Is an ETF Portfolio a Better Vehicle than a 529 Plan for College?

11/02/2010 0 comments

Sending kids to college is increasingly expensive but higher education is essential for the continued strength of our society. Enabling new graduates to have the minimum debt as the emerge into the workforce is a major achievement.

A recent post in the Portfolioist outlined the challenges and the 529 alternatives.

With an increasing number of low cost and effective ETFs, people saving for college may look with yearning at the grass (which is indeed greener) on the other side of the fence.

In this article, we compare the best 529 plan with the best ETF plan to examine whether the tax benefits offset the limitations of the plan. Put another way, if we invest normally in a high performance ETF portfolio, can the additional returns make up for the additional tax burden.

Contributions to 529 plans are made with after-tax dollars and any earnings grow tax-free at the federal level. Earnings withdrawn from 529 plans to pay for qualified higher education expenses are free from federal income tax for state-sponsored programs and programs of any eligible higher education institution.

Contributions to a taxable account are made with after-tax dollars and earnings are taxed. There is then no restriction on what that money may be used for.

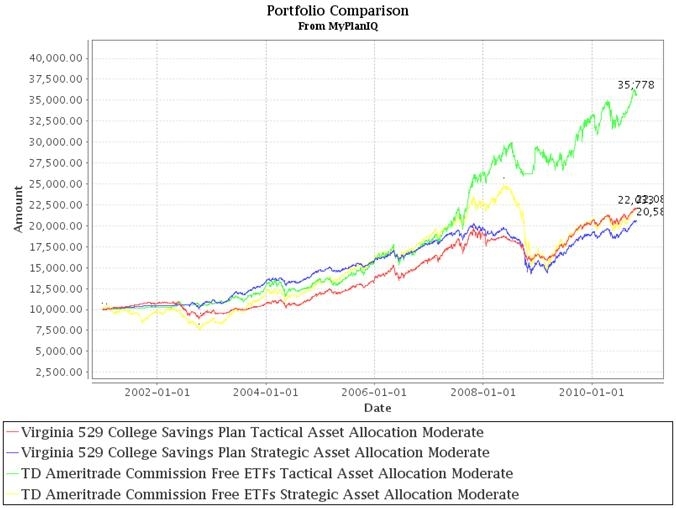

According to MyPlanIQ back testing, the 529 plan with the best returns performance is Virginia and the highest performance ETF portfolio is provided by TD Ameritrade. The chart and table below gives a comparison of the two plans.

click to enlarge images

Performance table (as of Oct 29, 2010):

|

Portfolio Name |

1Yr AR |

1Yr Sharpe |

3Yr AR |

3Yr Sharpe |

5Yr AR |

5Yr Sharpe |

|

Virginia 529 College Savings Plan Tactical Asset Allocation Moderate |

11% |

154% |

4% |

40% |

12% |

110% |

|

Virginia 529 College Savings Plan Strategic Asset Allocation Moderate |

11% |

153% |

1% |

1% |

6% |

54% |

|

TD Ameritrade Commission Free ETFs Tactical Asset Allocation Moderate |

15% |

108% |

11% |

75% |

20% |

127% |

|

TD Ameritrade Commission Free ETFs Strategic Asset Allocation Moderate |

11% |

101% |

-2% |

-14% |

8% |

43% |

Note that tax on gains are not taken into account at this point and intuitively it is clear that the strategic asset allocation strategy does not provide enough difference between the returns to make sense and so, to move to a taxable account, the tactical asset allocation strategy is going to be selected.

Also note that currently 529 plans allow rebalancing only once a year and so extra care must be taken for any sort of momentum or styles rotation approach. Essentially, 529 forces a lazy portfolio approach.

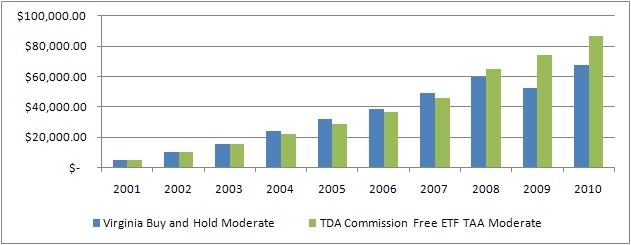

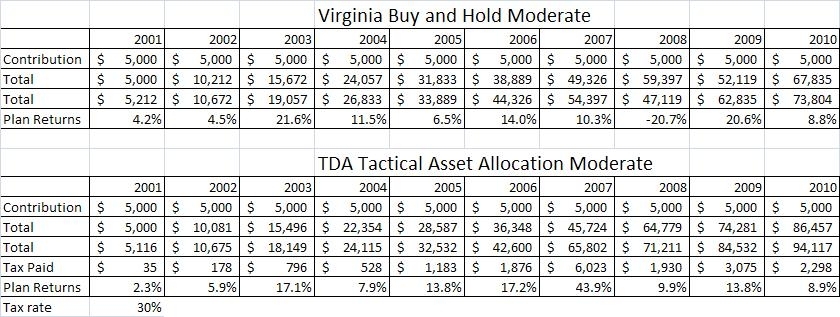

To be able to make a comparison, made the following assumptions

- $5000 was invested every year

- The return for the year was applied in one shot

- The ETF portfolio was taxed at 30%

From this we see that, in fact, the ETF portfolio outperforms that 529 plan even taxing the growth in the portfolio. In addition, the taxable portfolio has no restrictions and is completely liquid.

On the other hand, this is one of the best performing ETF portfolios and requires monthly action to achieve the returns. If you select a lower performance portfolio or don't want to be active every month, the results will be much closer.

The key takeaway is to carefully examine your choices when considering a college savings plan.

labels:investment,

comments 0

Or Start FREE 30-day trial now >>