Employee Stock Purchase Plans (ESPPs) are a valuable benefit offered by many companies, allowing employees to purchase company stock at a discounted price. Understanding how ESPPs work, their advantages, and the associated tax implications can help employees make informed financial decisions. This article covers the key concepts of ESPPs and explains tax treatment with examples.

What is an ESPP?

An Employee Stock Purchase Plan (ESPP) is a program that allows employees to buy company stock at a discount, often up to 15% off the market price. These plans typically have specific enrollment periods, offering periods, and purchase dates, making it essential for employees to understand how the plan works.

There are two main types of ESPPs:

- Qualified ESPPs (Section 423 plans) – Receive favorable tax treatment if specific holding requirements are met.

- Non-Qualified ESPPs – Do not receive special tax advantages and are taxed as ordinary income.

Now, let’s explore the fundamental ESPP concepts.

Key ESPP Concepts

1. Offering Period

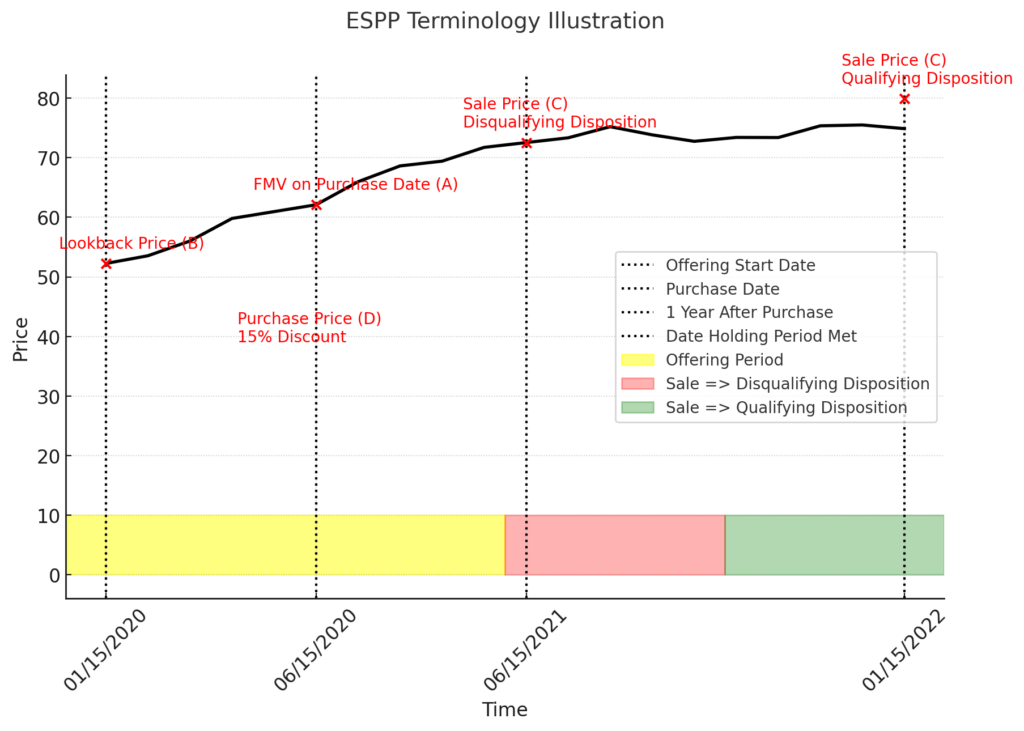

The offering period is the time frame during which employees can purchase company shares through ESPP. It typically lasts between 6 to 24 months and may include multiple purchase dates within it.

2. Enrollment Period and Start Date

The enrollment period is the designated window when employees sign up for the ESPP. Once enrolled, payroll deductions begin, accumulating funds to purchase stock on the purchase date.

3. Payroll Deduction Process

During the offering period, employees contribute a fixed percentage of their compensation (not just salary), often up to 10-15%, as determined by company policy. However, the IRS imposes an absolute cap of $25,000 per year on the fair market value of purchased shares, meaning that if 15% of an employee’s compensation exceeds this limit, only $25,000 worth of shares can be purchased, and any excess contributions are typically refunded., as per IRS or DOL requirements limiting contributions to a maximum of 15% of total compensation through automatic payroll deductions. These deductions are withheld after taxes (post-tax earnings) and accumulated in an account until the purchase date, when they are used to buy shares at the discounted price.

4. Purchase Price

On the purchase date, accumulated payroll contributions are used to buy company stock at a discount. The purchase price is determined by applying the ESPP discount (e.g., 15%) to the lower of:

- The stock price at the beginning of the offering period.

- The stock price on the purchase date.

5. Discount Price (Main Advantage #1)

One of the primary benefits of an ESPP is the discount price. Many plans allow employees to buy stock at 85% of the market price, instantly providing a 15% gain if the stock is sold immediately (subject to tax implications).

For example:

- If the stock price on the purchase date is $100 and the ESPP offers a 15% discount, the employee purchases the stock for $85.

- If they sell immediately, they lock in a $15 per share profit (before taxes).

6. Lookback Price (Main Advantage #2)

The lookback feature is another significant advantage. It allows employees to purchase stock at a discount based on the lower of:

- The stock price at the offering period start date.

- The stock price on the purchase date.

For example:

- If the stock price was $80 at the start of the offering period and $100 on the purchase date, the purchase price with a 15% discount would be $68 (85% of $80 instead of $100).

- This results in a higher profit margin if the employee sells the stock.

7. Qualified vs. Non-Qualified ESPPs

- Qualified ESPPs (Section 423) offer favorable tax treatment but require employees to hold the stock for at least 2 years from the offering date and 1 year from the purchase date to receive long-term capital gains treatment.

- Non-Qualified ESPPs do not have special tax benefits. The discount is taxed as ordinary income in the year of purchase.

The following illustrates the basic concepts in ESPP:

ESPP Tax Calculation Examples

1. Disqualifying Disposition (Selling Before Holding Period Ends)

- Example: An employee purchases stock at $85 with a 15% discount (lookback price applied). The stock price on the purchase date is $100, and they sell immediately at $110.

- Tax Treatment:

- The discount ($15 per share: $100 – $85) is taxed as ordinary income.

- The capital gain ($10 per share: $110 – $100) is taxed as short-term capital gains (same as ordinary income rates).

2. Qualifying Disposition (Holding Long Enough for Tax Benefits)

- Example: The same employee holds the stock for more than 2 years from the offering date and 1 year from the purchase date before selling at $120.

- Tax Treatment:

- The discount ($15 per share: $100 – $85) is taxed as ordinary income.

- The capital gain ($20 per share: $120 – $100) is taxed as long-term capital gains (lower tax rate than ordinary income).

3. Tax Withholding by Employer

For qualified ESPPs, employers do not withhold taxes at purchase. Employees are responsible for reporting and paying taxes when they sell the shares. However, for non-qualified ESPPs, the employer may withhold ordinary income tax on the discount portion immediately.

Nuances

1. Payroll Deduction Timing

- Payroll deductions occur at each pay period, rather than as a lump sum payment at the purchase date. This means employees are contributing continuously, which can be a slight disadvantage if they would prefer to invest the money elsewhere in the short term.

2. Immediate Sale Strategy

- If an employee can afford to purchase the stock, at a minimum, they can sell immediately after purchase to lock in guaranteed profits due to the discount and lookback feature.

- However, some employers may have a minimum holding period before employees can sell, so it’s crucial to check the company’s ESPP rules.

Should You Participate in an ESPP? Should You Sell and When?

Should You Participate?

- If your company offers a 15% discount and a lookback feature, ESPPs can be an excellent investment opportunity.

- If your financial situation allows you to contribute without impacting essential expenses, participating is usually beneficial.

Should You Sell Immediately or Hold?

- If you sell immediately, you lock in a guaranteed gain (subject to taxes), which minimizes risk.

- If you hold, you may benefit from long-term capital gains tax treatment but take on stock market risk.

- If your company stock is highly volatile, selling soon after purchase might be safer.

When Should You Sell?

- If you need short-term liquidity, selling immediately is a low-risk option.

- If you believe in your company’s long-term growth, holding can be advantageous.

- If you are concerned about concentration risk (too much of your portfolio in company stock), it may be better to sell and diversify.

Final Thoughts

An ESPP is a good workplace benefit, especially if it includes a 15% discount and a lookback feature. Understanding what it entails and taking advantage of its benefits can provide valuable additional compensation, sometimes substantial if the company’s stock value appreciates significantly over time. However, it is crucial to understand the tax implications and risks before deciding whether to participate or when to sell. By strategically managing ESPP participation and stock sales, employees can maximize their benefits while minimizing tax liabilities.