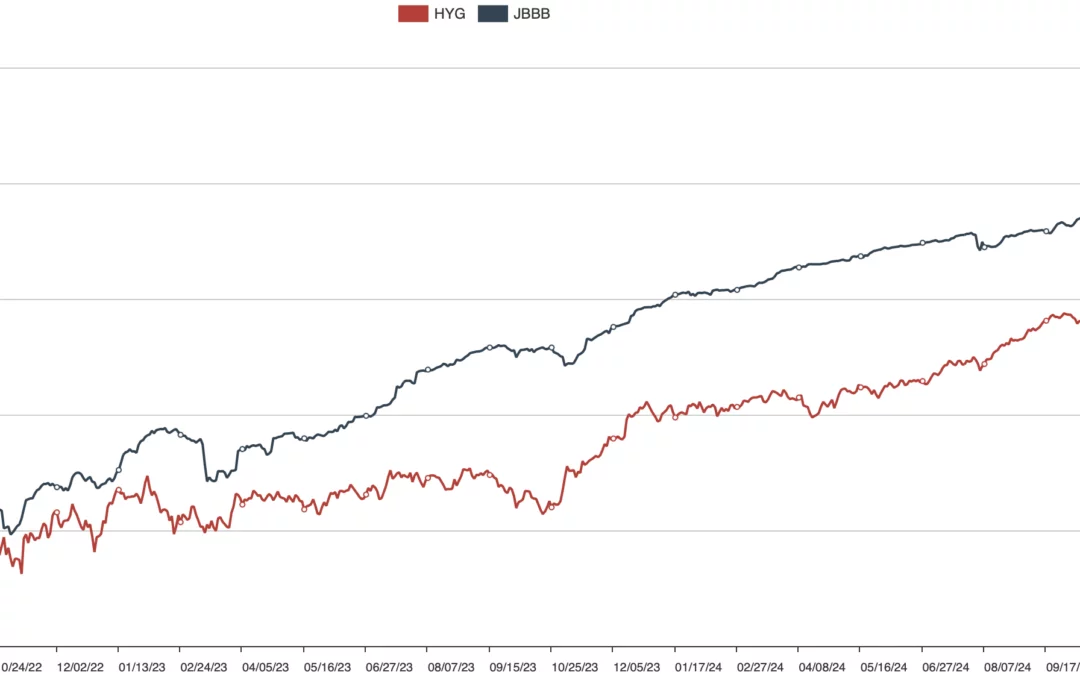

Most investors think about returns first. But what gets less attention, and probably deserves more, is volatility. Risk adjusted returns matter more. Being comfortable with portfoiio swings is the key to investment success.

Latest in Retirement Savings & Personal Finance: Review and Get Rid of Your Unused Subscriptions, Private Equity & Crypto Investments in Your Retirement Accounts, Germany’s Early Start Pension

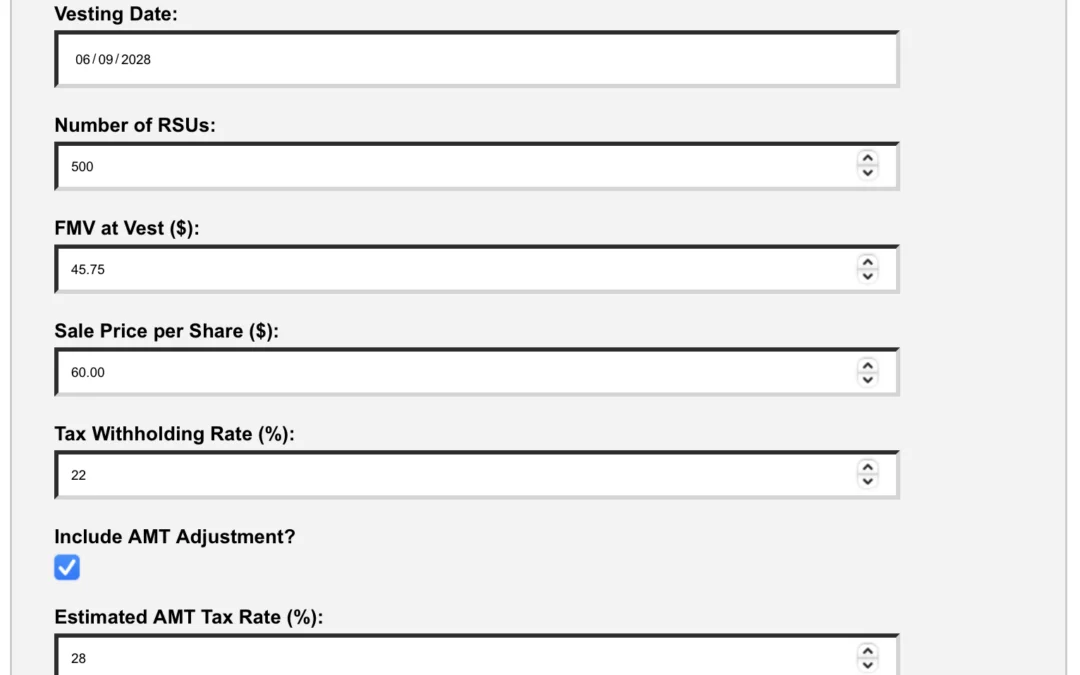

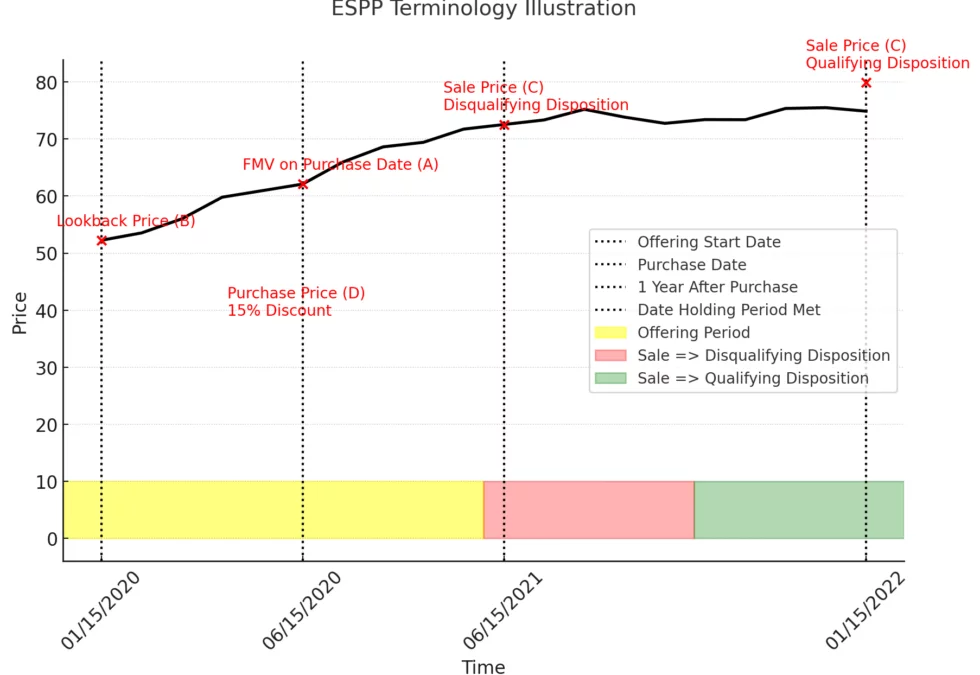

Stock Compensation 101: How People Build Wealth (or Blow It)

2024 Retirement Plan Contribution Limits 1. 401(k), 403(b), and 457(b) Plans Employee Contributions: Up to $23,000 (under age 50) Catch-up contribution: $7,500 (ages 50+) Total Combined Limit (Employee + Employer): $69,000 Roth Options: Available for 401(k), sometimes...

Multiple research results now point to what seems like a consistent pattern: active bond funds tend to outperform their passive peers more often than stock funds do.

Cadence Design Systems 401(k) Plan includes mainly ultra low-cost target date and index funds. We show these are good enough for its participants, experienced or novice.