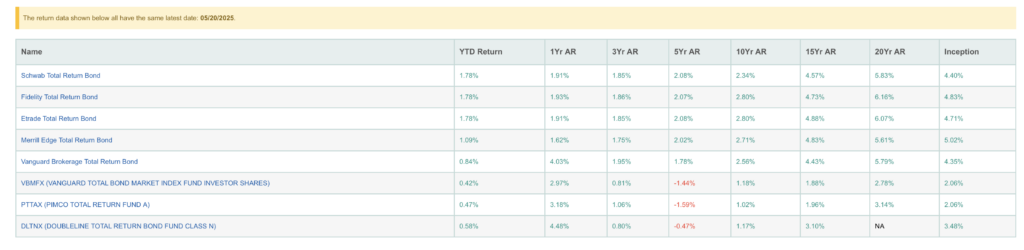

On top of that, we apply a relative momentum model to select from a curated list of flexible bond funds. These are total return funds that can allocate across the full fixed income universe—high yield, investment grade, emerging markets, mortgage-backed, Treasurys. These candidate funds have to pass some strict criteria one of which is that they are managed by excellent managers who have at least won an award like Morningstar Fixed Income Manager of The Year. These funds include those from PIMCO, DoubleLine, TCW, Loomis Sayles, and others with strong long-term records. The model scores the funds by short- and intermediate-term performance trends, volatility-adjusted, and typically selects the top one fund at any given time. The rebalance frequency is monthly.

Performance and Implementation

Over the last 15 years, this strategy has produced an annual excess return of 2% to 3% above general bond index funds such as the Vanguard Total Bond Market Index Fund. The excess return varies year by year, but the long-term trend is consistent—and achieved without leverage, complexity, or frequent trading.

Furthermore, the excessive returns are achieved with lower risk or lower maximum drawdown.

See Income Investors page for more information on our model portfolios.

Importantly, the implementation is straightforward. These are model portfolios built using only no-load, no-transaction-fee funds available through major brokerage platforms—Fidelity, Schwab, Vanguard, Merrill Edge, and E-Trade. Each platform’s version is tailored to the available fund lineup, so there’s no need for substitutes or forced choices.

For investors who are not on these platforms, or who prefer ETFs, we also maintain ETF-based versions of the model. These are designed for broader compatibility and can be used in virtually any brokerage account. They may be especially useful in managed accounts, third-party custodians, or advisory platforms with fund limitations.

Across both fund-based and ETF-based portfolios, turnover remains low. In many cases, there are only two or three rebalances updates per year. Some years may require no action at all.

Our long held research and monitoring results have also indicated similar strategies could be applied to many segments of fixed income investments including high yield bonds, ultra short term bonds and municipal bonds, and types of investments (such as closed end funds)

Intended Investors and Use Cases

This strategy is designed for income-focused investors, retirees, or those managing the fixed income portion of a diversified portfolio. It is also appropriate for institutional settings or advisor-managed accounts where reliable fixed income exposure with some adaptive flexibility is preferred.

The strategy is not about forecasting interest rates or making bold directional bets. Nor is it designed to take equity-like risk in pursuit of returns. Instead, it focuses on improving fixed income performance through a disciplined tactical process, grounded in both intuition and evidence.

We believe this type of framework is essential in a market where traditional bond indexes may lag behind inflation or expose investors to uncompensated risks—especially during periods of rate volatility or credit disruption.