Re-balance Cycle Reminder All MyPlanIQ’s newsletters are archived here.

Regular AAC (Asset Allocation Composite), SAA and TAA portfolios are always rebalanced on the first trading day of a month. the next re-balance will be on Tuesday December 1, 2020.

Please note: As of March 1, 2020, we officially phased out our old rebalance calendar for both SAA and TAA. They are now always rebalanced on the first trading day of a month.

As a reminder to expert users: advanced portfolios are still re-balanced based on their original re-balance schedules and they are not the same as those used in Strategic and Tactical Asset Allocation (SAA and TAA) portfolios of a plan.

Polls Are Useless vs. This Investment Strategy Doesn’t Work!

By the time you are reading this newsletter, it’s probably a nail biting time (less than 24 hours to go) to wait for the US president election result. The voter turnout of this election might be the highest presidential-year turnout since 1908. To make the matter more serious, it’s hotly debated and highly polarized.

What’s interesting is that we can see/learn something from election polling and apply this to investing in financial markets.

Polls are useless! Are they really?

Many people are dismissing election polls and think they are useless. This is because most polls faltered in the 2016 presidential election: they were predicting Hillary Clinton’s victory all along leading to the election night and then people were shocked to see Donald Trump won the election.

Of course, some pollsters were quick to point out that they were actually not that far off in 2016: in fact, Clinton did win the popular vote in 2016. So technically, the polls were not completely wrong at that time.

Now that we are on the eve of another election night, will we see the same thing happen again as at the moment, many polls are again forecasting the Democratic candidate Joe Biden will win the election? For example, the popular FiveThirtyEight.com tracks and synthesizes all major polls. Based on their statistical simulation, at the moment, it has the following forecast:

Before you quickly celebrate or dismiss the forecast, you are reminded that this newsletter does not intend to endorse or predict the election result. What we would like to do is to objectively understand and analyze this a bit deeper as how we approach to this type of forecast or methodology is very relevant/similar to what we do in investing.

What the above figures say is that among 40 thousand simulations, it observes 89 out 100 times when Biden wins while Trump wins 10 in 100 times( the other 1 left is hung or tie election). Put it another way, the likelihood or probability for Biden to win is about 89% and for Trump, it’s about 10%.

If asked to interpret the above prediction, virtually everyone (even Biden’s supporters) would agree that Trump still has a chance to win. In fact, 538 does put out an article right now as I’m Here To Remind You That Trump Can Still Win.

But come tomorrow or after the election, if Trump indeed wins, people will again quickly dismiss these polls and say they are useless.

This reveals a popular human tendency: though we accept statistical probability at its face value (in 2016, 538 predicted Trump had 28.6% chance to win), when an event with low odd does happen, people will forget about statistics and just dismiss the whole process.

But having a low probability, even at 1% or less, does mean such an event indeed can happen. Technically what the Trump’s 28.6% winning probability, for example, of the 538’s prediction for the 2016 election means is that Trump will win on average 28.6 number of times if the election is held in the ‘exact’ same setting for 100 times . Or to be more rigorous, Trump will win on average 286 times out of 1000 ‘elections’ or the same ratio when more ‘elections’ or samples are carried out.

So a single actual occurrence of Trump’s win in 2016 does not really invalidate the polls. However, it certainly doesn’t give strong support to the polls either. The difficulty for many people to comprehend lies in that we can’t afford to repetitively ‘test’ out this prediction in real world: for example, how in the world can we repeat the election in the same exact settings for 1000 times?

This problem is further exacerbated as it comes with some real substantial political, social and economical impacts. People tend to get very emotional when the results are more materially relevant to their own well-being.

On the other hand, there are indeed some problems (some of them might be serious) in the methodology of a poll. For example, the bias of samples, the ‘shy’ Trump supporters etc. So, it’s actually more important to first vet and validate the methodology of a polling analytically, instead of simply waiting for ‘real time’ results.

The above discussion by no means supports either candidate or even the polls (as indeed, there are quite some methodological deficiencies in most polling methods). What we want to point out is that the process of understanding whether a method works or not is also applicable to financial investing.

Investment strategies and mistakes

Long time readers might have sensed where we are leading to on investment strategies: over time, we have published many newsletters to touch on the topic of investment mistakes vs. temporary losses or miscalls:

- August 7, 2017: I Didn’t Learn Anything — Mistake vs. Temporary Underperformance

- October 17, 2016: Investment Mistakes And Good Or Bad Investment Strategies

- October 27, 2014: Investment Loss, Mistakes And Market Cycles

- July 23, 2012: The Difference Between Investment Loss & Investment Mistakes

We strongly suggest readers who are interested in this important subject to read the above newsletters.

Similar to election polls, investment strategies materially affect people’s well-being immediately (you can see your real time account balance statements these days). They are time related (so called time series): in investments, it requires a long time to observe large enough samples to get expected average results (returns). For example, we stated in August 7, 2017 newsletter:

- A strategic buy and hold strategy would require 15 to 20 years minimum to get a reasonable return

- A tactical asset allocation strategy like ours would require 10 to 15 years minimum to get a reasonable return

- A total return bond fixed income portfolio would require 2 years minimum to get a reasonable return (see July 24, 2017: Total Return Bond Fund Portfolios And Cash)

So people don’t have patience or just simply can’t afford to observe this in such a long time to validate or invalidate a strategy.

Similar to polling, we believe investors should not simply rely on real time results to validate a strategy (in fact, just like what’s discussed above, this is often not effective). What’s more important is to see whether an investment strategy has strong intuitive and fundamental backings such as long term stock or equity risk premium or inherent price momentum. These should always serve as the first line of filtration to weed out bad strategies that are often produced by data snooping or other statistic fluke (purely by luck). Only after that, one should look at historical back testing/simulation results to confirm/invalidate it.

After carefully vetting and selecting a strategy, the next step is to commit to it for a long enough of time: the reason is that for any strategy to converge/produce an expected or its average outcome (such as average annual returns), it just simply requires large enough of samples. During this period, one has to rigorously stick to the strategy and implement it as it is.

The second step is the one that can really challenge investors: when a strategy (or a portfolio) loses a good amount of money or underperform a market index at a time, is it simply just an inherent part of the samples or it signals its ‘real’ failure. This again leads us back to the first step: understanding thoroughly on the behavior of a strategy, even before you are committed to it is extremely important to help you navigate through real time turbulence. For example, buying and holding a stock index fund such as SPY can result in large drawdown as big as one half to two third at some point. On the other hand, buying and holding such a stock market aggregate will most likely make money in a long enough (at least 20 years or even longer) period. With this understanding, investors should be able to ride out some violent bear markets.

To summarize, we shouldn’t be too quick to dismiss or accept an investment strategy, just like an election poll. One should first thoroughly understand its methodology and behavior (and possible extreme outcomes) and then just let large enough real time samples play out in real life to gain its positive average outcome.

Market overview

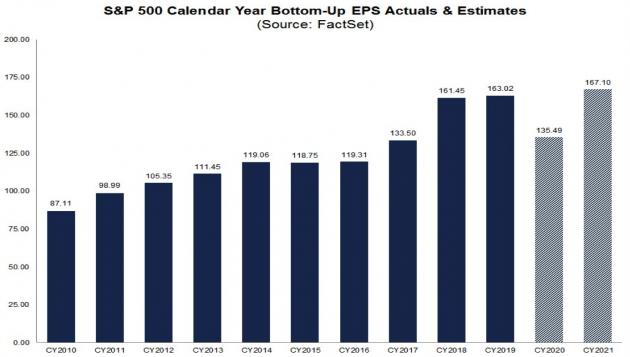

It’s everyone’s guess how the short term market reaction will be for the US election. However, we are clear on some noticeable conditions including extremely high stock valuation and the rising pandemic wave. On the other hand, it’s somewhat encouraging to see that S&P 500 dramatically outperformed the beaten down analysts’ earnings expectation for Q3 2020. For SP 500 companies, based on Factset:

- 86% of S&P 500 companies have reported a positive EPS surprise and 81% have reported a positive revenue surprise. This is the highest positive earnings surprise since 2008.

- The blended earnings decline is -9.8%, much better than -21.1% expected on September 30.

In a word, US companies have done way much better than what were expected. Looking ahead, S&P 500 companies EPS (Earnings Per Share) are:

So there won’t be much earnings growth in 2021 for S&P 500 ‘conglomerate’. The most stock price growth comes from price earnings (PE) multiple expansion.

Investors shouldn’t be complacent on the markets. As always, we should follow our strategies to navigate through this period:

- For strategic allocation (buy and hold) investors, ignore the current market behavior. Remember, as what we have emphasized numerous times, when you choose and commit to a strategic portfolio, you essentially know and commit that your investment horizon (or the time you need to utilize this capital) is 20 years or longer. As we pointed out, if your investments are those diversified (index) funds such as an S&P 500 index fund (VFINX, for example), you know your money is in some solid ‘business’ that eventually (20 years later) will deliver some reasonable returns. As long as you are comfortable with this thesis, you should sit tight and forget about the current gyration.

- For tactical investors, again, you have to ignore the current market noise. Furthermore, you should follow your strategy rigorously, especially in a time like this. Human emotion, both optimistic and pessimistic, and human desire, both greedy and fearful, are your worst enemies. This has been shown to be true time and time again.

Stock valuation now reached another high. For the moment, we believe it’s prudent to be cautious while riding on market uptrend. However how serious a correction might be, we have confidence in the US economy in the long term and thus in the stocks in aggregate. We just need to manage through interim losses carefully.

We again would like to emphasize that for any new investor and new money, the best way to step into this kind of markets is through dollar cost average (DCA), i.e. invest and/or follow a model portfolio in several phases (such as 2 or 3 months) instead of the whole sum at one shot.

Enjoy Newsletter

How can we improve this newsletter? Please take our survey

–Thanks to those who have already contributed — we appreciate it.

Latest Articles

- October 26, 2020: Recent Improvements

- October 19, 2020: REIT Indexes As Businesses

- October 12, 2020: Stock Indexes As Businesses

- October 12, 2020: Stock Indexes As Businesses

- October 5, 2020: Asset Trend Review

- September 28, 2020: Retirement Spending: Your Portfolio’s Volatility Matters

- September 21, 2020: Boring Utility Stocks Are Excellent Long Term Winners

- September 14, 2020: Surprised, Active Fixed Income Investors Have Done Better Than Stock Investors For The Last 20 Years!

- August 31, 2020: Investing In An Ultra-Low Return Environment

- August 24, 2020: Target Maturity Bond ETFs For Short Term Cash

- August 17, 2020: Newsletter Collection Update

- August 10, 2020: Fixed Income In A Speculative Era

- August 3, 2020: Sound Investment Strategies

- July 27, 2020: Total Return Bond Funds Update

- July 20, 2020: Divergence Between Value And Growth Stocks Everywhere

- July 13, 2020: Short Term Cash, Treasury Bills, CDs And Future Fixed Income

- July 6, 2020: Bond ETFs vs. Bond Mutual Funds

- June 29, 2020: Industry Sector ETF Rotation With Composite Momentum

- June 22, 2020: Industry Sector Rotation With Composite Momentum

- June 15, 2020: Advanced Minimum Equity Portfolios

- June 8, 2020: Recent Positive Developments

- June 1, 2020: Minimum Equity Portfolios

- May 18, 2020: Core Satellite Portfolios In The Current Pandemic

- May 11, 2020: Asset Trends Review

- May 4, 2020: The Real, Sensible And Wise Warren Buffett

- April 27, 2020: Total Return Bond Funds & Portfolios

- April 20, 2020: Multi-Factor ETFs and Rotation

- April 13, 2020: A Closer Look At 401(k) Investment Portfolios

- April 6, 2020: Long Term Stock Market Timing Since 1871 Revisited

- March 30, 2020: How Did Bond ETFs And Mutual Funds Fare In The Current Crisis?

- March 23, 2020: Chaos And Hope

- March 16, 2020: A Live Lesson

- March 9, 2020: Risk And Reward

- March 2, 2020: The Risk Of Coronavirus Outbreak

- February 24, 2020: Long Term Stock Valuation Based Investment Strategies

- February 10, 2020: Update On Short Term Cash, Treasury Bills and Brokered CDs

- February 3, 2020: Investment Landscape For Retirees And Would-be Retirees: Stocks

- January 27, 2020: Investment Landscape For Retirees And Would-be Retirees: Fixed Income

- January 13, 2020: Portfolio Performance: A Walk In The Past II

- January 6, 2020: Asset Outlook and Portfolio Strategies

- December 16, 2019: Q&As On Our Services

- December 9, 2019: Portfolio Constructions For Advanced Users

- December 2, 2019: Newsletter Collection Update

- November 25, 2019: Core ETFs or Core Mutual Funds Portfolios

- November 18, 2019: Introducing MyPlanIQ Asset Allocation Composite Strategy

- November 11, 2019: Market Indicator And Momentum

- November 4, 2019: Factor ETF Rotation

- October 28, 2019: Multi-factor ETFs vs. Equal Weight Multi-Factor Portfolios

- October 21, 2019: Multi-factor ETFs: Value And Momentum

- October 14, 2019: Low Volatility Factor ETFs

- October 7, 2019: Zero Commission Era Has Arrived, Is It Really That Good?

- September 30, 2019: Boosting Bond ETF Portfolio’s Return With Muni Bond ETFs

- September 23, 2019: Value ETFs

- September 16, 2019: Factor ETFs

- September 9, 2019: Momentum Factor Stock ETFs

- August 26, 2019: Employer 401k Match: Yet Another Free Lunch Not To Be Missed

- August 19, 2019: PIMCO Income Fund and Other Total Return Bond Funds Update

- August 12, 2019: Aggressive Fixed Income Portfolios?

- August 5, 2019: Long Term Investment Strategies And Short Term Market Noises

- July 29, 2019: Fixed Income Portfolios In A Lower Yield Environment

- July 22, 2019: Core Satellite Portfolios Balance Fluctuation

- July 15, 2019: Quality Stock Factor ETFs

- July 8, 2019: Surprise! Brokerages Make Most From Your Cash, Not Commissions

- July 1, 2019: Utilities Sector Review

- June 24, 2019: Asset Allocation Funds Review

- June 17, 2019: Latest Performance Comparison Among Several Advanced Strategies

- June 10, 2019: Money Market And Ultra Short Term Bond Funds

- June 3, 2019: What We Can Learn From The Seasonality Strategy

- May 20, 2019: Morningstar Portfolio Manager Awards

- May 13, 2019: Total Return Bond ETFs Review

- May 6, 2019: Global Allocation Revisited

- April 29, 2019: Asset Trend Review

- April 22, 2019: The Current State Of Fixed Income

- April 15, 2019: The Importance Of Fixed Income Returns For Retirement Spending

- April 8, 2019: Newsletter Collection Update

- April 1, 2019: S&P 500 As A Business

- March 25, 2019: Health Care Sector Review

- March 18, 2019: The Risk Of Stock Investing

- March 11, 2019: Consumer Staples Sector Review

- March 4, 2019: Global Stock Valuation Update

- February 25, 2019: ‘Bad’ Tactical Strategy

- February 11, 2019: “Best” Balanced Fund And Portfolios Revisited

- February 4, 2019: Cash And Money Market Funds: Interests And Safety

- January 28, 2019: Fixed Income Review

- January 14, 2019: Tactical Asset Allocation Portfolio Review

- January 7, 2019: Global Strategic Asset Allocation Portfolio Review

- December 17, 2018: Robinhood’s ‘Revolution’ Or Gimmick

- December 10, 2018: How Defensive Are REITs?

- December 3, 2018: Conservative Core Satellite Portfolio

- November 26, 2018: Allocation Mutual Fund Review

- November 19, 2018: Is The Recent Downtrend Sustainable?

- November 12, 2018: The Staggering Low Interest Rates From Big Banks

- November 5, 2018: The ‘Right’ Or ‘Wrong’ Decision

- October 29, 2018: Taxable Total Return Bond Plus Muni Bond Fund Based Portfolios

- October 22, 2018: DoubleLine Shiller CAPE 10 Based Fund Review

- October 15, 2018: Newsletter Collection Update

- October 8, 2018: Asset Trend Review

- October 1, 2018: Taxable vs. Tax Exempt High Yield Bonds

- September 24, 2018: High Yield Bonds In A Rising Rate Environment

- September 10, 2018: Value, Growth And Blend Stock Style Investing

- August 27, 2018: Money Market ETFs?

- August 20, 2018: How Momentum Investing Stacks Up?

- August 13, 2018: Total Return Bond ETF

- August 6, 2018: Fidelity Zero-Fee Index Funds

- July 30, 2018: Tax Efficient Portfolios

- July 23, 2018: Municipal Bond Funds And Portfolios

- July 16, 2018: A Guide To Conservative Portfolios

- July 9, 2018: Conservative Allocation Mutual Funds Based Portfolios

- July 2, 2018: Small Cap Stocks For The Long Term

- June 25, 2018: What Can We Learn From GE’s Removal From Dow Jones Index?

- June 18, 2018: The ‘Best’ Balanced Portfolio Continues To Excel

- June 11, 2018: Is 10 Year Long Enough For Portfolio Comparison?

- June 4, 2018: Action Plan: Risk Review For Investments

- May 21, 2018: Rising Rates, Consumer Staples And Stock Index

- May 14, 2018: Newsletter Collection Update

- May 7, 2018: Money Market Fund Taxonomy

- April 30, 2018: Momentum Investing Review

- April 23, 2018: Commodities In Current Environment

- April 16, 2018: Municipal Bonds As A Fixed Income Asset Class

- April 9, 2018: Exponential Or Compounding Nature In Investing

- April 2, 2018: Inside Of The Stock Chaos

- March 26, 2018: Total Return Bond Update

- March 19, 2018: Treasury Bills vs. Brokered CDs

- March 12, 2018: Defensive Conservative Portfolio Review

- March 5, 2018: Warren Buffett’s Advices

- February 26, 2018: Pros And Cons of Strategic And Tactical Portfolios In 2018

- February 12, 2018: Trend Review

- February 5, 2018: Market Selloff And Long Term Investing

- January 29, 2018: The New Addition To Our Total Return Bond Fund Candidates

- January 22, 2018: Where Are Bonds Heading?

- January 15, 2018: Tactical Portfolios Review

- January 8, 2018: Strategic Portfolios Review

- December 18, 2017: Record Highs And Risk

- December 11, 2017: Cash Return And Interest Rate Update

- December 4, 2017: Mutual Fund Star Ratings: Are They Useful?

- November 20, 2017: Thankful And Mindful

- November 13, 2017: Is This A Good Time For Retirees Or Would Be Retirees?

- November 6, 2017: Newsletter Collection Update

- October 30, 2017: Rising Interest Rates

- October 23, 2017: A Primer For Portfolios

- October 16, 2017: REITs As An Asset Class

- October 9, 2017: Conservative Portfolios Revisited

- October 2, 2017: The Role of Short Term Bond Funds

- September 25, 2017: Fees In Cash Investments

- September 18, 2017: Conservative Portfolios Review

- September 11, 2017: International Diversification Effect

- September 4, 2017: Invest And Speculate Revisited

- August 28, 2017: Total Return Bond Fund Portfolios: Where Do They Fit?

- August 21, 2017: Portfolio Performance: A Walk In The Past

- August 14, 2017: Fidelity Commission Free ETFs Update

- August 7, 2017: I Didn’t Learn Anything — Mistake vs. Temporary Underperformance

- July 31, 2017: Asset Classes And Fund Choices: A Primer

- July 24, 2017: Total Return Bond Fund Portfolios And Cash

- July 17, 2017: Long Term Stock Holding Periods For Retirement

- July 10, 2017: Half Year Asset Trend Review

- June 26, 2017: How To Beat The Best Balanced Allocation Fund

- June 19, 2017: Newsletter Collection Update

- June 12, 2017: A Mixed Bag Performance of Momentum Investing

- June 5, 2017: How To Start A New Portfolio

- May 29, 2017: Alternative Assets And Their Role In Portfolios

- May 22, 2017: Summer Seasonality And Portfolio Management

- May 15, 2017: Cash: Banking Or Investing?

- May 8, 2017: Holding Period of Long Term Timing Portfolios

- May 1, 2017: Debate on Risk vs. Volatility

- April 24, 2017: The Long Term Stock Market Timing Return Since 1871

- April 17, 2017: Risk vs. Volatility: Long Term Stock Market Returns

- April 10, 2017: Total Return Bond ETFs And Portfolios

- April 3, 2017: Quarter End Asset Trend Review

- March 27, 2017: Practical Consideration For IRAs And 401k Accounts

- March 20, 2017: Fund Fees: That’s (Still) Outrageous

- March 13, 2017: Long Term Stock Valuation Review

- March 6, 2017: Asset Classes for Retirement Investments

- February 27, 2017: Fidelity Total Bond Fund Review

- February 20, 2017: Long Term Stock Timing Based Portfolios And Their Roles

- February 13, 2017: Alternative Investment Portfolios Review

- February 6, 2017: Tax Free Municipal Bond Investments Review

- January 30, 2017: Brokerage Specific Conservative Portfolios

- January 23, 2017: Fixed Income Portfolio Review

- January 16, 2017: Long Term Trend Following Portfolio Review

- January 9, 2017: Tactical Asset Allocation Review

- January 3, 2017: Strategic Asset Allocation Review

- December 12, 2016: Enhanced Index Funds

- December 5, 2016: Review Of Broad Base Core Mutual Funds For Brokerages

- November 28, 2016: Core Index ETFs Review

- November 21, 2016: International Exposure Of U.S. Large Companies

- November 14, 2016: Asset Trends After The Election

- November 7, 2016: Rising Rate And Current Bond Trend

- October 31, 2016: Economy Power And Long Term Stock Returns

- October 24, 2016: Current Commodity Trend And Managed Futures

- October 17, 2016: Investment Mistakes And Good Or Bad Investment Strategies

- October 10, 2016: Momentum Investing Review

- October 3, 2016: Survey & Feedback

- September 26, 2016: Fixed Income Investing: Actively Managed Funds vs. Index Funds

- September 19, 2016: Stock Investing: Actively Managed Funds vs. Index Funds

- September 12, 2016: Newsletter Update

- September 5, 2016: Overvalued Markets And Long Term Timing Strategies

- August 29, 2016: Your 401K Finally Draws Attention

- August 22, 2016: Inflation Protected Securities TIPS For Current Overvalued Markets

- August 15, 2016: Risk On: Emerging Market Stocks And Small Cap Stocks

- August 8, 2016: Portfolio Construction Using Stock ETFs And Bond Mutual Funds

- August 1, 2016: Adding Value To Your Own Investments

- July 25, 2016: Tactical Asset Allocation Funds Review

- July 18, 2016: Strategic Asset Allocation & Lazy Portfolio Review

- July 11, 2016: Asset Trend Review

- June 27, 2016: Secular Cycles For Tactical And Strategic Investment Strategies

- June 20, 2016: A World of Debt

- June 13, 2016: Managed Futures For Portfolio Building

- June 6, 2016: Newsletter Summary

- May 30, 2016: Swensen Portfolio And Permanent Portfolios

- May 23, 2016: AAII Article And Some Web Changes

- May 16, 2016: The PIMCO (Dis)Advantages

- May 9, 2016: Boost Your Dull Summer Investments

- May 2, 2016: Low Cost Index Fund Investing

- April 25, 2016: Tax Free Municipal Bond Funds & Portfolios

- April 18, 2016: Asset Class Trend Review

- April 11, 2016: Construction of Sound And Conservative Portfolios

- March 28, 2016: Total Return Bond ETFs Review

- March 21, 2016: Small And Large Company Stock Performance In Different Economic Expansion Cycles

- March 14, 2016: Are Tactical And Timing Strategies Losing Steam?

- March 7, 2016: Defined Maturity Bond Fund Analysis

- February 29, 2016: Smart Strategic Asset Allocation Rebalance When Market Trend Changes

- February 22, 2016: Be Cash Smart

- February 15, 2016: Bond ETF Portfolios

- February 8, 2016: Newsletter Collection Update

- February 1, 2016: Total Return Bond Fund Portfolios In A Volatile Period

- January 25, 2016: Alternative Portfolios Review

- January 18, 2016: Strategic Asset Allocation: A Cautious Outlook

- January 11, 2016: Review Of Trend Following Tactical Asset Allocation

- January 4, 2016: What Worked And Didn’t In 2015

- December 21, 2015: Distressed Assets

- December 14, 2015: High Yield Bonds And Their Correlation With Stocks

- December 7, 2015: Diversification And Global Allocation

- November 30, 2015: Investors and Speculators Combined

- November 23, 2015: Active Stock Fund Performance Consistency

- November 16, 2015: Permanent, Risk Parity And Alternative Portfolios Review

- November 9, 2015: Broad Base Core Mutual Fund Review

- November 2, 2015: Broad Base Index Core ETFs Review

- October 26, 2015: Total Return Bond Fund Review

- October 19, 2015: Advanced Portfolio Review

- October 12, 2015: What About Commodities?

- October 5, 2015: Core Satellite Portfolios In A 401k Account

- September 28, 2015: Risk Managed Strategic Asset Allocation Portfolios Revisited

- September 21, 2015: Quest For The Best Investment Strategy

- September 14, 2015: Core Satellite Portfolios In Market Turmoil

- September 7, 2015: Market Rout Creates An Opportunity to Reposition Your Portfolios

- August 31, 2015: Review of Asset Allocation Funds and Portfolios

- August 24, 2015: Market Rout And Your Portfolios

- August 17, 2015: ETF or Mutual Fund Based Portfolios

- August 10, 2015: Updated Newsletter Collection

- August 3, 2015: Slippery Asset Trends

- July 27, 2015: Performance Dispersion Among Momentum Based Portfolios

- July 20, 2015: Global Balanced Portfolio Benchmarks

- July 13, 2015: Pain in Tactical Portfolios

- July 6, 2015: Fixed Income Total Return Bond Funds In Strategic Asset Allocation Portfolios

- June 29, 2015: Core ETF Commission Free Portfolios

- June 22, 2015: Secular Asset Trends

- June 15, 2015: Giving Up Bonds?

- June 1, 2015: Summer Blues?

- May 26, 2015: Cash, Bonds and Stocks In A Rising Rate Environment

- May 18, 2015: Portfolio Update

- May 11, 2015: Pain in Fixed Income?

- May 4, 2015: The Balanced Stock and Long Term Treasury Bond Portfolios

- April 27, 2015: Long Term Treasury Bond Behavior

- April 20, 2015: 529 College Savings Plan Rebalance Policy Change

- April 13, 2015: Total Return Bond Funds As Smart Cash

- April 6, 2015: The Low Return Environment

- March 30, 2015: Brokerage Specific Core Mutual Fund Portfolios 2

- March 23, 2015: Investment Arithmetic for Long Term Investments

- March 16, 2015: Brokerage Specific Core Mutual Fund Portfolios

- March 9, 2015: Newsletter Collection Update

- March 2, 2015: Total Return Bond ETFs

- February 23, 2015: Why Is Global Tactical Asset Allocation Not Popular?

- February 16, 2015: Where Are Permanent Portfolios Going?

- February 9, 2015: How Have Asset Allocation Funds Done?

- February 2, 2015: Risk Management Everywhere

- January 26, 2015: Composite Portfolios Review

- January 19, 2015: Fixed Income Investing Review

- January 12, 2015: How Does Trend Following Tactical Asset Allocation Strategy Deliver Returns

- January 5, 2015: When Forecast Fails

- December 22, 2014: Long Term Asset Returns: How Long Is Long?

- December 15, 2014: Beaten Down Assets

- December 8, 2014: Implementing Core Asset Portfolios In a Brokerage

- December 1, 2014: Two Key Issues of Investment Strategies

- November 24, 2014: Holiday Readings

- November 17, 2014: Retirement Spending Portfolios Update

- November 10, 2014: Fixed Income Or Cash

- November 3, 2014: Asset Trend Review

- October 27, 2014: Investment Loss, Mistakes And Market Cycles

- October 20, 2014: Strategic Portfolios With Managed Volatility

- October 13, 2014: Embrace Volatility

- October 6, 2014: Tips For 401k Open Enrollment

- September 29, 2014: What Can We Learn From Bill Gross’ Departure From PIMCO?

- September 22, 2014: Why Total Return Bond Funds?

- September 15, 2014: Equity And Total Return Bond Fund Composite Portfolios

- September 8, 2014: Momentum Based Portfolios Review

- September 1, 2014: Risk & Diversification: Mint.com Interview

- August 25, 2014: Remember Risk

- August 18, 2014: Consistency, The Most Important Edge In Investing: Tactical Case

- August 11, 2014: What To Do In Overvalued Stock Markets

- August 4, 2014: Is This The Peak Or Correction?

- July 28, 2014: Stock Musings

- July 21, 2014: Permanent Portfolios & Four Pillar Foundation Based Framework

- July 14, 2014: Composite Portfolios Review

- July 7, 2014: Portfolio Behavior During Market Corrections

- June 30, 2014: Half Year Brokerage ETF and Mutual Fund Portfolios Review

- June 23, 2014: Newsletter Collection Update

- June 16, 2014: There Are Always Lottery Winners

- June 9, 2014: The Arithmetic of Investment Mistakes

- June 2, 2014: Tips On Portfolio Rebalance

- May 26, 2014: In Praise Of Low Cost Core Asset Class Based Portfolios

- May 19, 2014: Consistency, The Most Important Edge In Investing: Strategic Case

- May 12, 2014: How To Handle An Elevated Overvalued Market

- May 5, 2014: Asset Allocation Funds Review

- April 28, 2014: Now The Economy Backs To The ‘Old Normal’, Should Our Investments Too?

- April 21, 2014: Total Return Bond Investing In The Current Market Environment